1) Transactions with related parties must be disclosed in the financial statements if they

are deemed to be material.

A) True

B) False

2) The international standards for the professional practice of internal auditing include

which two categories of standards?

A) attribute and performance

B) competency and professional skepticism

C) performance and integrity

D) ethics and rules of conduct

3) The most important balance-related audit objectives in the audit of cash include all

but which of the following?

A) Existence

B) Accuracy

C) Completeness

D) Occurrence

4) Which of the auditor’s defenses is ordinarily not available when lawsuits are filed by

a third party?

A) Absence of causal connections

B) Contributory negligence

C) Non-negligent performance

D) Lack of duty

5) When management has an adequate level of integrity for the auditor to accept the

engagement but cannot be regarded as completely honest in all dealings, auditors

normally:

A) reduce acceptable audit risk and increase inherent risk

B) reduce inherent risk and control risk

C) increase inherent risk and control risk

D) increase acceptable audit risk and reduce inherent risk

6) A record of insurance policies in force and the due date of each policy is contained in

the:

A) voucher register

B) insurance register

C) insurance expense account

D) prepaid insurance account

7) Which of the following statements best describes the auditor’s responsibility with

respect to illegal acts that do not have a material effect on the client’s financial

statements?

A) Generally, the auditor is under no obligation to notify parties other than personnel

within the client’s organization

B) Generally, the auditor is under an obligation to inform the PCAOB

C) Generally, the auditor is obligated to disclose the relevant facts in the auditor’s report

D) Generally, the auditor is expected to compel the client to adhere to requirements of

the Foreign Corrupt Practices Act

8) A weak internal control system allows a department supervisor to “clock in” for a

fictitious employee and then approve the employee’s time card at the end of the pay

period. This fraud would be detected if other controls were in place, such as having an

independent party:

A) distribute paychecks

B) recompute hours worked from time cards

C) foot the payroll journal and trace postings to the general ledger and the payroll

master file

D) compare the date of the recorded check in the payroll journal with the date on the

canceled checks and time cards

9) When the auditor believes the year-end bank reconciliation may be intentionally

misstated, it is appropriate to perform extended tests of the year-end bank

reconciliation. Assuming the client has a October 31 year-end, these extended tests

would not include:

A) comparing all September 30 reconciling items with canceled checks and other

documents in the October bank statement

B) comparing all canceled checks and deposit slips in the October bank statement with

the October cash disbursements and receipts records

C) carrying out all proper procedures subsequent to the end of the year with the use of

the bank cutoff statement

D) determining that all outstanding checks had cleared by the date of the bank cutoff

statement

10) A document received from the vendor indicating such things as the description and

quantity of goods and services received, price including freight, cash discount terms,

and date of billing is called the voucher.

A) True

B) False

11) The quarterly reports submitted to the SEC by the client:

A) have to be audited and the CPA firm must be identified

B) do not have to be audited, but the CPA firm which does the year-end audit must be

identified

C) have to be audited, but the CPA firm does not have to be identified

D) do not have to be audited, but the CPA firm which does the year-end audit must

review the quarterly statements before they are submitted to the SEC

12) When comparing misstatements with a measurement base, the auditor must

consider the pervasiveness of the misstatement. Of the following examples, the most

pervasive misstatement is a(n):

A) understatement of inventory

B) understatement of retained earnings caused by a miscalculation of dividends payable

C) misclassification of notes payable as a long-term liability when it should be current

D) misclassification of salary expense as a selling expense

13) General controls have which of the following effects on the operating effectiveness

of application controls?

A) nominal

B) pervasive

C) mitigating

D) worsening

14) In an examination of vendor statements or vendor confirmations when doing

substantive tests of balances the auditor needs to perform the following:

A) reconciliation with the accounts payable master file

B) reconciliation with vendor invoices

C) reconciliation with purchase orders

D) reconciliation with receiving reports

15) When auditors use documentation to support recorded transactions and amounts, the

process is usually called:

A) tracing

B) confirmations

C) vouching

D) reperformance

16) Balance-related audit objectives are usually applied to the ending balance in income

statement accounts; transaction-related audit objectives are usually applied to

transactions reflected in balance sheet accounts.

A) True

B) False

17) Which of the following best describes an audit that emphasizes how efficiently and

effectively functions interact?

