All investments in debt and equity securities that don’t fit the definitions of the other

reporting categories are classified as:

a. Trading securities.

b. Securities available for sale.

c. Held-to-maturity securities.

d. Consolidated securities.

When computing the cost-to-retail percentage for the average cost retail method,

included in the denominator are:

a. Net markups and net markdowns.

b. Neither net markups nor net markdowns.

c. Net markups, but not net markdowns.

d. Net markdowns, but not net markups.

Which of the following is not a characteristic of a liability?

a. It represents a probable, future sacrifice of economic benefits.

b. It must be payable in cash.

c. It arises from present obligations to other entities.

d. It results from past transactions or events.

When using the cost recovery method of accounting for long-term construction

contracts under IFRS:

a. Estimated losses on the overall contract are recognized before the contract is

completed.

b. Expenses are recorded each period, but revenue is only recognized when the contract

is completed.

c. Companies can use the percentage-of-completion method if that is their preference.

d. Neither gains nor losses are recognized until the contract is completed.

Which of the following is reported as a financing activity in the statement of cash

flows?

a. The sale of securities classified as available for sale.

b. The acquisition of stock for the purpose of retiring it.

c. The payment of interest on bonds payable.

d. The receipt of dividend revenue.

The primary reason for the popularity of LIFO is that it:

a. Provides better matching of physical flow and cost flow.

b. Saves income taxes currently.

c. Simplifies recordkeeping.

d. Provides a permanent reduction of income taxes.

Which of the following is reported as an investing activity in the statement of cash

flows?

a. The receipt of dividend revenue.

b. The payment of cash dividends.

c. The payment of interest on bonds.

d. The sale of machinery.

Pretax accounting income for the year ended December 31, 2016, was $50 million for

Truffles Company. Truffles’ taxable income was $60 million. This was a result of

differences between straight-line depreciation for financial reporting purposes and

MACRS for tax purposes. The enacted tax rate is 30% for 2016 and 40% thereafter.

What amount should Truffles report as the current portion of income tax expense for

2016?

a. $15 million.

b. $18 million.

c. $20 million.

d. $24 million.

When cash is received from customers in the form of a refundable deposit, the cash

account is increased with a corresponding increase in:

a. A current liability.

b. Revenue.

c. Shareholders’ equity.

d. Paid-in capital.

Surefeet Corporation changed its inventory valuation method. Which characteristic is

jeopardized by this change?

a. Comparability.

b. Representational faithfulness.

c. Consistency.

d. Feedback value.

Wilson Links Products sells a product that involves two separate performance

obligations: the SwingRight golf club weight and the SwingCoach teaching software.

SwingRight has a stand-alone selling price of $150. Wilson sells both the SwingRight

and the SwingCoach as a package deal for $200. The SwingCoach software is not sold

separately. Wilson is aware that other vendors charge $100 for similar software, and

Wilson’s prices are generally 10% lower than what is charged by those vendors. Wilson

estimates that it incurs approximately $65 of cost per copy of the software, and usually

charges 50% above cost on similar products.

Estimate the stand-alone selling price of the software using the expected cost plus

margin approach.

a. $50

b. $80

c. $90

d. $97.50

Red Manufacturing Company owns 40% of the outstanding common stock of Blue

Supply Company. During 2016, Red received a $50 million cash dividend from Blue.

What effect did this dividend have on Red’s 2016 statement of cash flows?

a. Cash from operating activities increased.

b. Cash from investing activities increased.

c. Cash from financing activities increased.

d. No effect.

