1) Raymond Company owns 90% of Rachel Company. Rachel Company owns 10% of

Raymond Company. The treasury stock method is used. On the books of Rachel

Company, we maintain the Investment in Raymond using the ________ method. The

ending balance in Investment in Raymond is ________ stockholders’ equity in the

consolidated balance sheet.

A) equity; deducted from

B) cost; deducted from

C) treasury stock; deducted from

D) conventional; added to

2) Bonds with relatively high risk of default are called

A) Brady bonds

B) junk bonds

C) zero coupon bonds

D) investment grade bonds

3) When the Treasury bond market becomes less liquid, other things equal, the demand

curve for corporate bonds shifts to the ________ and the demand curve for Treasury

bonds shifts to the ________

A) right; right

B) right; left

C) left; right

D) left; left

4) The purchase price of an option contract is typically recorded as

A) an expense

B) an asset

C) an amortized cost

D) a component of shareholders equity

5) Which one of the following statements is correct for an investor company?

A) The balance in the Investment in Osprey Co. account can be reduced to represent a

decline in the fair market value of the investment, but will not be adjusted if the fair

market value increases

B) Under the equity method, the balance in the Investment in Osprey Co. account can

be negative if the investee corporation operates at a loss

C) Once the balance in the Investment in Osprey Co. is reduced to zero, it will not be

reduced any further

D) Under the equity method, the balance in the Investment in Osprey Co. account will

increase when cash dividends are received

6) There are several theories for allocating constructive gains or losses between

purchasing and issuing affiliates. The Agency Theory

A) does so based on the par value of the bonds purchased

B) assigns the entire constructive gain or loss to the parent based on their control of the

decision to purchase the bonds

C) assigns the entire constructive gain or loss to the subsidiary based on the need to

have the noncontrolling interest share in the retirement of the debt

D) assigns the entire constructive gain or loss to whichever company issued the bonds

7) On January 1, 2011, Bosna borrowed $100,000 from Lenda. The three-year term note

carries a variable rate interest, based on LIBOR, and interest is payable at December 31

of each year, compounded annually. The first year’s rate of interest is 7% and Bosna

would like to assure that their rate does not increase. Bosna enters into a pay-fixed,

receive-variable interest rate swap agreement with Swamp City Bank, under which

Bosna will pay 7%, fixed. At December 31, 2011, it is determined that Bosna’s interest

rate to Lenda for 2012 will be 6%. At December 31, 2012, the interest rate for 2013 was

determined to be 8%. Treat as a cash flow hedge.

Required:

Determine the estimated fair value of the hedge at December 31, 2011, and prepare the

related journal entries required to document this hedge and the related interest payments

at December 31, 2011, 2012, and 2013, including final repayment on 12/31/13 . Assume

a flat interest rate curve.

8) Everything else held constant, abolishing all taxes will

A) increase the interest rate on corporate bonds

B) reduce the interest rate on municipal bonds

C) increase the interest rate on municipal bonds

D) increase the interest rate on Treasury bonds

9) Pan Corporation has total stockholders’ equity of $5,000,000 consisting of

$1,000,000 of $10 par value Common Stock, $1,000,000 of Additional Paid-in Capital,

and $3,000,000 of Retained Earnings. Pan owns 80% of Sailor Corporation’s common

stock purchased at book value, which equals fair value. Sailor has $900,000 of 10%

cumulative preferred stock outstanding, with no preferred dividends in arrears. The

preferred stock has no call price, redemption price or liquidation price. Pan acquired

60% of the preferred stock of Sailor for $500,000. After this transaction the balances in

Pan’s Retained Earnings and Additional Paid-in Capital accounts, respectively, are

A) $2,960,000 and $1,000,000

B) $3,000,000 and $960,000

C) $3,000,000 and $1,040,000

D) $3,040,000 and $1,000,000

10) Which of the following is not a quantitative threshold for determining a reportable

segment?

A) Segment assets are 10% or more of the combined assets of all operating segments

B) The absolute value of a segment’s profit or loss is 10% or more of the greater of (1)

the combined reported profit of all operating segments that reported a profit or (2) the

absolute value of the combined reported loss of all operating segments that reported a

loss

C) Segment reported revenue, including intersegment revenues, is 10% or more of the

combined revenue (both internal and external) of all operating segments

D) Segment residual profit after the cost of equity is 10% or more of the combined

residual profit of all operating segments

11) Which type of trust is created pursuant to a will?

