Which of the following is not an example of a change in accounting principle?

a. A change in the useful life of a depreciable asset.

b. A change from LIFO to FIFO for inventory costing.

c. A change to the full costing method in the extractive industries.

d. A change from the cost method to the equity method of accounting for investments.

Red Onion Restaurant would classify a six-month prepaid insurance policy as:

a. Property, plant, and equipment.

b. Investment.

c. Current asset.

d. Goodwill.

Z Co. filed suit against W Inc. in 2016 seeking damages for patent infringement. At

December 31, 2016, legal counsel for Z believed that it was probable that Z would be

successful against W for an estimated amount in the range of $30 million to $60

million, with each amount in that range considered equally likely. Z was awarded $40

million in April 2017. Z should report this award in its 2016 financial statements, issued

in March 2017 as:

a. A receivable and deferred revenue of $40 million.

b. A receivable and revenue of $40 million.

c. A disclosure of a gain contingency of $40 million.

d. A disclosure of a gain contingency of an undetermined amount in the range of $30

million to $60 million.

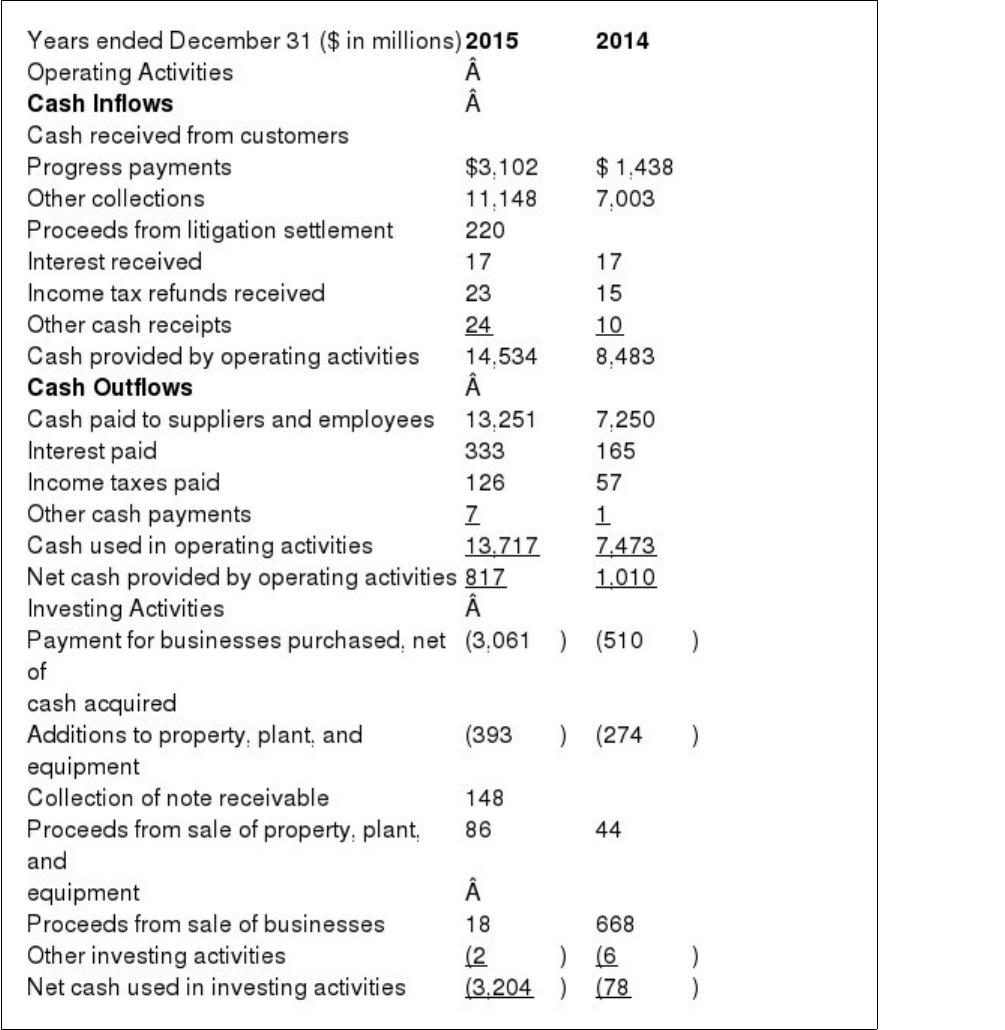

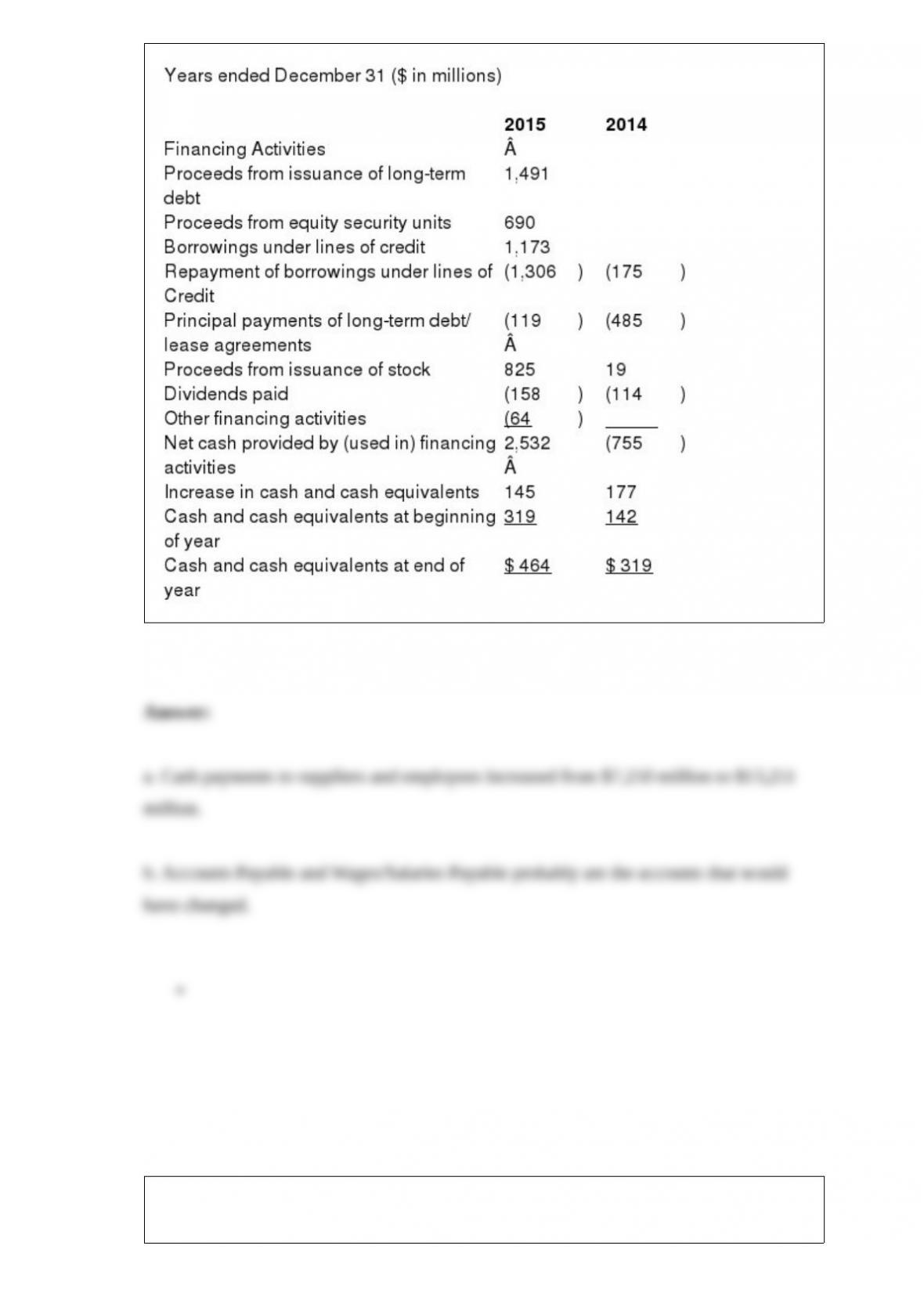

(a.) What is the most significant change in operating cash outflow activity in 2015

relative to

2014?

