1) a company that makes horsehair cowboy belts cannot meet the demand for belts due

to a limited supply of artisans who know how to make the belts. to determine which

models of the cowboy belts should be emphasized, the company should rank the models

by dividing the selling price of each model by the amount of time an artisan requires to

make the model.

2) only credit sales (i.e., sales on account) are included in the computation of the

accounts receivable turnover.

3) when the predetermined overhead rate is based on direct labor-hours, the amount of

overhead applied to a job is proportional to the amount of actual direct labor-hours

incurred on the job.

4) as total sales increase beyond the break-even point, the degree of operating leverage

will also increase.

5) the fact that the high-low method uses only two data points is a major defect of the

method.

6) defective units should be detected and scrapped or reworked after the bottleneck

operation rather than before it.

7) data concerning hahl corporation’s single product appear below:

the break-even in monthly dollar sales is closest to:

a.$485,800

b.$634,060

c.$1,081,360

d.$335,160

8) strap company uses the weighted-average method in its process costing system. the

company has only one processing department. the ending work in process inventory

consists of 10,000 units, 60% complete with respect to materials. the total dollar value

of this inventory is $38,000. the costs per equivalent unit are $5.00 for materials and

$4.00 for conversion costs for the period. with respect to conversion costs, the ending

work in process inventory is:

a.10% complete

b.20% complete

c.38% complete

d.30% complete

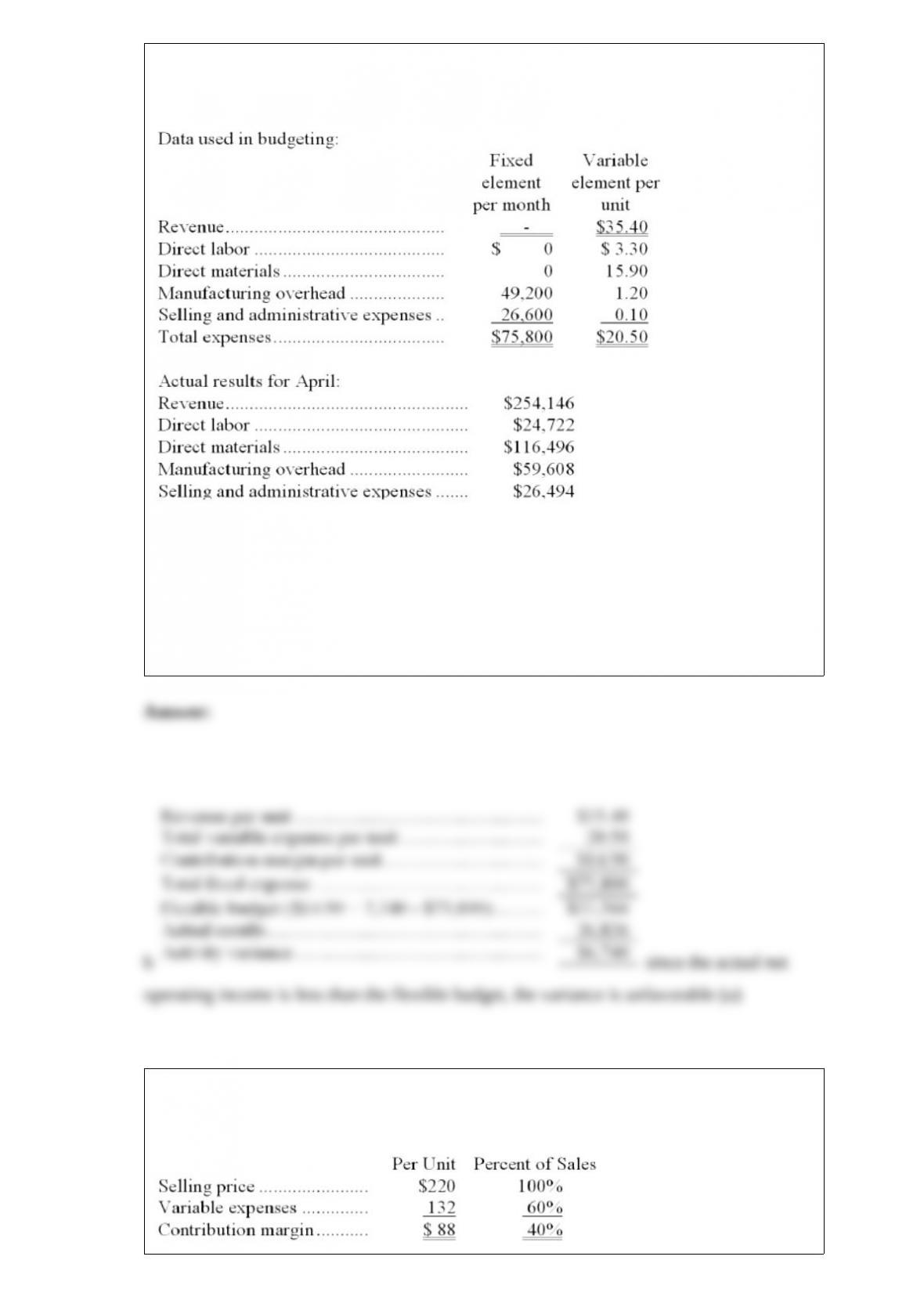

9) vandall corporation manufactures and sells a single product. the company uses units

as the measure of activity in its budgets and performance reports. during april, the

company budgeted for 7,300 units, but its actual level of activity was 7,340 units. the

company has provided the following data concerning the formulas used in its budgeting

and its actual results for april:

the overall revenue and spending variance (i.e., the variance for net operating income in

the revenue and spending variance column on the flexible budget performance report)

for april would be closest to:

a.$6,144 f

b.$6,740 u

c.$6,740 f

d.$6,144 u

10) hinsey corporation produces and sells a single product. data concerning the product

appear below:

fixed expenses are $300,000 per month. the company is currently selling 4,000 units per

month. consider each of the following questions independently.

this question is to be considered independently of all other questions relating to hinsey

corporation. refer to the original data when answering this question.

the marketing manager would like to cut the selling price by $13 and increase the

advertising budget by $21,000 per month. the marketing manager predicts that these

two changes would increase monthly sales by 900 units. what should be the overall

effect on the company’s monthly net operating income of this change?