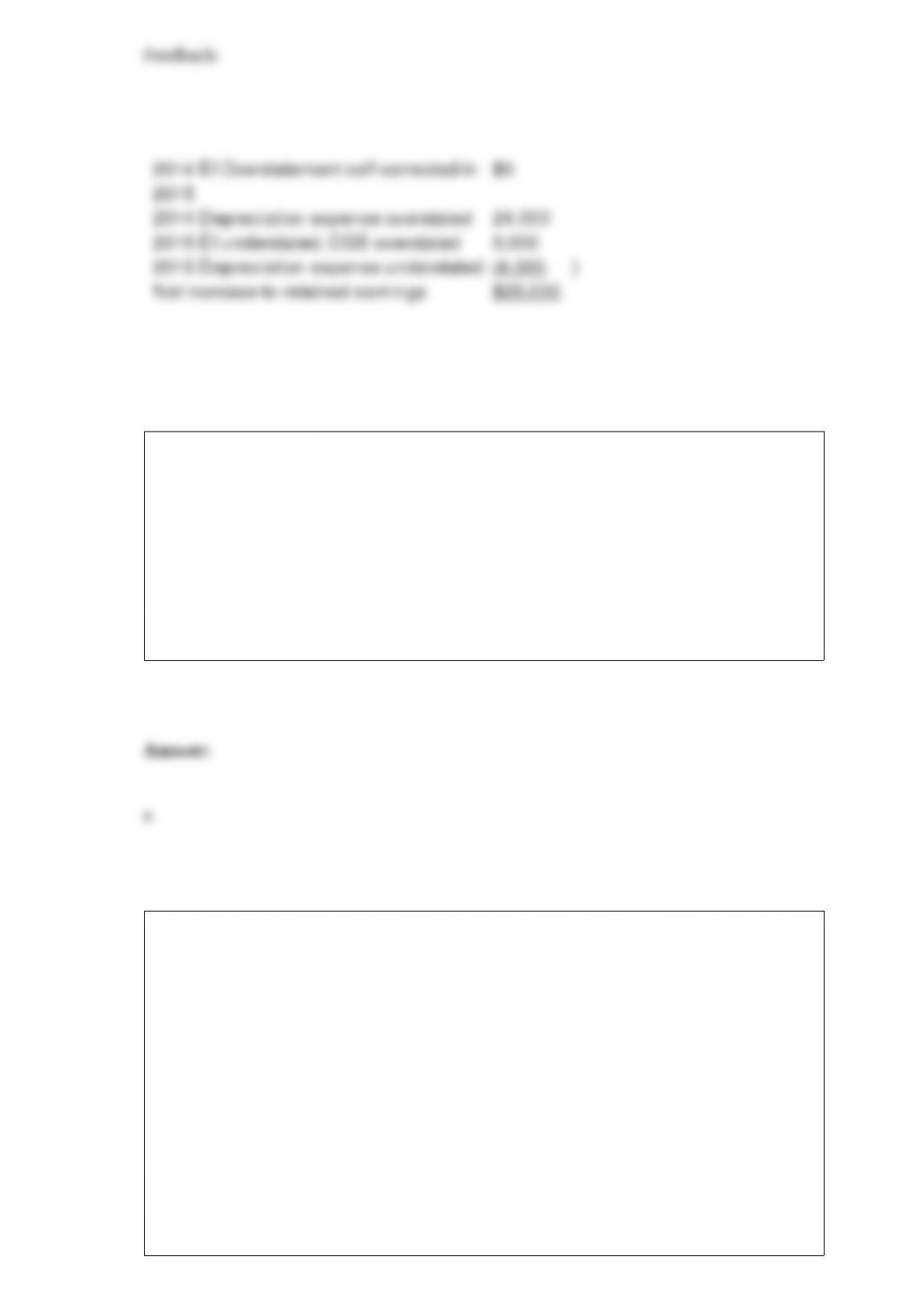

Powell Company had the following errors over the last two years:

2014: Ending inventory was overstated by $30,000 while depreciation expense was

overstated by $24,000.

2015: Ending inventory was understated by $5,000 while depreciation expense was

understated by $4,000.

By how much should retained earnings be adjusted on January 1, 2016? (Ignore taxes)

a. Increase by $15,000.

b. Decrease by $25,000.

c. Decrease by $6,000.

d. Increase by $25,000.

Under International Financial Reporting Standards, research expenditures are:

a. Expensed in the period incurred.

b. Expensed in the period they are determined to be unsuccessful.

c. Capitalized if certain criteria are met.

d. Expensed if unsuccessful, capitalized if successful.

