Which of the following is not true about deferred revenue?

a. Deferred revenue with respect to gift cards is recognized as revenue when the gift

cards expire.

b. Deferred revenue is a liability.

c. Deferred revenue is recognized on credit sales when collectibility can be estimated.

d. Customer prepayments typically require recognition of deferred revenue.

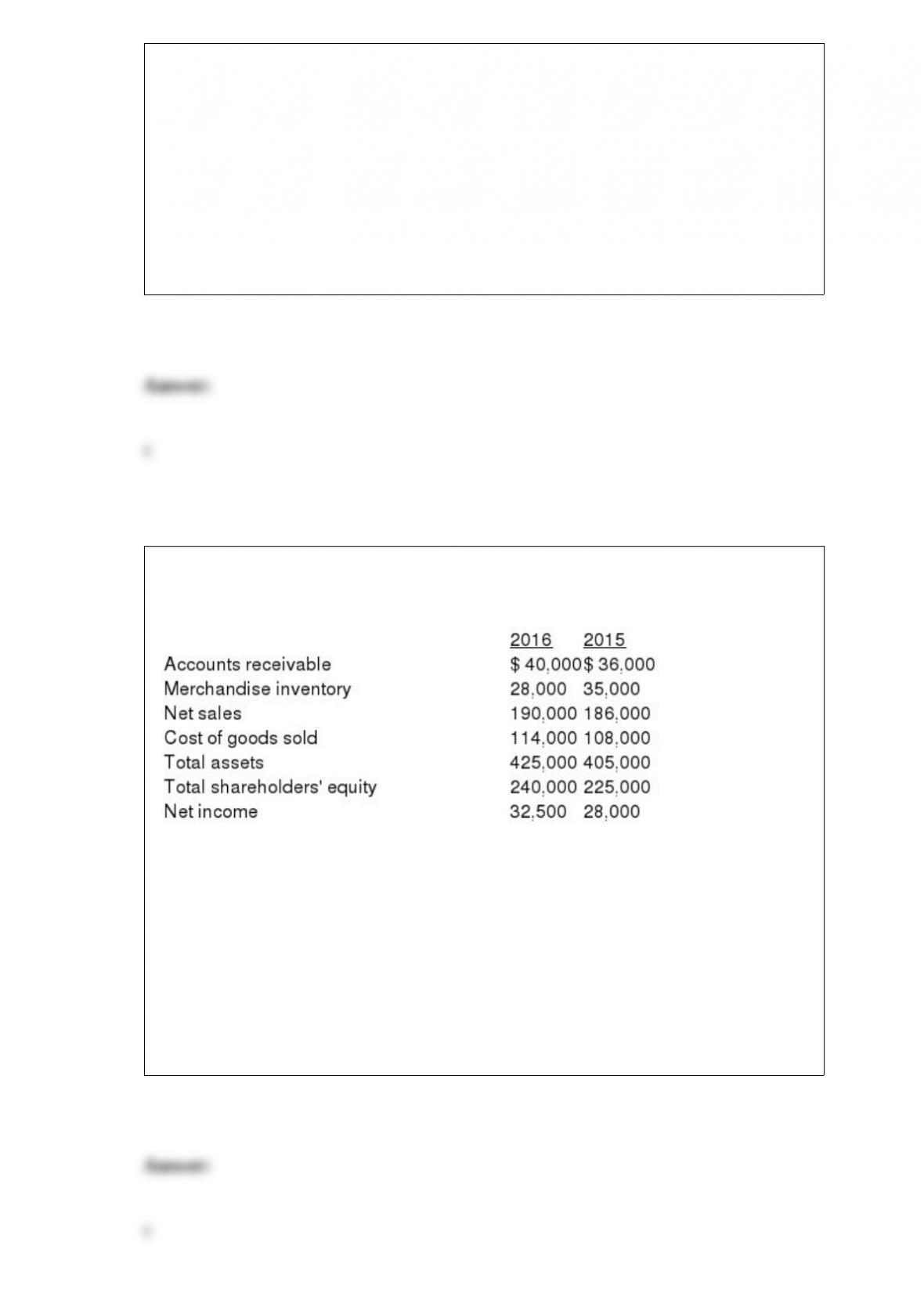

Excerpts from Hulkster Company’s December 31, 2016 and 2015, financial statements

are presented below:

Under IFRS, revenue for a product sale should occur when:

a) Inventory production is complete.

b) Warranty fulfillment is viewed as unlikely.

c) The seller has transferred to the buyer the risks and rewards of ownership and doesn’t

effectively manage or control the goods.

d) The buyer has paid a preponderance of installment amounts due.

What are the three types of expenses that a lessee experiences with a capital lease?

a. Lease expense, executory costs, interest expense.

b. Depreciation expense, lease expense, interest expense.

c. Executory costs, lease expense, depreciation expense.

d. Depreciation expense, interest expense, executory costs.

On February 1, 2015, Pat Weaver Inc. (PWI) issued 10%, $1,000,000 bonds for

$1,116,000. PWI retired all of these bonds on January 1, 2016, at 102. Unamortized

bond premium on that date was $92,800. How much gain or loss should be recognized

on this bond retirement?

a. $0 gain.

b. $111,800 gain.

c. $72,800 gain.

d. $96,000 gain.

