Revenue is recognized upon sale of gift cards, rather than being deferred.

Stock options will be dilutive and included in the calculation of dilutive EPS if the

exercise price is greater than the average market value of the stock.

Comprehensive income reports an expanded version of income to include certain types

of gains and losses not included in traditional income statements.

Changes in enacted tax rates only affect income tax expense in the years those changes

affect tax payable.

Most, but not all, changes in accounting principle are reported using the retrospective

approach.

The transaction price is only allocated to goods and services that are both capable of

being distinct and that are separately identifiable.

If the seller is a principal, the seller should recognize gross revenue and cost of sales

associated with the transaction.

Long-term debt that is callable by the creditor in the upcoming year should be classified

as a current liability only if the debt is expected to be called.

Under IFRS No. 9, investments for which the investor lacks significant influence use

basically the same reporting classifications as those used under U.S. GAAP.

The balance of net receivables represents the amount expected to be collected.

Determining fair value by calculating the present value of future cash flows is a level 1

type of input.

Unless specific sales criteria are met, the factoring of accounts receivable with recourse

is accounted for as a loan.

The purchase of treasury stock is an investing cash outflow.

The basic issue in deciding whether to record a valuation allowance for a deferred tax

asset is if probable taxable income is anticipated to be insufficient to realize the tax

benefit.

No allocation of contract price is required if the transaction involves a performance

obligation to be satisfied over time.

On March 1, 2016, Doll Co. issued 10-year convertible bonds at 106. During 2019, the

bonds were converted into common stock when the market price of Doll’s common

stock was 500 percent above its par value. Doll prepares its financial statements

according to International Financial Reporting Standards (IFRS). On March 1, 2016,

cash proceeds from the issuance of the convertible bonds should be reported as:

a. A liability for the entire proceeds.

b. Paid-in capital for the entire proceeds.

c. Paid-in capital for the portion of the proceeds attributable to the conversion feature

and as a liability for the balance.

d. A liability for the face amount of the bonds and paid-in capital for the premium over

the par value.

Liabilities payable within the coming year are classified as long-term liabilities if

refinancing is completed before date of issuance of the financial statements under:

a. U.S. GAAP.

b. IFRS.

c. Either U.S. GAAP and IFRS.

d. Neither U.S. GAAP and IFRS.

Under its executive stock option plan, Z Corporation granted options on January 1,

2016, that permit executives to purchase 15 million of the company’s $1 par common

shares within the next eight years, but not before December 31, 2018 (the vesting date).

The exercise price is the market price of the shares on the date of grant, $18 per share.

The fair value of the options, estimated by an appropriate option pricing model, is $4

per option. No forfeitures are anticipated. The options expired in 2022 without being

exercised. By what amount will Z’s shareholder’s equity be increased?

a. $ 60 million

b. $270 million.

c. $315 million.

d. $330 million.

Orange Corp. constructed a machine at a total cost of $70 million. Construction was

completed at the end of 2012 and the machine was placed in service at the beginning of

2013. The machine was being depreciated over a 10-year life using the

sum-of-the-years’-digits method. The residual value is expected to be $4 million. At the

beginning of 2016, Orange decided to change to the straight-line method. Ignoring

income taxes, what will be Orange’s depreciation expense for 2016?

a. $4.8 million.

b. $5.4 million.

c. $6.6 million.

d. $9.4 million.

Fellingham Corporation purchased equipment on January 1, 2014, for $200,000. The

company estimated the equipment would have a useful life of 10 years with a $20,000

residual value. Fellingham uses the straight-line depreciation method. Early in 2016,

Fellingham reassessed the equipment’s condition and determined that its total useful life

would be only six years in total and that it would have no salvage value. How much

would Fellingham report as depreciation on this equipment for 2016?

a. $24,000.

b. $27,333.

c. $36,000.

d. $41,000.

Universal Travel Inc. borrowed $500,000 on November 1, 2016, and signed a 12-month

note bearing interest at 6%. Interest is payable in full at maturity on October 31, 2017.

In connection with this note, Universal Travel Inc. should report interest payable at

December 31, 2016, in the amount of:

a. $ 8,000.

b. $30,000.

c. $ 5,000.

d. $25,000.

Which of the following is not true about accounting for long-term construction

contracts?

a. Long-term construction contracts could show a contract asset or contract liability,

depending on the relation between construction in progress and billings.

b. Billings on contracts in progress is a contra account to accounts receivable.

c. Gross profit is debited to construction in progress.

d. When a customer is billed for payment due, billings on contracts in progress is

credited at the same time accounts receivable is debited.

