1) Footing the sales journal and tracing the totals to the general ledger are tests relating

to the accuracy objective for sales.

A) True

B) False

2) The criterion that is most likely to be used as a framework in evaluating a company’s

internal control over financial reporting under Section 404 of the Sarbanes-Oxley Act is

the Enterprise Risk Management framework.

A) True

B) False

3) The major conclusion of the 1931 Ultramares case was that:

A) ordinary negligence is insufficient for liability to third parties

B) ordinary negligence is sufficient for liability to third-party beneficiaries

C) fraud or gross negligence is sufficient for liability to third parties

D) auditors have no liabilities to third parties

4) The auditor gets highly reliable evidence about individual transactions by examining:

A) vendors’ invoices

B) vendors’ statements

C) confirmations of accounts payable balances

D) detailed inventory counting instructions

5) When auditing the payroll and personnel cycle, tests of controls are routinely

performed.

A) True

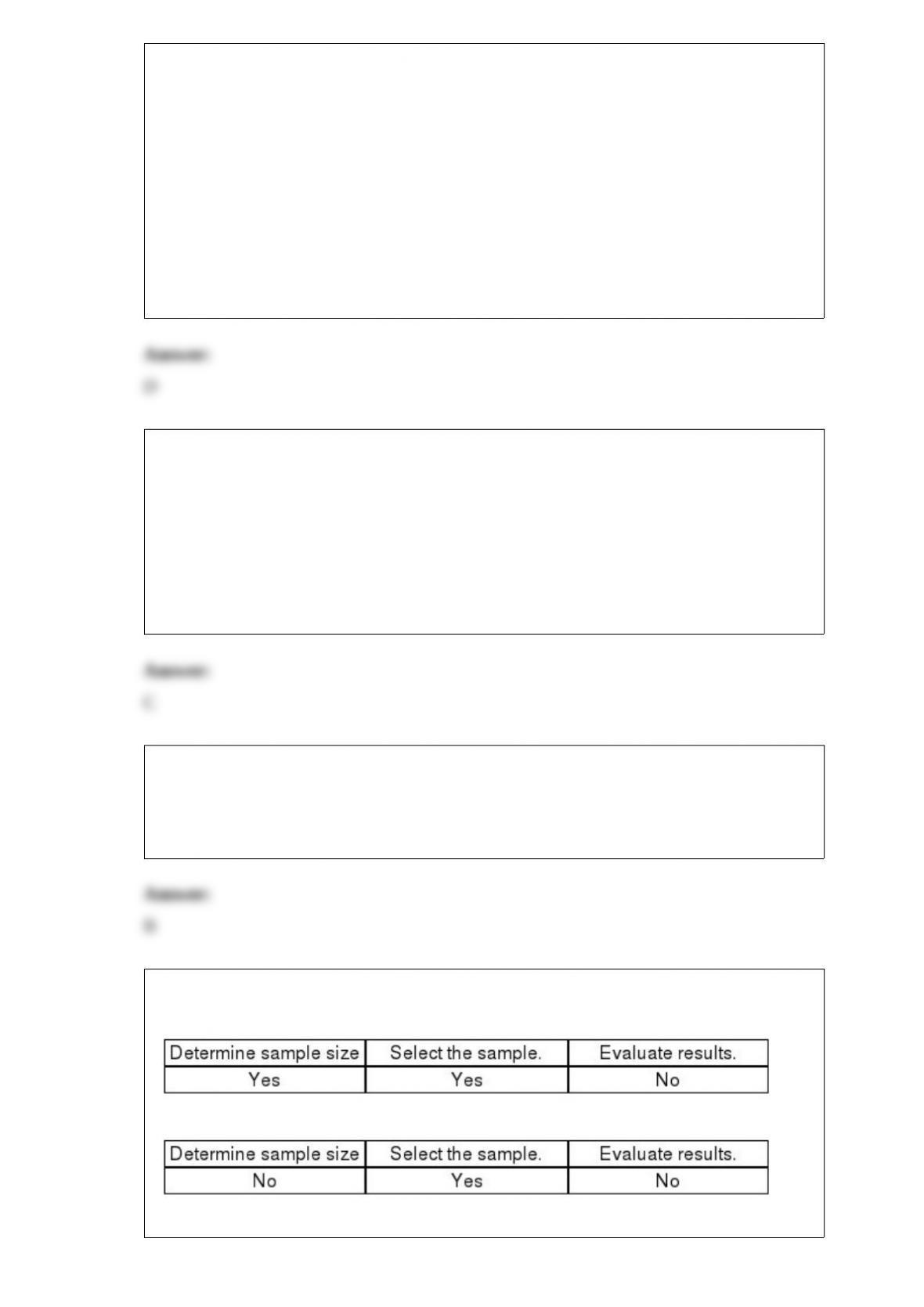

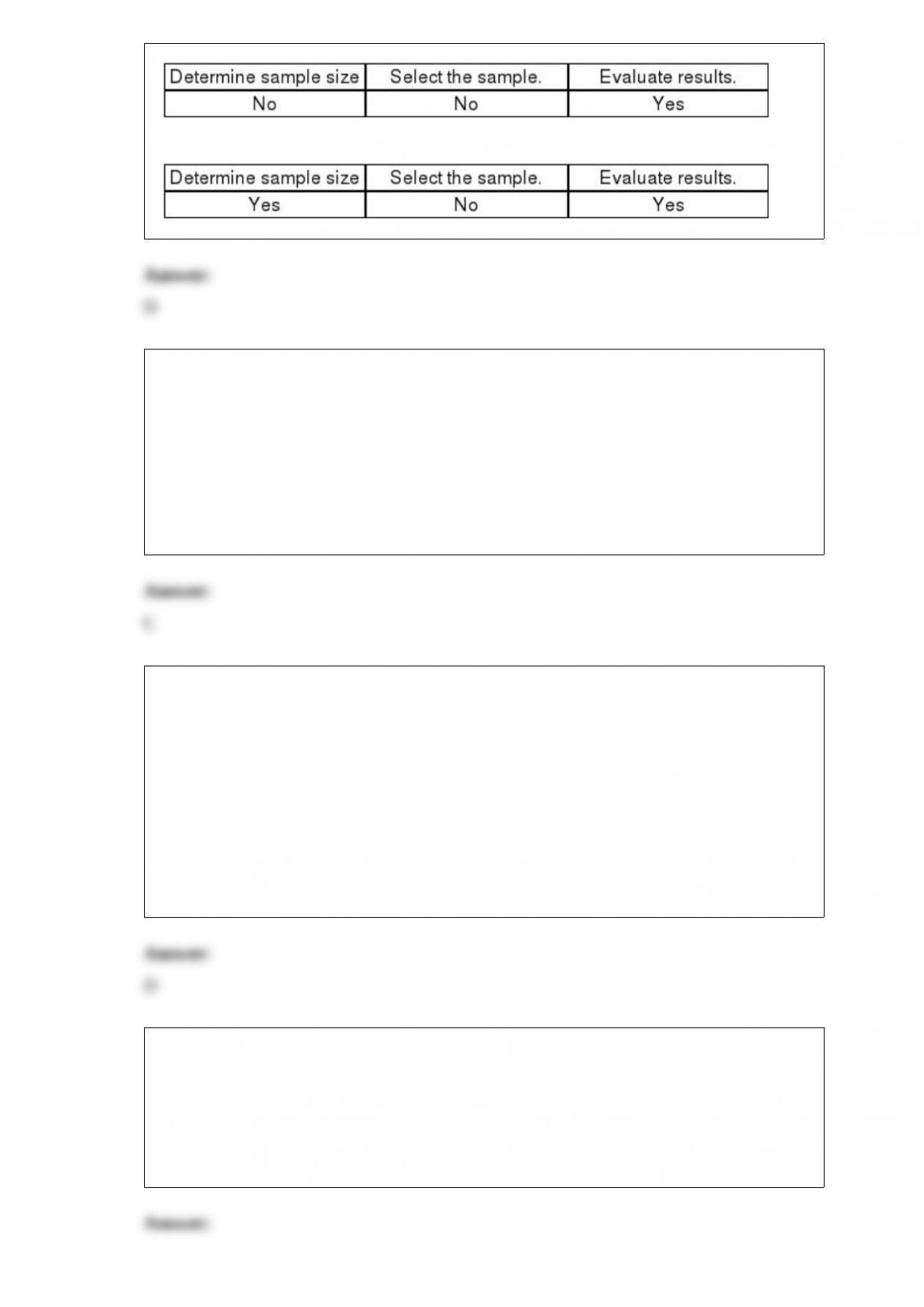

B) False

6) Which of the following does NOT represent an increased opportunity to commit

fraud?

A) Related Party Transactions

B) the company founder is the CEO and Chairman of the Board

C) the financial statements involve accounting estimates

D) the company is a new audit client for the CPA firm

7) Each of the following situations involves a possible violation of the rule on

independence. For each situation, (1) decide whether the Code of Professional Conduct