Hope Company bought 30% of Faith Corporation in the beginning of 2016. Hope’s

purchase price equaled 30% of the book value of Faith’s net identifiable assets, which

also equaled 30% of the fair value of Faith. During 2016, Faith reported net income in

the amount of $4,000,000 and declared and paid dividends in the amount of $500,000.

Hope mistakenly accounted for the investment as available for sale instead of using the

equity method. What effect would this error have on the investment account and net

income, respectively, for 2016?

a. Overstated by $1,050,000; understated by $1,050,000.

b. Understated by $1,050,000; understated by $1,050,000.

c. Overstated by $1,200,000; overstated by $1,200,000.

d. Understated by $1,200,000; overstated by $1,050,000.

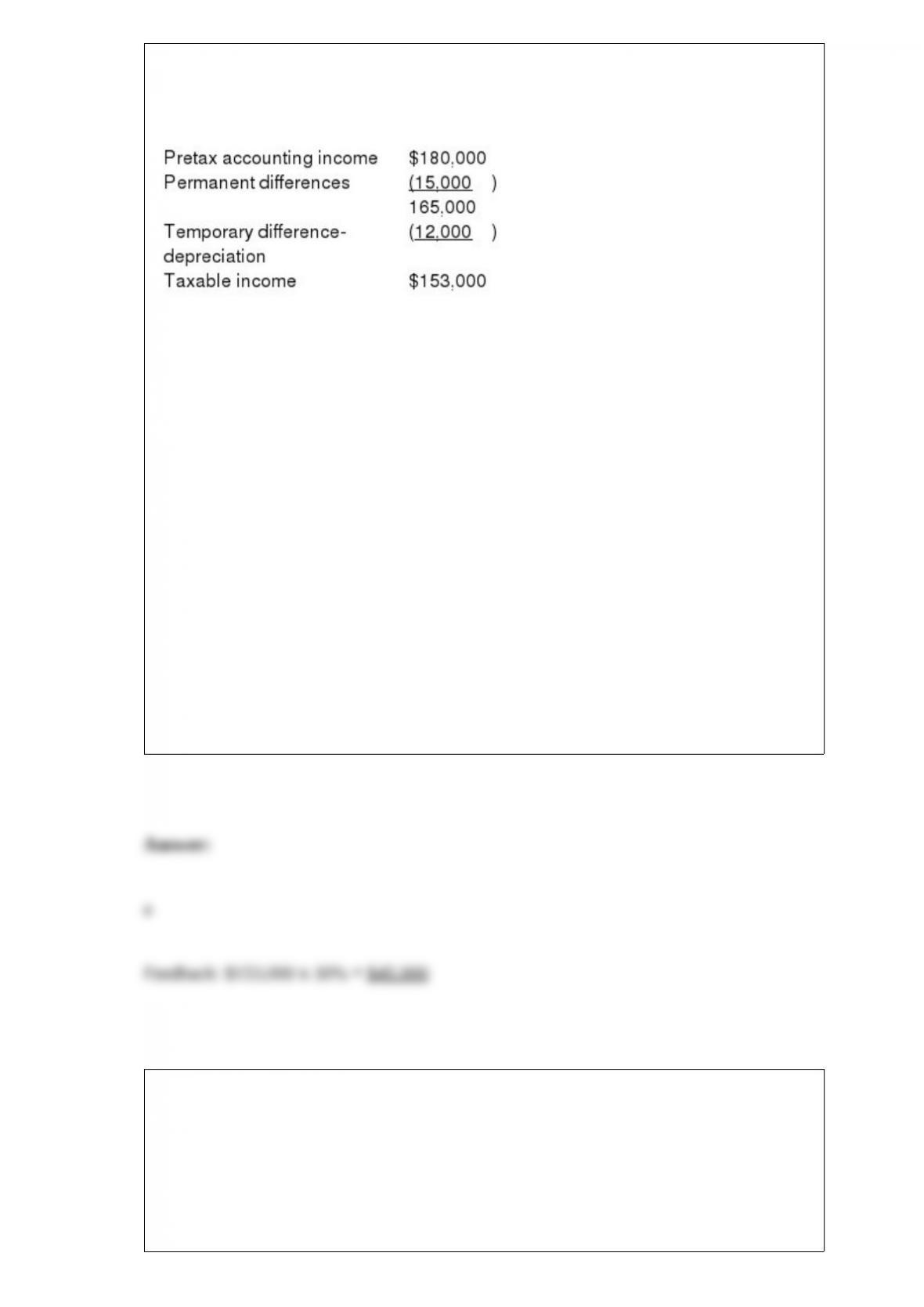

Information for Kent Corp. for the year 2016:

Reconciliation of pretax accounting income and taxable income:

Cumulative future taxable amounts all from depreciation temporary differences:

As of December 31, 2015 $13,000

As of December 31, 2016 $25,000

The enacted tax rate was 30% for 2015 and thereafter.

What should Kent report as the current portion of its income tax expense in the year

2016?

a. $45,900.

b. $49,500.

c. $54,000.

d. None of these answer choices are correct.

The use of LIFO during a long inflationary period can result in:

a. A net increase in income tax expense.

b. An inflated balance sheet.

c. Significant cash flow advantages over FIFO.

d. A reduction in inventory turnover over FIFO.

The equity method of accounting for investments in voting common stock is

appropriate when:

a. The investor can significantly influence the investee.

b. The investor has voting control over the investee.

c. The investor intends to hold the common stock indefinitely.

d. The investor is assured of a continued supply of a valuable raw material.

