1) Stockholders’ equity consists of paid-in capital and retained earnings.

2) The series of activities that add value to a company’s products or services is called a

value chain.

3) When partners invest in a partnership, their capital accounts are credited for the

amount invested.

4) The primary objective of financial accounting is to provide general purpose financial

statements to help external users analyze and interpret an organization’s activities.

5) If the exchange rate for Canadian and U.S. dollars is 0.7382 to 1, this implies that 2

Canadian dollars will buy 1.48 worth of U.S. dollars.

6) A noncash investing transaction should be disclosed in either a footnote or at the

bottom of the statement of cash flows.

7) When using the allowance method of accounting for uncollectible accounts, the entry

to record the bad debts expense is a debit to Bad Debts Expense and a credit to

Accounts Receivable.

8) Evaluation of the performance of a department involves only financial measures.

9) The percent of sales method of estimating bad debts is focused more on realizable

value of accounts receivable than matching.

10) The petty cash fund should be reimbursed when it is nearing zero and at the end of

the accounting period when financial statements are prepared.

11) Direct costs in process cost accounting include only those costs that can be readily

identified with individual product units.

12) When preparing the operating activities section of the statement of cash flows using

the indirect method, an increase in income taxes payable is added to net income.

13) As the level of output activity increases, the variable cost per unit remains constant.

14) The monetary unit assumption means that all international transactions must be

expressed in dollars.

15) The cost of partially completed products is included in the balance of the Goods in

Process Inventory account.

16) Scatter diagrams plot volume on the vertical axis and cost on the horizontal axis.

17) A company sells computers at a selling price of $1,800 each. Each computer has a 2

year warranty that covers replacement of defective parts. It is estimated that 2% of all

computers sold will be returned under the warranty at an average cost of $150 each.

During November, the company sold 30,000 computers, and 400 computers were

serviced under the warranty at a total cost of $55,000. The balance in the Estimated

Warranty Liability account at November 1 was $29,000. What is the company’s

warranty expense for the month of November?

A.$26,000

B.$45,000

C.$55,000

D.$60,000

E.$90,000

18) Of the following, which one affects cash during a period?

A.The declaration of a stock dividend

B.Writing off an uncollectible account receivable

C.The declaration of a cash dividend

D.An adjusting entry recognizing the expiration of prepaid insurance

E.The payment of interest expense accrued in a previous accounting period

19) Uncertainties such as natural disasters:

A.Are not contingent liabilities because they are future events not arising from past

transactions or events

B.Are contingent liabilities because they are future events arising from past transactions

or events

C.Should be disclosed because of their usefulness to financial statements

D.Are estimated liabilities because the amounts are uncertain

E.Arise out of transactions such as debt guarantees

20) On September 30, the Cash account of Value Company had a normal balance of

$5,000. During September, the account was debited for a total of $12,200 and credited

for a total of $11,500. What was the balance in the Cash account at the beginning of

September?

A.A $0 balance

B.A $4,300 debit balance

C.A $4,300 credit balance

D.A $5,700 debit balance

E.A $5,700 credit balance

21) Long-term investments in held-to-maturity debt securities are accounted for using

the:

A.Fair value method with fair value adjustment to income

B.Fair value method with fair value adjustment to equity

C.Cost method with amortization

D.Cost method without amortization

E.Equity method

22) When standard manufacturing costs are recorded in the accounts and the cost

variances are immaterial at the end of the accounting period, the cost variances should

be:

A.Carried forward to the next accounting period

B.Allocated between cost of goods sold, finished goods, and goods in process

C.Closed to cost of goods sold

D.Written off as a selling expense

E.Ignored

23) Andrea Conaway opened Wonderland Photography on January 1 of the current year.

During January, the following transactions occurred and were recorded in the

company’s books:

1>Conaway invested $13,500 cash in the business.

2> Conaway contributed $20,000 of photography equipment to the business.

3> The company paid $2,100 cash for an insurance policy covering the next 24 months.

4> The company received $5,700 cash for services provided during January.

5> The company purchased $6,200 of office equipment on credit.

6> The company provided $2,750 of services to customers on account.

7> The company paid cash of $1,500 for monthly rent.