Harlequin Co. has used the dollar-value LIFO retail method since it began operations in

early 2015 (its base year). Its beginning inventory for 2016 was $36,000 at cost and

$72,000 at retail prices. At the end of 2016, it computed its estimated ending inventory

at retail to be $120,000. Assuming its cost-to-retail percentage for 2016 transactions

was 60%, what is the inventory balance that Harlequin Co. would report in its 12/31/16

balance sheet?

a. $64,800.

b. $72,000.

c. $120,000.

d. The balance can’t be determined with the given information.

On January 1, 2016, Dreamworld Co. began construction of a new warehouse. The

building was finished and ready for use on September 30, 2017. Expenditures on the

project were as follows:

Dreamworld had $5,000,000 in 12% bonds outstanding through both years.

What was the final cost of Dreamworld’s warehouse?

a. $2,154,480.

b. $2,143,860.

c. $1,950,000.

d. $1,254,000.

The O’Hara Group is owed $1,000,000 by Hilton Enterprises under an 8% note with

three years remaining to maturity. The prior year of interest was unpaid. O’Hara agrees

to restructure the note under terms that yield a present value of $880,000. The journal

entry that O’Hara would make to record this transaction would include a loss on

troubled debt restructuring of:

a. $0.

b. $80,000.

c. $200,000.

d. $220,000.

What is the EITF and what is its purpose?