Pension benefits and postretirement health benefits typically are similar in their:

a. Application of present value concepts.

b. Vesting policies.

c. Coverage for eligible dependents.

d. Relationship between cost of coverage and length of service.

Patrick Rach International issued 5% bonds convertible into shares of the company’s

common stock. Rach applies International Financial Reporting Standards (IFRS). Upon

issuance, Patrick Rach International should record:

a. The proceeds of the bond issue as part debt and part equity.

b. The proceeds of the bond issue entirely as debt.

c. The proceeds of the bond issue entirely as equity.

d. The proceeds of the bond issue entirely as debt if the bonds are mandatorily

redeemable.

The income statement reports changes in fair value for which type of securities?

a. Securities reported under the equity method.

b. Trading securities.

c. Held-to-maturity securities.

d. Securities available for sale.

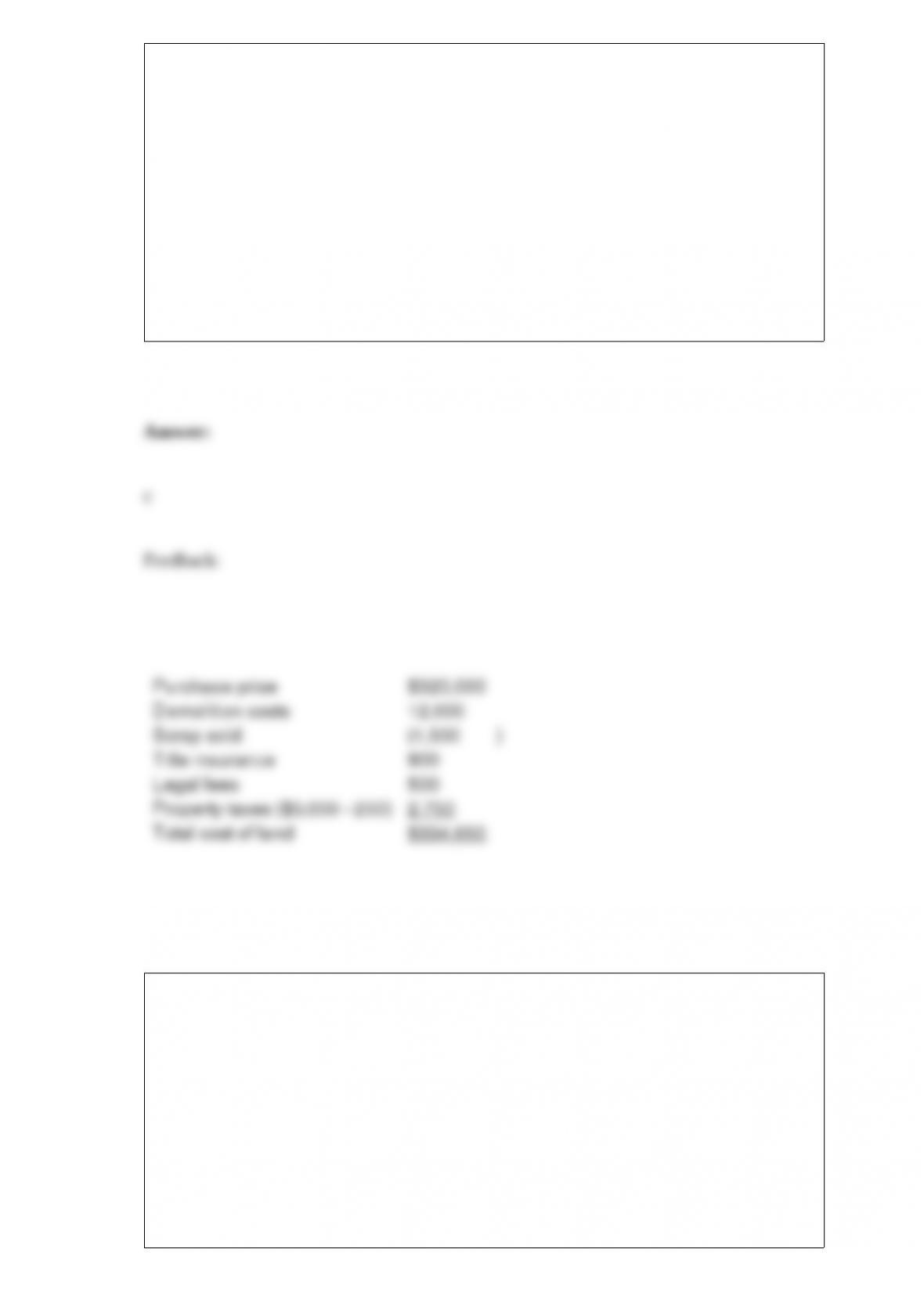

Vijay Inc. purchased a three-acre tract of land for a building site for $320,000. On the