8> The company paid $3,100 on the office equipment purchased in transaction #5

above.

9> Paid $275 cash for January utilities.

Based on this information, the balance in the Andrea Conaway, Capital account

reported on the Statement of Owner’s Equity at the end of the month would be:

A.$31,400

B.$39,200

C.$31,150

D.$40,175

E.$30,875

24) At the end of the day, the cash register’s record shows $1,250, but the count of cash

in the cash register is $1,245. The correct entry to record the cash sales is

A.Debit Cash $1,245; Credit Sales $1,245

B.Debit Cash $1,245; debit Cash Over and Short $5; credit Sales $1,250

C.Debit Cash $1,250; credit Sales $1,250

D.Debit Cash $1,250; credit Sales $1,245, credit Cash Over and Short $5

E.Debit Cash Over and Short $5, credit Sales $5

25) Sales taxes payable:

A.Is an estimated liability

B.Is a contingent liability

C.Is a current liability for retailers

D.Is a business expense

E.Is a long-term liability

26) Obligations due to be paid within one year or the company’s operating cycle,

whichever is longer, are:

A.Current assets

B.Current liabilities

C.Earned revenues

D.Operating cycle liabilities

E.Bills

27) The gross margin ratio:

A.Is also called the net profit ratio.

B.Measures a merchandising firm’s ability to earn a profit from the sale of inventory.

C.Is also called the profit margin.

D.Is a measure of liquidity.

E.Should be greater than 1.

28) Baker Company’s sales mix is 3 units of A, 2 units of B, and 1 unit of C. Selling

prices for each product are $20, $30, and $40, respectively. Variable costs per unit are

$12, $18, and $24, respectively. Fixed costs are $320,000. What is the break-even point

in composite units?

A.1,111

B.1,600

C.2,666

D.4,000

E.5,000

29) A discount on bonds payable:

A.Occurs when a company issues bonds with a contract rate less than the market rate

B.Occurs when a company issues bonds with a contract rate more than the market rate

C.Increases the Bond Payable account

D.Decreases the total bond interest expense

E.Is not allowed in many states to protect creditors

30) In a process operation, the direct labor of a production department includes:

A.All labor used exclusively by that department, even if the labor is not applied to the

product itself

B.All labor used exclusively by that department, but only if the labor is applied to the

product itself

C.All labor for that department, including labor for services that help more than one

production department, such as clerical, repair, and computer technicians

D.Only labor that helps more than one production department, such as clerical, repair,

and computer technicians

E.Only that labor that is recorded in the Factory Payroll account

31) At the end of June, the job cost sheets for Monson Manufacturing show the

following total costs accumulated on three custom jobs.

Job 203 was started in production in May and the following costs were assigned to it in

May: direct materials, $12,000; direct labor, $6,000; and overhead $8,700. Jobs 204 and

205 are started in June. Overhead cost is applied with a predetermined rate based on

direct labor cost. Jobs 203 and 204 are finished in June, and Job 205 will be finished in

July. No raw materials are used indirectly in June. Using this information, answer the

following questions assuming the company’s predetermined overhead rate did not

change.

a. What is the cost of the raw materials requisitioned in June for each of the three jobs?

b. How much direct labor cost is incurred during June for each of the three jobs?

c. What predetermined overhead rate is used during June?

d. How much total cost is transferred to finished goods during June?

