1) Which of the following is the primary basis used to decide materiality for a for-profit

entity?

A) net sales

B) net assets

C) net income before tax

D) all of the above

2) During the course of an audit, a CPA observes that the recorded interest expense

seems to be excessive in relation to the balance in the long-term debt account. This

observation could lead the auditor to suspect that:

A) long-term debt is understated

B) discount on bonds payable is overstated

C) long-term debt is overstated

D) premium on bonds payable is understated

3) An auditor uses statistical sampling for attributes in internal control testing. She

would most likely reduce the planned reliable on the control tested when:

A) the sample deviation rate plus the adjustment for sampling risk exceeded the

tolerable deviation rate

B) the sample deviation rate plus the adjustment for sampling risk equaled the tolerable

deviation rate

C) the tolerable deviation rate less the adjustment for sampling risk exceeded the

expected population deviation rate

D) the tolerable deviation rate plus the adjustment for sampling risk was less than the

expected population deviation rate

4) When selecting a stratified sample, the sample size is:

A) determined for the unstratified population and then apportioned to each stratum

B) determined for each stratum and selected from that stratum

C) determined for each stratum and selected randomly from the entire unstratified

population

D) always larger than if unstratified sampling had been used

5) Which of the following requires recognition in the auditor’s opinion as to

consistency?

A) The correction of an error in the prior year’s financial statements resulting from a

mathematical mistake in capitalizing interest

B) A change in the estimate of provisions for warranty costs

C) The change from the cost method to the equity method of accounting for investments

in common stock

D) A change in depreciation method which has no effect on current year’s financial

statements but is certain to affect future years

6) The most important element of the audit risk model is control risk.

A) True

B) False

7) All CPA firms registered with the PCAOB are required to undergo a peer review

annually.

A) True

B) False

8) A document sent to each customer showing his or her beginning accounts receivable

balance and the amount and date of each sale, cash payment received, any debit or

credit memo issued, and the ending balance is the:

A) accounts receivable subsidiary ledger

B) monthly statement

C) remittance advice

D) sales invoice

9) You have been assigned to the accounts payable transaction cycle as part of your

auditing responsibilities. You have decided to vouch a sample of entries in the accounts

payable master file to supporting documents. Which assertion is this test of controls

most likely to support?

A) Accuracy

B) Classification

C) Completeness

D) Occurrence

10) Which of the following is most correct with regard to the comparison of the

financial auditing standards of the Yellow Book with the 10 General Auditing Standards

for financial audits?

A) the same as

B) quite different from

C) incompatible with

D) consistent with

11) The receipt of a customer order from a customer is the starting point for the entire

sales and collection cycle.

A) True

B) False

12) The auditor would expect that an account receivable from a customer would be

written off by the client when which of the following occurs:

A) the customer files for bankruptcy

B) the account is at least six months old

C) a collection agency cannot inspire customer to pay the debt

D) the client company concludes that an amount is no longer collectible

13) When the auditor decides to select less than 100 percent of the population for

testing, the auditor is said to use:

A) audit sampling

B) representative sampling

C) poor judgment

D) estimation sampling

14) If the auditor lacks independence, a disclaimer of opinion must be issued:

A) if the client requests it

B) only if it is highly material

C) only if it is material but not pervasive

D) in all cases

15) The Audit Standards Board of the

I.The “General” standards of GAAS will be termed “Responsibilities”.

II.The “Fieldwork” standards will be termed “Performance”.

III.The “Reporting” standards will be termed “Communications”.

A) I and II

B) I and III

C) II and III

D) I, II and III

16) Matthews & Co., CPAs, issued an unqualified opinion on Dodgers Corporation.

Millennium Bank, which relied on the audited financial statements, granted a loan of

$200,00,000 to Dodgers Corporation. Dodgers subsequently defaulted on the loan. To

succeed in an action against Matthews & Co., Millennium Bank must prove that the

bank was:

A) in privity of contract with Dodgers

B) in privity of contract with Millennium

C) free from contributory negligence

D) justified in relying on the financial statements in granting the loan

17) Place the following steps in their proper order:

1>Analyze exceptions

2>Select the sample

3>Define attributes and exception conditions

4>State the objectives of the audit test

5>Specify the tolerable exception rate

A) 1, 3, 2, 4, 5

B) 4, 3, 1, 2, 5

C) 4, 3, 5, 2, 1

D) 1, 2, 3, 4, 5

18) Relevance of evidence can only be considered in terms of specific audit objectives.

A) True

B) False

19) Which of the following would not be considered further audit procedures?

