1) When auditing insurance expense, auditors normally rely on analytical procedures

and limited testing of the debits to ensure that they arose from credits to prepaid

insurance.

A) True

B) False

2) The four categories for describing the size of audit firms include: the Big Four

international firms; national firms; regional and local firms; and small firms. Which of

the following is not a characteristic of a small firm?

A) Most have fewer than 25 professionals

B) They perform audits on small and not-for-profit businesses

C) Tax services are more important to their practice than auditing

D) They do not audit publically traded companies

3) Which of the following statements relating to the competence of evidential matter is

always true?

A) Evidence from outside an enterprise is always reliable

B) Accounting data developed under satisfactory conditions of internal control are more

relevant than data developed under unsatisfactory internal control conditions

C) Oral representations made by management are not reliable evidence

D) Evidence must be both reliable and relevant to be considered appropriate

4) The audit approach in which the auditor runs his or her own program on a controlled

basis to verify the client’s data recorded in a machine language is:

A) the test data approach

B) called auditing around the computer

C) the generalized audit software approach

D) the microcomputer-aided auditing approach

5) Which of the following is a factor that relates to incentives or pressures to commit

fraudulent financial reporting?

A) Significant accounting estimates involving subjective judgments

B) Excessive pressure for management to meet debt repayment requirements

C) Management’s practice of making overly aggressive forecasts

D) High turnover of accounting, internal audit, and information technology staff

6) A CPA learns that his client has paid a vendor twice for the same shipment, once

based upon the original invoice and once based upon the monthly statement. A control

procedure that should have prevented this duplicate payment is:

A) attachment of the receiving report to the disbursement report

B) prenumbering of disbursement vouchers

C) use of a limit or reasonableness test

D) prenumbering of receiving reports

7) Which of the following is not a risk in an IT system?

A) need for IT experienced staff

B) separation of IT duties from accounting functions

C) improved audit trail

D) hardware and data vulnerability

8) The two characteristics of the appropriateness of evidence are:

A) relevance and timeliness

B) relevance and accuracy

C) relevance and reliability

D) reliability and accuracy

9) In performing an audit of internal control over financial reporting which of the

following is the auditor required to do?