a.increase of $46,500

b.decrease of $46,500

c.increase of $165,300

d.decrease of $5,500

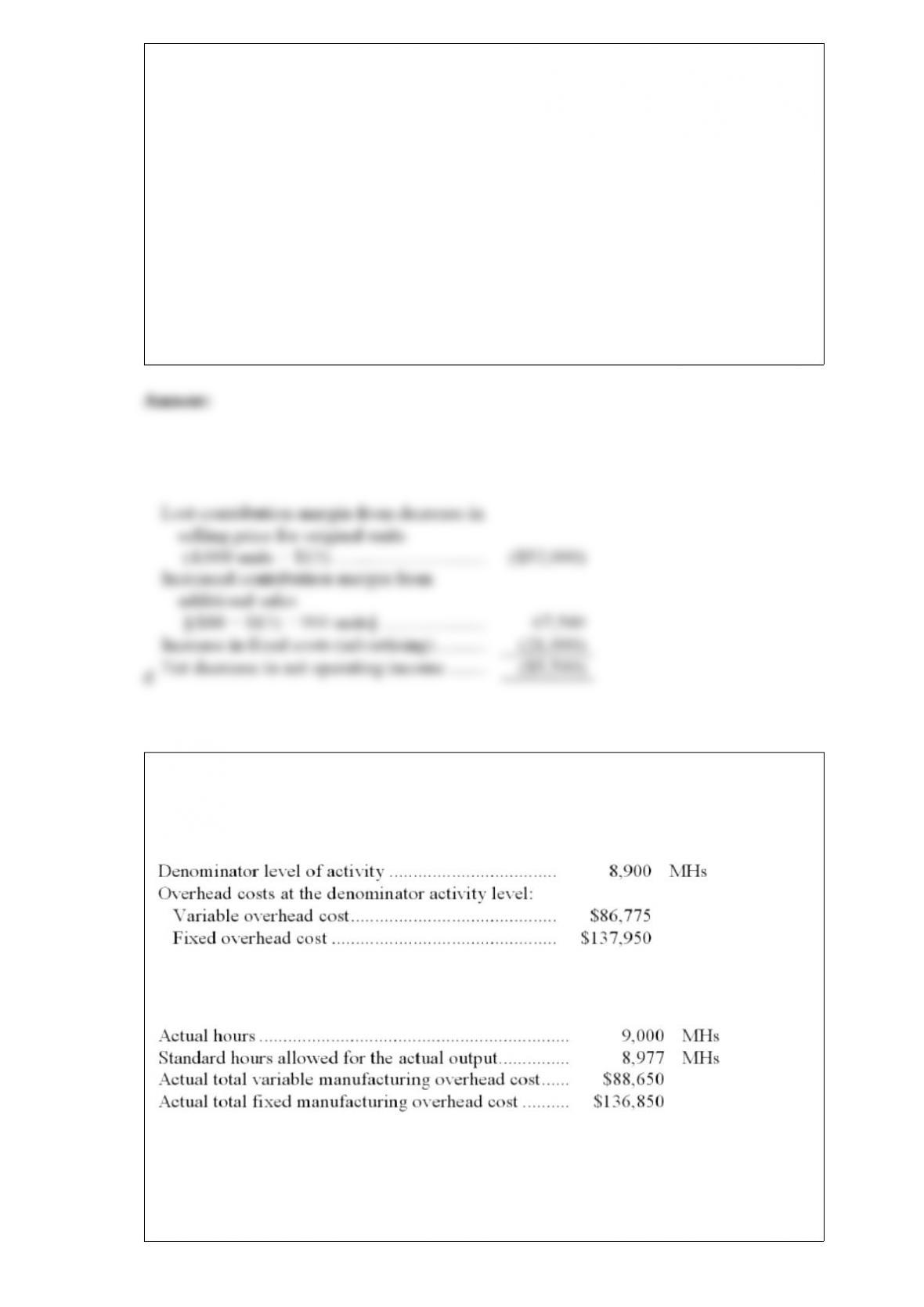

11) a manufacturing company uses a standard costing system in which standard

machine-hours (mhs) is the measure of activity. data from the company’s flexible

budget for manufacturing overhead are given below:

the following data pertain to operations for the most recent period:

how much overhead was applied to products during the period to the nearest dollar?

a.$225,500

b.$227,250

c.$224,725

d.$226,669

12) which of the following should be classified as a financing activity on a statement of

cash flows?

