1) Ohme Framing’s cost formula for its supplies cost is $1,620 per month plus $13 per

frame. For the month of April, the company planned for activity of 882 frames, but the

actual level of activity was 878 frames. The actual supplies cost for the month was

$13,500. The supplies cost in the flexible budget for April would be closest to:

A.$13,086

B.$13,500

C.$13,034

D.$13,027

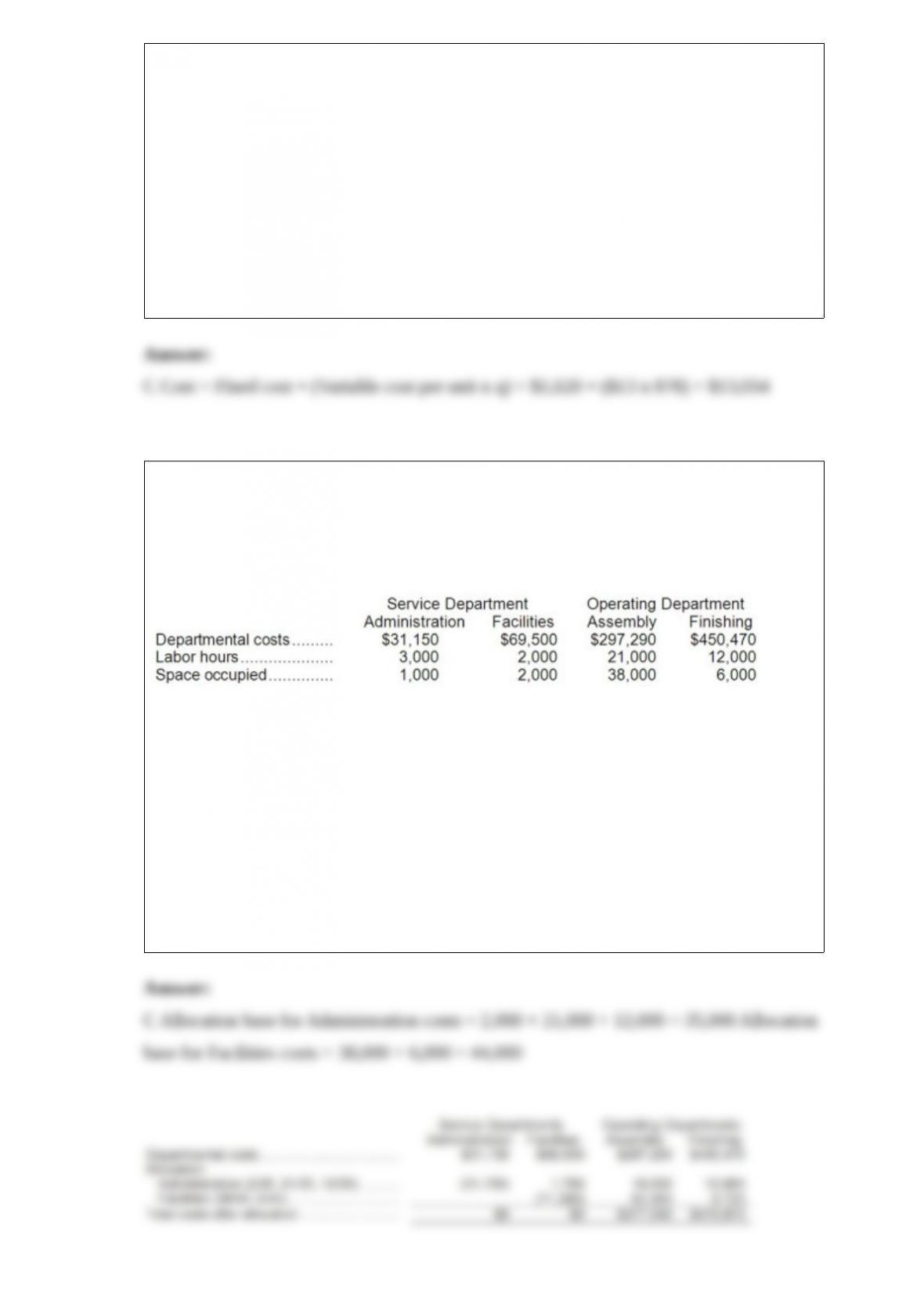

2) Silcott Corporation, a manufacturer, uses the step-down method to allocate service

department costs to operating departments. The company has two service departments,

Administration and Facilities, and two operating departments, Assembly and Finishing.