A) tests of controls

B) substantive analytical procedures

C) tests of details of balances

D) risk assessment procedures

20) Objective evidence is more reliable, and hence more persuasive, than subjective

evidence.

A) True

B) False

21) The file for recording each payroll transaction for each employee and maintaining

total employee wages paid for the year to date is the:

A) payroll master file

B) summary payroll report

C) payroll journal

D) job time ticket

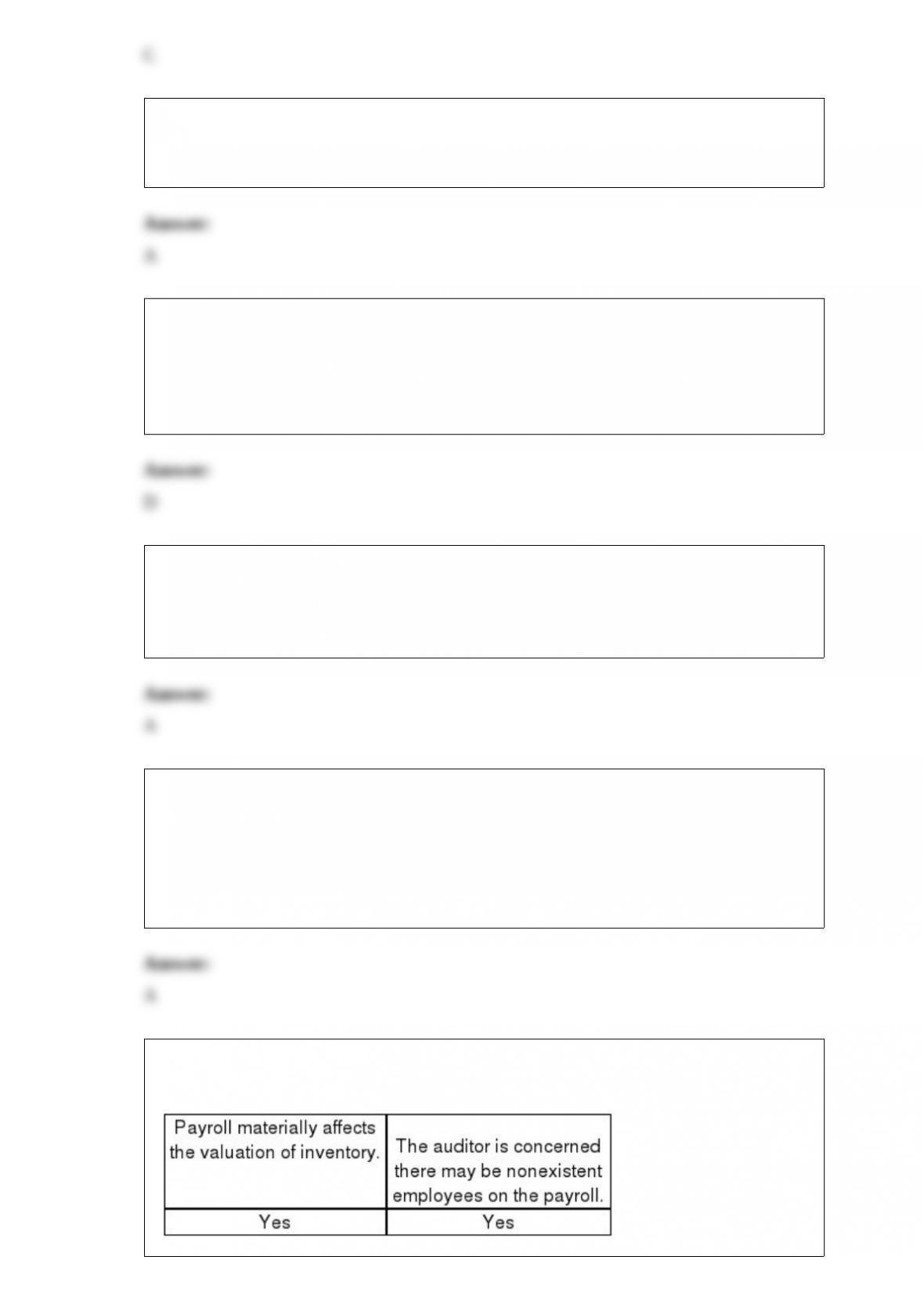

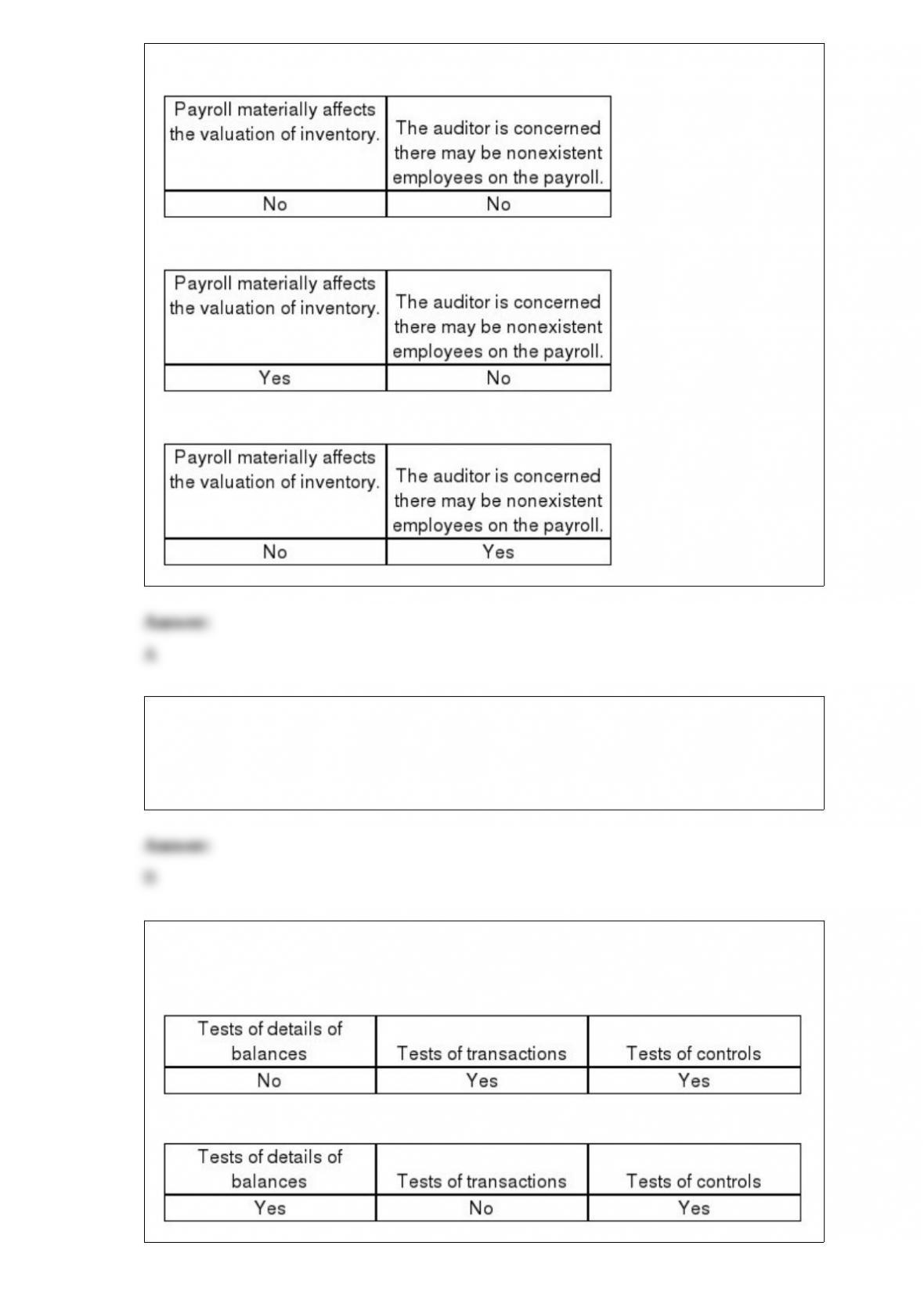

22) Auditors may extend their tests of payroll in which of the following circumstances?

A)

B)

C)

D)

23) When auditing the general cash account, receipt of a standard bank confirmation is

the starting point for verifying the company’s general cash account balance.