A) A testamentary trust

B) A Crummey trust

C) A generation-skipping trust

D) A life estate trust

12) Under GAAP, the ________ will include the variable interest entity in consolidated

financial statements.

A) special purpose entity

B) limited liability company

C) trust

D) primary beneficiary

13) Typically, yield curves are

A) gently upward sloping

B) mound shaped

C) flat

D) bowl shaped

14) On January 1, 2010, Shrimp Corporation purchased a delivery truck with an

expected useful life of five years, and a salvage value of $8,000. On January 1, 2012,

Shrimp sold the truck to Pacet Corporation. Pacet assumed the same salvage value and

remaining life of three years used by Shrimp. Straight-line depreciation is used by both

companies. On January 1, 2012, Shrimp recorded the following journal entry:

Debit Credit

Cash50,000

Accumulated depreciation18,000

Truck53,000

Gain on Sale of Truck15,000

Pacet holds 60% of Shrimp. Shrimp reported net income of $55,000 in 2012 and Pacet’s

separate net income (excludes interest in Shrimp) for 2012 was $98,000.

The noncontrolling interest share for 2012 was

A) $18,000

B) $22,000

C) $23,000

D) $27,000

15) On July 1, 2011, Piper Corporation issued 23,000 shares of its own $2 par value

common stock for 40,000 shares of the outstanding stock of Sector Inc. in an

acquisition. Piper common stock at July 1, 2011 was selling at $16 per share. Just

before the business combination, balance sheet information of the two corporations was

as follows:

PiperSectorSector

Book BookFair

ValueValueValue

Cash$25,000$17,000$17,000

Inventories55,00042,00047,000

Other current assets110,00040,00030,000

Land100,00045,00035,000

Plant and equipment-net660,000220,000280,000

$950,000$364,000$409,000

Liabilities$220,000$70,000$75,000

Capital stock, $2 par value500,000100,000

Additional paid-in capital170,00090,000

Retained earnings60,000104,000

$950,000$364,000

Required:

1>Prepare the journal entry on Piper Corporation’s books to account for the investment

in Sector Inc.

2>Prepare a consolidated balance sheet for Piper Corporation and Subsidiary

immediately after the business combination.

16) Greta, Harriet, and Ivy have a retail partnership business selling personal

computers. The partners are allowed an interest allocation of 6% on their average

capital. Capital account balances on the first day of each month are used in determining

weighted average capital, regardless of additional partner investment or withdrawal

transactions during any given month. Withdrawals of capital that are debited to the

capital account are used in the average calculation. Partner capital activity for the year

was:

Capital accountsGretaHarrietIvy

Jan 1 balance$680,000$500,000$580,000

Feb 12 investment40,000

Mar 26 investment20,000

Apr 20 withdrawal(10,000)

May 8 withdrawal(15,000)(8,000)

Jul 3 investment14,000

Sep 29 investment8,0003,0006,000

Nov 5 investment3,000

Required:

Calculate weighted average capital for each partner, and determine the amount of

interest that each partner will be allocated. Round all calculations to the nearest whole

dollar.