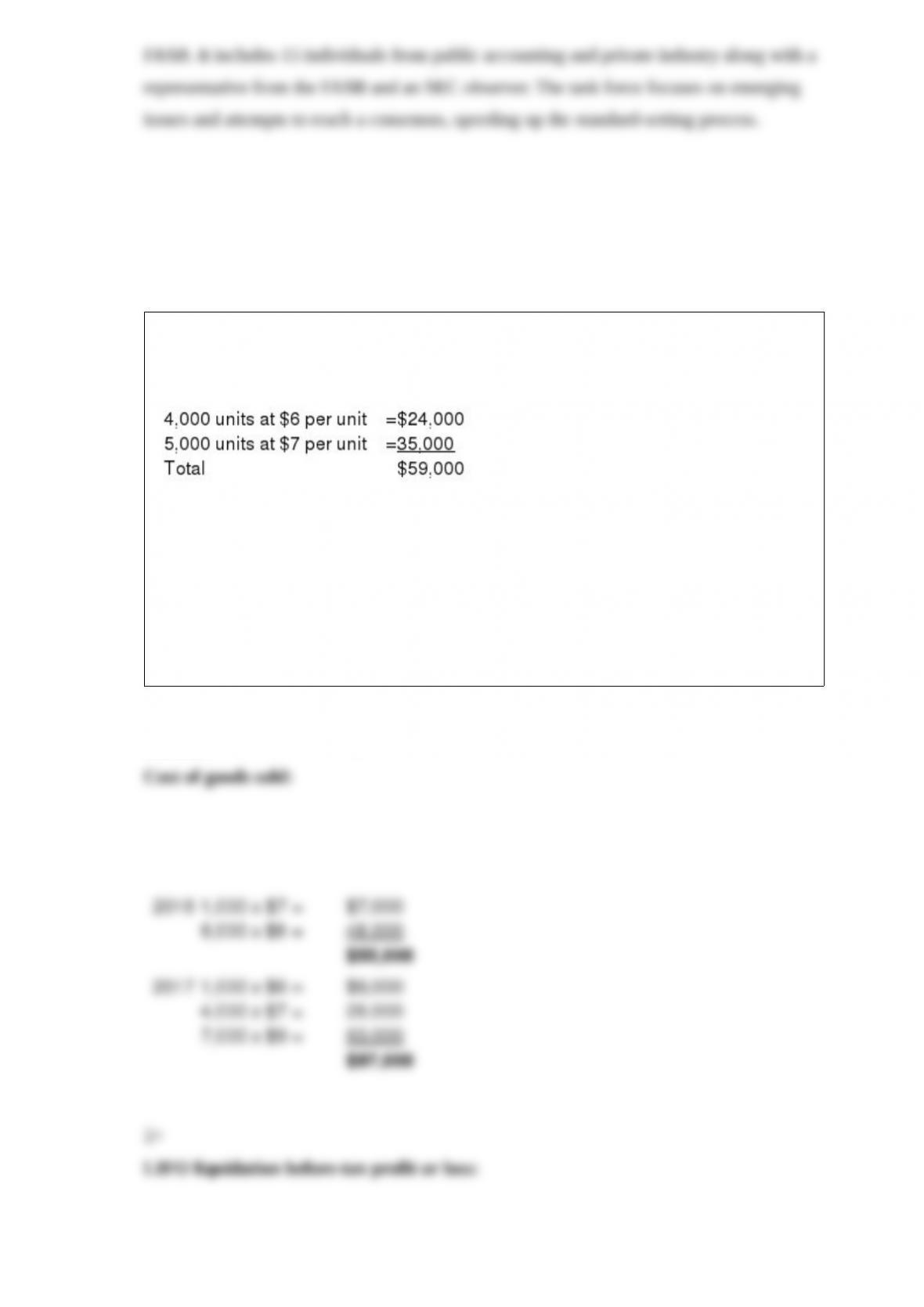

Hazelton Corporation uses a periodic inventory system and the LIFO method to value

its inventory. The company began 2016 with $59,000 in inventory of its only product.

The beginning inventory consisted of the following layers:

During 2016, 6,000 units were purchased at $8 per unit and during 2017, 7,000 units

were purchased at $9 per unit. Sales, in units, were 7,000 and 12,000 during 2016 and

2017, respectively. Required:

1> Calculate cost of goods sold for 2016 and 2017.

2> Disregarding income tax, determine the LIFO liquidation profit or loss, if any, for

2016 and 2017.