Which of the following is not true about accounting for an equity investment under

IFRS No. 9?

a. The investor can elect to account for the investment as FVOCI.

b. Unrealized gains and losses on the investment will be recognized in income unless

the investor elects to account for the investment as FVOCI.

c. If the investor elects to account for the investment as FVOCI, gains and losses will be

recognized in net income when the investment is sold.

d. Unrealized gains and losses are recognized in net income if the investor accounts for

the investments as FVPL.

On January 1, 2016, Legion Company sold $200,000 of 10% ten-year bonds. Interest is

payable semiannually on June 30 and December 31. The bonds were sold for $177,000,

priced to yield 12%. Legion records interest at the effective rate. Legion should report

bond interest expense for the six months ended June 30, 2016, in the amount of:

a. $ 8,850.

b. $10,000.

c. $10,620.

d. $12,000.

If bond interest expense is $800,000, bond interest payable increased by $8,000 and

bond discount decreased by $2,000, cash paid for bond interest is:

a. $790,000.

b. $784,000.

c. $806,000.

d. $910,000.

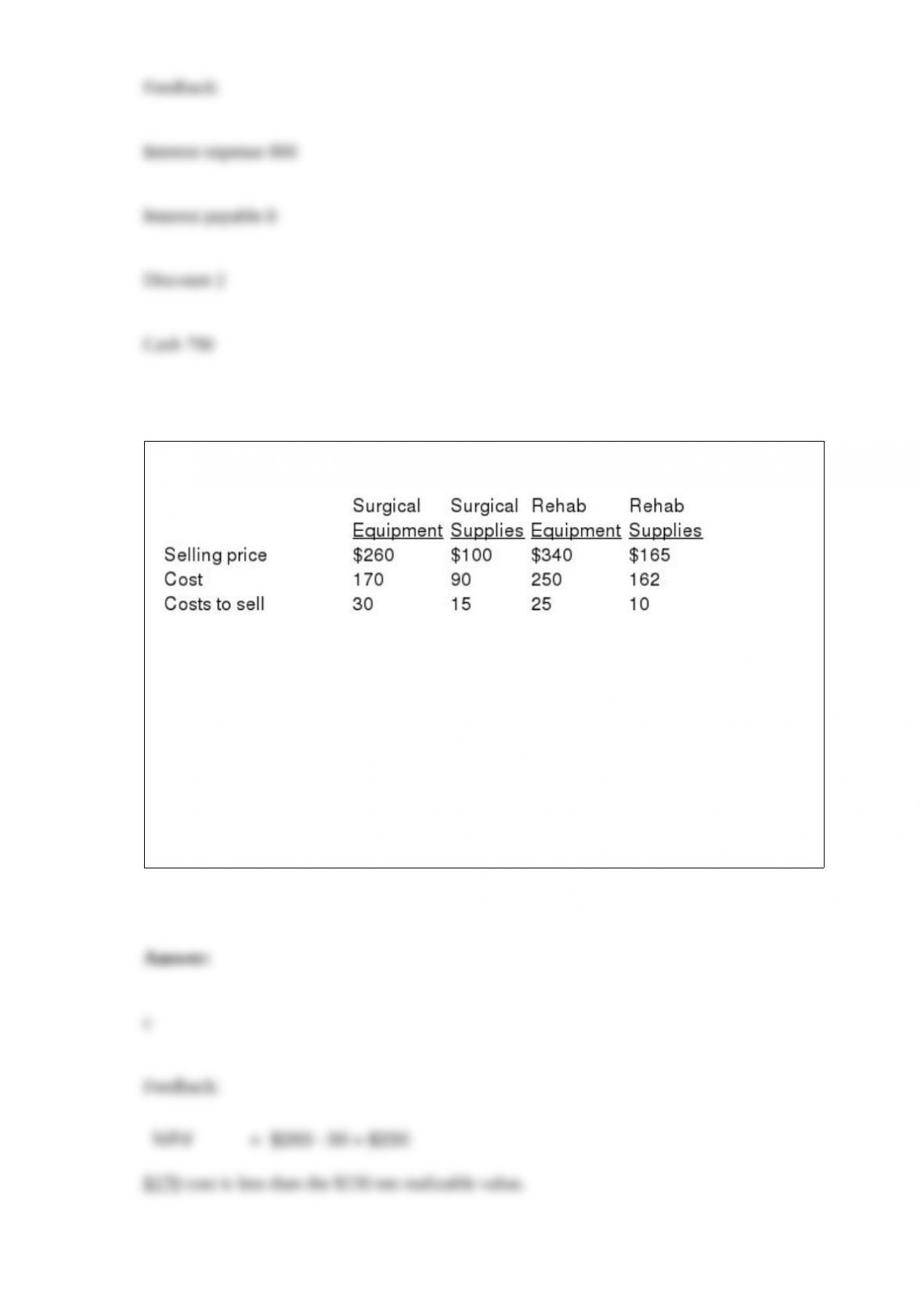

Data related to the inventories of Costco Medical Supply are presented below:

In applying the lower of cost and net realizable value rule, the inventory of surgical

equipment would be valued at:

a. $230.

b. $240.

c. $170.

d. $152.