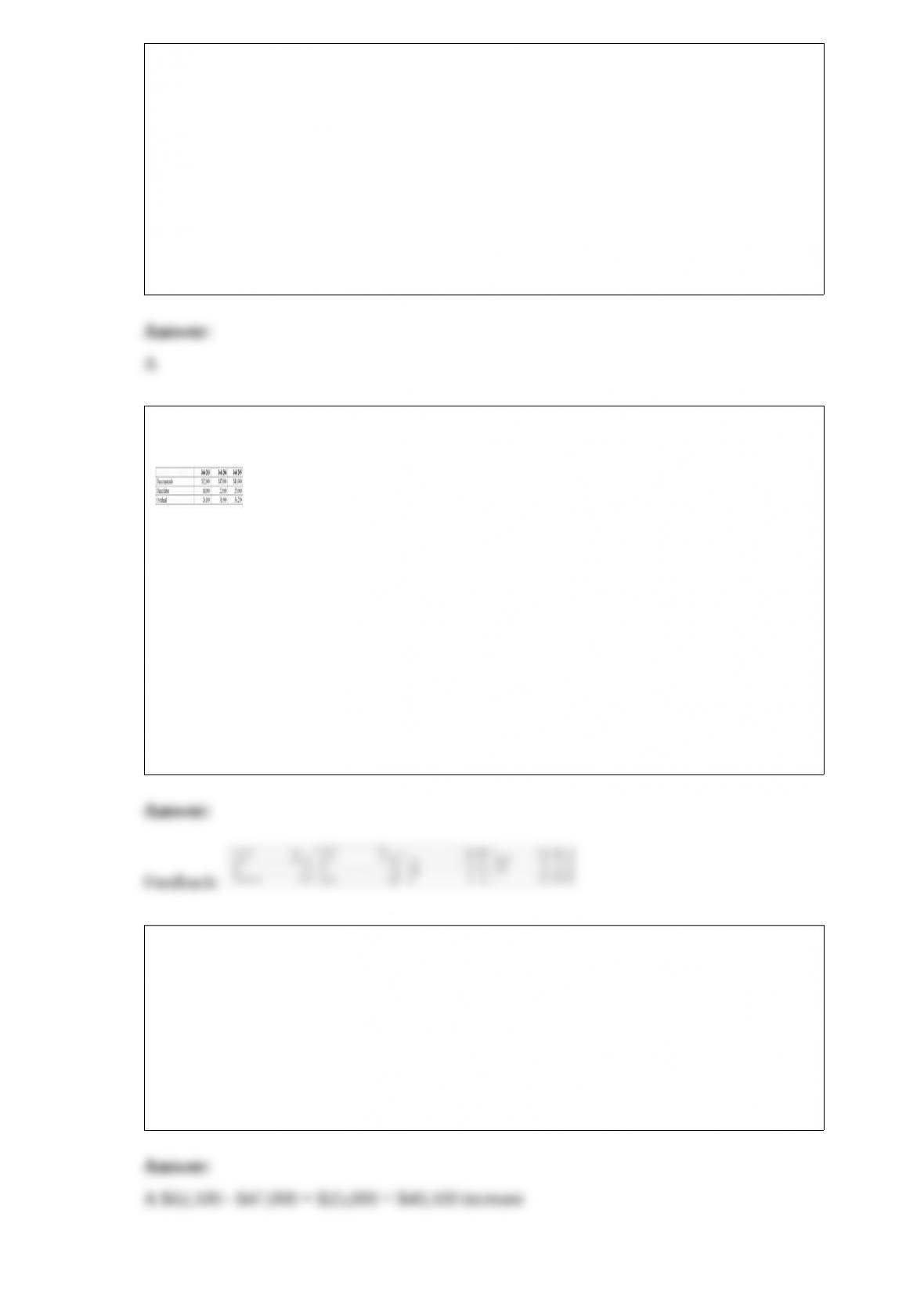

32) Flash had cash inflows from operations $62,500; cash outflows from investing

activities of $47,000; and cash inflows from financing of $25,000. The net change in

cash was:

A.$40,500 increase

B.$40,500 decrease

C.$134,500 decrease

D.$134,000 increase

E.$9,500 increase

33) All of the following statements related to recording warranty expense are True

except:

A.Recording estimated warranty expense complies with the full disclosure principle

B.Warranty expense should be recorded in the period when the warranty service is

performed

C.Recording estimated warranty expense complies with the matching principle

D.The seller reports a warranty obligation as a liability

E.Warranty costs are probable and the amount can be estimated

34) On November 1, Jay Company loaned an affiliate $100,000 at a 9.0% interest rate.