land was a building with an appraised value of $120,000. The company demolished the

old building at a cost of $12,000, but was able to sell scrap from the building for

$1,500. The cost of title insurance was $900 and attorney fees for reviewing the

contract were $500. Property taxes paid were $3,000, of which $250 covered the period

subsequent to the purchase date. The capitalized cost of the land is:

a. $336,400.

b. $336,150.

c. $334,650.

d. $201,150.

Under the dollar-value LIFO retail method, to determine the value of a LIFO layer:

a. Divide the LIFO layer by the layer-year price index and multiply by the layer-year

cost-to-retail percentage.

b. Multiply the LIFO layer by the base year price index and the current year

cost-to-retail percentage.

c. Multiply the LIFO layer by the layer-year price index and by the layer-year

cost-to-retail percentage.

d. Divide the LIFO layer by the layer-year cost-to-retail percentage and multiply by the

layer-year price index.

The following facts apply to TinyPart Toy Company’s pending litigation as of

December 31, 2016: a. TinyPart is defending against a lawsuit and believes there is a

51% chance it will lose in court. If it loses, TinyPart estimates that damages will be

$100,000.

b. TinyPart is defending against another lawsuit for which management believes it is

virtually certain to lose in court. If it loses the lawsuit, management estimates damages

will fall somewhere in the range of $30,000 to $50,000, with each amount in that range

equally likely to occur.

c. TinyPart is defending against another lawsuit that is identical to item (b), but the

relevant losses will only occur far into the future. The present values of the endpoints of

the range are $15,000 and $25,000. TinyPart’s management believes the effects of time

value of money on these amounts are material, but also believes the timing of these

amounts is uncertain.

d. TinyPart is defending against a fourth lawsuit and believes there is only a 25%

chance it will lose in court. If TinyPart loses, it believes damages will fall somewhere in

the range of $35,000 to $40,000, with each amount in that range equally likely to occur.

Indicate how TinyPart would disclose or account for the lawsuit described in part (b)

under U.S. GAAP and under IFRS in the financial statements for the year ended

December 31, 2016.

Peecher accepted a three-year, noninterest-bearing note in exchange for merchandise

sold. Which of the following is true?

a. Peecher would credit a discount on note receivable when recording the sale.

b. Peecher would debit interest revenue over the life of the note.

c. Peecher would debit notes receivable when the note is collected

d. Peecher would multiply sales revenue by the effective interest rate to determine