a.direct exchange transactions involving common stock

b.interest paid on a long-term notes payable

c.a loan made to a long time supplier of component parts

d.both a and c above

e.none of these

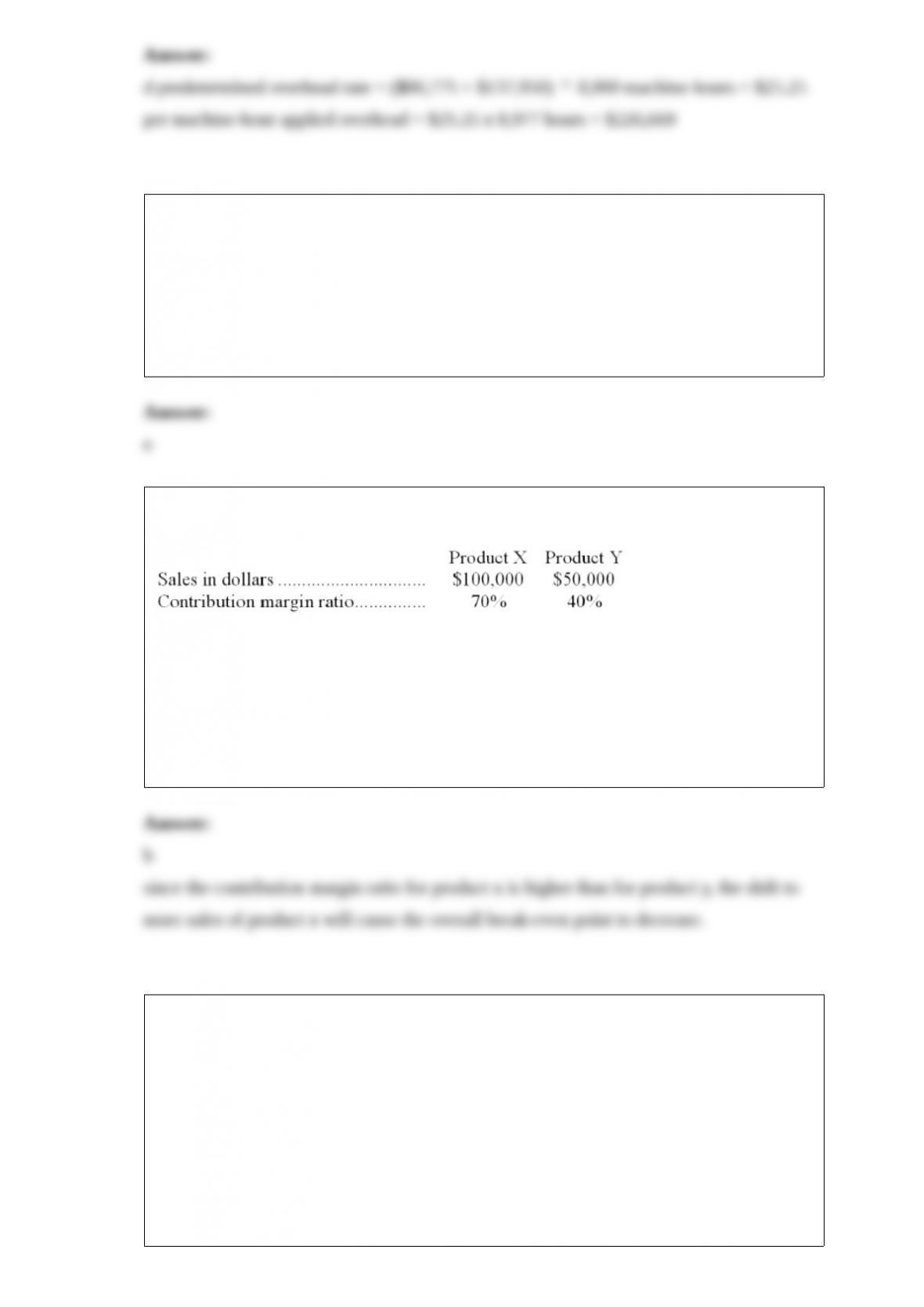

13) the following data concern two products sold by redding corporation.

if the sales mix shifts toward product x, and product contribution margin ratios remain

unchanged, one would expect the break-even point for the company as a whole to:

a.increase

b.decrease

c.remain unchanged

d.it is impossible to determine

14) (ignore income taxes in this problem.) denny corporation is considering replacing a

technologically obsolete machine with a new state-of-the-art numerically controlled

machine. the new machine would cost $450,000 and would have a ten-year useful life.

unfortunately, the new machine would have no salvage value. the new machine would

cost $20,000 per year to operate and maintain, but would save $100,000 per year in

labor and other costs. the old machine can be sold now for scrap for $50,000. the simple

rate of return on the new machine is closest to:

a.8.75%

b.20.00%

c.7.78%

d.22.22%

15) keppler corporation applies manufacturing overhead to products on the basis of

standard machine-hours. the company’s cost formula for variable overhead cost is $4.90

per machine-hour. the actual variable overhead cost for the month was $25,160. the

original budget for the month was based on 5,000 machine-hours. the company actually

worked 5,320 machine-hours during the month. the standard hours allowed for the

actual output of the month totaled 5,220 machine-hours. what was the variable

overhead efficiency variance for the month?