When accounting for revenue over time for a long-term contract, the percentage of

completion used to recognize revenue in the first year usually is determined by

measuring:

a. Costs incurred in the first year, divided by estimated remaining costs to complete the

project.

b. Costs incurred in the first year, divided by estimated total costs for the completed

project.

c. Costs incurred in the first year, divided by estimated gross profit.

d. Costs incurred in the first year, divided by estimated total costs to be incurred in the

remaining years of the project.

SkiPark Company purchased a gondola for $440,000 (no residual value) at the

beginning of 2013. The gondola was being depreciated over a 10-year life using the

sum-of-the-years’-digits method. At the beginning of 2016, it was decided to change to

straight-line. An accompanying disclosure note would include each of the following

except:

a. The effect of a change on any financial statement line items affected for all periods

reported.

b. Justification that the change is preferable.

c. The cumulative effect of the change.

d. The effect of a change on per share amounts affected for all periods reported.

Which of the following differences between financial accounting and tax accounting

ordinarily creates a deferred tax asset?

a. Tax depreciation in excess of book depreciation.

b. Revenue collected in advance

c. The installment sales method for tax purposes.

d. None of these answer choices are correct.

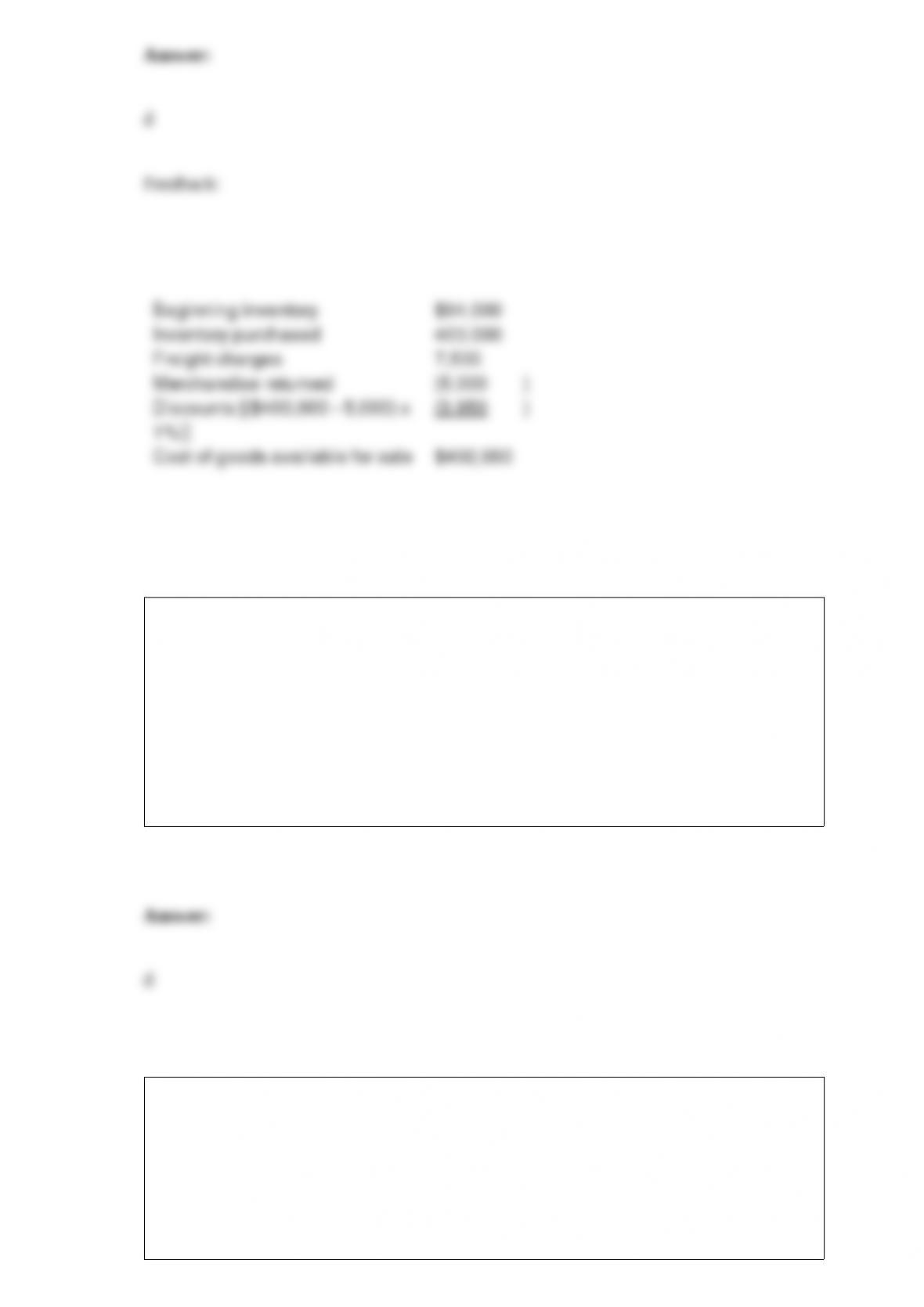

Northwest Fur Co. started 2016 with $94,000 of merchandise inventory on hand.

During 2016, $400,000 in merchandise was purchased on account with credit terms of

1/15, n/45. All discounts were taken. Purchases were all made f.o.b. shipping point.

Northwest paid freight charges of $7,500. Merchandise with an invoice amount of

$5,000 was returned for credit. Cost of goods sold for the year was $380,000.

