Before making adjusting entries at the end of an accounting period, some accounts may

not show proper financial statement amounts even though all transactions were

correctly recorded.

The work sheet is used to record transactions as they occur.

For a business, provincial sales tax (PST) paid is included in the amount recorded as an

asset or an expense when a purchase is made.

The balance sheet shows whether or not the firm achieved its primary objective of

earning a profit.

A contingent liability is an obligation to make a future payment if an uncertain future

event occurs.

Items posted from the General Journal carry the initial P.

There is no difference in the amount of inventory calculated by the periodic and

perpetual inventory systems when using FIFO or weighted average cost flow

assumptions.

Trade discounts are entered into the accounting system.

Closing entries are normally entered in the General Journal and then recorded on the

work sheet.

Unlimited liability is an advantage for both a proprietorship and a partnership.

The clerk who has access to the cash in the cash register should not have access to the

register tape or file.

Firms have the option of recording credit card expense as a discount from sales or as a

selling expense.

Reversing entries are prepared to adjust accrued assets and liabilities that were created

by adjusting entries at the end of the previous reporting period.

In applying LCNRV, net realizable value is defined as the sales price less costs incurred

to make the sale.

A high accounts receivable turnover rate in comparison with that of competitors’

suggests that the firm should tighten its credit policy.

Most businesses apply the lower of cost and net realizable value rule to groups of

similar or related items.

A journal entry with a debit to cash of $980, a debit to Sales Discounts of $20, and a

credit to Accounts Receivable of $1,000 means that a customer has taken a 10% cash

discount for early payment.

A payee of a note usually honours a note and pays it in full.

Adjusting entries are posted to the general ledger.

Harley Ravidson’s current assets are $400 million and its current liabilities are $250

million. Its current ratio is .63 to 1.

At the end of the day, the cash register shows a balance of $635. The cash drawer has a

balance of $650. The difference of $15 should be debited to miscellaneous expense.

When purchase prices do not change, the choice of an inventory costing method is

unimportant.

Adjusting entries may affect only balance sheet accounts.

A management information system (MIS) is designed to collect and process data within

an organization for the purpose of providing users with information.

As a rule, revenues should not be recognized in the accounting records until received in

cash.

Step Two of the accounting cycle requires that we record transactions in a record called

a journal.

In a period of inflation, FIFO usually gives a lower taxable income and thus a tax

advantage.

International Accounting Standards have been created to improve comparability of

accounting information across countries.

The natural business year can only be used when the seasonal variation in sales does not

match the calendar year.

The inventory cost flow assumption that is used cannot have a material impact on the

financial statements.

An owner’s cash investment in a business creates an asset (cash), a liability (note

payable), and equity (owner investments).

Accounting is an information system that identifies, measures, records and

communicates relevant information that faithfully represents an organization’s

economic activities.

The Sales Journal and Cash Receipts Journal may have GST payable and PST payable

columns added to them to facilitate recording.

Cost of goods sold is:

A. Another term for net sales.

B. The term used for the cost of buying and preparing merchandise.

C. An operating expense.

D. Also called gross margin.

E. The cost of goods sold to customers.

During the month of November, Cornish Company had cash receipts of $3,500 and paid

out $1,000 for expenses. The November 30th cash balance was $4,300. What was the

cash balance on November 1?

A. $1,800.

B. $2,800.

C. $4,300.

D. $5,800.

E. $7,300.

The days’ sales uncollected ratio is calculated by:

A. Dividing accounts receivable by net sales.

B. Dividing accounts receivable by net sales and multiplying the result by 365.

C. Dividing net sales by accounts receivable.

D. Dividing net sales by accounts receivable and multiplying the result by 365.

E. Multiplying net sales by accounts receivable and dividing the result by 365.

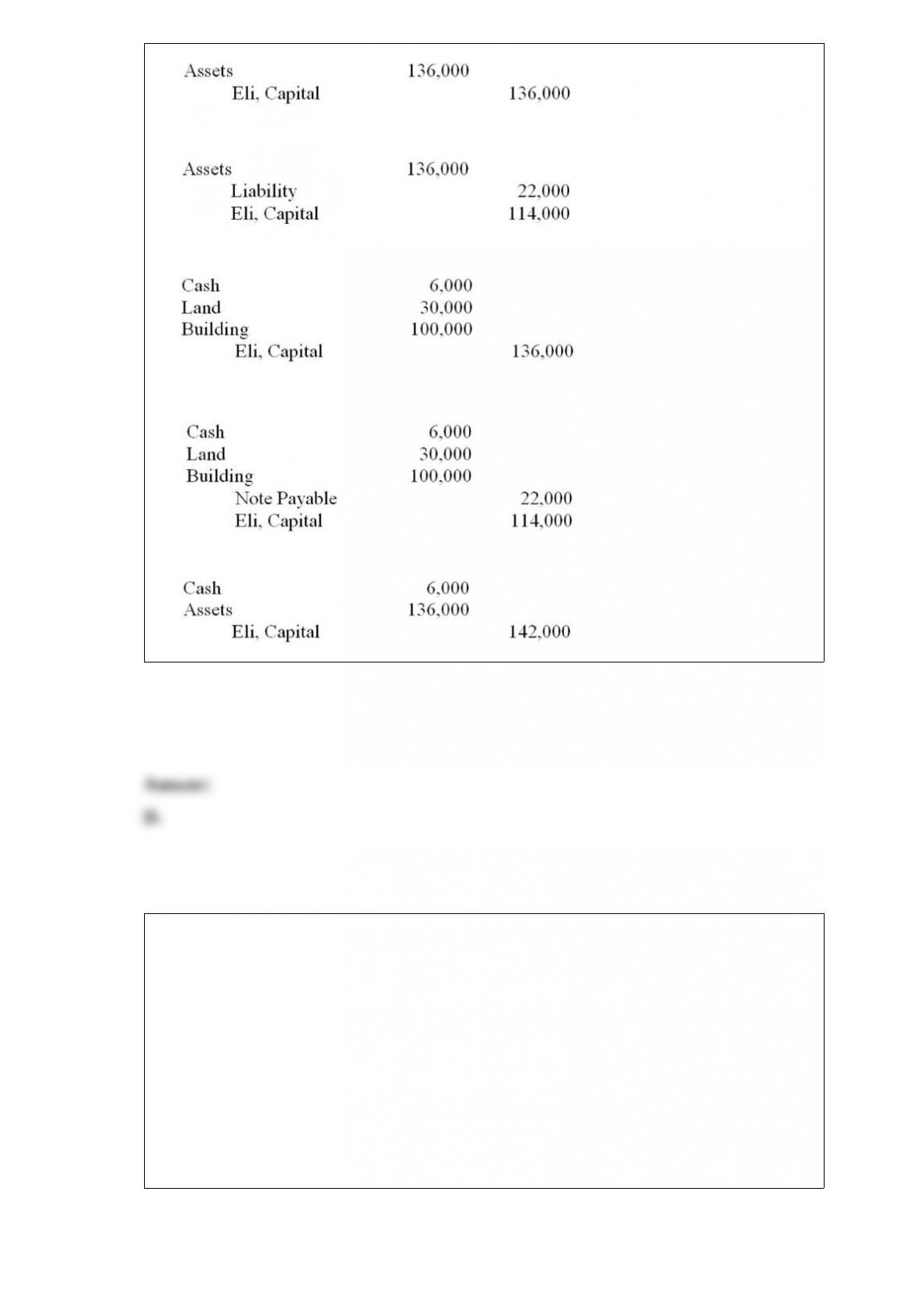

Eli opened a new business by investing the following assets: cash, $6,000; land,

$30,000; building, $100,000. Also, the business will assume responsibility for a note

payable of $22,000. Eli signed the note as part of his payment for the land and building.

Which journal entry should be used on the books of the new business to record the

investment by Eli?

A.

B.

C.

D.

E.

Risks involved in e-commerce include:

A. Firewalls.

B. Encryption.

C. Missing documents.

D. Computer viruses.

E. All of these answers are correct.

Internal documents prepared by accountants when organizing the information presented

in formal reports to internal and external decision makers are called:

A. Adjusting papers.

B. Statement papers.

C. Working papers.

D. Closing papers.

E. Business papers.

An Accounts Payable subledger is:

A. A subsidiary ledger that contains an account for each supplier that grants credit to the

company.