(b.) What balance sheet accounts would likely have changed during 2015 in relation to

the

cash flow change that you identify in (a)?

In its 2015 Annual Report to Shareholders, Henchman & Co. provided the following

Statement of Cash Flows:

Francisco leased equipment from Julio on December 31, 2016. The lease is a 10-year

lease with annual payments of $150,000 due on December 31 of each year beginning

December 31, 2016. The present value of the lease is $1,020,000. Francisco’s

incremental borrowing rate is 12% for this type of lease. The implicit rate of 10% is

known by the lessee. What should be the balance in Francisco lease liability at

December 31, 2017?

a. $824,400.

b. $807,000.

c. $806,400.

d. $792,000.

Nanki Corporation purchased equipment on January 1, 2014, for $650,000. In 2014 and

2015, Nanki depreciated the asset on a straight-line basis with an estimated useful life

of eight years and a $10,000 residual value. In 2016, due to changes in technology,

Nanki revised the useful life to a total of six years with no residual value. What

depreciation would Nanki record for the year 2016 on this equipment?

a. $108,333.

b. $106,667.

c. $122,500.

d. None of these answer choices are correct.

A broadcasting company failed to make a year-end accrual of $400,000 for fines due to

a violation of FCC rules. Its tax rate is 30%. As a result of this error, net income was:

a. Unaffected.

b. Overstated by $400,000.

c. Overstated by $280,000.

d. Overstated by $120,000.

Permanent accounts would not include:

a. Cost of goods sold.

b. Inventory.

c. Current liabilities.

d. Accumulated depreciation.

Change statements include a:

a. Retained earnings statement, balance sheet, and cash flow statement.

b. Balance sheet, cash flow statement, and income statement.

c. Cash flow statement, income statement, and retained earnings statement.

d. Retained earnings statement, balance sheet, and income statement.

For a capital lease, an amount equal to the present value of the minimum lease

payments should be recorded by the lessee as a(n):

a. Asset and a liability.

b. Asset and a different amount should be recorded as a liability.

c. Liability and a different amount should be recorded as an asset.

d. Expense.