Northwest uses a perpetual inventory system. Assuming Northwest uses the gross

method to record purchases, what is the cost of goods available for sale?

a. $492,500.

b. $496,500.

c. $490,500.

d. $492,550.

Which of the following statements typifies defined contribution plans?

a. Investment risk is borne by the corporation sponsoring the plan.

b. The plans are more complex than defined benefit plans.

c. Present value factors are used to determine the annual contributions to the plan.

d. The employer’s obligation is satisfied by making the periodic contribution to the plan.

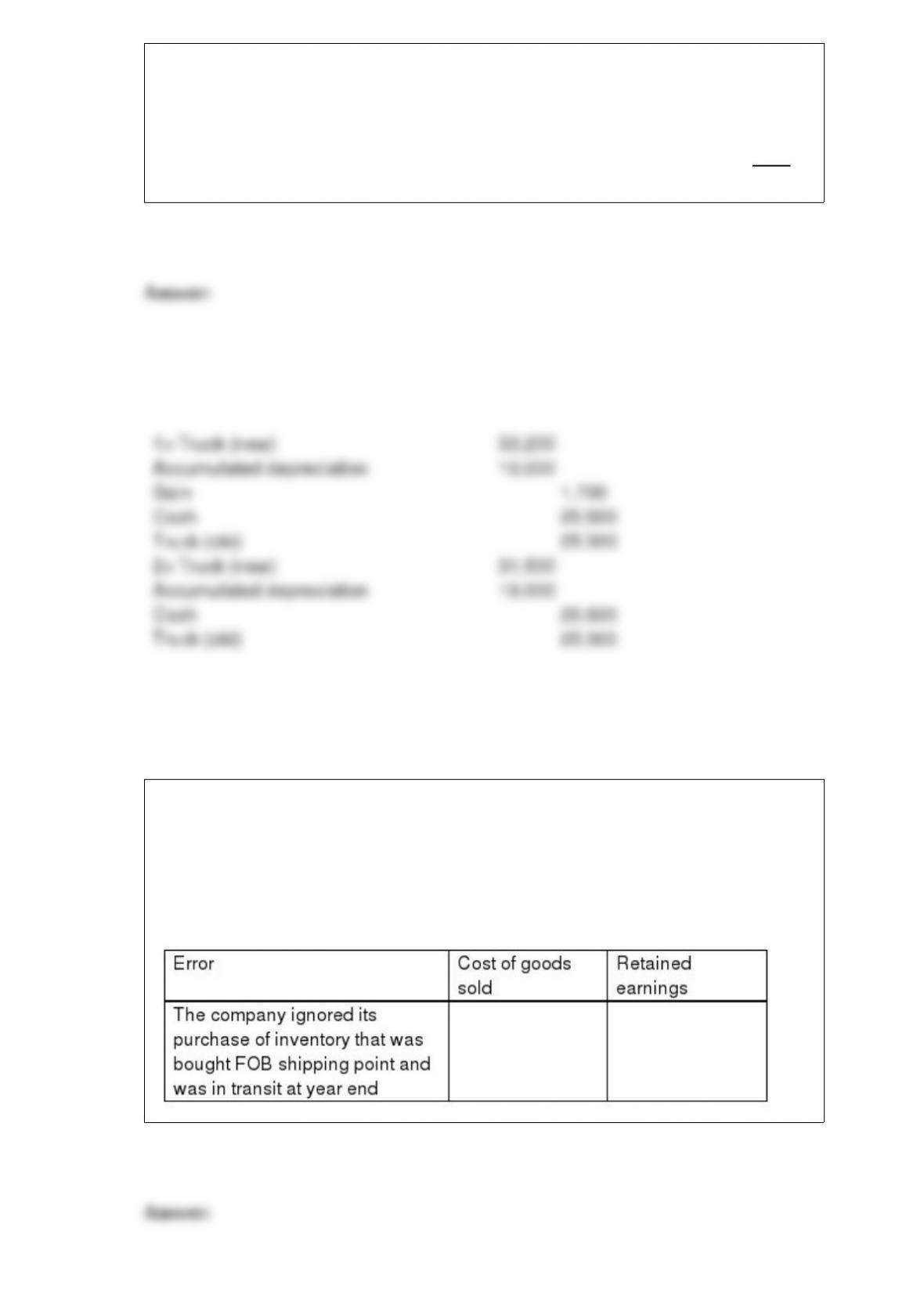

Wendell Corporation exchanged an old truck and $25,500 cash for a new truck. The old

truck had a book value of $6,000 (original cost of $25,000 less $19,000 in accumulated

depreciation) and a fair value of $7,700.

Required:

1> Prepare the journal entry to record the exchange. Assume the exchange has

commercial

substance.

2> Prepare the journal entry to record the exchange assuming that the exchange lacks

commercial substance.

In the following questions, inventory errors are noted for 2016. Assume that the errors

are not discovered until 2017, and that the company uses a periodic inventory system.

