On January 1, 2016, Green Corporation purchased 20% of the outstanding voting

common stock of Gold Company for $300,000. The book value of the acquired shares

was $275,000. The excess of cost over book value is attributable to an intangible asset

on Gold’s books that was undervalued and had a remaining useful life of five years. For

the year ended December 31, 2016, Gold reported net income of $125,000 and paid

cash dividends of $25,000. What is the carrying value of Green’s investment in Gold at

December 31, 2016?

a. $295,000.

b. $300,000.

c. $315,000.

d. $320,000.

Which of the following statements is not true regarding the correction of an error?

a. The correction is reported prospectively and previous financial statements are not

revised.

b. A journal entry is needed to correct any account balances that are incorrect as a result

of the error.

c. Prior years’ financial statements are restated to reflect the correction of the error (if

the error affected those statements).

d. A disclosure note should describe the nature of the error and the impact of its

correction on net income, income before extraordinary items, and earnings per share.

When investments are treated as available-for-sale, other comprehensive income (OCI)

also includes the tax effects associated with unrealized holding gains and losses. As a

result:

a. Accumulated other comprehensive income would be increased by the tax benefits

typically associated with unrealized holding gains.

b. Other comprehensive income typically would be reduced by the tax expense

associated with unrealized holding gains.

c. Accumulated other comprehensive income would not be affected by taxes.

d. None of these answer choices is correct.

Dooling Corporation reported balances in the following accounts for the current year:

Cost of goods sold was $7,500. What was the amount of cash paid to suppliers?

a. $7,000.

b. $7,200.

c. $7,300.

d. $7,500.

Crawford Inc. has bonds outstanding during a year in which the general (risk-free) rate

of interest has risen. Crawford elected the fair value option for the bonds upon issuance.

What will the company report for the bonds in its income statement for the year?

a. Interest expense and a gain.

b. Interest expense and a loss.

c. A gain and no interest expense.

d. Interest expense and no gain or loss.

Auerbach Inc. issued 4% bonds on October 1, 2016. The bonds have a maturity date of

September 30, 2026 and a face value of $300 million. The bonds pay interest each

March 31 and September 30, beginning March 31, 2017. The effective interest rate

established by the market was 6%. Assuming that Auerbach issued the bonds for

$255,369,000, what would the company report for its net bond liability balance at

December 31, 2016, rounded up to the nearest thousand?

a. $252,369,000.

b. $256,369,000.

c. $256,200,000.

d. $257,030,070.

Research and development expense for a given period includes:

a. The full cost of newly acquired equipment that has an alternative future use.

b. Depreciation on a research and development facility.

c. Research and development conducted on a contract basis for another entity.

d. Patent filing and legal costs.

The valuation allowance account that is used in conjunction with deferred taxes relates:

a. Only to deferred tax liabilities.

b. To both deferred tax assets and liabilities.

c. Only to deferred tax assets.

d. Only to income taxes receivable due to net operating loss carrybacks.

Grossman Products began operations in 2016. The following selected transactions

occurred from September 2016 through March 2017. Grossman’s fiscal year ends on

December 31.

2016:

(a.) On September 5, Grossman opened a checking account and negotiated a short-term

line of credit of up to $10,000,000 at 10% interest. The company is not required to pay

any commitment fees.

(b.) On October 1, Grossman borrowed $8,000,000 cash and issued a 5-month

promissory note with 10% interest payable at maturity.

(c.) Grossman received $3,000 of refundable deposits in December for reusable

containers.

(d.) For the September through December period, sales totaled $5,000,000. The state

sales tax rate is 4% and 75% of sales are subject to sales tax.

(e.) Grossman recorded accrued interest.

2017:

(f.) Grossman paid the promissory note on the March 1 due date.

(g.) Half of the storage containers are returned in March, with the other half expected to

be returned over the next 6 months.

Required:

1> Prepare the appropriate journal entries for the 2016 transactions.