a.$1,078 unfavorable

b.$490 unfavorable

c.$418 favorable

d.$908 favorable

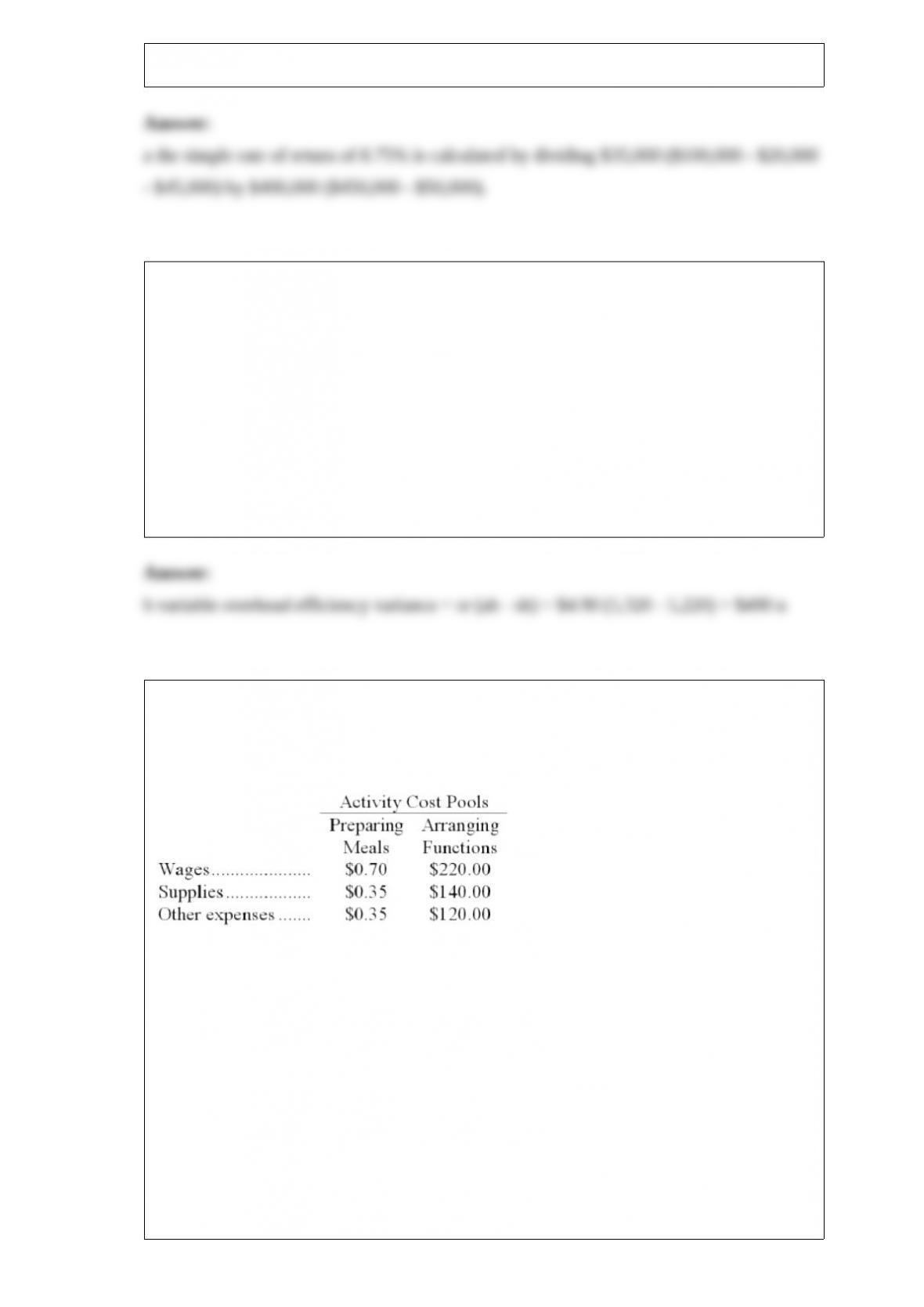

16) grodin catering uses activity-based costing for its overhead costs. the company has

provided the following data concerning the activity rates in its activity-based costing

system:

the number of meals served is the measure of activity for the preparing meals activity

cost pool. the number of functions catered is used as the activity measure for the

arranging functions activity cost pool.

management would like to know whether the company made any money on a recent

function at which 180 meals were served. the company catered the function for a fixed

price of $15.00 per meal. the cost of the raw ingredients for the meals was $9.65 per

meal. this cost is in addition to the costs of wages, supplies, and other expenses detailed

above.

for the purposes of preparing action analyses, management has assigned ease of

adjustment codes to the costs as follows: wages are classified as a yellow cost; supplies

and raw ingredients as a green cost; and other expenses as a red cost.

suppose an action analysis report is prepared for the function mentioned above. what

would be the “yellow margin” in the action analysis report? (round to the nearest whole

dollar.)

a.$489

b.$414

c.$539

d.$594

17) roal corporation manufactures a product that has the following costs:

the company uses the absorption costing approach to cost-plus pricing as described in

the text. the pricing calculations are based on budgeted production and sales of 37,000

units per year.

the company has invested $220,000 in this product and expects a return on investment

of 9%.

required:

a. compute the markup on absorption cost.

b. compute the selling price of the product using the absorption costing approach.