interest revenue each period

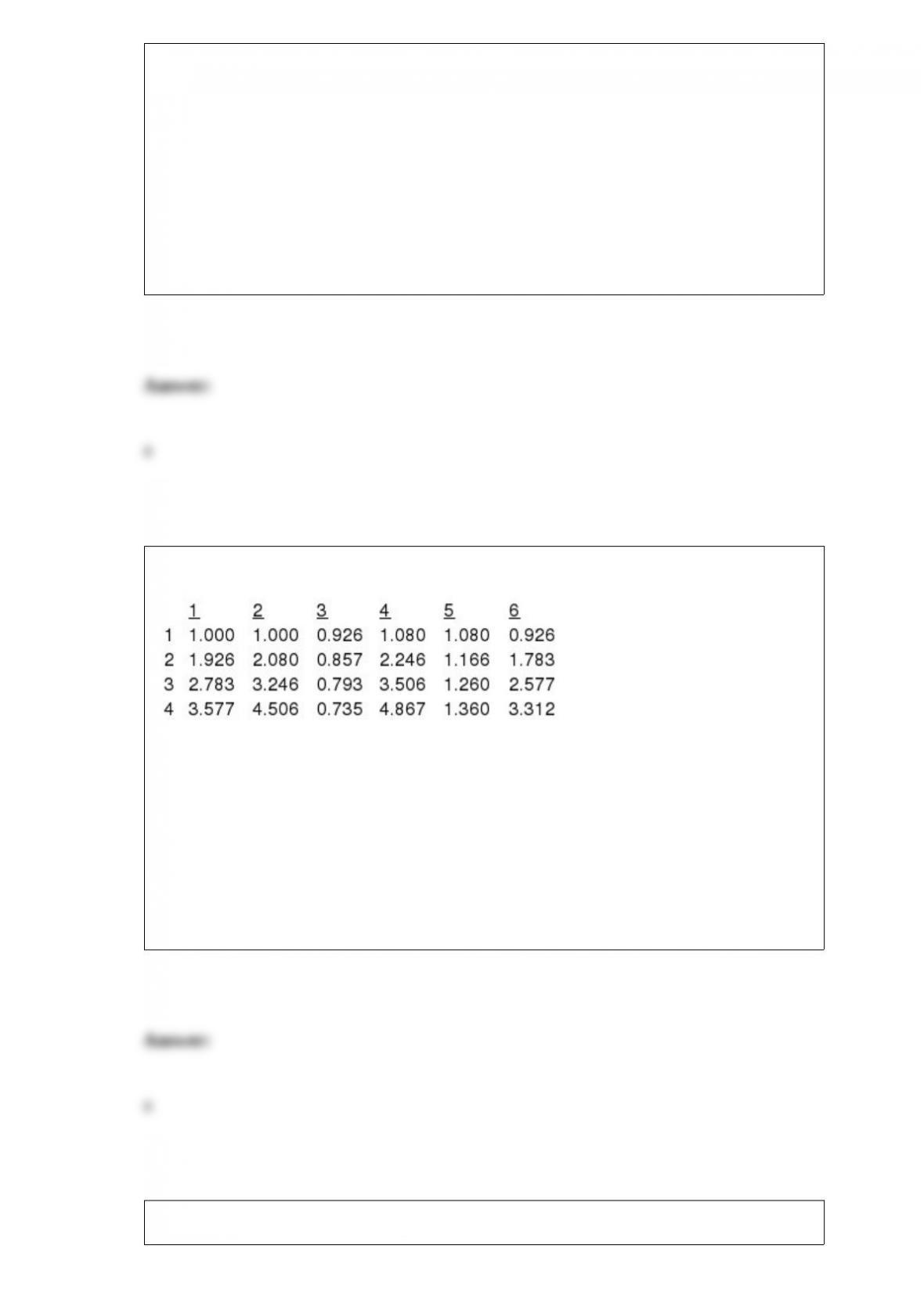

Below are excerpts from time value of money tables for the 8% rate.

Column 3 is an interest table for the:

a. Present value of 1.

b. Future value of 1.

c. Present value of an ordinary annuity of 1.

d. Present value of an annuity due of 1.

Castillo Company has a defined benefit pension plan. At the end of the reporting year,

the following data were available: beginning PBO, $75,000; service cost, $18,000;

interest cost, $5,000; benefits paid for the year, $9,000; ending PBO, $89,000; the

expected return on plan assets, $10,000; and cash deposited with pension trustee,

$17,000. There were no other pension-related costs. The journal entry to record the

annual pension costs will include a credit to the PBO for:

a. $13,000.

b. $17,000.

c. $18,000.

d. $23,000.

General Product Inc. distributed 100 million coupons in 2016. The coupons are

redeemable for 30 cents each. General anticipates that 70% of the coupons will be

redeemed. The coupons expire on December 31, 2017. There were 45 million coupons

redeemed in 2016 and 30 million redeemed in 2017. What was General’s coupon

promotion expense in 2016?

a. $30.0 million.

b. $21.0 million.

c. $13.5 million.

d. $7.5 million.