has been violated, and (2) briefly explain how the situation violates (or does not violate)

the Code of Professional Conduct.

a. Harry Brown is a partner in the Topeka office of Hedley & Co., CPAs. Harry’s

brother is employed in an audit-sensitive position by Jensen Appliances, a publicly held

company in Kansas. Jensen Appliances is one of Hedley & Co.’s audit clients. Neither

Harry nor personnel from the Topeka office is involved in the audit of Jensen.

Violation? Yes No

Explanation:

b. John Woods is an audit manager with Calden & Co., CPAs, a one-office CPA firm.

John owns 100 shares of common stock in one of the firm’s audit clients, but he does

not provide any audit or non-audit services to the company.

Violation? Yes No

Explanation:

c. The accounting firm of Fine & Herman, CPAs, provides bookkeeping and tax

services for Henderson Corporation, a privately held company. Fine & Herman also

performs the annual audit of Henderson Corporation.

Violation? Yes No

Explanation:

d. Bob Shelton CPA, is the auditor of Cafe Ecko. A couple of weeks ago, Cafe Ecko’s

management commenced litigation against Bob, alleging he was negligent in last year’s

audit.

Violation? Yes No

Explanation:

e. Hamilton Appliance has not paid Karen Linwood, CPA, her audit fee for the past two

years. Karen is starting work on the current year’s audit of Hamilton.

Violation? Yes No

Explanation:

8) Which of the following forms of review are permissible under SSARS?

A) review without positive assurance

B) review on financial statements that omit substantially all disclosures

C) reviews without CPA independence

D) review without limited procedures

9) Which of the following most likely would be detected by a review of a client’s sales

cutoff?

A) Excessive sales discounts

B) Unrecorded sales for the year

C) Unauthorized goods returned for credit

D) Lapping of year-end accounts receivable

10) An individual who is not party to the contract between a CPA and the client, but

who is known by both and is intended to receive certain benefits from the contract is

known as:

A) a third party

B) a common law inheritor

C) a tort

D) a third-party beneficiary

11) An auditor is performing a credit analysis of customers with balances over 60 days

due. She is most likely obtaining evidence for which audit related objective?

A) realizable value

B) existence

C) completeness

D) occurrence

12) For a private company client, auditors are required to test any internal controls they

believe have not been operating effectively during the period under audit.

A) True

B) False

13) Reports on agreed-upon procedures are intended to be distributed:

A) to only the involved parties, who would have the requisite knowledge about those

procedures and the level of assurance resulting from them

B) to only the involved parties, who would have the requisite knowledge about those

procedures but not the level of assurance resulting from them

C) to any party to whom the client wishes

D) only to the stockholders of the client

14) Which of the following audit objectives is least important in the audit of capital

stock and paid-in-capital in excess of par?