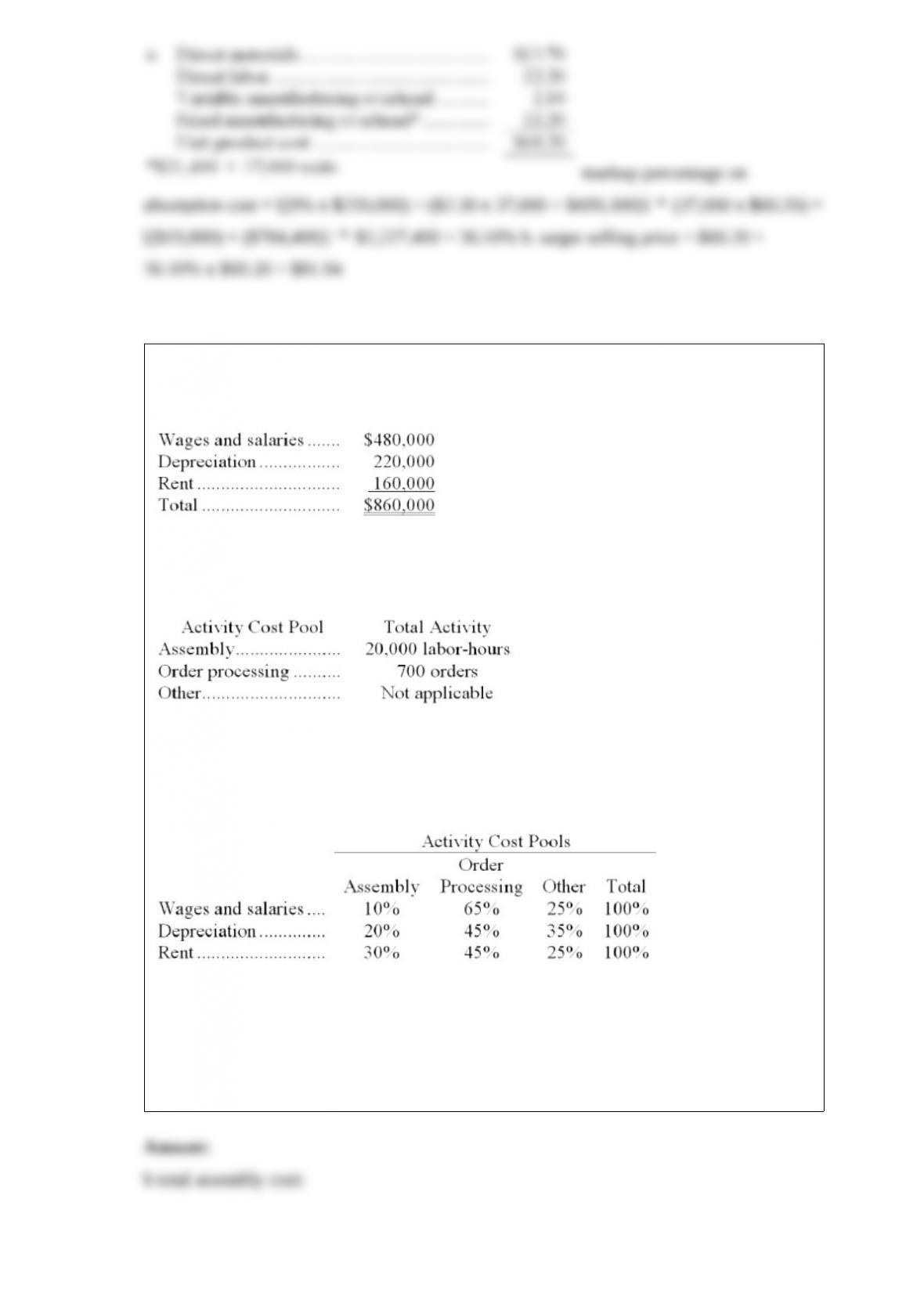

18) whiting corporation has provided the following data concerning its overhead costs

for the coming year:

the company has an activity-based costing system with the following three activity cost

pools and estimated activity for the coming year:

the other activity cost pool does not have a measure of activity; it is used to accumulate

costs of idle capacity and organization-sustaining costs.

the distribution of resource consumption across activity cost pools is given below:

the activity rate for the assembly activity cost pool is closest to:

a.$4.30 per labor-hour

b.$7.00 per labor-hour

c.$8.60 per labor-hour

d.$12.90 per labor-hour

19) cardwell corporation manufactures a variety of products. last year, the company’s

variable costing net operating income was $63,900 and ending inventory increased by

900 units. fixed manufacturing overhead cost per unit was $3.

required:

determine the absorption costing net operating income for last year. show your work!

20) payment inc. is preparing its cash budget for february. the budgeted beginning cash

balance is $27,000. budgeted cash receipts total $136,000 and budgeted cash

disbursements total $128,000. the desired ending cash balance is $50,000. the company

can borrow up to $110,000 at any time from a local bank, with interest not due until the

following month.

required:

prepare the company’s cash budget for february in good form. make sure to indicate

what borrowing, if any, would be needed to attain the desired ending cash balance.

