1) Many small/local accounting firms do not perform audits as their primary services to

their clients include accounting and tax.

A) True

B) False

2) Sarbanes-Oxley requires management to issue an internal control report that includes

two specific items. Which of the following is one of these two requirements?

A) A statement that management is responsible for establishing and maintaining an

adequate internal control structure and procedures for financial reporting

B) A statement that management and the board of directors are jointly responsible for

establishing and maintaining an adequate internal control structure and procedures for

financial reporting

C) A statement that management, the board of directors, and the external auditors are

jointly responsible for establishing and maintaining an adequate internal control

structure and procedures for financial reporting

D) A statement that the external auditors are solely responsible

3) Ordinarily, if you are auditing a continuing client, it is unnecessary to test the

accuracy objective or the classification objective for fixed assets acquired in prior years.

A) True

B) False

4) Because of confidentiality requirements and potential losses of payroll funds, outside

service center systems are rarely used by companies for payroll-related functions.

A) True

B) False

5) Which of the following statements is correct?

A) A letter of representation is documentation of management’s acceptance of

responsibility for the financial statements and is deemed to be reliable evidence

B) A letter of representation is not deemed to be reliable evidence because of the

potential incompetence of management

C) A letter of representation is not deemed to be reliable evidence because of the lack of

independence of the preparers

D) A letter of representation is documentation of the CPA’s acceptance of responsibility

for the audit of the financial statement and is deemed to be reliable

6) Examples of cash equivalents include time deposits, certificates of deposit, and

marketable securities.

A) True

B) False

7) Which of the following statements is most correct with respect to separation of

duties?

A) Employees should not have temporary and permanent custody of assets

B) Employees who authorize transactions should not have custody of related assets

C) It is permissible to allow an employee to open cash receipts and record those receipts

D) Employees who authorize transactions should have recording responsibility for these

transactions

8) The acceptable risk of incorrect acceptance is most related to:

A) audit efficiency

B) audit results

C) audit effectiveness

D) audit estimation

9) If the result obtained from a particular sample for control and substantive tests of

transactions is critical to the formation of an audit opinion, which of the following is the

most important to the auditor in concluding of the appropriateness and sufficiency of

evidence gathered?

A) Acceptable risk of assessing control risk too low

B) Estimated population exception rate

C) Tolerable exception rate

D) Size of the population

10) In testing acquisitions the auditor needs to understand the appropriate accounting

guidance related to acquisition accounting. Which of the following is NOT an

accounting consideration for the auditor as regards to acquisition cost?

A) Inclusion of material transportation and installation costs

B) Recording of trade-in costs

C) Allocating costs when building and equipment are purchased at one price

D) Verifying that purchased equipment amounts correspond to the budgeted amount

11) In systematic sample selection, the population size is divided by the number of

sample items desired in order to determine the:

A) sampling interval

B) tolerable exception rate

C) computed upper exceptions rate

D) mean

12) In describing the cycle approach to segmenting an audit, which of the following

statements is not true?

A) All general ledger accounts and journals are included at least once

B) Some journals and general ledger accounts are included in more than one cycle

C) The “capital acquisition and repayment” cycle is closely related to the “acquisition of

goods and services and payment” cycle

D) The “inventory and warehousing” cycle may be audited at any time during the

engagement since it is unrelated to the other cycles

13) Auditors are not always required to obtain bank confirmations.

A) True

B) False

14) Which of the following is not correct regarding an auditor’s decision that a lower

acceptable audit risk is appropriate?

A) More evidence is accumulated

B) Less evidence is accumulated

C) Special care is required in assigning experienced staff

D) Review of audit documentation is performed by personnel not assigned to the

engagement

15) When a company has treasury stock certificates on hand, a year-end count of the

certificates by the auditor is:

A) always required

B) not required if treasury stock is a deduction from stockholders’ equity

C) required when the company classifies treasury stock with other assets

D) required when the company had treasury stock transactions during the year

16) In monetary-unit sampling, the relationship between tolerable misstatement size and

required sample size is:

A) direct

B) inverse

C) varied

D) indeterminable

17) The computer file used for recording payroll transactions for each employee and

maintaining total wages paid for the year to date is the:

A) payroll transaction file

B) payroll master file

C) payroll bank account reconciliation

D) payroll tax returns

18) Which of the following is least likely to uncover fraud?