2> Prepare the liability section of the balance sheet at December 31, 2016, based on the

data supplied.

3> Prepare the appropriate journal entries for the 2017 transactions.

On May 1, Foxtrot Co. agreed to sell the assets of its Footwear Division to Albanese

Inc. for $80 million. The sale was completed on December 31, 2016. The following

additional facts pertain to the transaction:

– The Footwear Division qualifies as a component of the entity according to GAAP

regarding discontinued operations.

– The book value of Footwear’s assets totaled $48 million on the date of the sale.

– Footwear’s operating income was a pre-tax loss of $10 million in 2016.

– Foxtrot’s income tax rate is 40%.

Suppose that the Footwear Division’s assets had not been sold by December 31, 2016,

but were considered held for sale. Assume that the fair value of these assets at

December 31 was $80 million. In the 2016 income statement for FoxtrotCo., under

discontinued operations it would report a:

a. $ 6 million loss.

b. $ 10 million loss.

c. $13.2 million income.

d. None of the other answers is correct.

Classifying liabilities as either current or long-term helps creditors assess:

a. Profitability.

b. The relative risk of a firm’s liabilities.

c. The degree of a firm’s liabilities.

d. The amount of a firm’s liabilities.

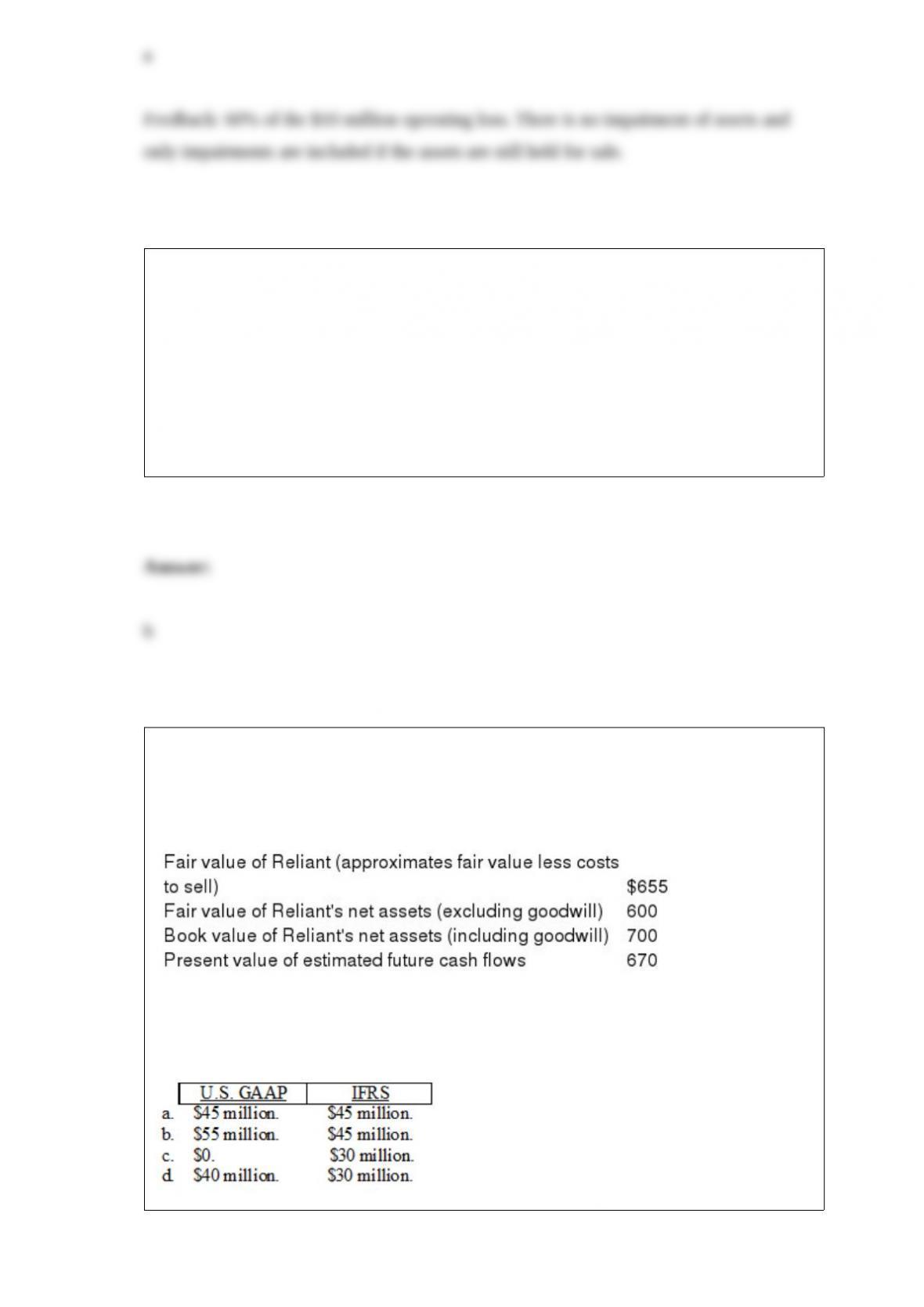

Kingston Corporation has $95 million of goodwill on its books from the 2014

acquisition of Reliant Motors. At the end of its 2016 fiscal year, management has

provided the following information for its required goodwill impairment test ($ in

millions):

Assuming that Reliant is considered a reporting unit for U.S. GAAP and a

cash-generating unit for IFRS, the amount of goodwill impairment loss that Kingston

should recognize according to U.S. GAAP and IFRS, respectively, is:

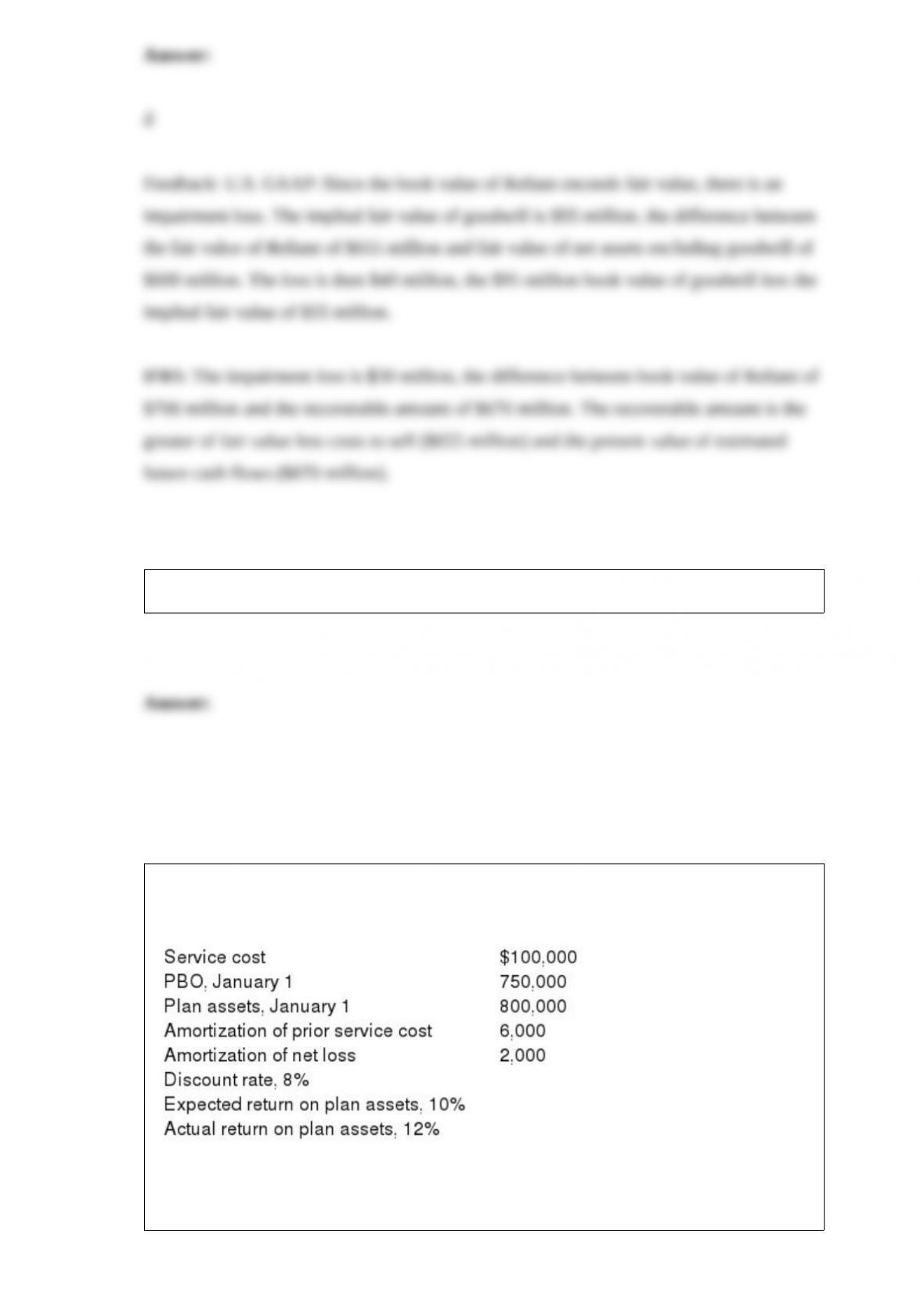

Pension data for Goldman Company included the following for the current calendar

year:

Required:

Determine pension expense for the year.