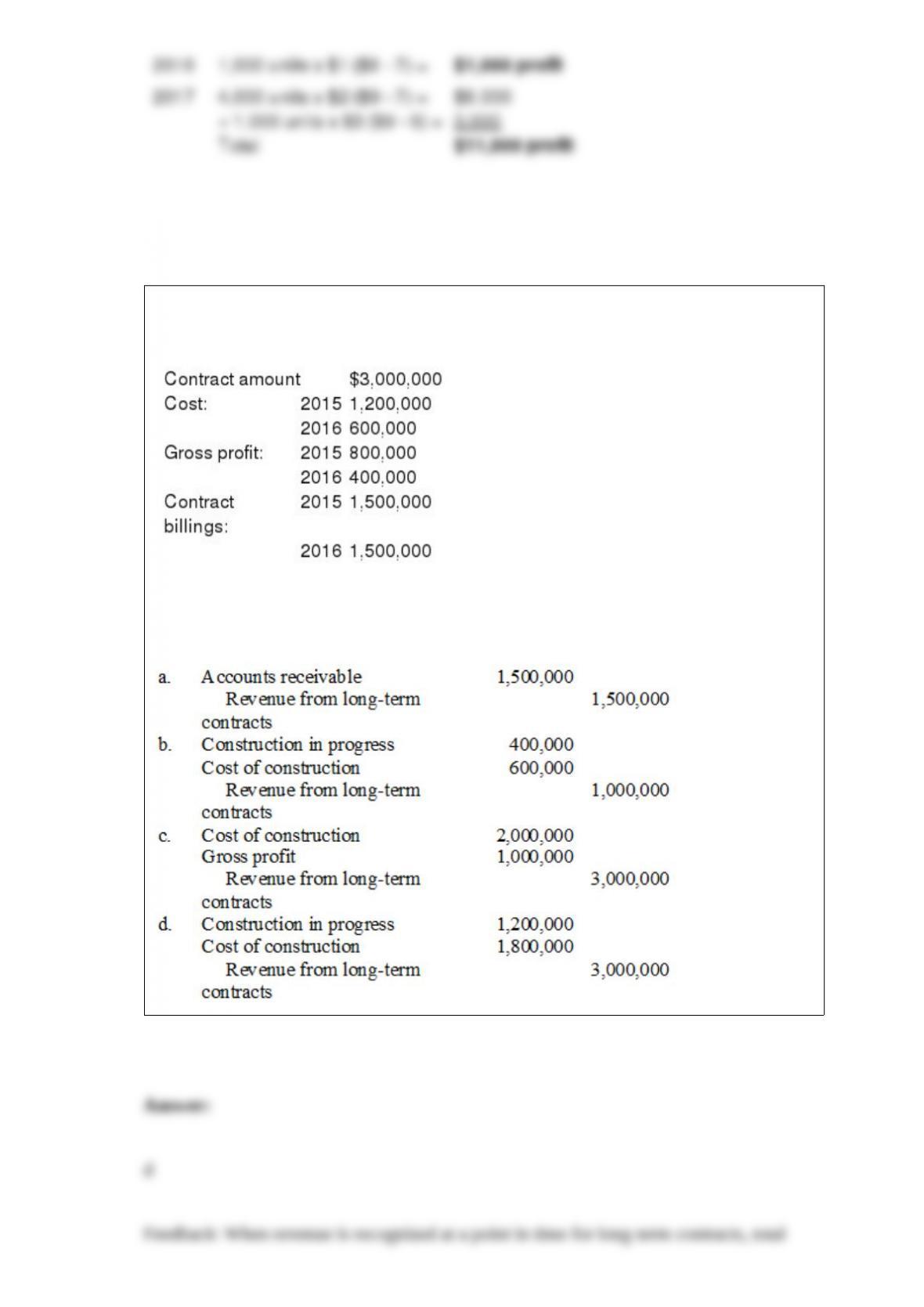

Arizona Desert Homes (ADH) constructed a new subdivision during 2015 and 2016

under contract with Cactus Development Co. Relevant data are summarized below:

ADH recognizes revenue upon completion of the contract.

What is the journal entry in 2016 to record revenue?

Colorado Consulting Company has been using the sum-of-the-years’-digits depreciation

method to depreciate some office equipment that was acquired at the beginning of 2014.

At the beginning of 2016, Colorado Consulting decided to change to the straight-line

method. The equipment cost $120,000 and is expected to have no salvage value. The

estimated useful life of the equipment is five years. Ignore income taxes.

Required:

1) Prepare the appropriate journal entry, if any, to record the accounting change.

2) Prepare the journal entry to record depreciation for 2016.

On September 1, 2016, Jacob Furniture Mart enters into a tentative agreement to sell

the assets of its office equipment division. This division qualifies as a component of the

entity according to GAAP regarding discontinued operations. The division’s

contribution to Jacob’s operating income for 2016 was a $3 million loss before taxes.

Jacob has an average tax rate of 30%. Required: Consider independently the

appropriate accounting by Jacob under the three scenarios below.

Scenario 2: Assume that Jacob had not yet sold the division’s assets by the end of 2016.

Further, assume that the fair value less costs to sell of the division’s assets at December

31, 2016, was $24 million and was expected to remain the same when the assets are

sold in 2017. The book value of the division’s assets was $19 million at the end of the

year. Under these assumptions, what would Jacob report in its 2016 income statement

regarding the office equipment division? Explain where this information would be

presented.