A) External auditors

B) Internal auditors

C) Internal controls

D) Management

19) You are auditing the inventory account and are concerned about the possibility of an

inventory overstatement. What is the best audit procedure to detect damaged inventory?

A) observe the condition of inventory during the client’s physical count

B) compare the condition of inventory from the previous year’s count to the current year

C) compare inventory turnover from the previous year’s inventory to the current year’s

inventory

D) reconcile the inventory counts to the cost accounting records

20) After finishing the review phase of the study and evaluation of internal control in an

audit, the auditor should perform tests of controls on:

A) those controls that the auditor wants and plans to rely upon

B) those controls in which material weaknesses were identified

C) those controls that have a material effect upon the financial statement balances

D) a random sample of the controls that were reviewed

21) The permanent audit file would usually include the following:

A) client’s working trial balance

B) summary of the risk assessment procedures performed

C) organizational chart of the company’s employees

D) summary of the auditors test of controls for the current years audit

22) The audit procedure “Examine canceled check for authorized signature, proper

endorsement, and cancellation by the bank” is used to test the occurrence objective for

cash disbursements.

A) True

B) False

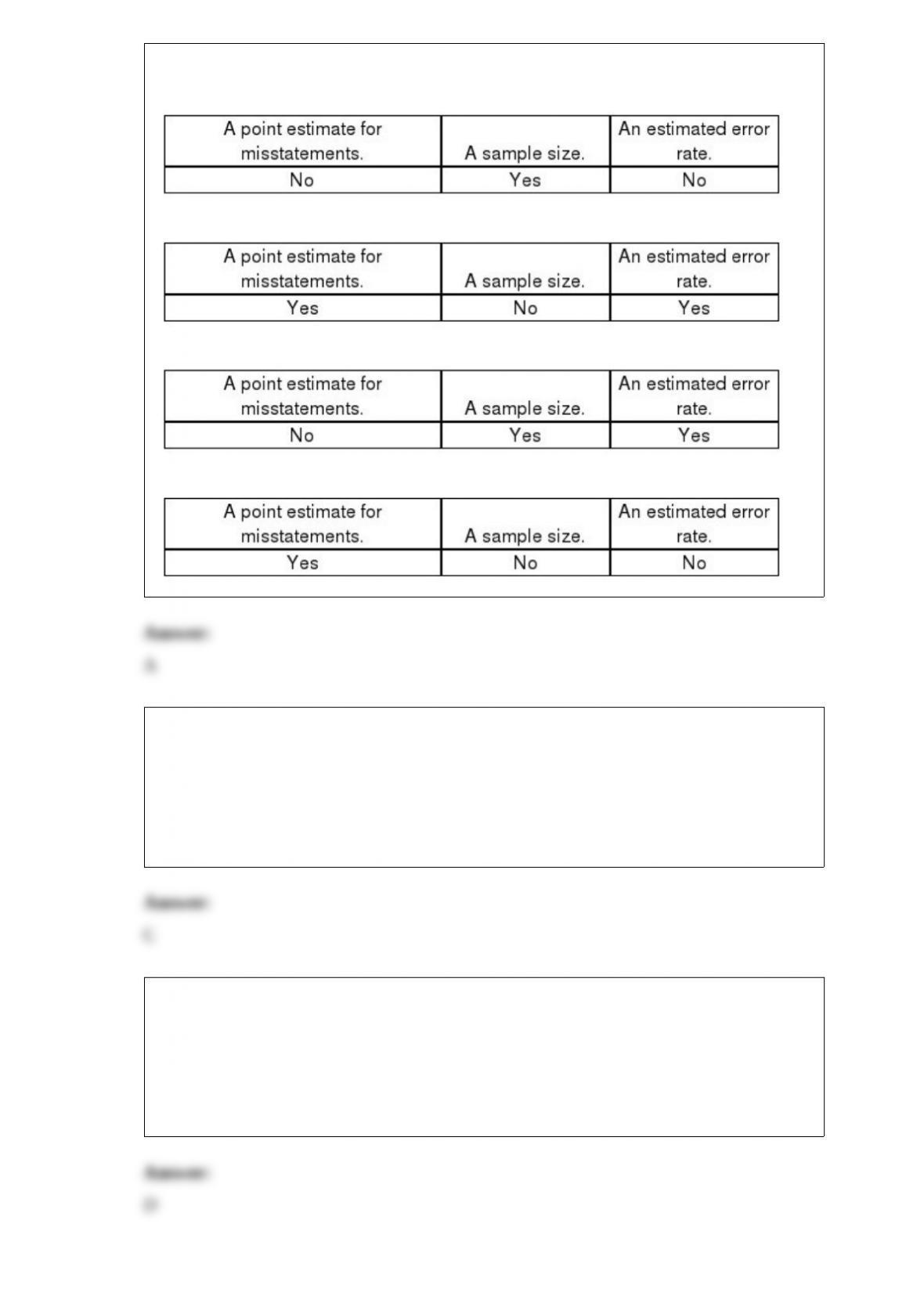

23) Which of the following items is not needed to apply MUS?

A)

B)

C)

D)

24) Auditors frequently refer to the terms audit assurance, overall assurance, and level

of assurance to refer to ________.

A) detection risk

B) audit report risk

C) acceptable audit risk

D) inherent risk

25) Which of the following is most correct regarding external auditors use of internal

auditors directly on the audit engagement?

A) discourage

B) prohibit

C) encourage

D) permit

26) Below are five audit procedures, all of which are tests of transactions associated

with the audit of the acquisition and payment cycle. Also below are the six general

transaction-related audit objectives and the five management assertions. For each audit