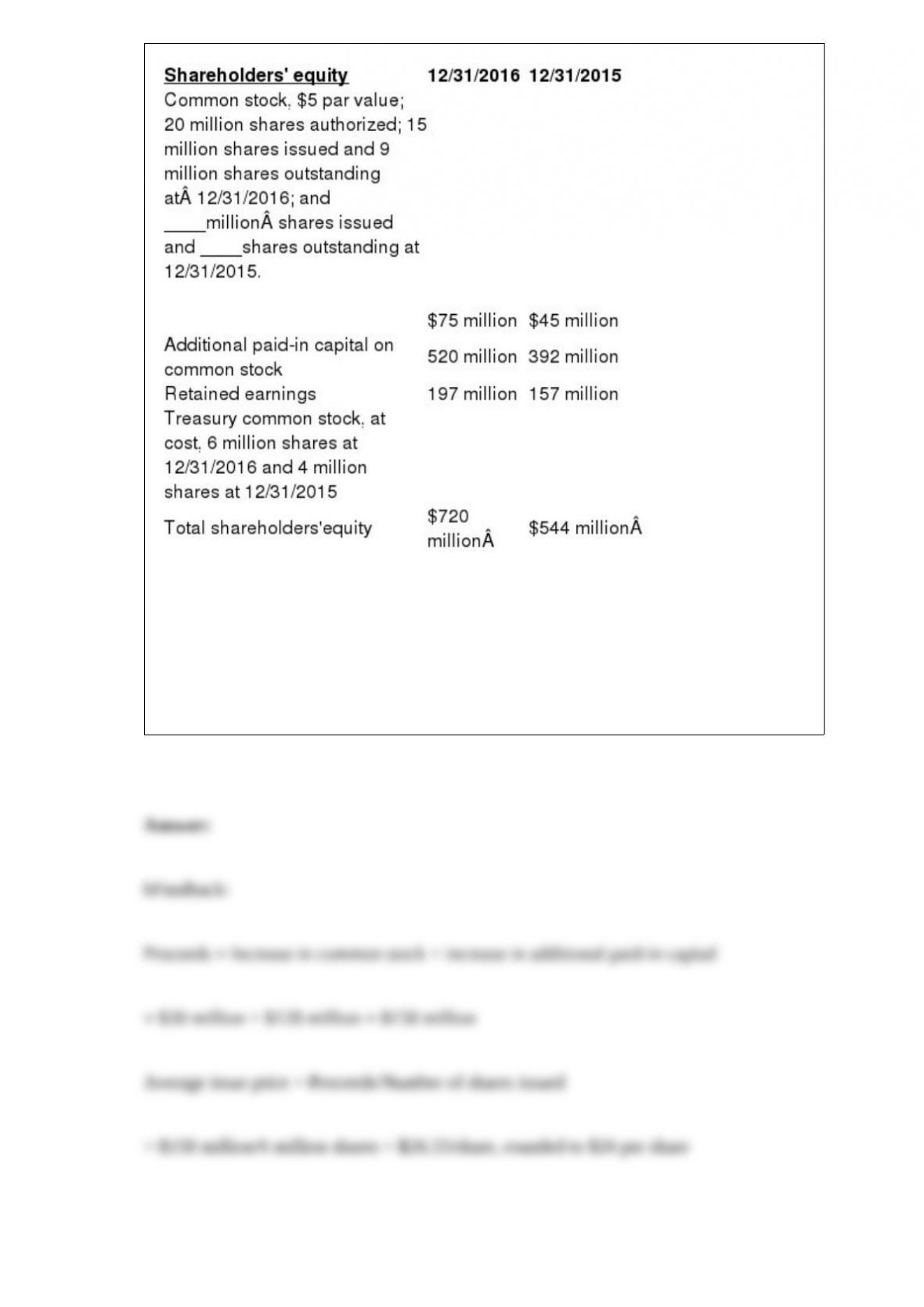

What was the average price (rounded to the nearest dollar) of the additional shares

issued by Levi in 2016?

The following partial information is taken from the comparative balance sheet of Levi

Corporation:

a. $5 per share.

b. $26 per share.

c. $39 per share.

d. Cannot be determined from the given information.