Data concerning those departments follow:

Administration Department costs are allocated first on the basis of labor hours and

Facilities Department costs are allocated second on the basis of space occupied.

The total Finishing Department cost after allocations is closest to:

A.$460,190

B.$471,275

C.$470,870

D.$468,994

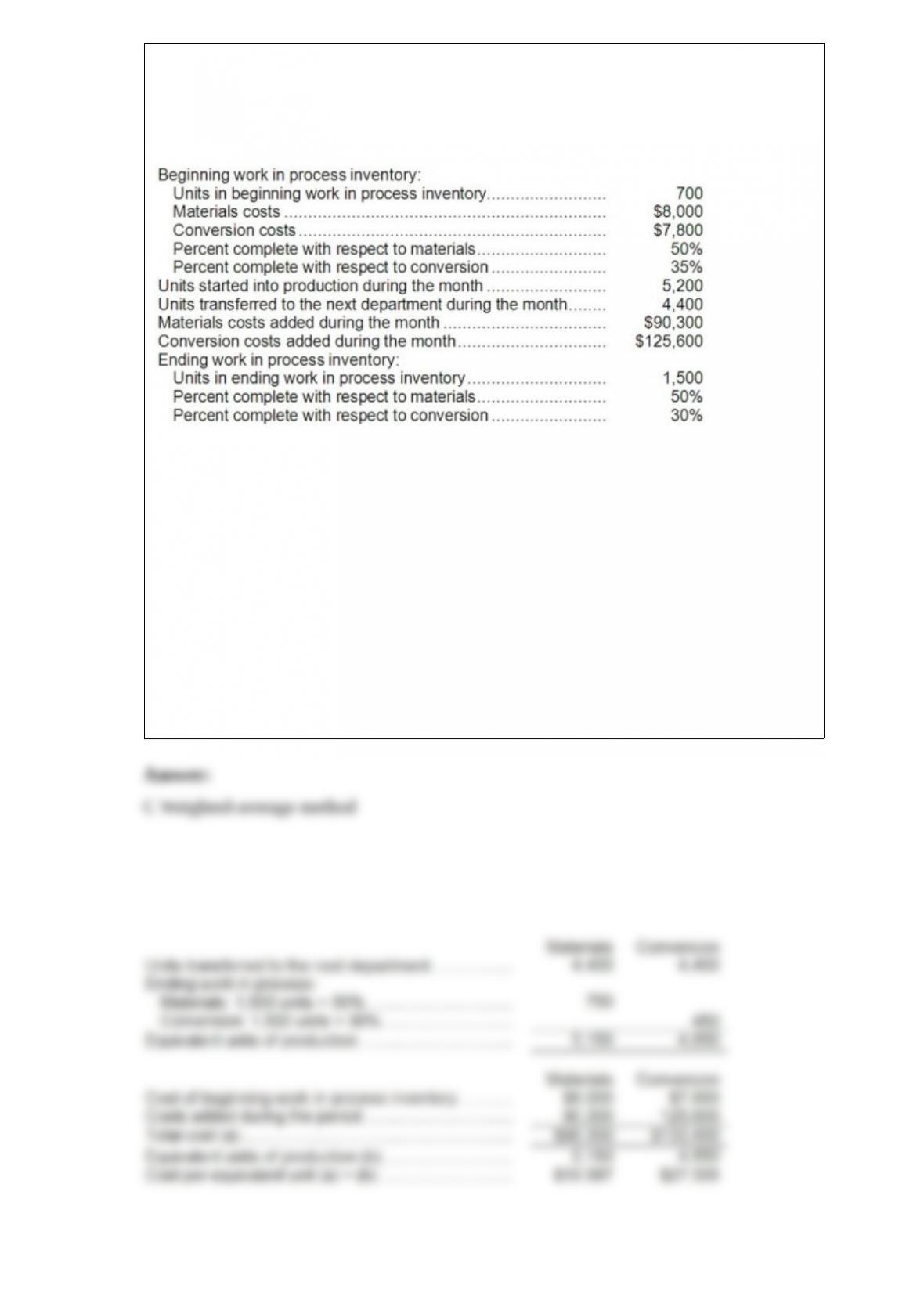

3) Hache Corporation uses the weighted-average method in its process costing system.