A) Test routine and nonroutine transactions equally

B) Form an opinion on the effectiveness of internal for financial reporting

C) Rely on the work on internal auditors in order to promote audit efficiency

D) Use the audit conclusions before starting the audit of financial statements

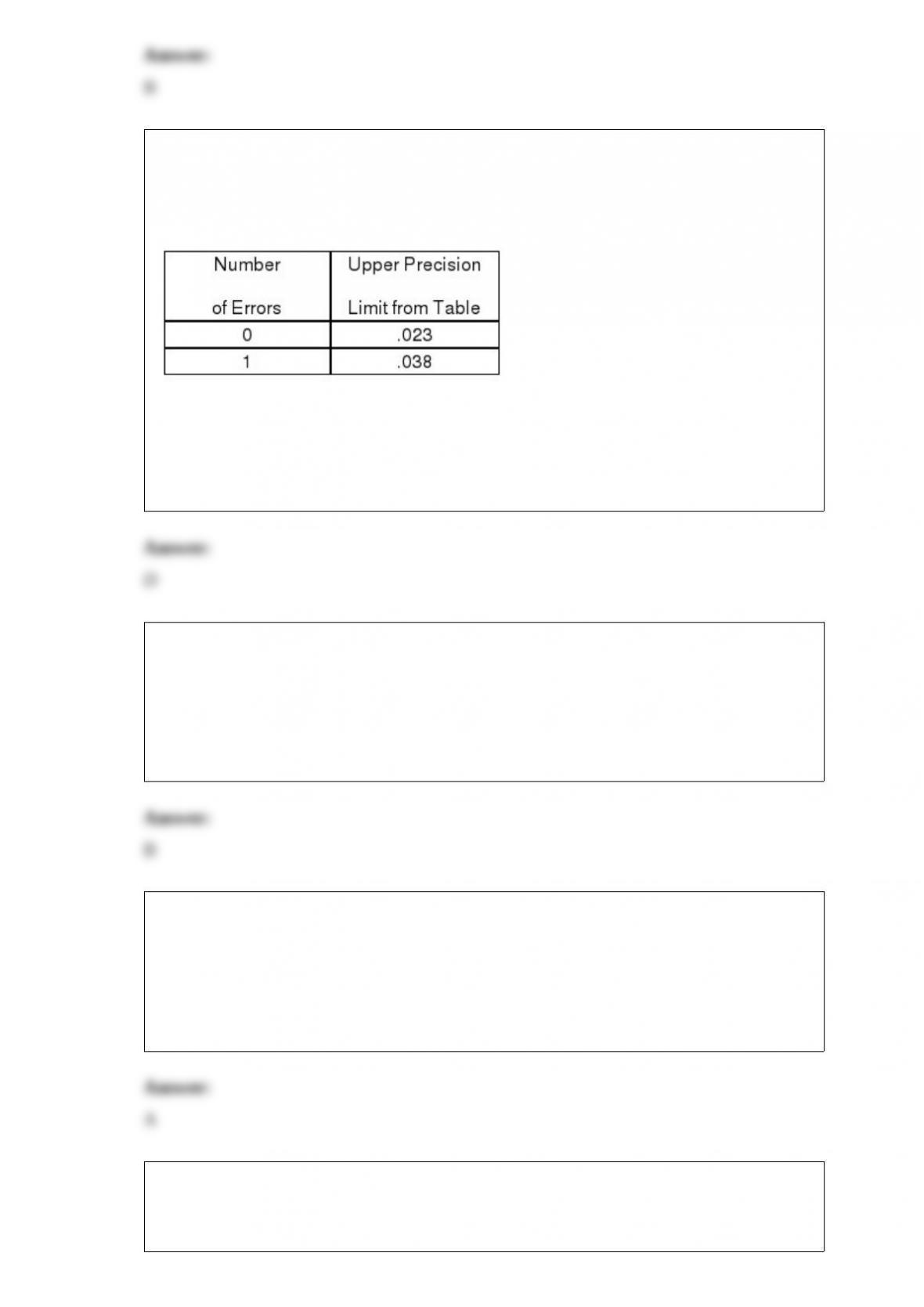

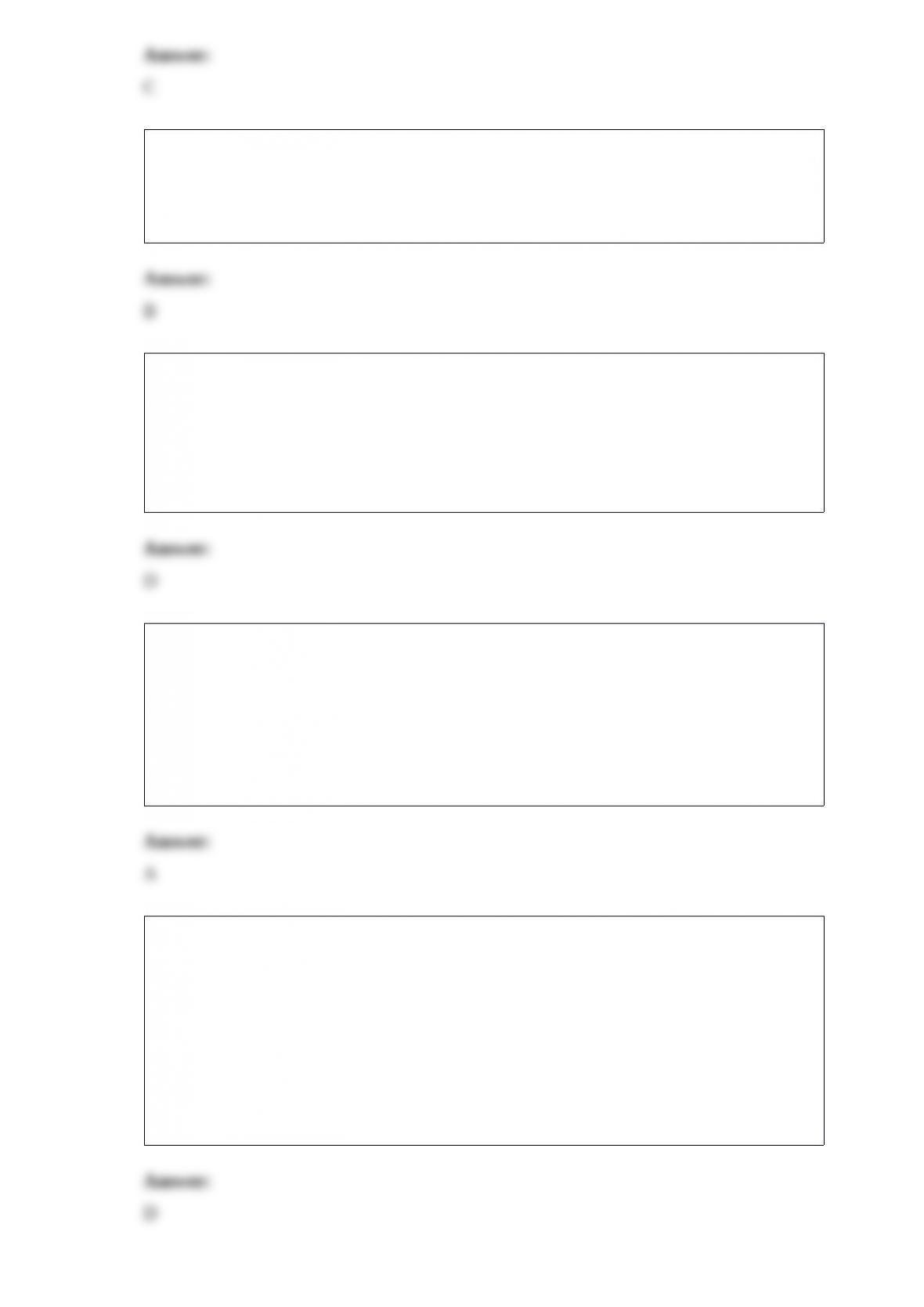

10) The auditor must deal with layers of the computed upper deviation rate from the

attributes table because there are different error assumptions for each error. Assume a

sample of 100 had found one error, and the computed upper deviation rate is shown in

the following table:

The precision limit for the layer with one error is:

A) 2.3%

B) 3.8%

C) 6.1%

D) 1.5%

11) If an auditor were concerned with obtaining evidence about the appropriateness of

the value of inventory, which of the following tests would be most appropriate?

A) compilation tests

B) price tests

C) confirmation of inventory held by outside parties

D) physical examination of the inventory

12) If no material differences are found using analytical procedures and the auditor

concludes that misstatements are not likely to have occurred:

A) other substantive tests may be reduced

B) it will be necessary to increase the tests of balances

C) it will not be necessary to perform tests of balances

D) it will be necessary to increase the tests of transactions

13) You are performing the audit of internal control for Clifton Company. Which of the

following would represent a material weakness in internal control?

A) The company’s audit committee has experienced unusual turnover of members

B) The company’s CFO was indicted for embezzling from the company

C) Bank reconciliations are done monthly

D) The CEO was forced to resign due to an inappropriate relationship with an outside

vendor

14) The audit report date is the date the auditor completed audit procedures in the field.