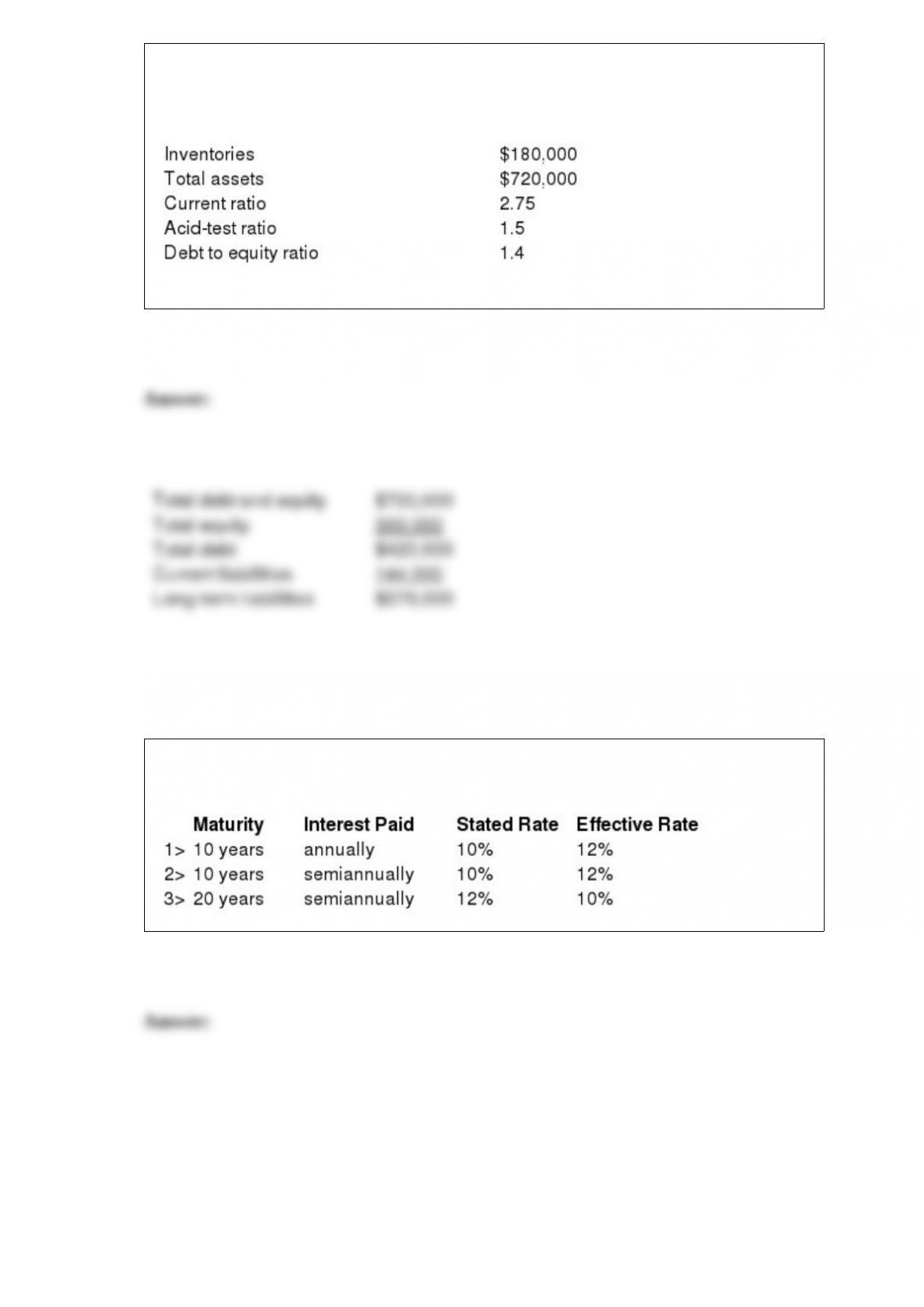

Spartan Sportswear’s current assets consist of cash, marketable securities, accounts

receivable, and inventories. The following data were abstracted from a recent financial

statement:

Required: Compute the following for Spartan: Long-term liabilities

Determine the price of a $500,000 bond issue under each of the following independent

assumptions:

Meca Concrete purchased a mixer on January 1, 2014, at a cost of $45,000.

Straight-line depreciation for 2014 and 2015 was based on an estimated eight-year life

and $3,000 estimated residual value. In 2016, Meca revised its estimate and now

believes the mixer will have a total service life of only six years, and that the residual

value will be only $2,000.

Required:

Compute depreciation for 2016 and 2017.

Prepare a list of how retiree health benefits differ from pension benefits with respect to

accounting, funding, regulation, and employee benefits.

Briefly explain the advantages of dollar-value LIFO (DVL).

CompuTime Center sells a full assortment of computer parts, including motherboards,

video cards, and cables. It also offers complementary computer assembly services. A

customer places an order for an advanced workstation, and CompuTime asks for

$3,500. If CompuTime were to sell only the parts in an advanced workstation, with no

assembly, the price would be $3,300.

Required: Assuming that computer parts and assembly service are separate

performance

obligations, estimate the stand-alone selling price of the assembly service based on the

residual

approach.