Data concerning the first processing department for the most recent month are listed

below:

Note: Your answers may differ from those offered below due to rounding error. In all

cases, select the answer that is the closest to the answer you computed. To reduce

rounding error, carry out all computations to at least three decimal places.

The total cost transferred from the first processing department to the next processing

department during the month is closest to:

A.$231,700

B.$274,893

C.$205,007

D.$215,900

4) Which of the following will have the largest dollar effect on the net present value of

a 10 year investment project?

A.a decrease of $20,000 in the initial investment required with no effect on the expected

salvage value in 10 years.

B.an increase of $20,000 in the expected salvage value in 10 years with no effect on the

initial investment.

C.a decrease of $20,000 in both the working capital needed to start the project and the

amount being released at the end of the 10 years.

D.an increase of $2,000 in the annual cash inflows from this project.

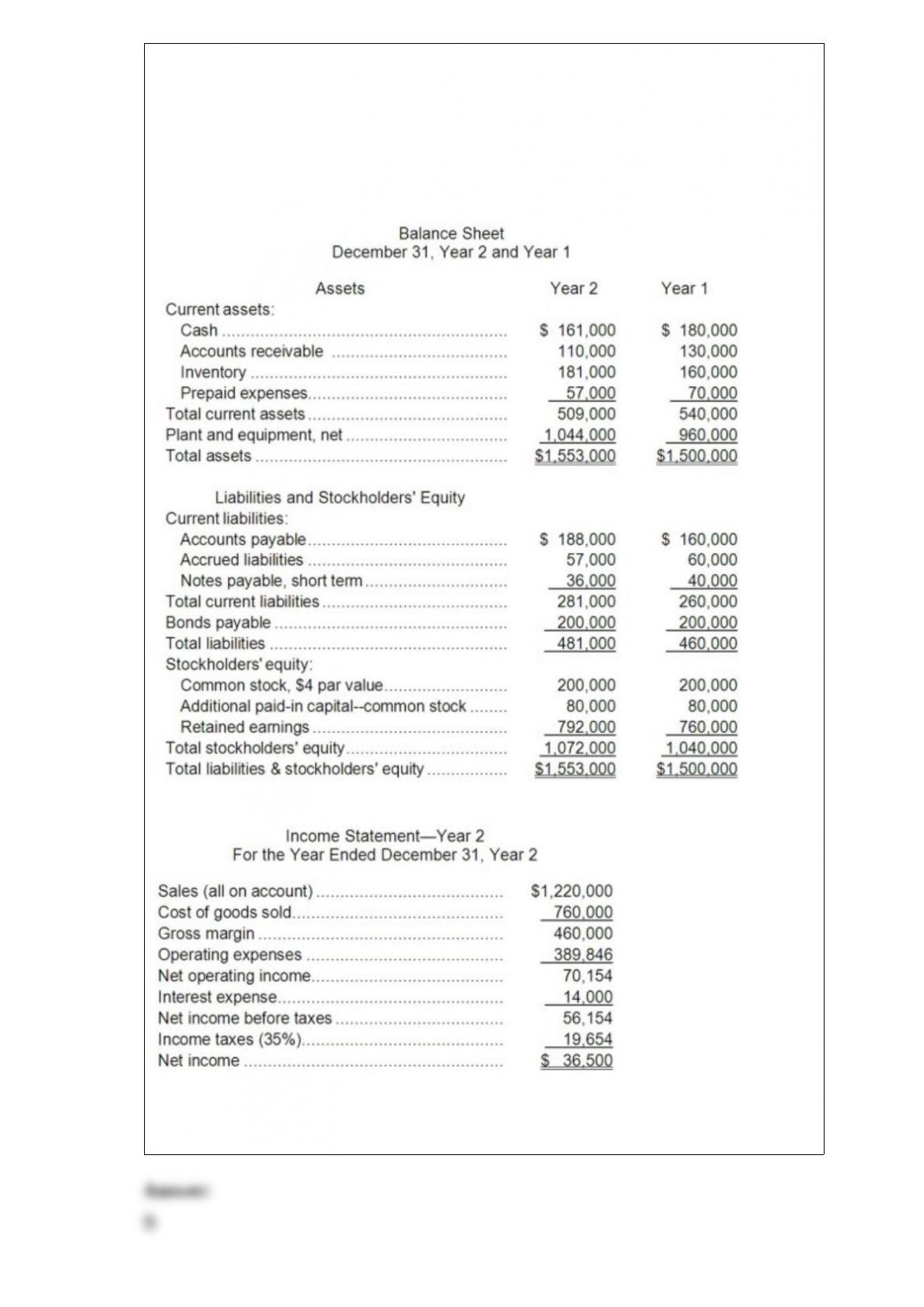

5) The average sale period for Year 2 is closest to:

A.28.1 days

B.45.0 days

C.50.0 days

D.227.7 days

6) The company’s equity multiplier at the end of Year 2 is closest to:

A.0.64

B.1.65

C.1.57

D.0.61

Equity multiplier = Average total assets* Average stockholders’ equity*

= $1,179,000 $716,000 = 1.65 (rounded)

*Average total assets = ($1,198,000 + $1,160,000) 2 = $1,179,000

**Average stockholders’ equity = ($732,000 + $700,000) 2 = $716,000

Fayer Corporation has provided the following financial data:

Dividends on common stock during Year 2 totaled $4,500. The market price of common

stock at the end of Year 2 was $10.88 per share.