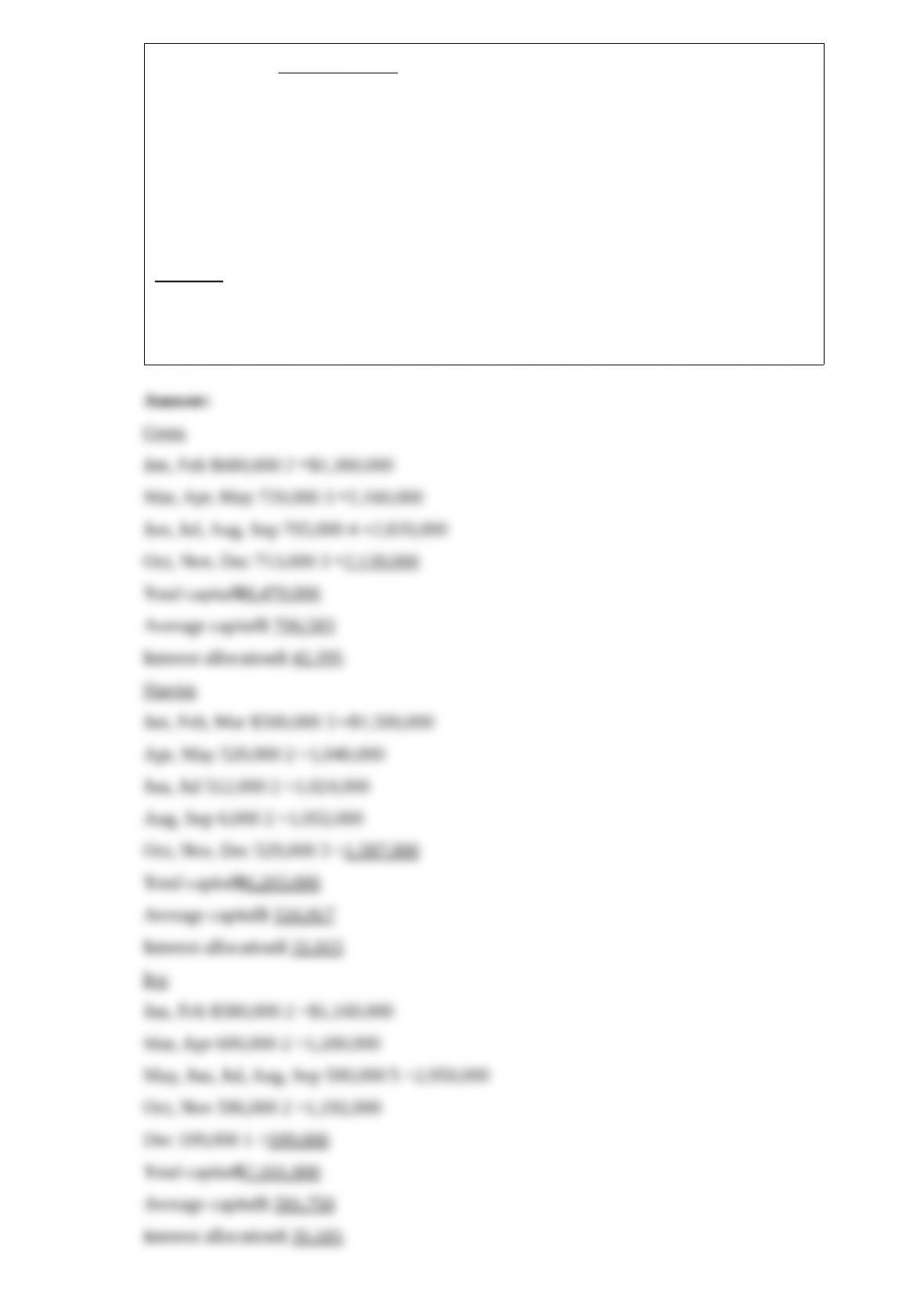

17) Parrot Corporation acquired 90% of Swallow Co. on January 1, 2011 for $27,000

cash when Swallow’s stockholders’ equity consisted of $10,000 of Capital Stock and

$5,000 of Retained Earnings. The difference between the fair value and book value of

Swallow’s net assets was allocated solely to a patent amortized over 5 years. The

separate company statements for Parrot and Swallow appear in the first two columns of

the partially completed consolidation working papers.

Required:

Complete the consolidation working papers for Parrot and Swallow for the year 2011 .

18) The Vera, Wade, and Xena partnership was dissolved, and a cash distribution plan

was developed, as follows:

Priority

CreditorsVeraWadeXena

First $462,000100%

Next $173,00060%40%

Next $240,0007/125/12

Remainder20%30%50%

Required:

If $1,000,000 of cash was distributed by the partnership, how much was received

respectively by the priority creditors, Vera, Wade, and Xena?

19) Pretax operating incomes of Panitz Corporation and its 80%-owned subsidiary,

Salazar Corporation, for the year 2011, are shown below.

Panitz and Salazar belong to an affiliated group. Salazar pays total dividends of $35,000

for the year. There are no unamortized book value/fair value differentials relating to

Panitz’s investment in Salazar. During the year, Panitz sold land to Salazar at a total loss

of $15,000 which is included in its pretax operating income. Salazar still holds this land

at the end of the year. The marginal corporate tax rate for both corporations is 34%.

PanitzSalazar

Sales revenue$890,000$700,000

Loss on sale of land(15,000)

Cost of sales(400,000)(250,000)

Other expenses(350,000)(350,000)

Depreciation expense(50,000)(35,000)

Pretax operating income

(does not include Salazar investment income)$75,000$65,000

Required:

1> Determine the separate amounts of income tax expense for Panitz and Salazar as if

they had filed separate tax returns.

2> Determine Panitz’s net income from Salazar.