B. A list of the balances of all the accounts in the Accounts Receivable ledger that is

added to show the total amount of accounts receivable outstanding.

C. A book of original entry that is designed and used for recording only a specified type

of transaction.

D. The ledger that contains the financial statement accounts of a business.

E. A subsidiary ledger that contains a separate account for each customer that grants

credit to the company.

Merchandisers:

A. Earn net income from buying and selling merchandise.

B. Receive fees in exchange for services.

C. Earn net income from commissions.

D. Earn net income from fares.

E. Do not report gross profit.

A book of original entry is:

A. A book in which amounts are posted from a journal.

B. Another name for the cash account.

C. Another name for the general journal.

D. Also called a ledger.

E. Sometimes called a book of final entry.

One difference in the Sales Journal between the perpetual and periodic systems is:

A. The column to record cost of goods sold and inventory amounts sold.

B. The addition of a sales tax payable column.

C. The deletion of a sales tax payable column.

D. The column to record cost of goods sold and inventory amounts sold and the deletion

of a sales tax payable column.

E. The column to record cost of goods sold and inventory amounts sold and the addition

of a sales tax payable column.

Adjusting entries are journal entries made at the end of an accounting period for the

purpose of:

A. Updating related liability and asset accounts.

B. Assigning revenues to the period in which they are earned.

C. Assigning expenses to the period in which the expiration of benefit has incurred.

D. Recording internal transactions.

E. All of these answers are correct.

Unearned revenue is reported in the financial statements as:

A. A revenue on the balance sheet.

B. A liability on the balance sheet.

C. An unearned revenue on the income statement.

D. An asset on the balance sheet.

E. An operating activity on the statement of cash flows.

A journal in which transactions are first recorded is:

A. A book of original entry.

B. A ledger.

C. A book of final entry.

D. A revenue account.

E. The cash ledger.

The difference between a company’s assets and its liabilities, or the residual interest in

the assets of an entity that remains after deducting its liabilities, is called:

A. Net income.

B. Shares.

C. Equity.

D. Revenue.

E. Net loss.

An exchange between two parties of economic consideration such as goods, services,

money, or rights to collect money is called:

A. The accounting equation.

B. Bookkeeping.

C. A business transaction.

D. An audit.

E. A gift.

On May 1, 2015. Bee Advertising Company received $2,500 from Julie Cee for

advertising services to be completed by April 30, 2016. Assume the receipt was

recorded as unearned fees and that at December 31, 2015, $1,000 of the fees had been

earned. The adjusting entry prepared by Bee on December 31, 2015, should include:

A. A debit to Unearned Fees for $500.

B. A credit to Unearned Fees for $500.

C. A credit to Earned Fees for $1,000.

D. A debit to Earned Fees for $1,000.

E. A debit to Earned Fees for $500.

(A) In a sole proprietorship, Income Summary is closed to what account? (B) In

following the steps of the accounting cycle, what two steps must be done before

preparation of an unadjusted trial balance?

Acceptable inventory cost flow assumptions in Canada include:

A. FIFO.

B. Specific identification.

C. Weighted-average method.

D. FIFO and specific identification.

E. All of these answers are correct.

The length of time covered by periodic financial statements and other reports is the:

A. Fiscal year.

B. Natural business year.

C. Accounting period.

D. Business cycle.

E. Operating cycle.

The Income Summary account is used:

A. To adjust and update asset accounts.

B. To close the revenue and expense accounts.

C. To determine the appropriate withdrawal amount.

D. To replace the income statement under certain circumstances.

E. To replace the capital account in some businesses.

The normal order for the asset section of a classified balance sheet is:

A. Current assets, prepaid expenses, long-term investments, intangible assets.

B. Long-term investments, current assets, property, plant and equipment, intangible

assets.

C. Current assets, long-term investments, property, plant and equipment, intangible

assets.

D. Intangible assets, current assets, long-term investments, property, plant and

equipment.

E. Property, plant and equipment, intangible assets, long-term investments, current

assets.