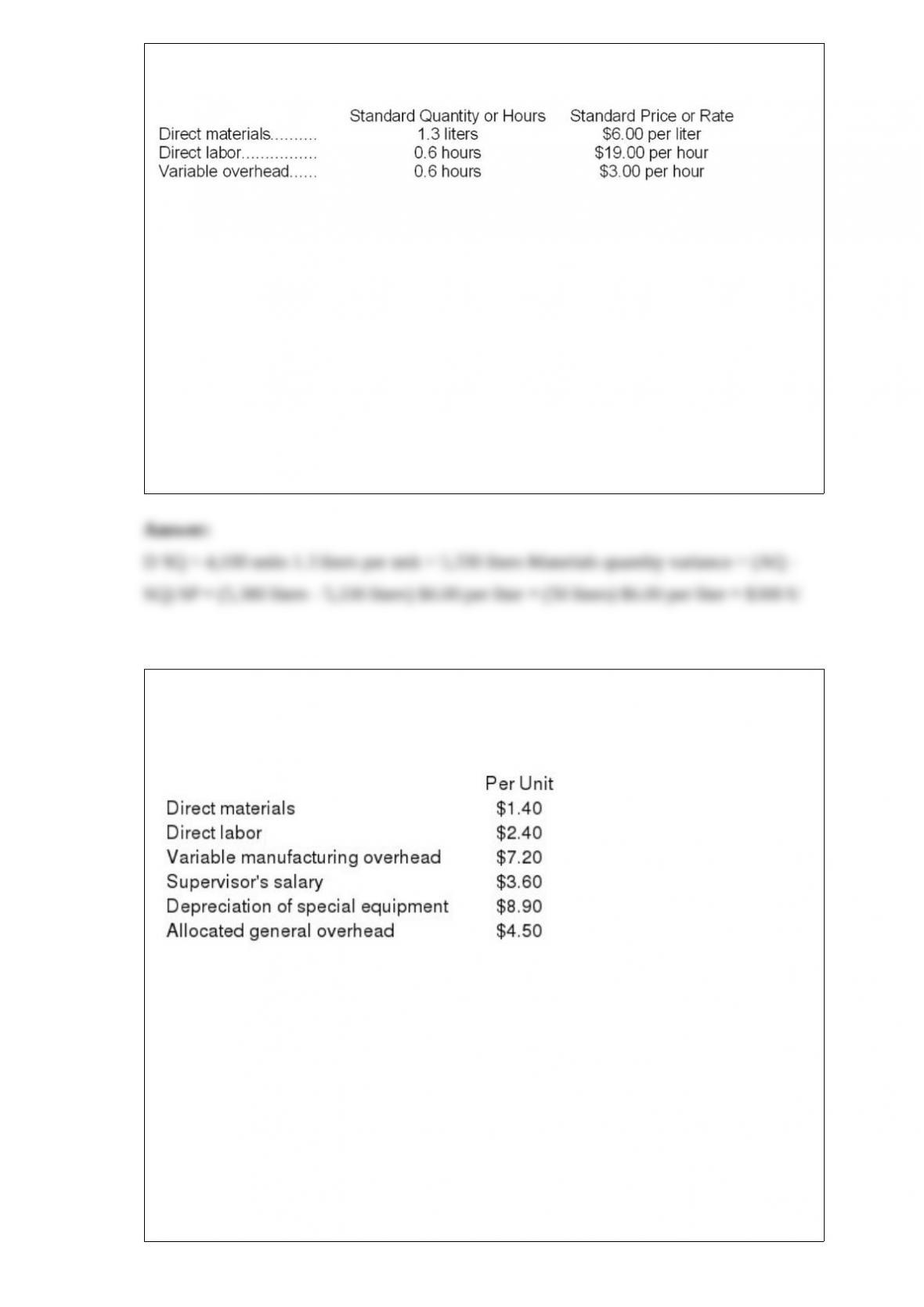

7) BieryCorporation makes a product with the following standard costs:

The company produced 4,100 units in April using 5,380 liters of direct material and

2,610 direct labor-hours. During the month, the company purchased 6,000 liters of the

direct material at $5.80 per liter. The actual direct labor rate was $19.80 per hour and

the actual variable overhead rate was $2.90 per hour.

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The materials quantity variance for April is:

A.$290 F

B.$290 U

C.$300 F

D.$300 U

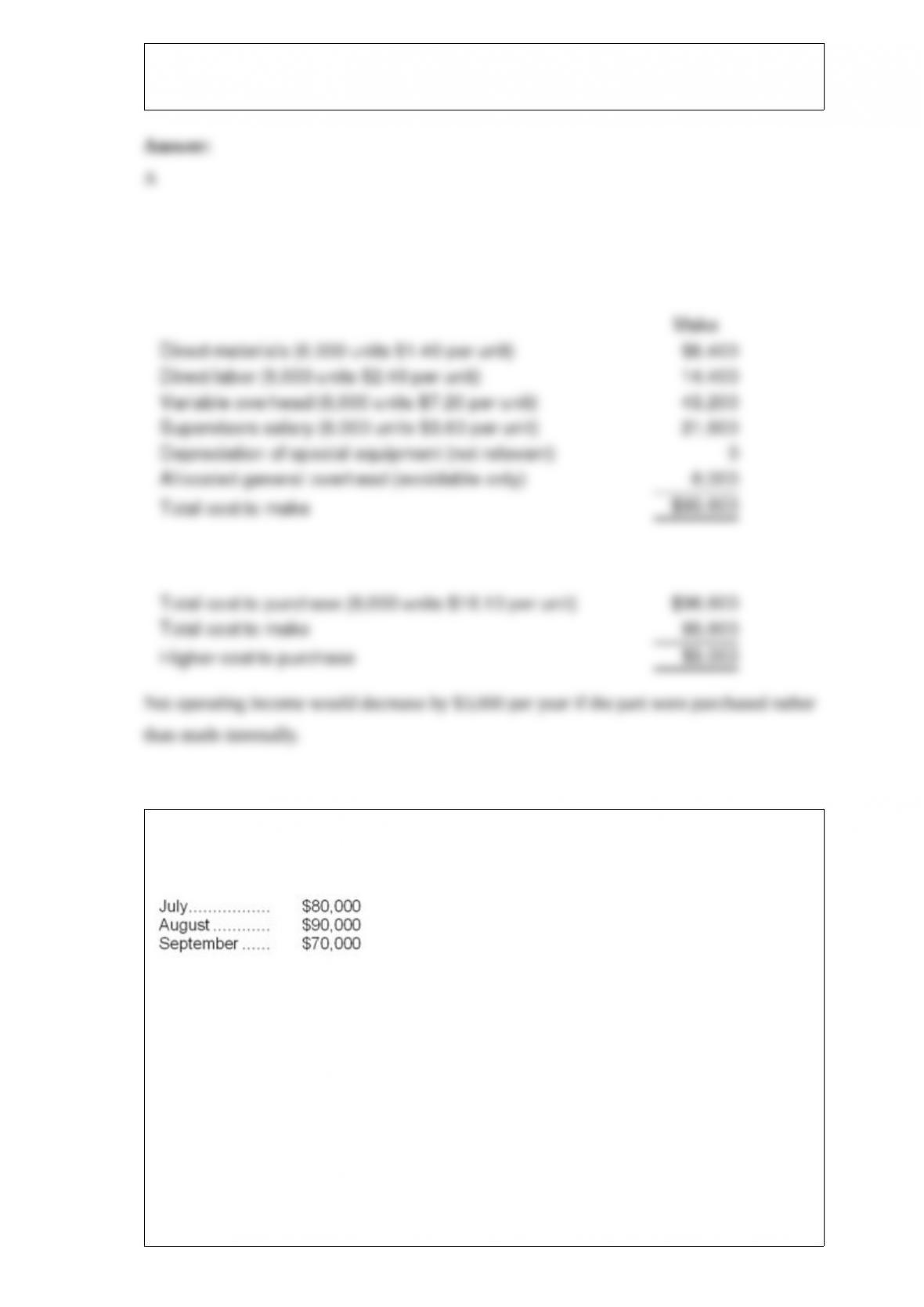

8) Part S00 is used in one of Morsey Corporation’s products. The company makes 6,000

units of this part each year. The company’s Accounting Department reports the

following costs of producing the part at this level of activity:

An outside supplier has offered to produce this part and sell it to the company for

$16.10 each. If this offer is accepted, the supervisor’s salary and all of the variable

costs, including direct labor, can be avoided. The special equipment used to make the

part was purchased many years ago and has no salvage value or other use. The allocated

general overhead represents fixed costs of the entire company. If the outside supplier’s

offer were accepted, only $6,000 of these allocated general overhead costs would be

avoided.

If management decides to buy part S00 from the outside supplier rather than to continue

making the part, what would be the annual impact on the company’s overall net

operating income?

A) Net operating income would decrease by $3,000 per year.

B) Net operating income would decrease by $71,400 per year.

C) Net operating income would decrease by $77,400 per year.

D) Net operating income would decrease by $65,400 per year.

9) May Corporation, a merchandising firm, has budgeted sales as follows for the third

quarter of the year:

Cost of goods sold is equal to 65% of sales. The company wants to maintain a monthly

ending inventory equal to 130% of the Cost of Goods Sold for the following month.

The inventory on June 30 is less than this ideal since it is only $65,000. The company is

now preparing a Merchandise Purchases Budget.

The desired beginning inventory for September is:

A.$117,000

B.$76,050

C.$91,000

D.$59,150

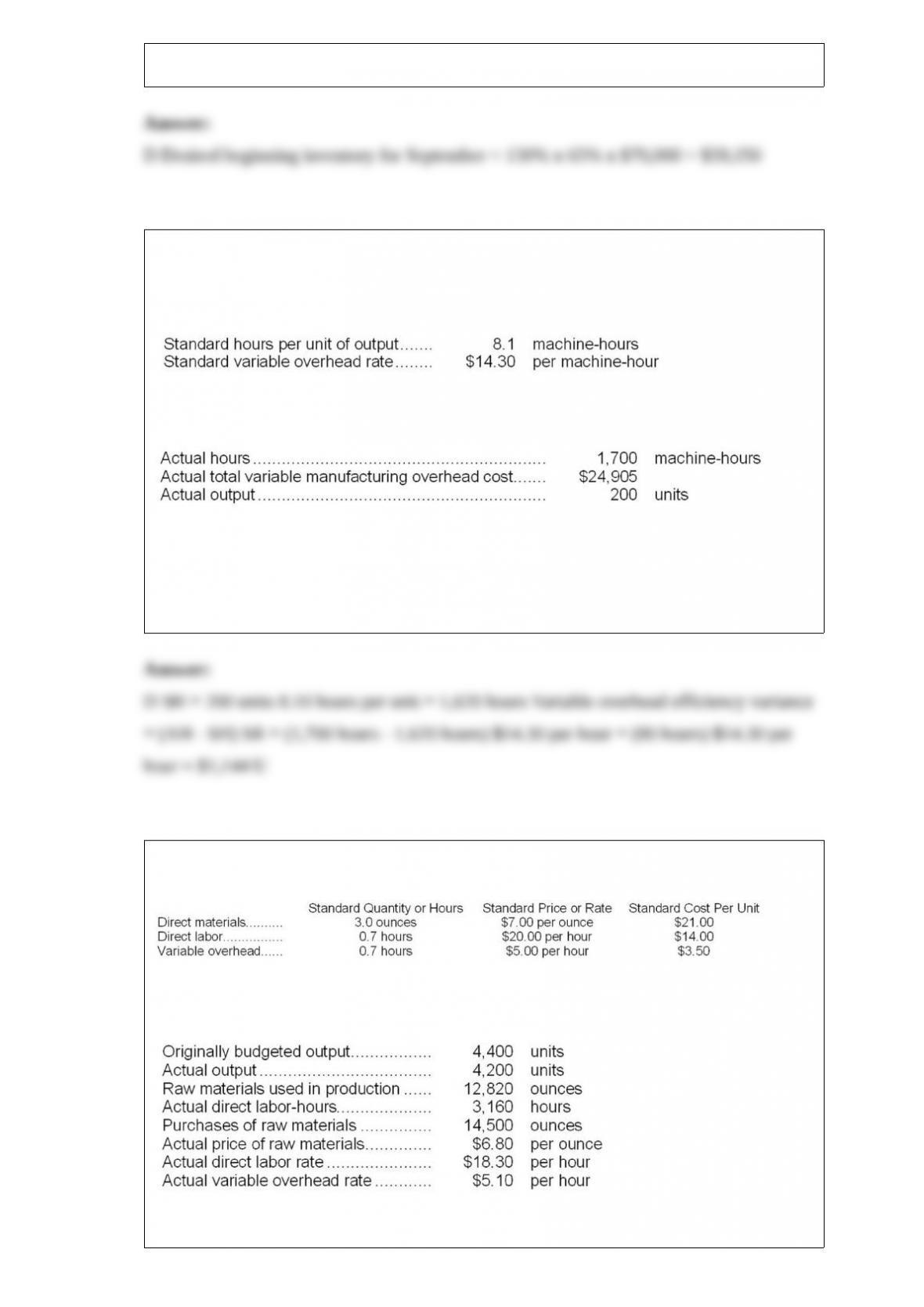

10) A manufacturing company that has only one product has established the following

standards for its variable manufacturing overhead. Variable manufacturing overhead

standards are based on machine-hours.

The following data pertain to operations for the last month:

What is the variable overhead efficiency variance for the month?

A.$1,172 F

B.$567 F

C.$1,172 U

D.$1,144 U

11) Oddo Corporation makes a product with the following standard costs:

The company reported the following results concerning this product in December.