Indicate the effect of the error, if any, on the accounts noted in the columns, using the

following code:

U = Understated; O = Overstated; NE = No effect

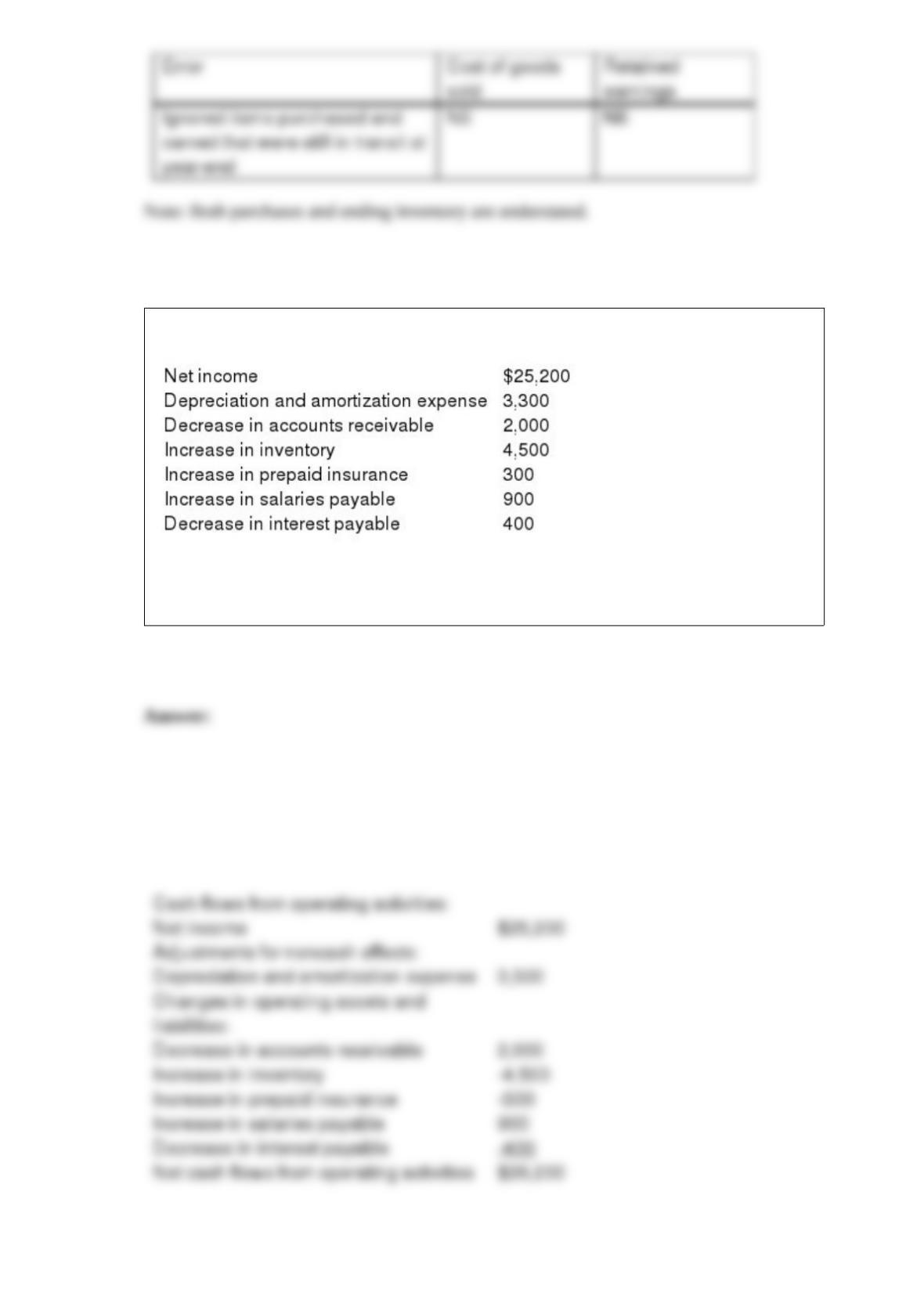

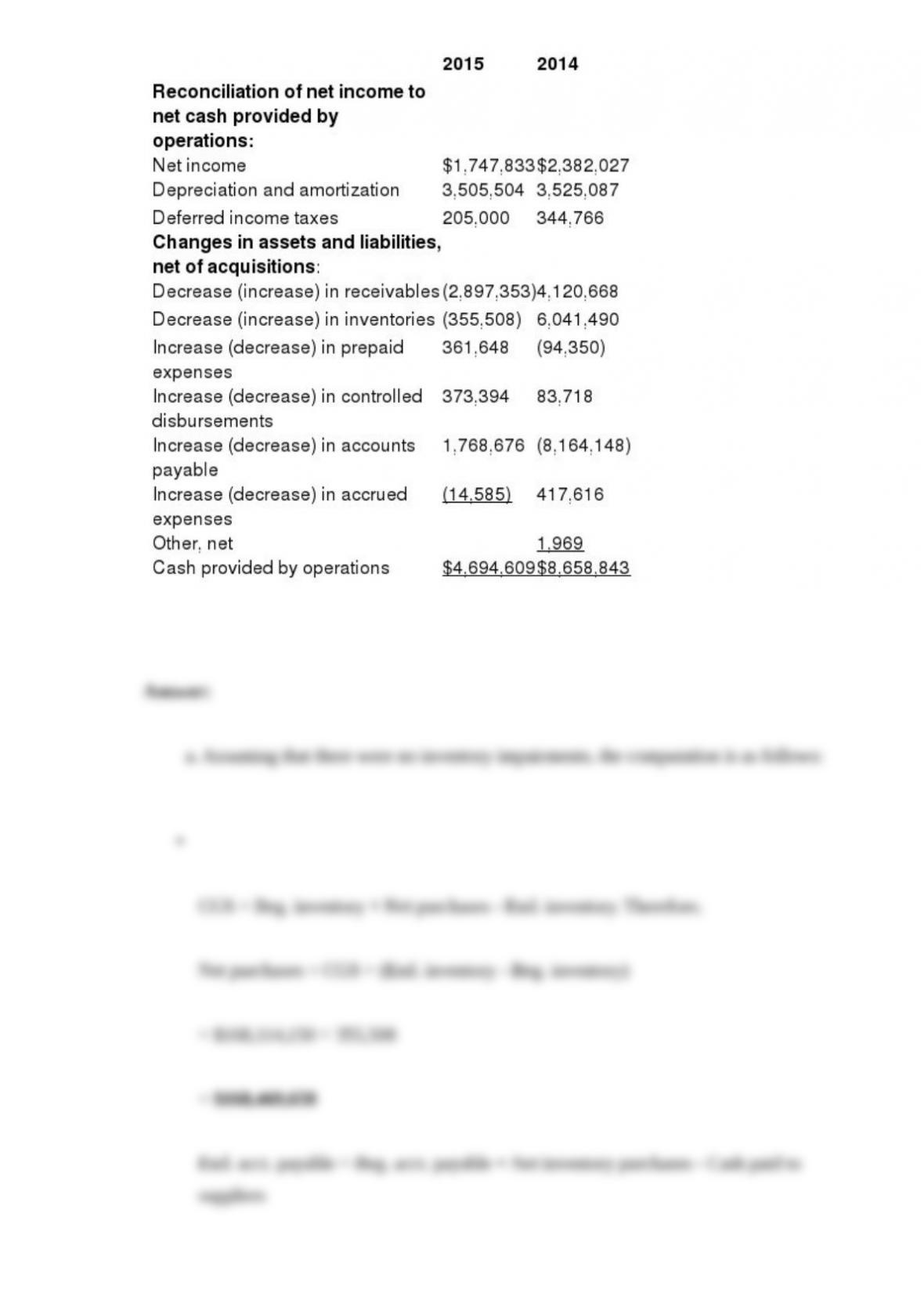