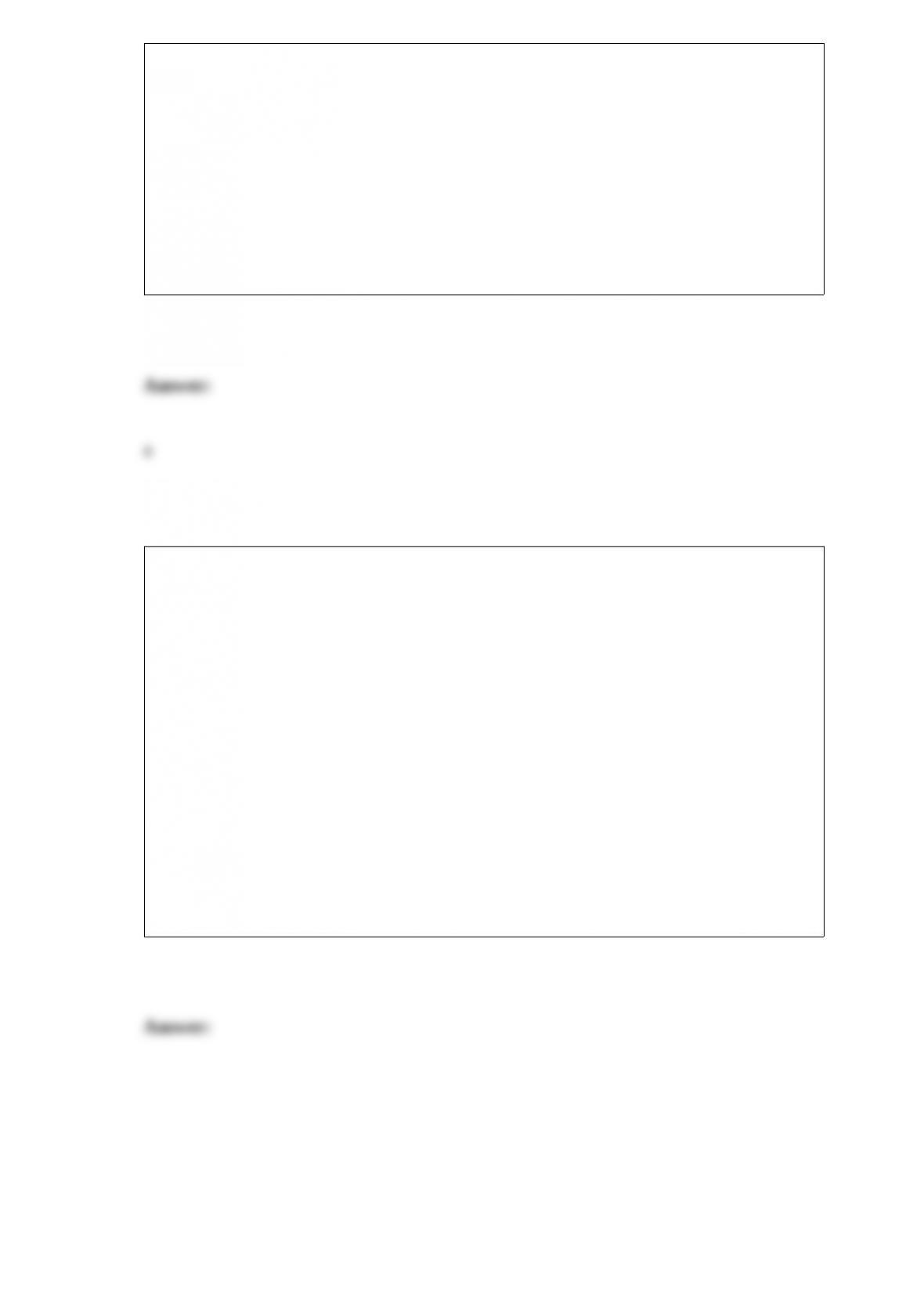

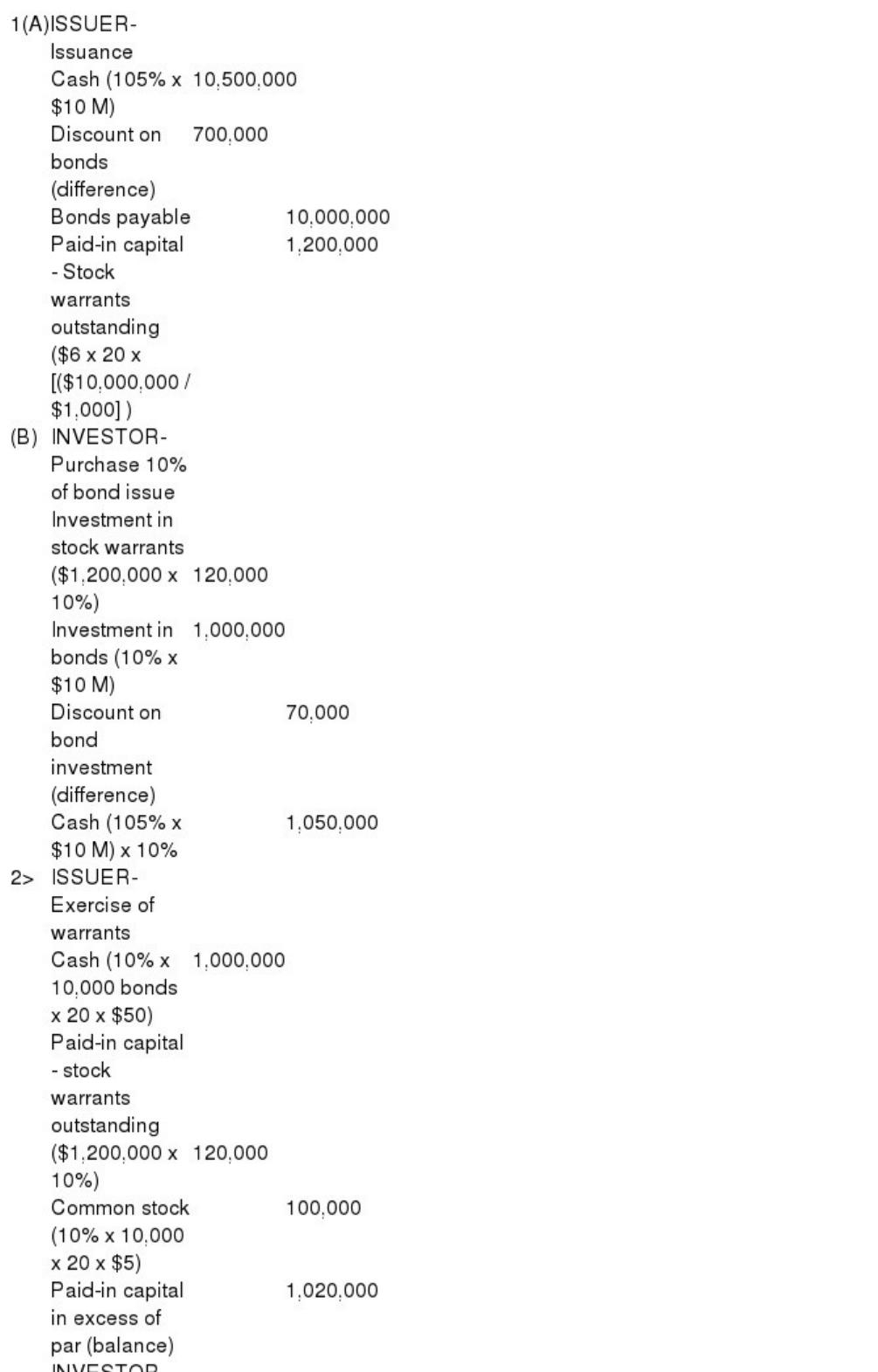

On August 1, 2017, United Corporation issued $10 million of 8% convertible bonds at

105. The bonds mature in 20 years. Each $1,000 bond was issued with 20 detachable

stock warrants, each of which entitled the bondholder to purchase, for $50, one share of

United $5 par common stock. World Company purchased 10% of the bond issue. On

August 1, 2017, the market value per share for United stock was $56 and the market

value of each warrant was $6. In March 2023, when United common stock had a market

price of $70 per share and the unamortized premium balance was $300,000, World

exercised the warrants it held.

Required:

1> Prepare the journal entries on August 1, 2017, to record (A) the issuance of the

bonds by United and (B) the investment by World.

2> Prepare the journal entries for both companies in March 2023 to record the exercise

of the warrants.

When an equipment dealer receives a long-term note in exchange for equipment, and

the stated rate of interest is indicative of the market rate of interest at the time of the

transaction, the present value of the future cash flows received on the notes:

a. Is treated as a current liability at the exchange date.

b. Is recorded as interest revenue at the exchange date.

c. Is recorded as interest receivable at the exchange date.

d. Is credited to sales revenue at the exchange date.

Which of the following statements is true when dividends are not declared or paid on

cumulative preferred stock?

a. The shareholders must be allowed to convert their shares to common stock.

b. The unpaid dividends are accrued as a liability.

c. The unpaid dividends are reported in a note to the financial statements.

d. The unpaid dividends accrue interest until paid.