A) Completeness

B) Accuracy

C) Rights and obligations

D) Presentation and disclosure

15) Distribution of which of the following types of reports is limited?

A) audit

B) review

C) agreed-upon procedures

D) examination

16) Controls over the acquisition and recording of insurance are a part of which of the

following transaction cycles?

A) Inventory and warehousing cycle

B) Capitalization cycle

C) Treasury cycle

D) Acquisition and payment cycle

17) When the auditor recomputes the unexpired portion of prepaid insurance, she is

satisfying which audit objective?

A) Completeness

B) Existence

C) Accuracy and detail tie-in

D) Rights

18) Under the federal securities acts, one significant result occurring directly due to the

Escott et al. v. Bar Chris Construction Corporation case was that SAS was changed to

require:

A) greater emphasis on subsequent events procedures

B) new standards for unaudited statements

C) a broader definition of third-party beneficiaries

D) more companies to file annual reports with the SEC

19) To issue an unqualified opinion on internal control over financial reporting, there

must be no identified material weaknesses and no restrictions on the scope of the audit.

A) True

B) False

20) Tolerable exception rate (TER) is inversely related to sample size.

A) True

B) False

21) Readers of financial statements often interpret that the number of paragraphs in the

independent auditor’s report is a ‘signal” of the entity’s financial fairness. Which of the

following is not true regarding the number of paragraphs in an independent auditor’s

report?

A) More than three paragraphs indicates either a qualification or report modification

B) An additional paragraph is added before the opinion for a qualified, adverse or

disclaimer of opinion

C) An additional paragraph is added after the opinion when there is required

information the auditor must report when the opinion is unqualified

D) No explanatory paragraph is required for an unqualified shared report involving

other auditors, however, explanatory language is added in the introductory paragraph

22) Which of the following statements is most correct with respect to the evaluation of

non-probabilistic sample results?

A) It is acceptable to make non-probabilistic evaluations only when probabilistic

sample selection is used

B) It is acceptable to make non-probabilistic evaluations only if the auditor cannot

quantify sampling risk

C) It is never acceptable to evaluate a non-probabilistic sample using statistical methods

D) All of the above are correct

23) The criteria used by an external auditor to evaluate published financial statements

are known as generally accepted auditing standards.

A) True

B) False

24) Tolerable misstatement is used to:

A)

B)

C)

D)

25) When the auditor concludes that there is substantial doubt about the entity’s ability

to continue as a going concern, the appropriate audit report could be:

I.an unqualified opinion with an explanatory paragraph.

II.a disclaimer of opinion.

A) I only

B) II only

C) I or II

D) Neither I nor II

26) Gregory & Hedrick, a medium-sized CPA firm, employed Elise as a staff

accountant. Elise was negligent while auditing several of the firm’s clients. Under these

circumstances, which of the following statements is true?

A) Elise would have no personal liability for negligence

B) Gregory & Hedrick is not liable for Elise’s negligence because CPAs are generally

considered to be independent contractors

C) Gregory & Hedrick would not be liable for Elise’s negligence if Winters disobeyed

specific instructions in the performance of the audits

D) Gregory & Hedrick can recover against its insurer on its malpractice policy even if

one of the partners was also negligent in reviewing Elise’s work

27) Which of the following is not one of the categories of items included in the client

letter of representation?

A) subsequent events

B) Completeness of information

C) recognition, measurement, and disclosure

D) materiality

28) A lawsuit has been filed against your client. If, in the opinion of legal counsel, the

likelihood your client will lose the lawsuit is remote, no financial statement accrual or

disclosure of the potential loss would generally be required.

A) True

B) False

29) With which of the following client personnel would it generally not be appropriate

to inquire about commitments or contingent liabilities?

A) Controller

B) President

C) Accounts receivable clerk

D) Vice president of sales

30) Qualitative factors can affect an auditor’s assessment of materiality. Which of the

following qualitative factors could influence the assessment of materiality?