Businesses can take the following form(s):

A. Sole proprietorship.

B. Not-for-profit.

C. Partnership.

D. Sole proprietorship and partnership.

E. All of these answers are correct.

An analysis that explains the difference between the balance of a chequing account

shown in the depositor’s records and the balance shown on the bank statement is a(n):

A. Internal audit.

B. Bank reconciliation.

C. Bank audit.

D. Trial reconciliation.

E. Analysis of debits and credits.

On July 1, 2015, Nuby Trucking Company purchased a new truck for $52,000. The

truck is estimated to have a useful life of six years and a residual value of $10,000. How

much depreciation expense will be recorded for the truck during the year ended

December 31, 2015?

A. $3,000.

B. $3,500.

C. $4,000.

D. $6,000.

E. $7,000.

Expenses that support the overall operations of a business and include the expenses of

such activities as providing accounting services, human resource management, and

financial management are called:

A. Operating expenses.

B. Selling expenses.

C. Purchasing expenses.

D. General and administrative expenses.

E. Miscellaneous expenses.

Interest on $8,400 at 7% for 60 days is:

A. $36.45

B. $41.42

C. $52.65.

D. $65.25.

E. $96.66.

In which of the following situations would the trial balance not balance?

A. A $1,000 collection of an account receivable was incorrectly posted as a debit to

Accounts Receivable and a credit to Cash.

B. The purchase of office supplies on account for $3,250 was incorrectly recorded in

the journal as $2,350.

C. $50 cash receipt for the performance of a service was not recorded.

D. The purchase of office equipment for $1,200 was posted as a debit to Office

Supplies.

E. The payment of a $750 account payable was posted as a debit to Accounts Payable

and a debit to Cash for $750.

On January 1, 2015, Peach Company purchased a five-year insurance policy for $5,000.

If the cost was debited to Prepaid Insurance, the adjusting entry at the end of 2015 is:

A. Debit Prepaid Insurance, $1,800; credit Cash, $1,800.

B. Debit Prepaid Insurance, $1,000; credit Insurance Expense, $1,000.

C. Debit Prepaid Insurance, $360; credit Insurance Expense, $360.

D. Debit Insurance Expense, $360; credit Prepaid Insurance, $360.

E. Debit Insurance Expense, $1,000, credit Prepaid Insurance $1,000.

Cash equivalents:

A. Include savings accounts.

B. Include chequing accounts.

C. Are short-term investments that a company invests their cash in to increase their

earnings.

D. Include savings and chequing accounts.

E. All of these answers are correct.

The consistency principle:

A. Requires a company to use the same accounting methods period after period.

B. Requires a company to use one cost flow assumption exclusively.

C. Allows a company to change its cost flow assumption period after period in order to

maximize net income.

D. Is also called the matching principle.

E. Allows a company to change its cost flow assumption period after period in order to

minimize income taxes.

Lang leased a portion of its store to Pang for 12 months beginning on November 1, at a

monthly rate of $400. Pang paid the entire $4,800 on November 1, which Lang

recorded as unearned revenue. The journal entry made by Lang at year-end, December

31, would include:

A. A debit to Rent Earned for $400.

B. A credit to Unearned Rent for $400.

C. A debit to Cash for $800.

D. A credit to Rent Earned for $800.

E. A debit to Unearned Rent for $4,800.

Match the following terms with the appropriate definition.

Describe a work sheet and explain why it is useful.

Explain the difference between the book value and the market value of an asset.

A current ratio of 1.1 suggests that a company has ____________ current assets to

cover current liabilities.

Explain the difference between honouring and dishonouring a note receivable.

The accounting process for the trial balance includes (1) preparing journal entries, (2)

______________________, (3) calculating account balances, (4)

_________________________, and (5) totalling the trial balance columns.

How does the going concern principle affect reporting asset values of a business?

Prepaid expenses, depreciation, and unearned revenues each reflect transactions where

cash is received or paid ______________ a related expense or revenue is recognized.

The _____________________ method is used to estimate the value of inventory that

has been destroyed, lost, or stolen.

A parcel of land is offered for sale at $135,000, is assessed for tax purposes at $60,000,

is recognized by its purchasers as easily being worth $108,000, and is purchased for

$106,000. At what amount should the land be recorded in the purchaser’s books? What

accounting principle supports your answer?

Lionel’s Laundry has assets of $180,000 and liabilities of $120,000. Calculate the

amount of equity.

What types of costs are assigned to merchandise inventory?

_______________ is the process of transferring journal entry information to the ledger.