The note receivable plus interest will not be collected until March 1 of the following

year. The company’s annual accounting period ends on December 31. The adjusting

entry needed on December 31 is:

A.Debit Interest Receivable, $750; credit Interest Revenue, $750

B.Debit Interest Expense, $750; credit Interest Payable, $750

C.Debit Interest Expense, $1,500; credit Interest Payable, $1,500

D.Debit Interest Receivable, $2,250; credit Interest Revenue, $2,250

E.Debit Interest Receivable, $1,500; credit Interest Revenue, $1,500

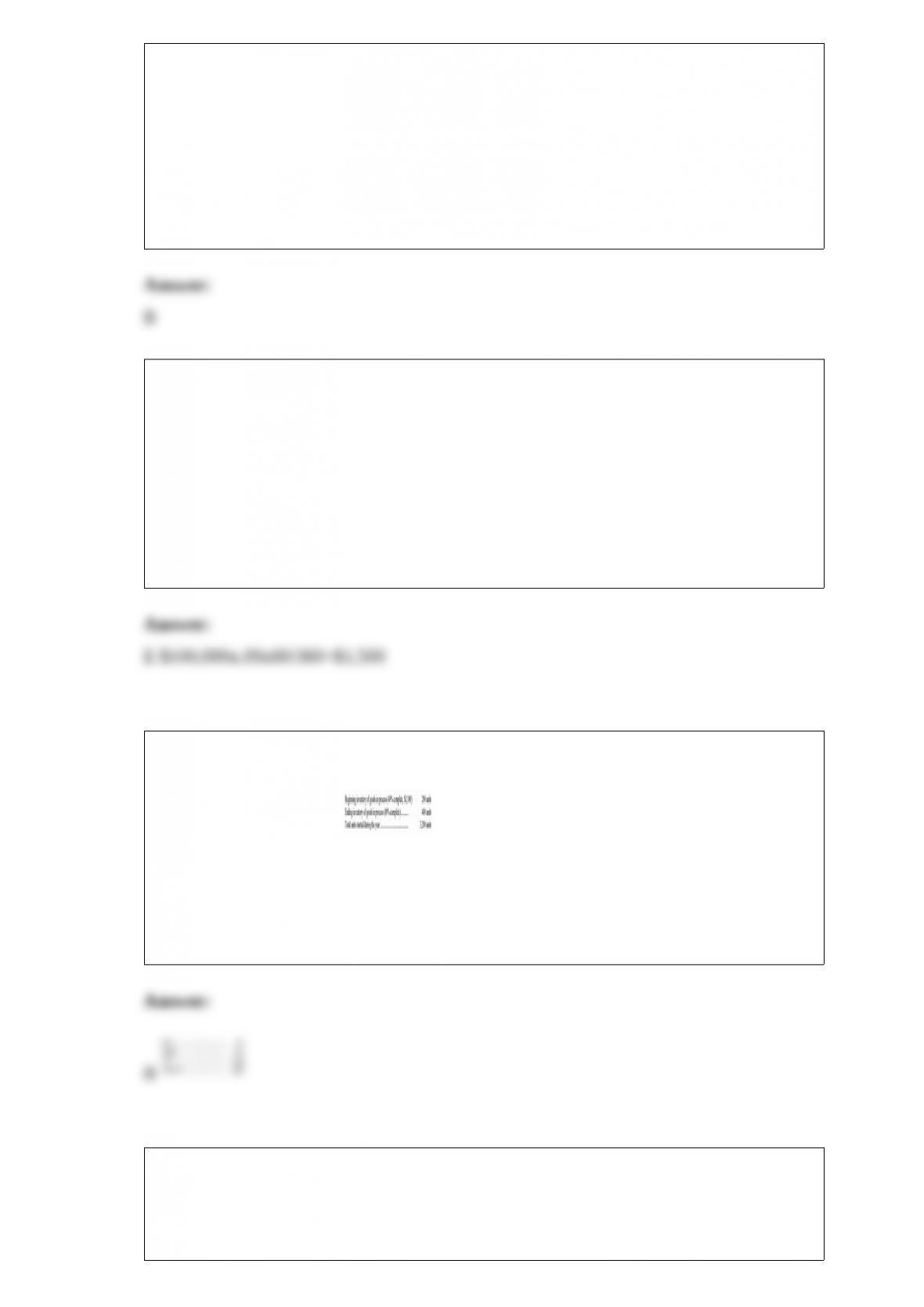

35) Medina Corp. uses the weighted average method for inventory costs and had the

following information available for the year. The number of units transferred to finished

goods during the year is:

A.3,200 units

B.3,000 units

C.3,400 units

D.3,160 units

E.3,500 units

36) At acquisition, debt securities are:

A.Recorded at their cost, plus total interest that will be paid over the life of the security

B.Recorded at the amount of interest that will be paid over the life of the security

C.Recorded at cost

D.Not recorded, because no interest is due yet

E.Recorded at cost plus the amount of dividend income to be received

37) Which of the following statements is incorrect?