procedure, indicate (1) its audit objective, and (2) the management assertion being

tested.

Audit Objectives A. Occurrence B. Completeness C. Accuracy D. Posting and

summarization E. Classification F. Timing Assertions V. Occurrence W. Completeness

X. Accuracy Y. Classification Z. Cutoff

27) When labor is a material part of inventory, auditors should emphasize substantive

tests of transactions.

A) True

B) False

28) The balance-related audit objectives of realizable value and rights are not affected

by assessed control risk.

A) True

B) False

29) Examination attestation engagements result in a conclusion that is in a positive

form, whereas review attestation engagements result in a conclusion in the form of a

negative assurance.

A) True

B) False

30) Match seven of the terms (a-k) with the definitions provided below (1-7):

a.Accounts receivable balance-related audit objectives

b.Aged trial balance

c.Alternative procedures

d.Blank confirmation form

e.Cutoff misstatements

f.Evidence planning worksheet

g.Negative confirmation

h.Positive confirmation

i.Realizable value of accounts receivable

j.Timing difference in an account receivable confirmation

k.Invoice confirmation

________ 1> The follow-up of a positive confirmation not returned by the debtor with

the use of documentation evidence to determine whether the recorded receivable exists

and is collectible.

________ 2> A letter, addressed to the debtor, requesting that the recipient indicate

directly on the letter whether the stated account balance is correct or incorrect and, if

incorrect, by what amount.

________ 3> Misstatements that take place as a result of current period transactions

being recorded in a subsequent period, or subsequent period transactions being recorded

in the current period.

________ 4> A form used to help the auditor decide whether planned detection risk for

tests of details of balances should be low, medium, or high for each balance-related

audit objective.

________ 5> A letter, addressed to the debtor, requesting a response only if the

recipient disagrees with the amount of the stated account balance.

________ 6> A reported difference in a confirmation from a debtor that is determined

to be a timing difference between the client’s and debtor’s records and therefore not a

misstatement.