21) bauerkemper inc. is considering a project that would require an initial investment of

$924,000 and would have a useful life of 7 years. the annual cash receipts would be

$693,000 and the annual cash expenses would be $347,000. the salvage value of the

assets used in the project would be $92,000. the company’s tax rate is 30%. for tax

purposes, the entire initial investment without any reduction for salvage value will be

depreciated over 5 years. the company uses a discount rate of 17%.

required:

compute the net present value of the project.

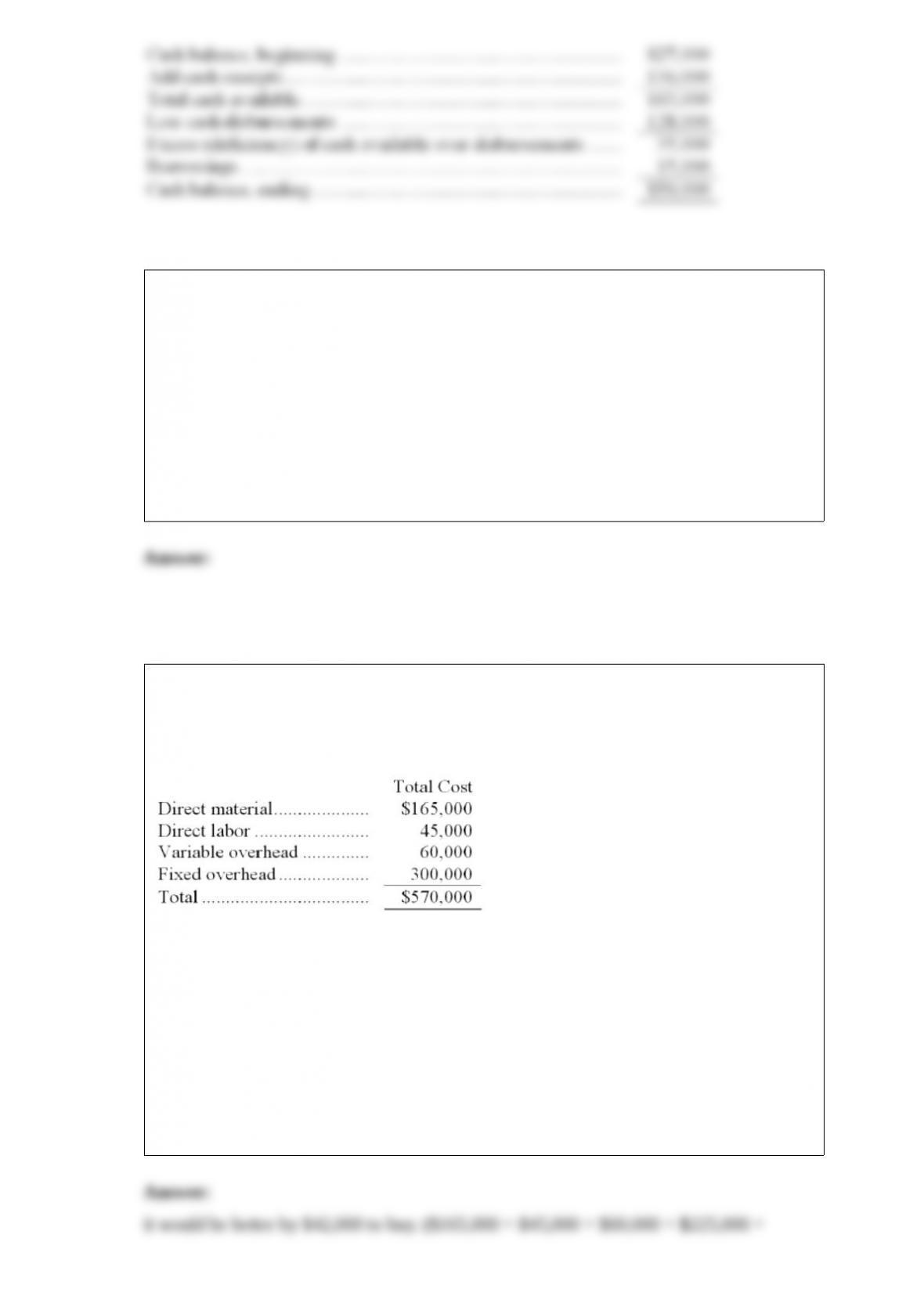

22) janeiro skate, inc. currently manufactures the wheels that it uses for its in-line

skates. the annual costs to manufacture the 150,000 wheels needed each year are as

follows:

kasba rubber company has offered to provide janeiro with all of its annual wheel needs

for $3.50 per wheel. if janeiro accepts this offer, 75% of the fixed overhead above could

be totally eliminated. also, janeiro would be able to rent out the freed up space and

could generate $72,000 of income annually.

required:

based on this information, would janeiro be better off to continue making the wheels or

to buy them from kasba? show your computations.