A) True

B) False

15) A broad interpretation of the rights of third-party beneficiaries holds that users that

the auditor should have been able to foresee as being likely users of financial statements

have the same rights as those with privity of contract. This is known as the concept of:

A) foreseen users

B) foreseeable users

C) expected users

D) four-party contracts

16) An official record of meetings of the board of directors and stockholders is included

in the corporate:

A) bylaws

B) charter

C) minutes

D) license

17) Which of the following statements is not correct regarding probabilistic and

non-probabilistic sample selection?

A) In probabilistic selection, every population item has a known chance of being

selected

B) It is not acceptable to make non-probabilistic evaluations using probabilistic

selection

C) Probabilistic selection is required for all statistical sampling methods

D) Both methods are acceptable and commonly used

18) For cash receipts, the occurrence transaction-related audit objective affects which of

the following balance-related audit objective?

A) Existence

B) Completeness

C) Rights

D) Detail tie-in

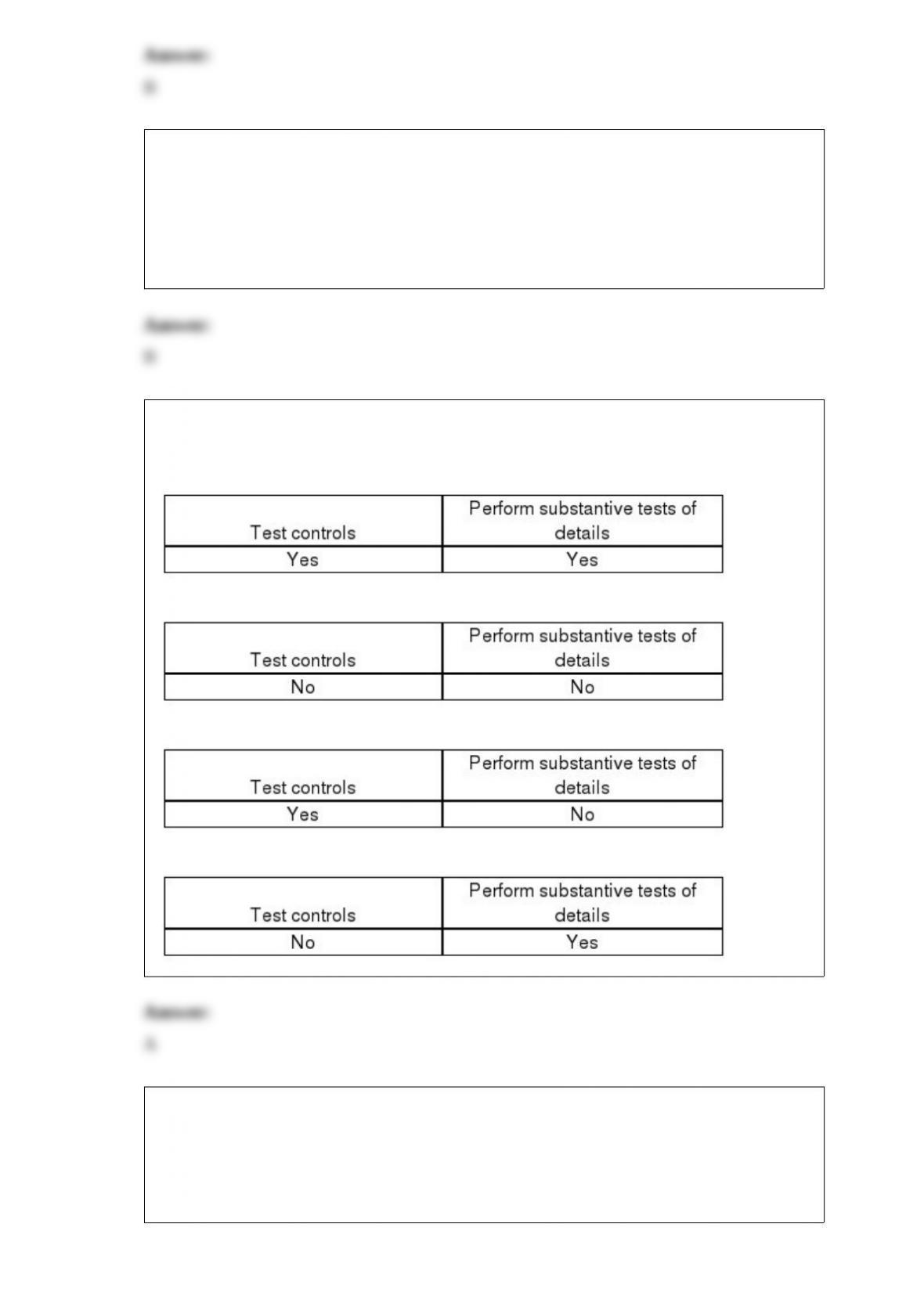

19) Before making the final assessment of internal control at the end of an integrated

audit, the auditor must:

A)

B)

C)

D)

20) Which of the following is not an unqualified opinion with modified wording?

A) Emphasis of a matter

B) Reports involving other auditors

C) Auditor disagrees with client’s departure from GAAP

D) Lack of consistent application of GAAP

21) If inherent risk is increased to medium from low, tests of details of balances can be

reduced.

A) True

B) False

22) Which of the following would be a subsequent discovery of facts which would not

require a response by the auditor?

A) discovery of the inclusion of material nonexistent sales

B) discovery of the failure to write off material obsolete inventory

C) discovery of the omission of a material footnote

D) decrease in the value of investments

23) After general audit objectives are understood, specific audit objectives for each

account balance on the financial statements can be developed. Which of the following

statements is true?

A) There should be at least one specific objective for each relevant general objective

B) There will be only one specific objective for each relevant general objective

C) There will be many specific objectives developed for each relevant general objective

D) There must be one specific objective for each general objective

24) Which of the following statements is not correct?