A) operational

B) compliance

C) financial

D) organizational

18) The auditor’s main concerns in verifying transfers of inventory do not include

whether:

A) recorded transfers exist

B) transfers represent appropriate uses of company resources

C) all actual transfers are recorded

D) the details of the transfer are accurately recorded

19) With respect to a small company’s system of purchasing supplies, an auditor’s

primary concern should be to obtain satisfaction that supplies ordered and paid for have

been:

A) requested by and approved by authorized individuals who have no incompatible

duties

B) used in the course of business and solely for business purposes during the year under

audit

C) received, counted, and checked to quantities and amounts on purchase orders and

invoices

D) properly recorded as assets and systematically amortized over the estimated useful

life of the supplies

20) A surprise payroll payoff in which employees must pick-up and sign for their pay

check is one means of:

A) identifying employees who do not have proper work credentials

B) establishing a tightly controlled, fraud-free work environment

C) testing for nonexistent employees

D) identifying employees who have not submitted proper W-2 forms

21) A financial institution sues the audit firm for failure to discover that a borrower’s

financial statements are materially misstated. This is an example of which of the

following legal liability concepts?

A) Liability to clients

B) Liability to 3rd parties under common law

C) Civil liability under federal securities law

D) Criminal liability

22) Which of the following procedures performed for the billing function may provide

evidence that the accounts receivable subsidiary ledger is in agreement with the

accounts receivable control account?

A) Making sure that all shipments have been billed

B) Making sure that no shipment has been billed more than twice

C) Making sure that each shipment is billed at the correct amount

D) Making sure that each shipment is billed to the proper customer

23) If an auditor performs an audit of a public company, the scope paragraph should

make reference to which standards?

A) GAAP

B) GAAS

C) Standards issued by the PCAOB (U.S.)