Explain briefly how IFRS and U.S. GAAP differ in determining whether a transfer of

an accounts receivable qualifies as a sale.

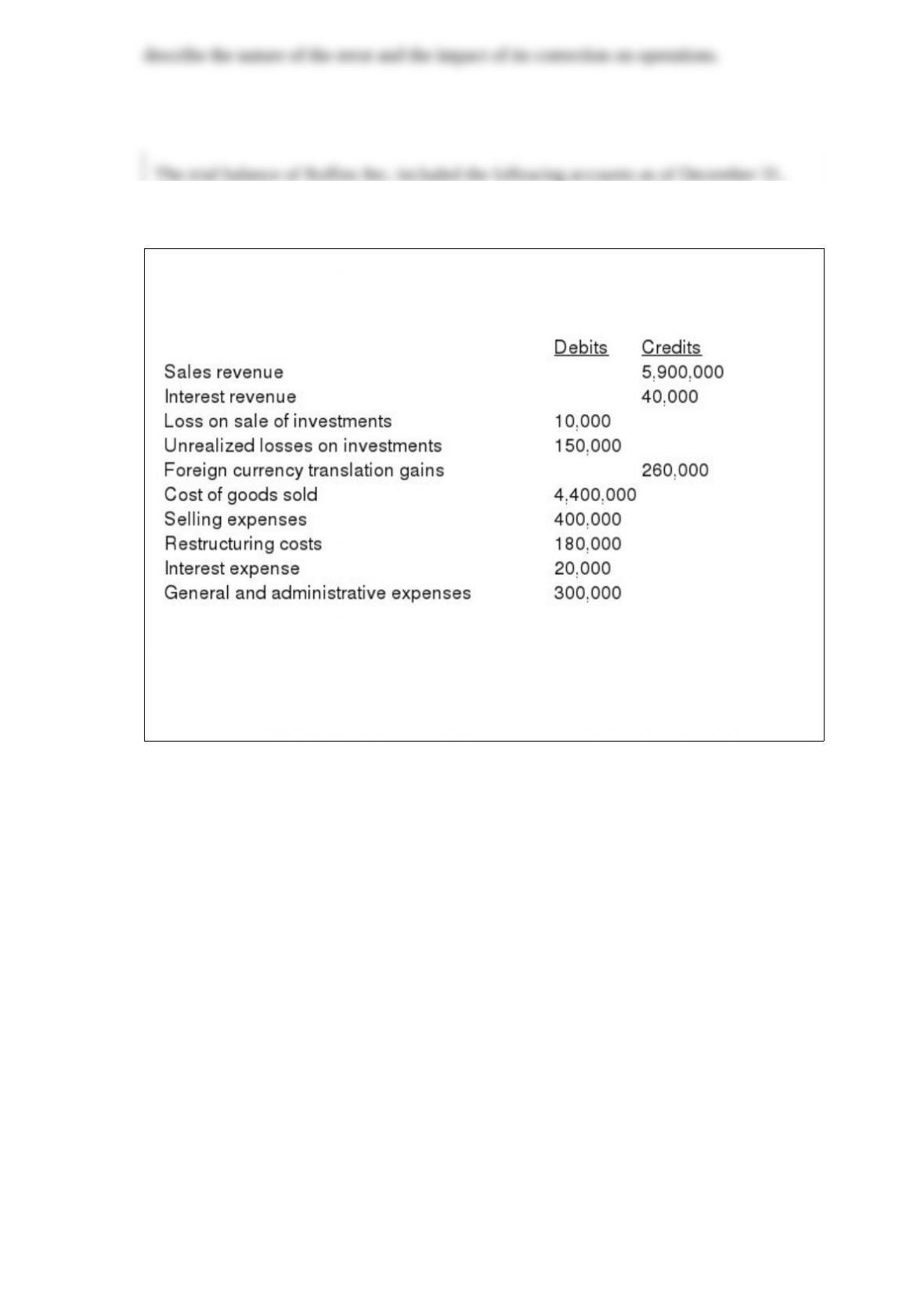

Describe the way we account for an error when that error is discovered in a subsequent

reporting period.

The trial balance of Rollins Inc. included the following accounts as of December 31,

2016:

Rollins had 100,000 shares of stock outstanding throughout the year. Income tax

expense has not yet been accrued. The effective tax rate is 40%.

Required: Prepare a 2016 single, continuous statement of comprehensive income for

Rollins Inc. Use a multiple-step income statement format.