A) True

B) False

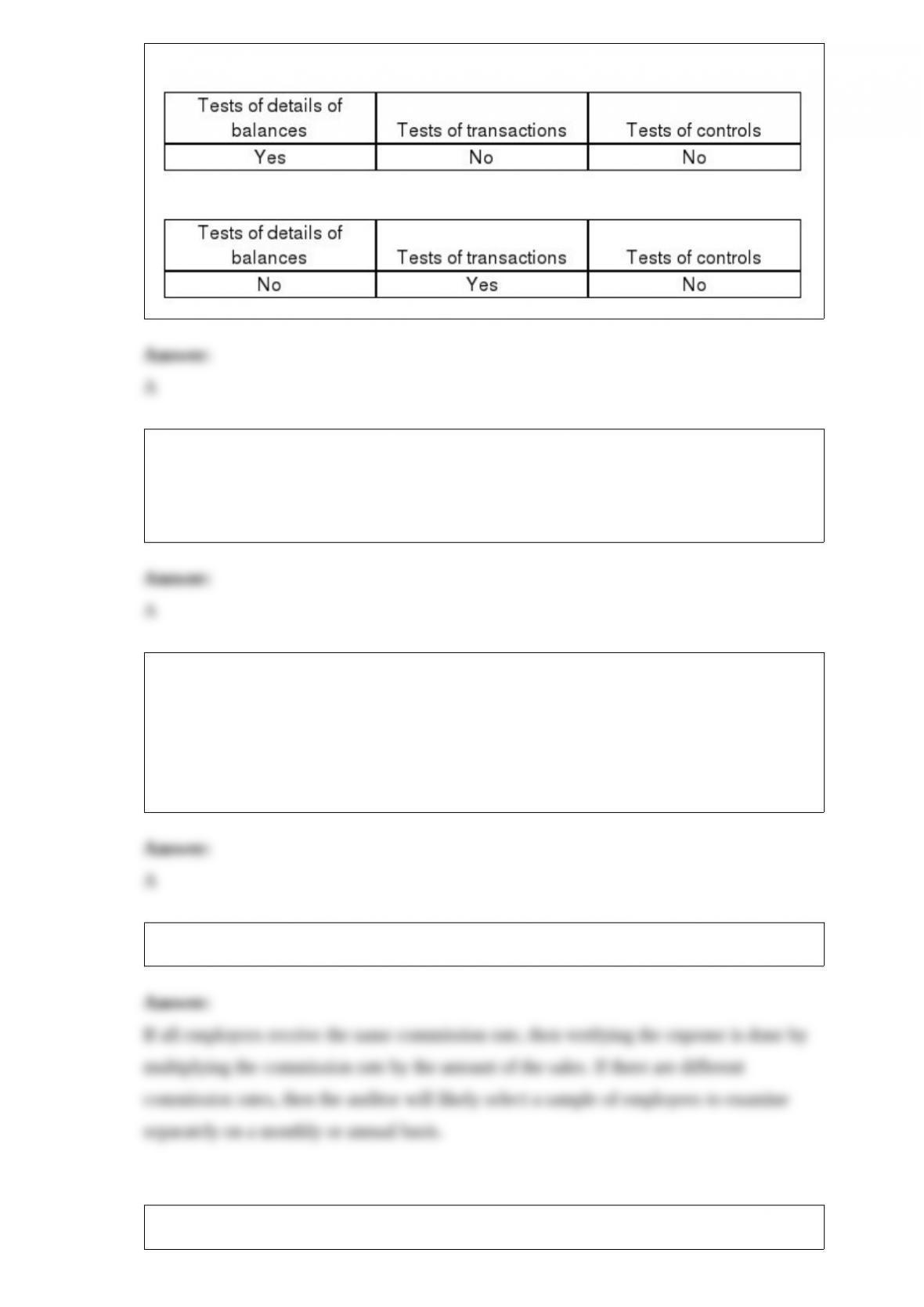

24) What type of audit test will auditors use when testing to see if existing capital stock

transactions are recorded?

A)

B)

C)

D)

25) The type of receivables confirmation is a major factor affecting sample size, with

negative confirmations normally requiring a larger sample than positive confirmations.

A) True

B) False

26) Which of the following is not a similarity between external and internal auditors?

A) Both must be independent of the company

B) Both must be competent

C) Both follow a similar methodology in performing their audits

D) Both consider risk and materiality deciding the extent of their tests and evaluating

results

27) How do auditors commonly verify sales commission expense?

28) When an auditor uses negative confirmations, several factors must be considered.

What are those factors?

29) In addition to an opinion on whether the financial statements are in accordance with

GAAP, identify four other reports required by the OMB Circular A-133.

30) Describe the sources of information gathered to assess fraud risks.

31) Discuss the sanctions the Securities and Exchange Commission can impose on

auditors.

32) When assessing planned control risk for sales, the auditor is concerned about proper

authorization at three key points. Discuss each of these three points.

33) What are the auditor’s primary concerns in verifying the transfer of inventory from

one location to another?

34) Discuss the relationship of each of the following to the extent of planned tests of

details of balances: (1) tolerable misstatement, (2) inherent risk, (3) control risk, and (4)

acceptable audit risk.