I.Misstatements that are otherwise immaterial may be material if they affect earnings

trends.

II.Minor misstatements resulting from the consequences of contractual obligations.

A) I only

B) II only

C) I and II

D) neither I nor II

31) Procedures to obtain an understanding of internal control may suffice for tests of

controls when the auditor is assessing control risk in a well defined transaction cycle

that has not contained material misstatements in prior audits.

A) True

B) False

32) According to the profession’s ethical standards, an auditor would be considered

independent in which of the following instances?

A) The auditor’s checking account, which is fully insured by a federal agency, is held at

a client financial institution

B) The auditor is also an attorney who advises the client as its general counsel

C) An employee of the auditor serves as treasurer of a charitable organization that is a

client

D) The client owes the auditor fees for two consecutive annual audits

33) Which of the following is the correct definition of “control deficiency”?

A) A control deficiency exists if the design or operation of controls does not permit

company personnel to prevent or detect misstatements on a timely basis

B) A control deficiency exists if one or more deficiencies exist that adversely affect a

company’s ability to prepare external financial statements reliably

C) A control deficiency exists if the design or operation of controls results in a more

than remote likelihood that controls will not prevent or detect misstatements

D) A control deficiency exists if the design or operation of controls results in a more

than probable likelihood that controls will prevent or detect misstatements

34) Which of the following situations would most likely require special audit planning?

A) Inventory consists of precious stones

B) Some items of factory and office equipment do not bear identification numbers

C) Depreciation methods used on the client’s tax return differ from those used on the

books

D) Assets costing less than $500 are expensed even though their expected life exceeds

one year

35) Which of the following explanations might satisfy an auditor who discovers

significant debits to an accumulated depreciation account?

A) Extraordinary repairs have lengthened the life of an asset

B) Prior years’ depreciation charges were erroneously understated

C) A reserve for possible loss on retirement has been recorded

D) An asset has been recorded at its fair value

36) The primary role of the United States General Accounting Office is the enforcement

of the federal tax laws as defined by Congress and interpreted by the courts.

A) True

B) False

37) Which of the following is not one of the reasons that auditors provide only

reasonable assurance on the financial statements?

A) The auditor commonly examines a sample, rather than the entire population of

transactions

B) Accounting presentations contain complex estimates which involve uncertainty

C) Fraudulently prepared financial statements are often difficult to detect

D) Auditors believe that reasonable assurance is sufficient in the vast majority of cases

38) Which of the following is responsible for establishing a private company’s internal

control?

A) Senior Management

B) Internal Auditors

C) Senior Management and auditors

D) Audit committee

39) Which of the following management assertions is not associated with

transaction-related audit objectives?

A) Occurrence

B) Classification and understandability

C) Accuracy

D) Completeness

40) While analytical procedures are commonly used when auditing balance sheet

accounts, they are normally not very useful when auditing income statement accounts.

A) True

B) False

41) Discuss the major activities and procedures performed by the auditor in the plan

and design of the audit approach.

42) Cutoff misstatements can occur for sales, sales returns, and cash receipts. List

below the threefold approach an auditor performs for each account above to determine

the reasonableness of the cutoff.

43) Explain why there is a special need for ethical conduct in the auditing profession.

44) Explain the purpose of testing the client’s bank reconciliation, and discuss the major

audit procedures involved.

45) Property, plant, and equipment is normally audited in a different manner than

current asset accounts. State three reasons why this is so, and discuss the differences in

how property, plant, and equipment is audited compared to current assets.

46) The “tone at the top” provides a foundation upon which a more detailed code of

conduct can be developed to provide specific guidance for the organization and its

employees. Components of a code of conduct may include sections on 1> general

employee conduct, 2> relationships with clients and suppliers and 3> conflicts of

interest. Give a narrative description of what might be included in each of the above

components of a code of conduct.

47) Briefly define general controls and application controls.

48) A financial statement review conducted in compliance with SSARS emphasizes five

activities, one of which is to “perform analytical procedures.” State the other four.