A) Analytical procedures are used to isolate accounts or transactions that should be

investigated more extensively

B) For certain immaterial accounts, analytical procedures may be the only evidence

needed

C) In some instances, other types of evidence may be reduced when analytical

procedures indicate that an account balance appears reasonable

D) Analytical procedures use supporting documentation to determine which account

balances need additional detailed procedures

25) The results of tests of controls and substantive tests of transactions affect the design

of tests of details of balances.

A) True

B) False

26) Analytical procedures are normally designed at the account level, whereas tests of

controls and substantive tests of transactions are normally designed at the

transaction-related objective level.

A) True

B) False

27) Which of the following is the risk that audit tests will not uncover existing

exceptions in a sample?

A) Sampling risk

B) Nonsampling risk

C) Audit risk

D) Detection risk

28) The audit procedure “Foot the inventory listing schedules for raw materials,

work-in-process, and finished goods” provides assurance mainly for the accuracy

objective for inventory pricing and compilation.

A) True

B) False

29) Early appointment of the independent auditor will enable:

A) a more thorough examination to be performed

B) a proper study and evaluation of internal control to be performed

C) sufficient competent evidential matter to be obtained

D) a more efficient examination to be planned

30) An example of a fraud risk factor describing incentives/pressures is “ineffective

board of director oversight over financial reporting.”

A) True

B) False

31) For audit evidence to be compelling to the auditor it must be sufficient and

appropriate. Which statement below is not correct regarding the appropriateness of

audit evidence?

A) The more effective the internal control system, the more assurance it provides the

auditor about the reliability of financial reporting by the client

B) An auditor’s opinion, to be economically useful and profitable to the auditing firm

needs to be formed within a reasonable time and based on evidence obtained that

assures profits for the auditing firm

C) Evidence obtained from independent sources outside the entity is generally more

reliable than evidence secured solely within the entity

D) The independent auditor’s direct personal knowledge, obtained through inquiry,

observation and inspection, is generally more persuasive than information obtained

indirectly