The accounting records of Rockness Company provided the data below ($ in 000s).

Required:

Prepare a reconciliation of net income to net cash flows from operating activities.

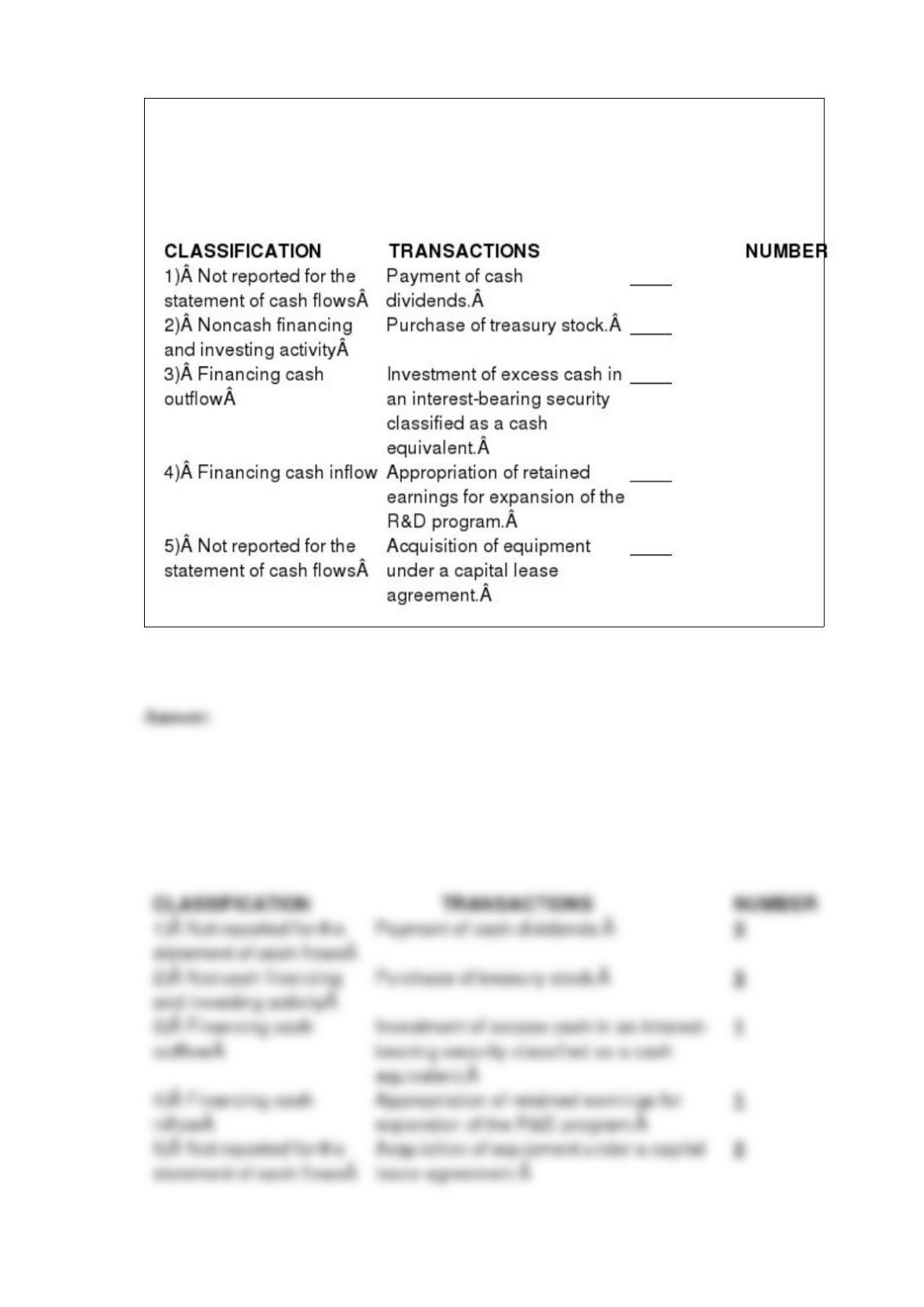

Listed below are the reporting classifications for a statement of cash flows using the