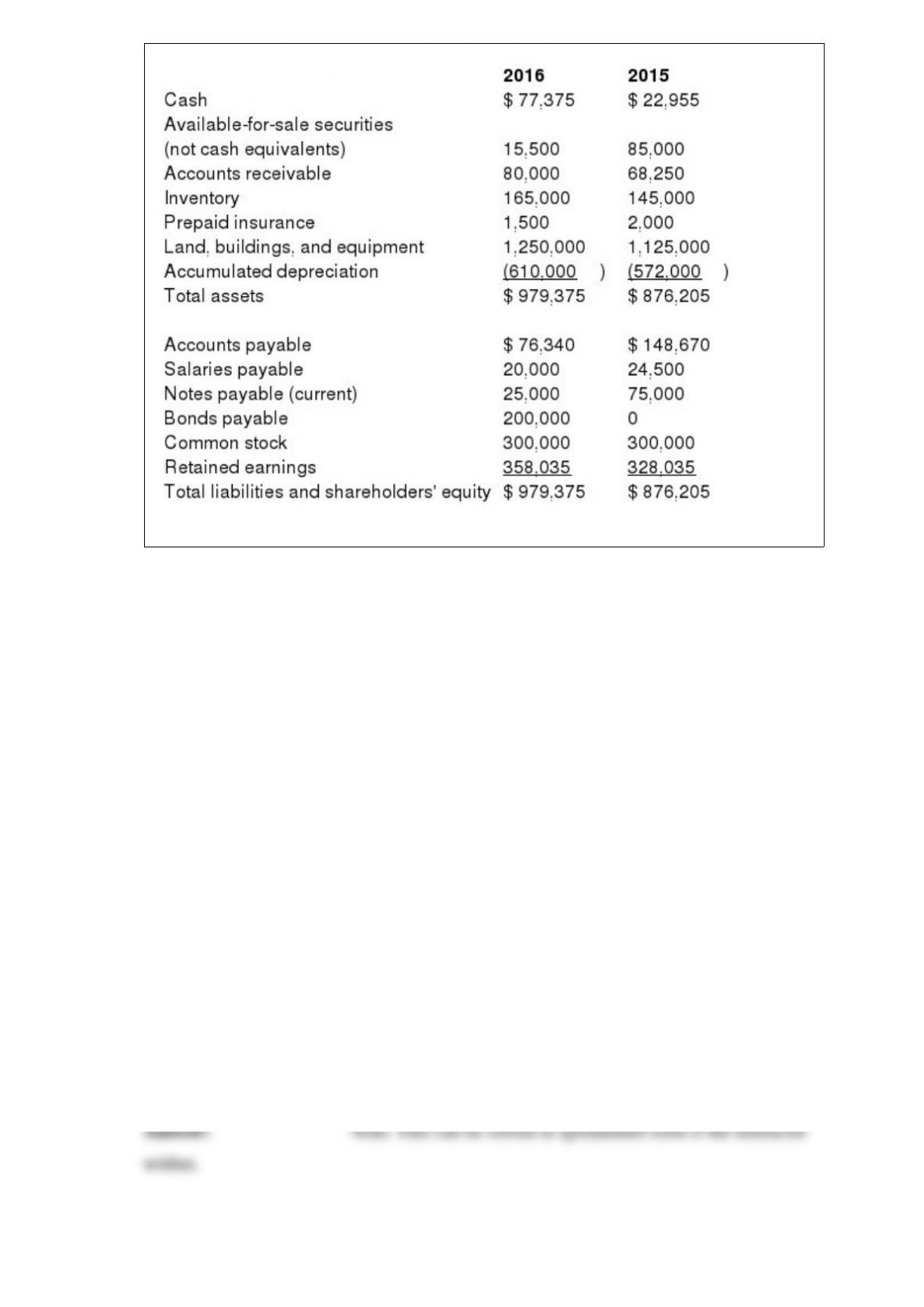

The Murdock Corporation reported the following balance sheet data for 2016 and 2015:

Additional information for 2016:

•Sold available-for-sale securities costing $69,500 for $74,000.

•Equipment costing $20,000 with a book value of $5,000 was sold for $6,000.

•Issued 6% bonds payable at face value, $200,000.

•Purchased new equipment for $145,000 cash.

•Paid cash dividends of $20,000.

•Net income was $50,000.

•

Required:

Prepare a statement of cash flows for 2016 in good form using the indirect method

for cash flows from operating activities.

MullerB Company’s employees earn vacation time at the rate of 1 hour per 40-hour

work period. The vacation pay vests immediately, meaning an employee is entitled to

the pay even if employment terminates. During 2016, total wages paid to employees

equaled $808,000, including $8,000 for vacations actually taken in 2016, but not

including vacations related to 2016 that will be taken in 2017. All vacations earned

before 2016 were taken before January 1, 2016. No accrual entries have been made for

the vacations. Required:

Prepare the appropriate adjusting entry for vacations earned but not taken in 2016.

Describe in detail the way companies report most voluntary changes in accounting

principle.