________ 7> A listing of the balances in the accounts receivable master file at the

balance sheet date broken down according to the amount of time that has passed

between the date of sale and the balance sheet date.

31) The preferred defense in third-party suits is absence of causal connection.

A) True

B) False

32) Under GAAS, which of the following reflects a concept from the general group?

A) The confirmation of accounts receivable

B) Completing an internal control questionnaire

C) The initial planning of the audit with the audit partner, manager, senior, staff and

client personnel

D) The assignment of audit personnel to an engagement where they have no financial

interest

33) Accounts receivable need not be confirmed if they are immaterial to the financial

statements.

A) True

B) False

34) Which of the following is true concerning financial statements issued by a U.S.

entity to the Securities and Exchange Commission?

A) Financial statements can be prepared using International Financial Reporting

Standards

B) The United States now allows an auditor to perform an audit of financial statements

of a U.S. entity in accordance with both GAAS and International Audit Standards

C) The United States only allows an auditor to perform an audit of financial statement

of an entity in accordance with GAAS if they are using International Financial

Reporting Standards

D) An audit that uses both the GAAS and International Audit standards must modify the

scope paragraph to include both sets of standards

35) Which of the following statements is true? The CPA firm will lose its independence

if:

A) a staff auditor providing audit services to the client acquires stock in that client

B) a staff tax preparer who provides 15 hours of non-audit services to the client

acquires stock in that client

C) an audit manager in an office different than the office providing audit services has a

direct, immaterial financial interest in the audit client

D) a covered member has an indirect, immaterial financial interest in an audit client

36) When performing an operational audit, the internal audit team must first determine

that:

A) a financial audit has been performed by an independent auditor

B) a financial audit has been performed by an internal auditor

C) a review was performed by either an independent or an internal auditor

D) specific criteria are developed to define effectiveness

37) Due professional care, the third general standard, is concerned with what is done by

the independent auditor and how well it is done. For example, due care in the matter of

audit documentation requires that audit documentation of the evidence gathered by the

auditor meets which of the following criteria?

A) Workpapers be indexed to the general ledger accounts and include both a permanent

file and a general file

B) The content be sufficient to provide support for the auditor’s opinion, including the

auditor’s representation as to compliance with auditing standards

C) Audit evidence is principally gathered to determine if the client’s financial

statements, as prepared by management, can be relied upon to make managerial

decisions about the firm

D) Audit evidence as displayed in the workpapers is primarily performed to protect the

auditing firm in the case of a lawsuit by investors

38) Discuss what is meant by ‘sampling risk” and “nonsampling risk”.

39) Senior management is responsible for promoting a culture of honesty and ethics.

Describe what that implies for the organization.

40) Draft a report that would be appropriate when an independent accountant has

performed a compilation of financial statements with disclosures in accordance with

GAAP.

41) What are three factors that have increased the importance of obtaining an

understanding of a client’s business and industry? How can an auditor obtain this

understanding?

42) Using your knowledge of the relationships among acceptable audit risk, inherent

risk, control risk, planned detection risk, tolerable misstatement, and planned evidence,

state the effect on planned evidence (increase or decrease) of changing each of the

following factors, while the other factors remain unchanged.

1>An increase in acceptable audit risk.________.

2>An increase in inherent risk. ________.

3>A decrease in control risk. ________.

4>An increase in planned detection risk. ________.

5>An increase in tolerable misstatement. ________.

43) There are 14 steps to attributes sampling, divided into three sections: plan the

sample, select the sample and perform the audit procedures, and evaluate the results. In

the planning section there are 9 steps, beginning with ‘state the audit objective” and

ending with “determine the initial sample size”. Name and discuss at least 3 steps

between the ones listed above.

44) Describe what analytical procedures and tests of details of balances are and give an

example of each.

45) The audit of the inventory and warehousing cycle consists of five parts. State the

five parts and, for each part, identify the cycle in which that part is tested by the auditor.

46) What is a WebTrust engagement? What is a SysTrust engagement? How do they

differ?

47) Define the following terms: control deficiency, significant deficiency, and material

weakness.