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The materials quantity variance for December is:

A.$1,540 U

B.$1,496 F

C.$1,540 F

D.$1,496 U

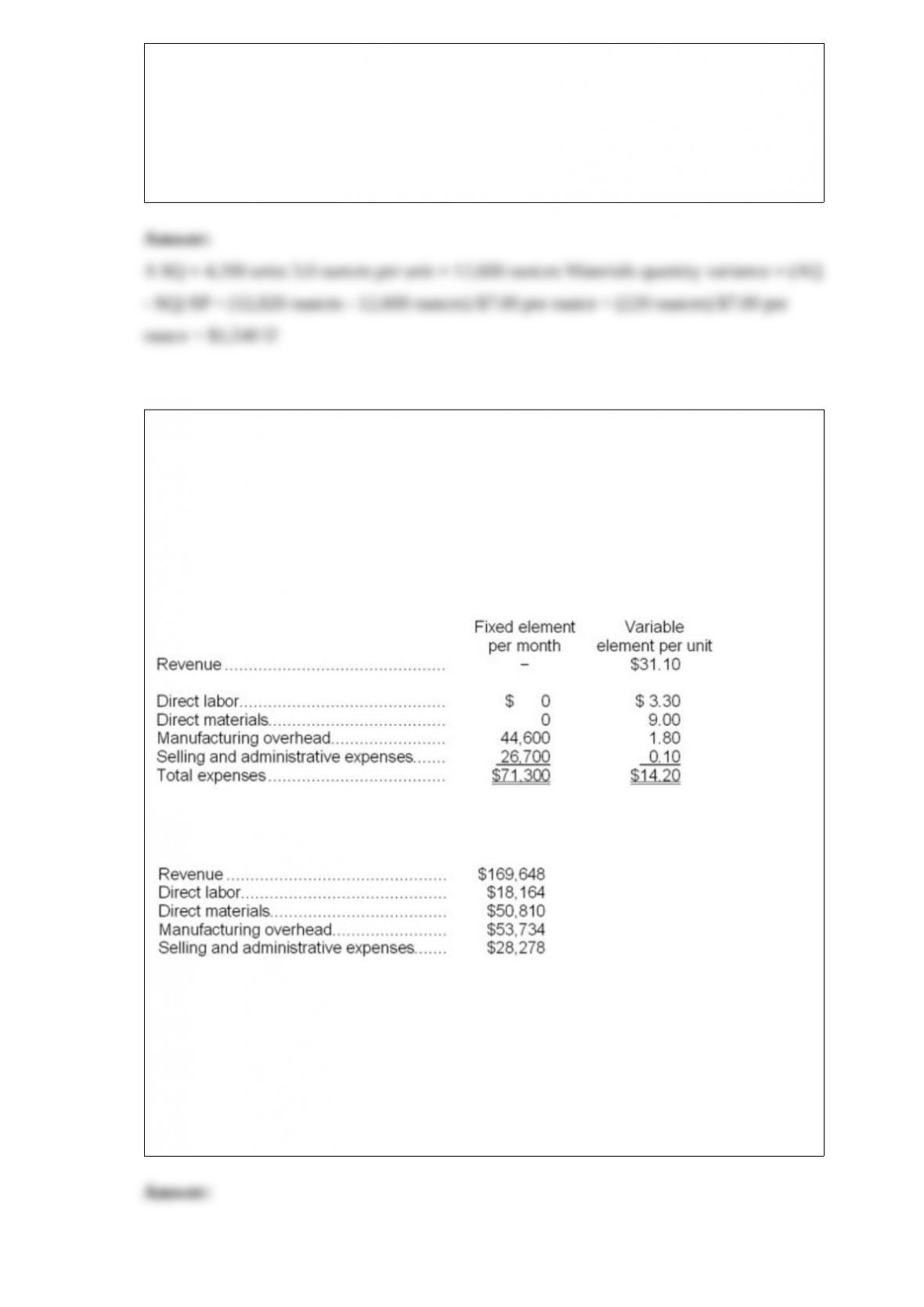

12) Prater Corporation manufactures and sells a single product. The company uses units

as the measure of activity in its budgets and performance reports. During February, the

company budgeted for 5,400 units, but its actual level of activity was 5,380 units. The

company has provided the following data concerning the formulas used in its budgeting

and its actual results for February:

Data used in budgeting:

Actual results for February:

The net operating income in the flexible budget for February would be closest to:

A.$19,960

B.$18,593

C.$18,731

D.$19,622