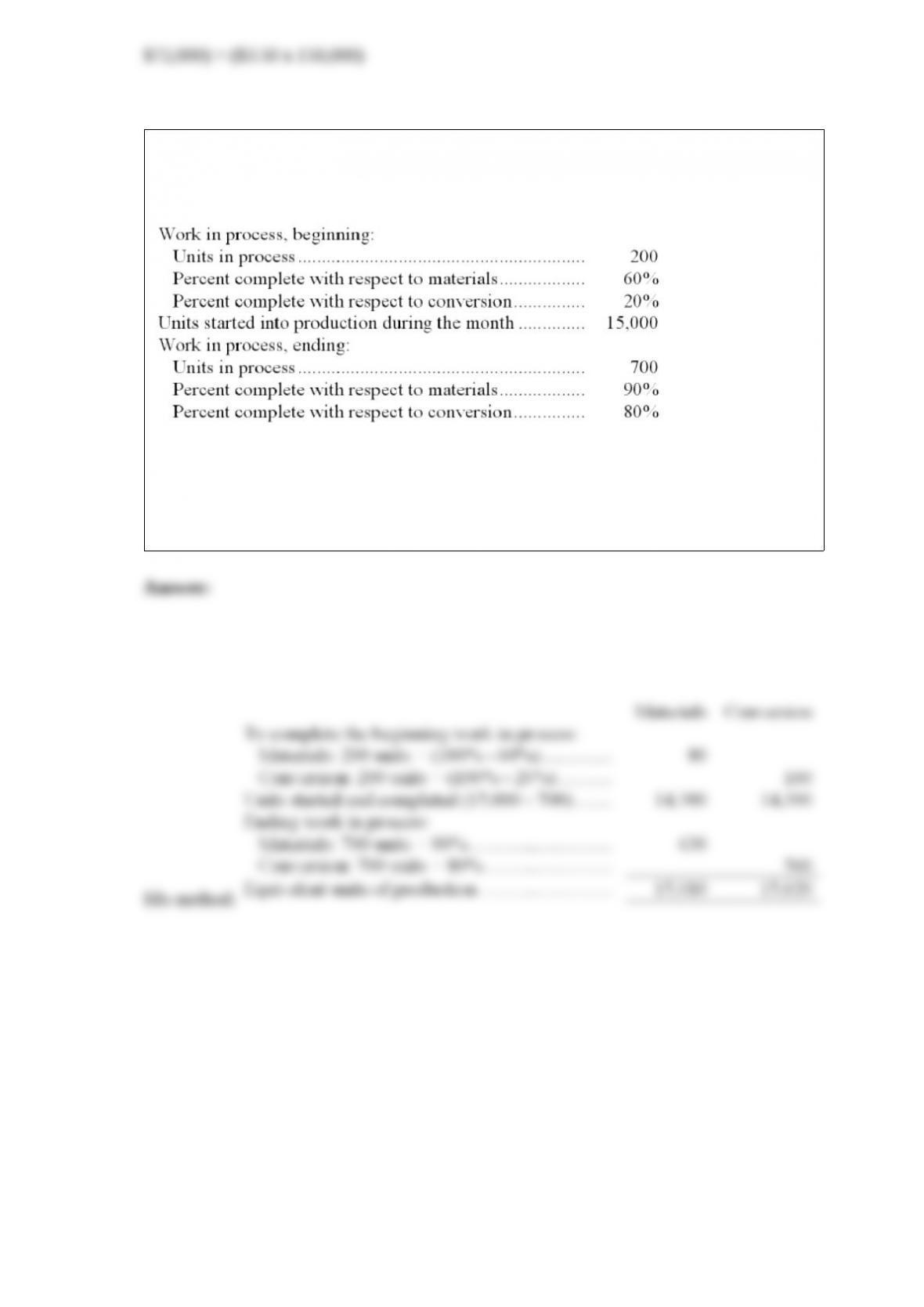

23) fryer inc. uses the fifo method in its process costing system. the following data

concern the operations of the company’s first processing department for a recent month.

required:

using the fifo method, determine the equivalent units of production for materials and

conversion costs.