direct method for reporting operating cash flows. Indicate the reporting classification

that would apply to each of the five transactions described below by placing the number

of the reporting classification in the space provided by each transaction.

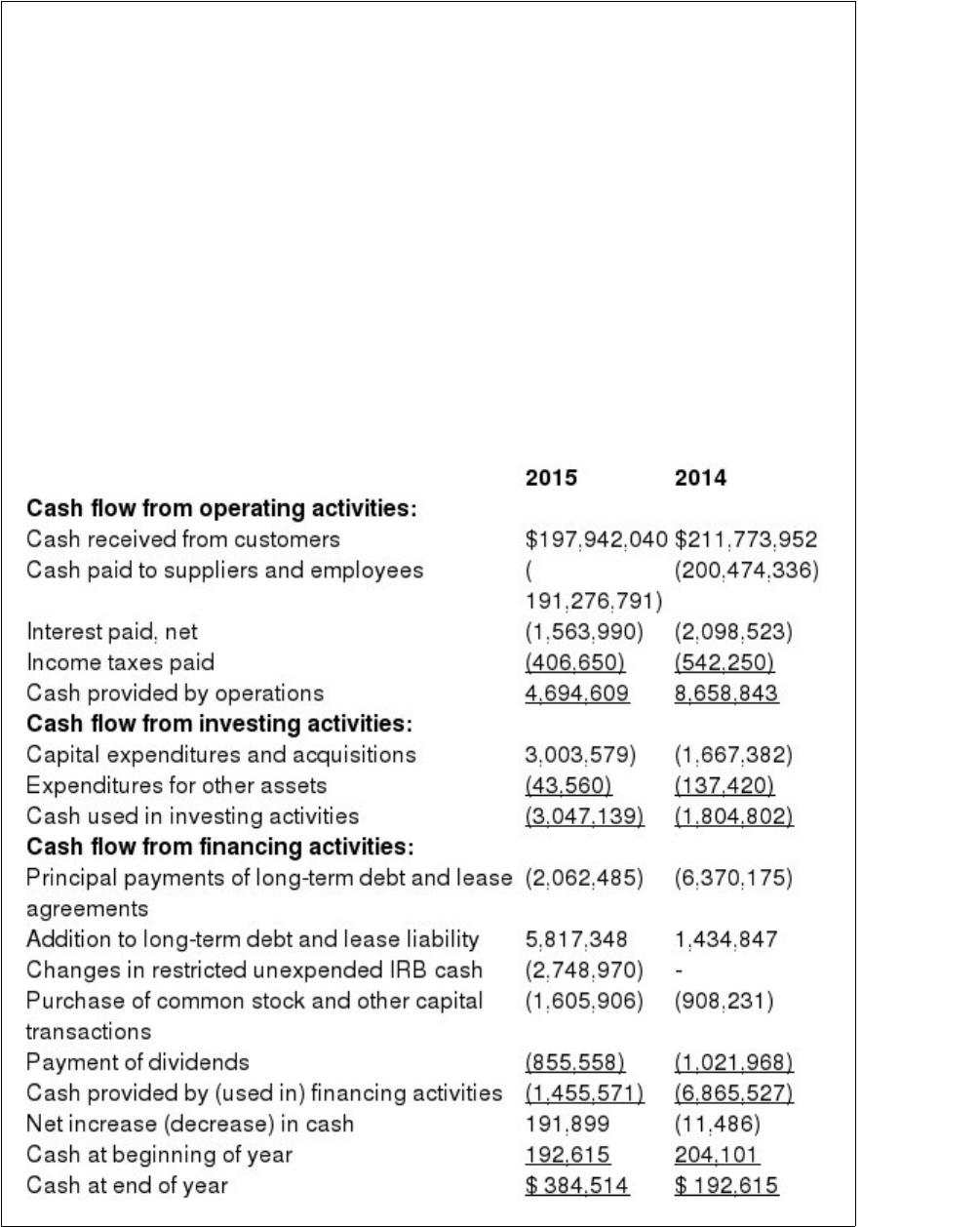

Kinney reported cost of goods sold of $168,114,150 in its fiscal 2015 income statement.

Assuming that Kinney uses accounts payable strictly for inventory purchases and that

all such purchases are on credit, how much cash did Kinney pay during the year for

inventories:

a. To inventory suppliers?

b. To employees?

c. In its 2015 Annual Report to Shareholders, Kinney Inc. reported the following

Consolidated Statement of Cash Flows:

d. For the years ended December 31,

•

Listed below are five terms followed by a list of phrases that describe or characterize

five of the terms. Match each phrase with the number for the correct term.