D) International Audit Standards

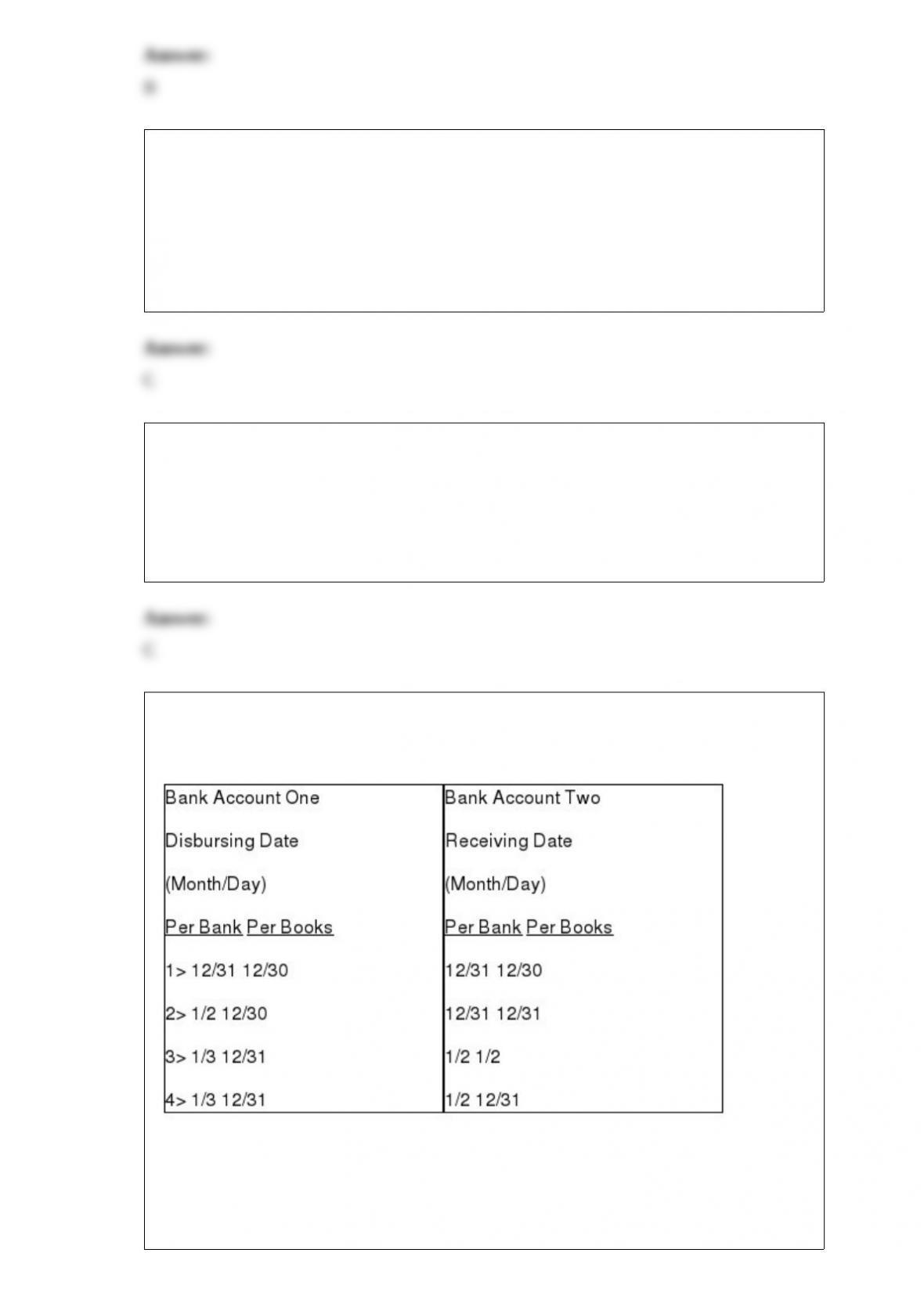

24) Listed below are four interbank cash transfers, indicated by the numbers 1, 2, 3, and

4, of a client for late December 2007 and early January 2008:

Based on the schedule of interbank transfers above, which of the cash transfers

indicates an error in cash cutoff at December 31, 2007?

A) 1

B) 2

C) 3

D) 4

25) When may auditors observe the physical inventory count?

A)

B)

C)

D)

26) A document generally received from the vendor which indicates a reduction in the

amount owed due to the company granting an allowance is:

A) vendor invoice

B) debit memo

C) credit adjustment form

D) credit memo

27) The audit objective that requires that existing notes payable be included in the notes

payable schedule is satisfied by performing which of the following audit procedures?

A) confirm notes payable

B) trace the total of the notes payable schedule to the general ledger

C) review the notes payable schedule to determine whether any are related parties

D) obtain confirmations from creditors who have held notes from the client in the past

and are not currently included in the notes payable schedule

28) After considering a client’s internal controls, an auditor has concluded that it is well

designed and is functioning as intended. Under these circumstances the auditor would

most likely:

A) perform tests of controls to the extent outlined in the audit program

B) determine the control procedures that should prevent or detect errors and

irregularities

C) not increase the extent of predetermined substantive tests

D) determine whether transactions are recorded to permit preparation of financial

statements in conformity with generally accepted accounting principles

29) When designing audit procedures, tracing of source documents to the customers

subsidiary ledger and subsequently to the general ledger is done to satisfy what

assertion?

A) valuation

B) cutoff

C) completeness

D) classification

30) Statements on Auditing Standards (SASs) are considered to be interpretations of the

ten generally accepted auditing standards.

A) True

B) False

31) Benchmarking is one source of evaluation criteria for completing an operational

audit.

A) True

B) False

32) A measure of the auditor’s assessment of the likelihood that there are material

misstatements in an account before considering the effectiveness of the client’s internal

control is called:

A) control risk

B) acceptable audit risk

C) statistical risk

D) inherent risk

33) Paying employees for their services ends the payroll and personnel cycle.

A) True

B) False

34) Assuming the client’s internal controls are adequate, describe how the auditor can

verify proper cutoff of sales transactions.

35) Discuss the advantages and disadvantages of monetary-unit sampling over other

sampling methods.

36) An environmental clean-up lawsuit is pending against your client. What information

about the lawsuit would you as the auditor need in order to determine the “correct”

accounting?

37) Briefly explain each management assertion related to classes of transactions and

events for the period under audit.

38) State three lists or requests that should be included in a standard “inquiry of

attorney” letter.

39) When using nonstatistical sampling, the auditor must subjectively consider whether

the true population misstatement exceeds a tolerable amount. This is done by

considering five factors. One factor is the difference between the point estimate and

tolerable misstatement. State the other four factors the auditor must consider.

40) Discuss three of the following influences on the persuasiveness of evidence.

1>Relevance

2>Independence of provider

3>Effectiveness of client’s internal controls

4>Auditor’s direct knowledge

5>Degree of objectivity

6>Timeliness

41) When auditing disposals of property, plant, and equipment, the search for

unrecorded disposals is essential. State the four audit procedures frequently used for

verifying disposals.

42) List each of the five types of audit tests and list at least two types of evidence that

may be obtained from each type of test.

43) Auditors often use Generalized Audit Software during their testing of a client’s

internal controls. For the following uses of the software provide a description and an

example.

Verify extensions and footings

Print confirmation requests

Compare data on separate files