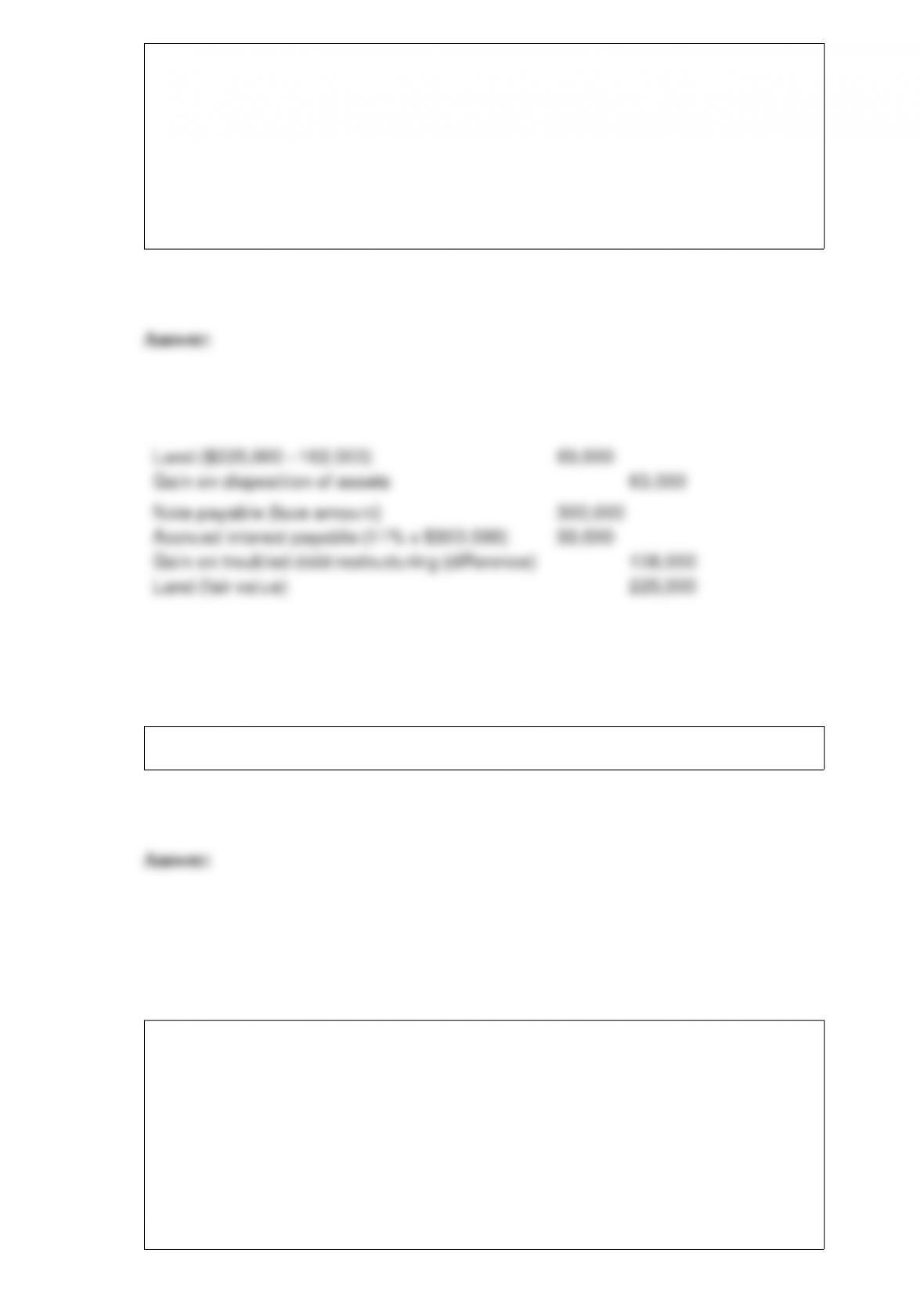

At January 1, 2016, TD owed First Bank $300,000, under an 11% note with three years

remaining to maturity. Due to financial difficulties, TD was unable to pay the previous

year’s interest. First Bank agreed to settle TD’s debt in exchange for land having a fair

value of $225,000. TD purchased the land in 2012 for $162,000.

Required:

Prepare the journal entry(s) to record the restructuring of the debt by TD.

()

2015: Net Income would be reduced by $10,000 due to the net unrealized holding loss

on trading securities on companies A, B, and C.

2016: Net Income would be increased by $2,000 due to the net unrealized holding gain

on trading securities on companies A, B, and C.