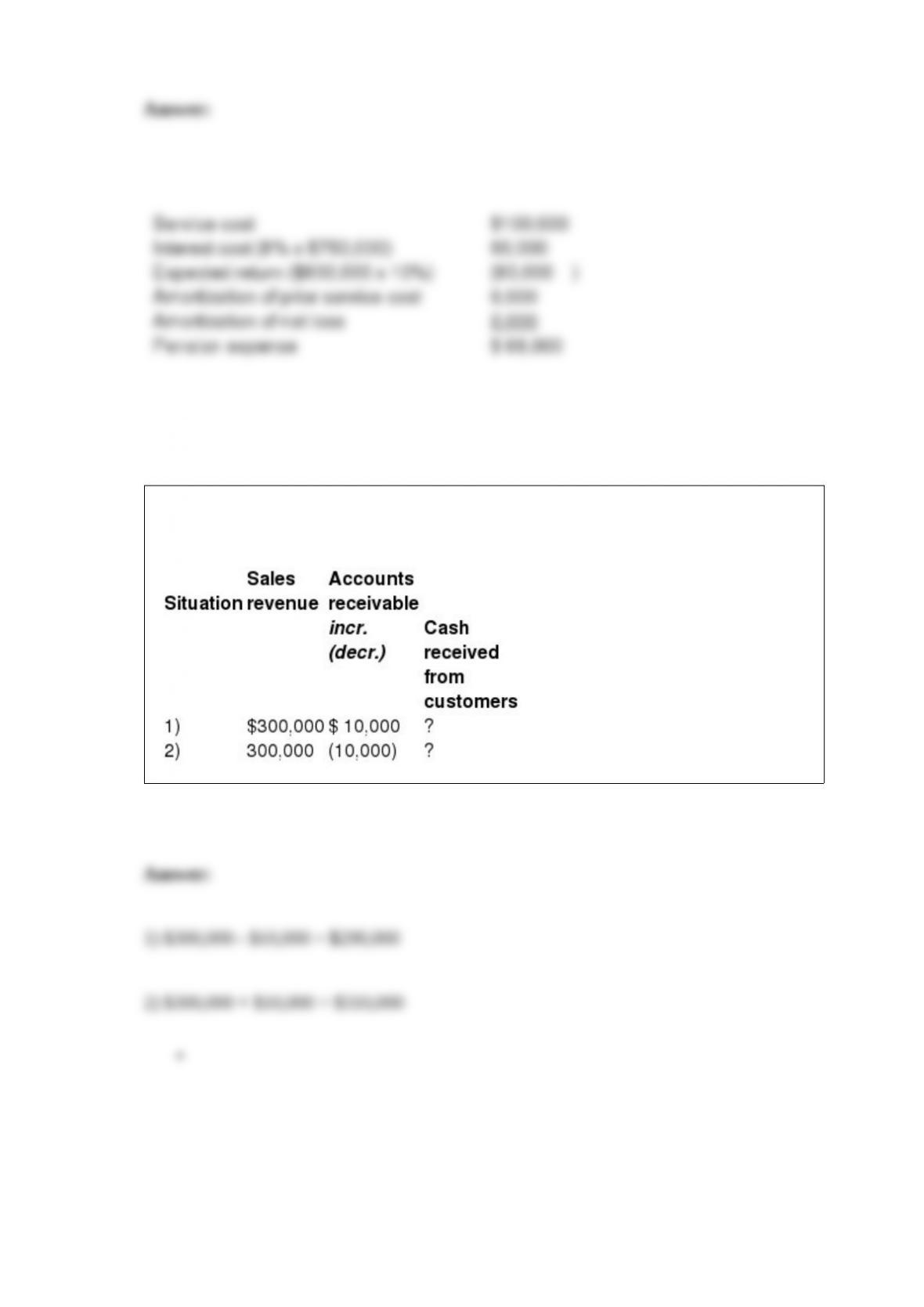

Determine the amount of cash received from customers for each of the two independent

situations below.