A.Permanent accounts is another name for nominal accounts

B.Temporary accounts carry a zero balance at the beginning of each accounting period

C.The Income Summary account is a temporary account

D.Real accounts remain open as long as the asset, liability, or equity items recorded in

the accounts continue in existence

E.The closing process applies only to temporary accounts

38) The current ratio:

A.Is used to measure a company’s profitability

B.Is used to measure the relation between assets and long-term debt

C.Measures the effect of operating income on profit

D.Is used to help evaluate a company’s ability to pay its debts in the near future

E.Is calculated by dividing current assets by equity

39) Match the following definitions with terms 1 through 8. Place the letter that

identifies the best definition in the blank space next to the term.

1>Assets an owner takes from the company for personal use A. Assets

2>A principle that requires the information in financial statements to be supported by

independent unbiased evidence B. Going-concern principle

3>A principle that requires financial statements to reflect the assumption that the

business will continue operating instead of being closed or sold. C. Statement of

owner’s equity.

4>The accounting principle that requires assets and services to be recorded initially at

the cash or cash-equivalent amount given in exchange D. Net assets

5>A financial statement that reports the changes in equity over the reporting period;

including increases such as owner investment and net income and for decreases such as

owner withdrawals or net loss E. Objectivity principle

6>Resources owned or controlled by a company that are expected to yield future

benefits F. Cost principle

7>Another term for equity G. Owner withdrawal

8>Gross increase in equity from a company’s earnings activities H. Revenues

40) Intangible assets include:

A.Patents

B.Copyrights

C.Trademarks

D.Goodwill

E.All of these

41) Flash has beginning equity of $257,000, net income of $51,000, withdrawals of

$40,000 and investments by owners of $6,000. Its ending equity is:

A.$223,000

B.$240,000

C.$268,000

D.$274,000

E.$208,000

42) Viscount Company collected $42,000 cash on its accounts receivable. The effects of

this transaction as reflected in the accounting equation are:

A.Total assets decrease and equity increases

B.Both total assets and total liabilities decrease

C.Total assets, total liabilities, and equity are unchanged

D.Both total assets and equity are unchanged and liabilities increase

E.Total assets increase and equity decreases

43) A company paid $0.75 in cash dividends per share. Its earnings per share is $3.50,

and its market price per share is $37.50. Its dividend yield equals:

A.4.7%

B.2.0%

C.9.3%

D.21.4%

E.46.7%

44) Describe the purpose of horizontal financial statement analysis and how it is

applied.

45) During the current year ended December 31, clients paid fees in advance for

accounting services amounting to $25,000. These fees were recorded in an account

called Unearned Accounting Fees. If $3,500 of these fees remain unearned on

December 31 of this year present the December 31 adjusting entry to bring the accounts

up to date.

46) On January 1, the Plimpton Corporation leased some equipment on a 2-year lease,

paying $15,000 per year each December 31. The lease is considered to be an operating

lease. Prepare the general journal entry to record the first lease payment on December

31.

47) Golden Age Co. exports Native American artwork to Japan. Prepare journal entries

for the following transactions.

48) Express the following balance sheets for Alberts Company in common-size

percents.

49) A company made the following merchandise purchases and sales during the month

of May:

There was no beginning inventory. If the company uses the weighted average periodic

method, what would be the cost of the ending inventory?

50) Identify each of the following items would likely serve as a source document by

marking an X in the appropriate column. The first one is done as an example

51) Revenues, expenses, withdrawals, and Income Summary are called

_________________ accounts because they are closed at the end of each accounting

period.