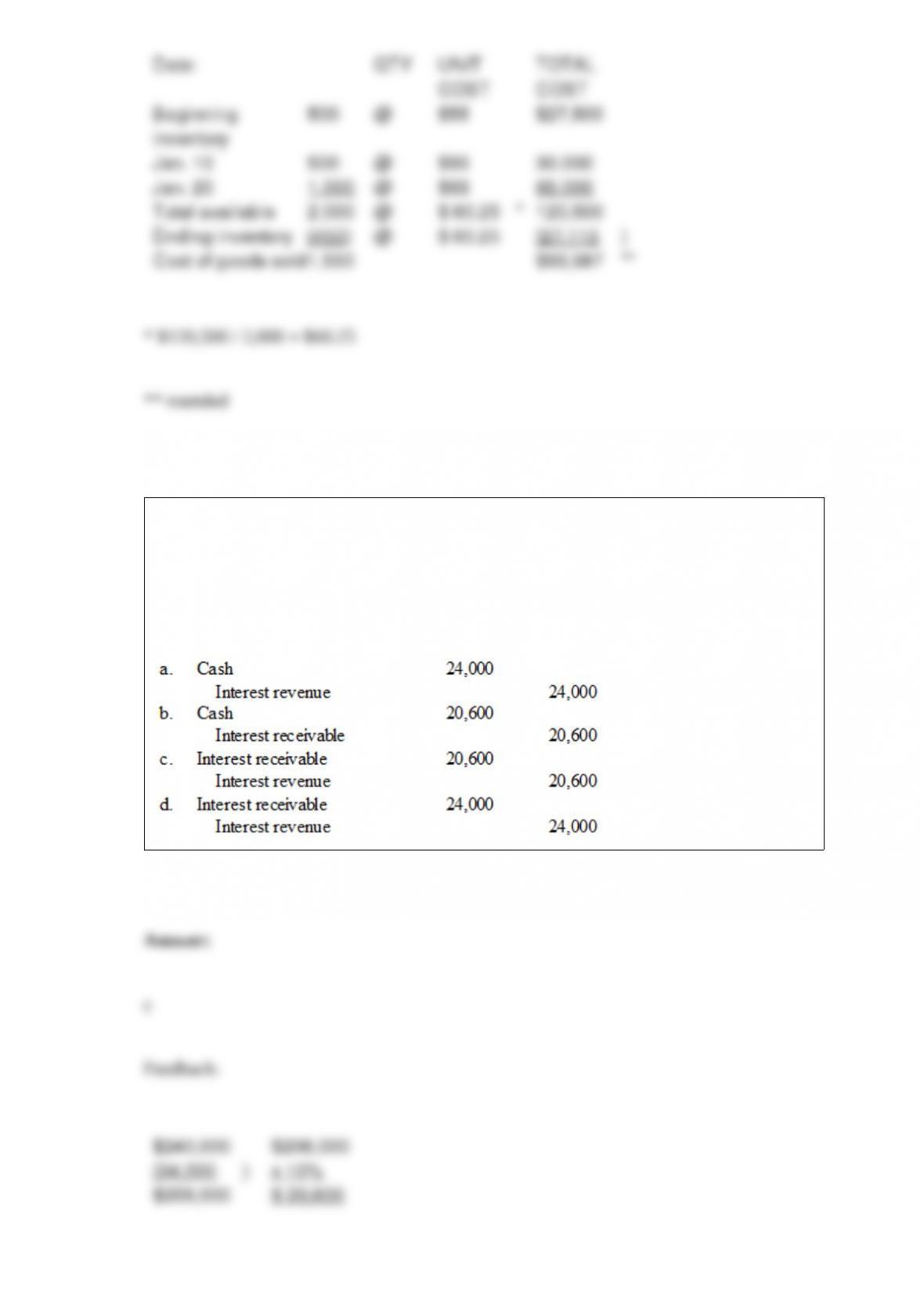

Shown below is activity for one of the products of Denver Office Equipment: January 1

balance, 500 units @ $55 $27,500

Purchases:

January 10: 500 units @ $60

January 20: 1,000 units @ $63

Sales:

January 12: 800 units

January 28: 750 units Required: Compute the January 31 ending inventory and cost of

goods sold for January, assuming Denver uses average cost and a periodic inventory

system.

On January 1, 2016, Calloway Company leased a machine to Zone Corporation. The

lease qualifies as a direct financing lease. Calloway paid $240,000 for the machine and

is leasing it to Zone for $34,000 per year, an amount that will return 10% to Calloway.

The present value of the minimum lease payments is $240,000. The lease payments are

due each January 1, beginning in 2016. What is the appropriate interest entry on

December 31, 2016?