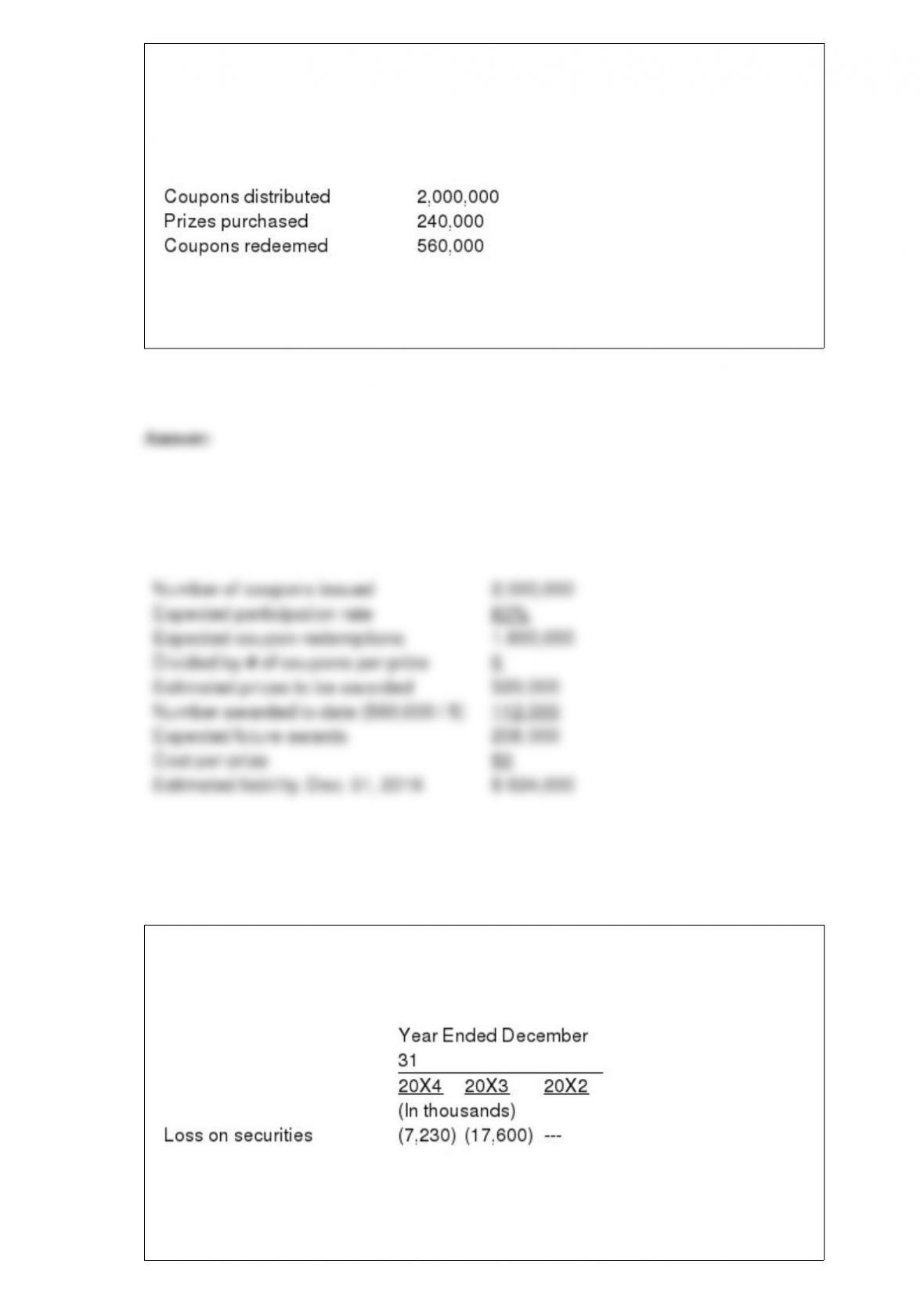

Albertson Corporation began a special promotion in July 2016 in an attempt to increase

sales. A coupon was provided at various grocery stores upon checkout. Customers could

send in five coupons for a free prize. Each prize cost Albertson Corporation $3.00.

Albertson’s management estimated that 80% of the coupons would be redeemed. For

the six months ended December 31, 2016, the following information is available:

Required:

What is the estimated liability associated with the coupons at December 31, 2016?

In its 20X4 annual report to shareholders, Maytag Corporation included the following

disclosures in its income statement and related footnotes: CONSOLIDATED

STATEMENTS OF INCOME

Special Charges and Loss on Securities

During the fourth quarter of 20X4, the Company recorded special charges and loss on

securities totaling $17.0 million, or $13.5 million after-tax. Special charges of $9.8

million, or $6.2 million after-tax, were associated with a salaried workforce reduction

of approximately 250 employees. Cash expenditures for 20X4 related to this charge

were $3.7 million. Loss on securities of $7.2 million resulted from the write-down of

the remaining investment in a privately held Internet-related company.

During the fourth quarter of 20X3, the Company recorded special charges and loss on

securities totaling $57.5 million, or $36.5 million after-tax. Special charges of $39.9

million, or $25.3 million after-tax, were associated with terminated product initiatives,

asset write-downs, and executive severance costs related to management changes. Loss

on securities of $17.6 million, or $11.2 million after-tax, resulted from a lower market

valuation of securities of TurboChef Technologies, Inc., and investments in privately

held Internet-related Companies ‘¦.. The loss on securities charge of $17.6 million was

noncash.

Required:

Discuss the possible rationale behind the losses on securities reported by Maytag in

20X3 and 20X4.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the most correct term.

The Peach Corporation provides restricted stock to certain executives. Under the plan,

the company granted 30 million shares on January 1, 2016, which vest in four years.

The fair value of the shares is $14. No forfeitures are anticipated. Ignore taxes.

Required:

1) Determine the total compensation cost pertaining to the restricted stock.

2) Prepare the appropriate journal entry (if any) to record the award of restricted stock

on January 1, 2016.

3) Prepare the appropriate journal entry (if any) to record compensation expense on

December 31, 2016.