The holding gains and losses on the securities available for sale are reported as a

separate component of shareholders’ equity in the balance sheet and do not affect the

income statement.

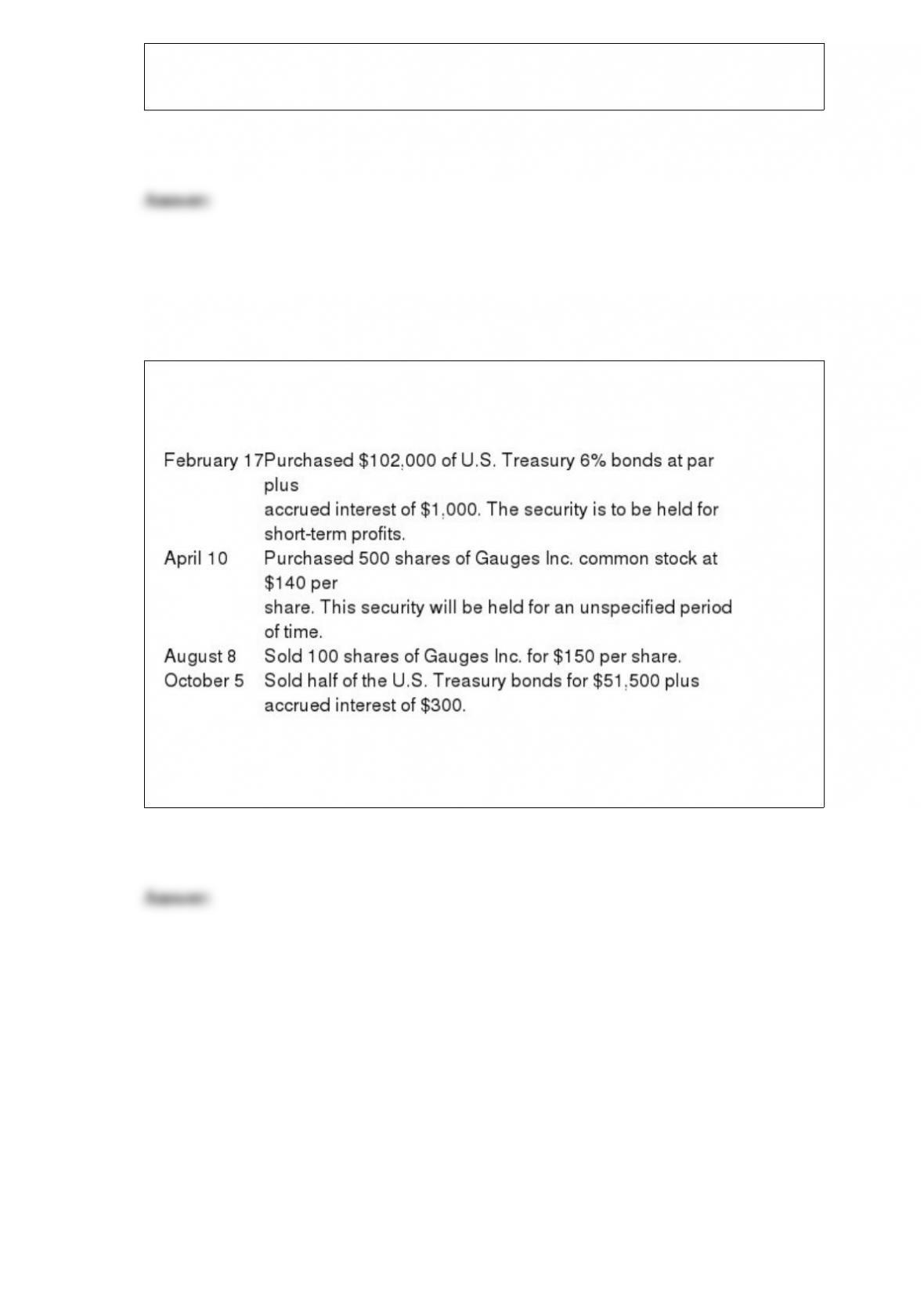

Bentz Corporation bought and sold several securities during 2016. Listed below is a

summary of the transactions:

Required:

Prepare the journal entries for the above transactions. Show calculations.