1) The actual manufacturing overhead incurred at Fraze Corporation during November

was $79,000, while the manufacturing overhead applied to Work in Process was

$65,000. The Corporation’s Cost of Goods Sold was $385,000 prior to closing out its

Manufacturing Overhead account. The Corporation closes out its Manufacturing

Overhead account to Cost of Goods Sold. Which of the following statements is true?

A.Manufacturing overhead for the month was underapplied by $14,000; Cost of Goods

Sold after closing out the Manufacturing Overhead account is $399,000

B.Manufacturing overhead for the month was overapplied by $14,000; Cost of Goods

Sold after closing out the Manufacturing Overhead account is $371,000

C.Manufacturing overhead for the month was overapplied by $14,000; Cost of Goods

Sold after closing out the Manufacturing Overhead account is $399,000

D.Manufacturing overhead for the month was underapplied by $14,000; Cost of Goods

Sold after closing out the Manufacturing Overhead account is $371,000

2) Rank the products in order of their current profitability from most profitable to least

profitable. In other words, rank the products in the order in which they should be

emphasized.

A.PW,UN,ZG

B.UN,ZG,PW

C.ZG,PW,UN

D.UN,PW,ZG

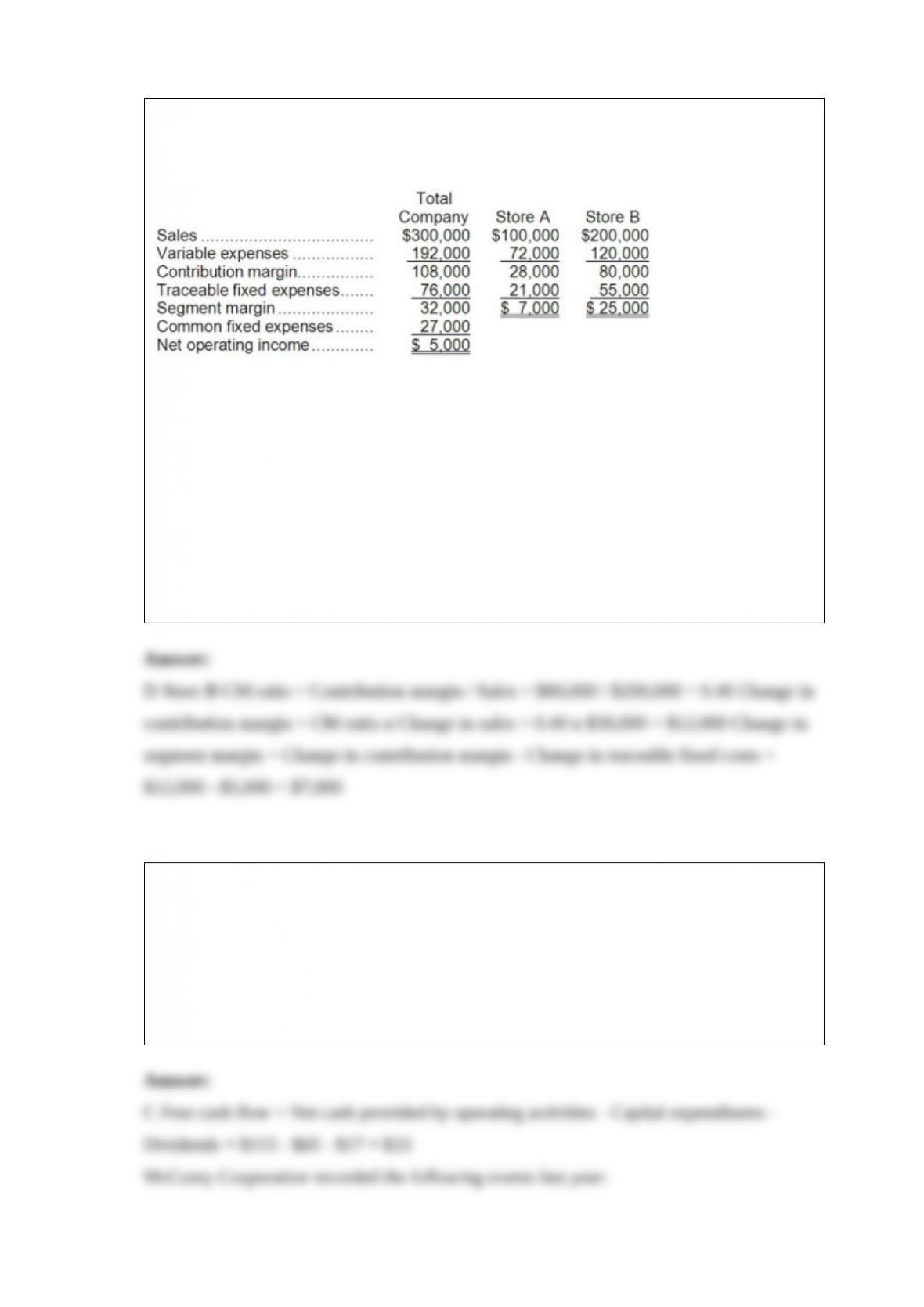

3) O’Neill, Incorporated’s segmented income statement for the most recent month is

given below.

For each of the following questions, refer back to the above original data.

If sales in Store B increase by $30,000 as a result of a $5,000 increase in traceable fixed

expenses:

A.the contribution margin should increase by $18,000

B.the segment margin should increase by $17,000

C.the contribution margin should increase by $12,000

D.the segment margin should increase by $7,000

4) Beacham Corporation’s net cash provided by operating activities was $115; its net

income was $95; its capital expenditures were $65; and its cash dividends were $17.

The company’s free cash flow was:

A.$292

B.$13

C.$33

D.$128

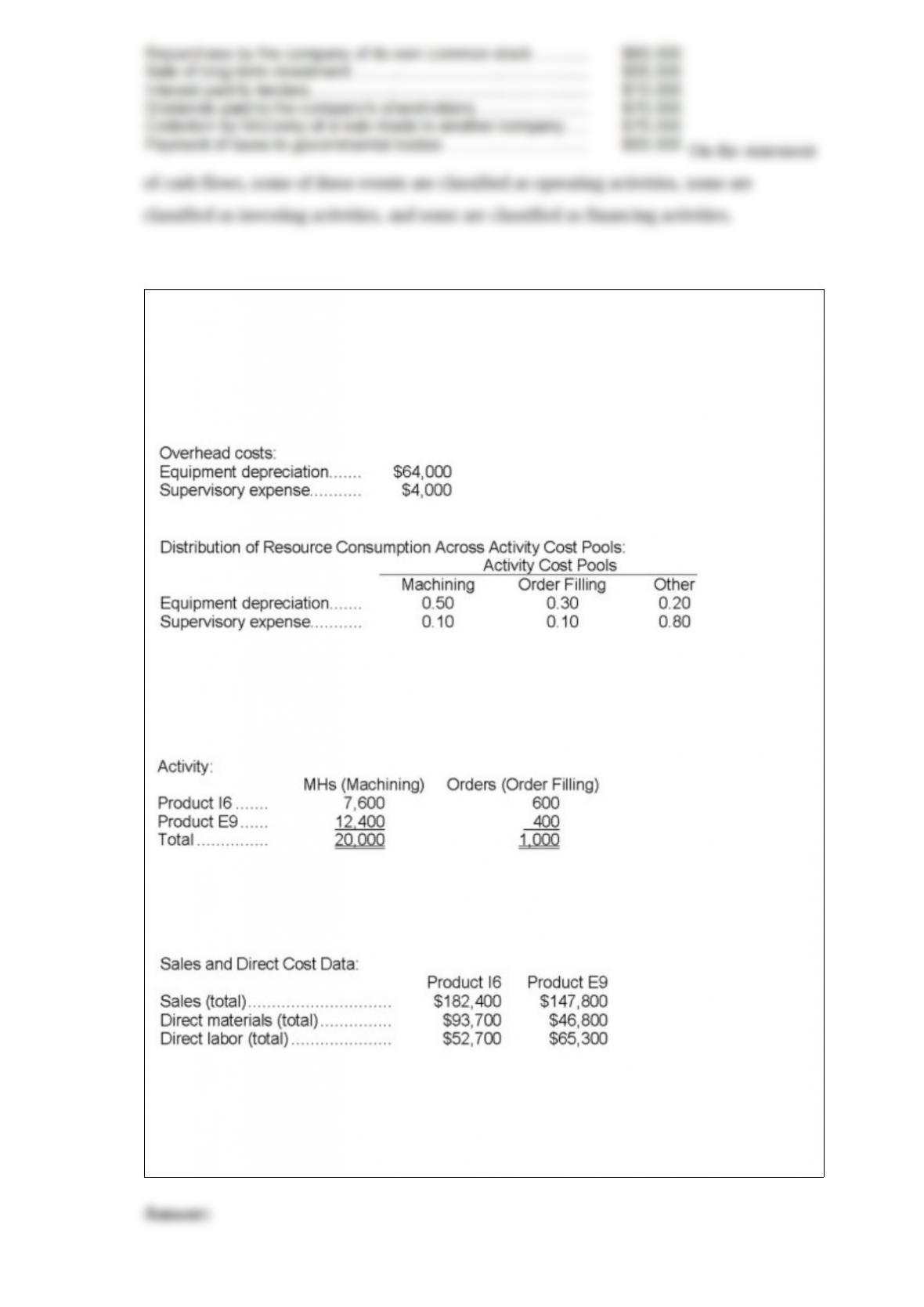

5) Vontungeln Corporation uses activity-based costing to compute product margins. In

the first stage, the activity-based costing system allocates two overhead

accounts-equipment depreciation and supervisory expense-to three activity cost

pools-Machining, Order Filling, and Other-based on resource consumption. Data to

perform these allocations appear below:

In the second stage, Machining costs are assigned to products using machine-hours

(MHs) and Order Filling costs are assigned to products using the number of orders. The

costs in the Other activity cost pool are not assigned to products.

Finally, sales and direct cost data are combined with Machining and Order Filling costs

to determine product margins.

What is the product margin for Product I6 under activity-based costing?

A.$2,000

B.$36,000

C.$11,928

D.$23,688

6) The company’s earnings per share for Year 2 is closest to:

A.$8.18 per share

B.$0.38 per share

C.$0.54 per share

D.$0.68 per share

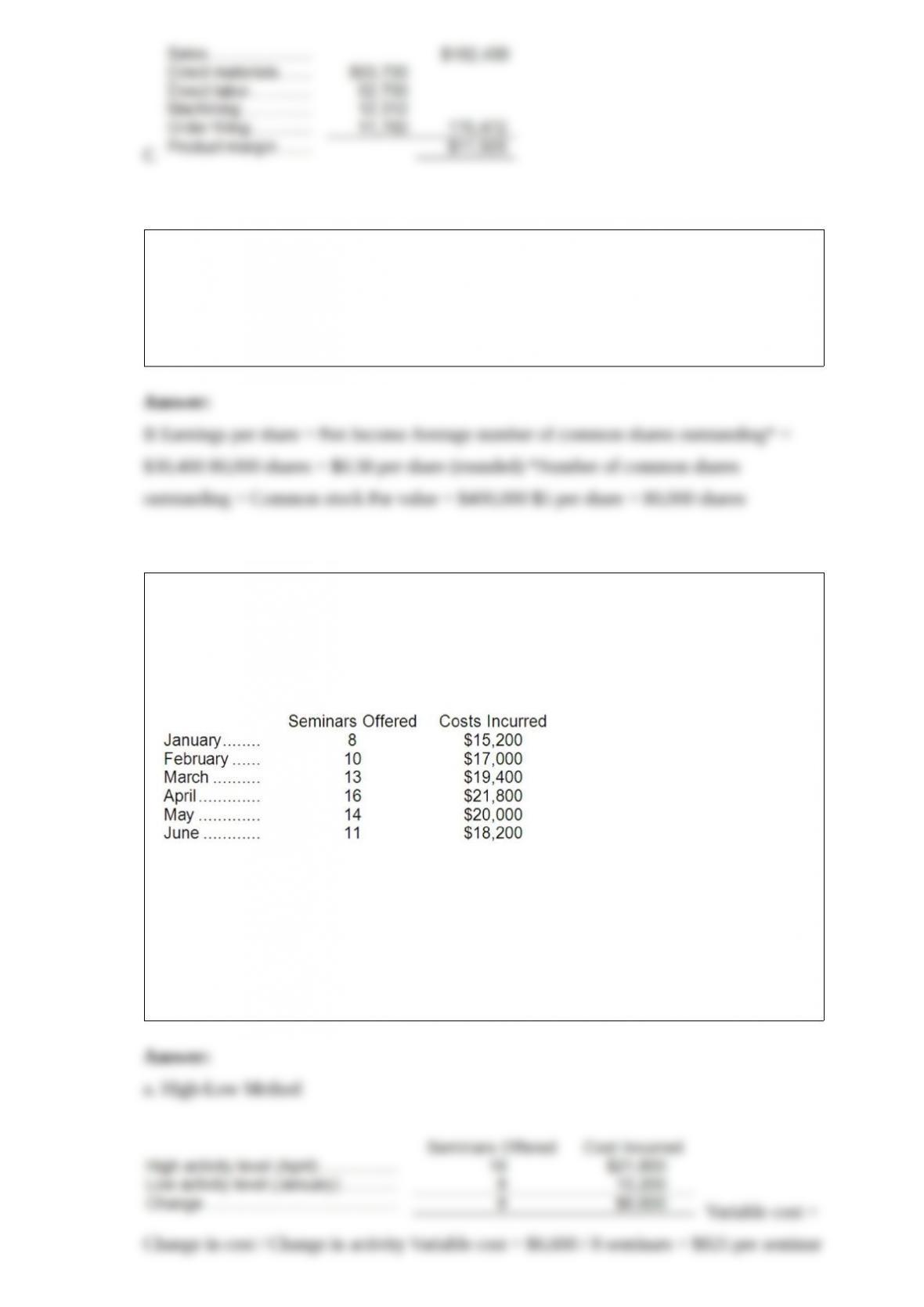

7) CPE for CPAs, Inc., provides continuing professional education for certified public

accountants. The company is relatively new and management is seeking information

regarding the company’s cost structure. The following information has been gathered

for the first six months of the current year:

Required:

a. Using the high-low method, estimate the variable cost per seminar and the total fixed

cost per month.

b. Using the least-squares regression method, estimate the variable cost per seminar and

the total fixed cost per month.

8) ( Neighbors Corporation is considering a project that would require an investment of

$279,000 and would last for 8 years. The incremental annual revenues and expenses

generated by the project during those 8 years would be as follows:

The scrap value of the project’s assets at the end of the project would be $15,000. The

cash inflows occur evenly throughout the year. The payback period of the project is

closest to:

A.2.0 years

B.2.6 years

C.2.5 years

D.1.9 years

9) How many units of product G16F should be produced each month?

A.570

B.250

C.1,041

D.0

10) From the standpoint of the entire company, if it is a choice between sales of one unit

of one product versus another, which product should the salespersons emphasize?

A.I200

B.I100

C.I300

D.I400

11) The company’s debt-to-equity ratio at the end of Year 2 is closest to:

A.0.29

B.0.38

C.0.23

D.0.64

12) The market price of Friden Company’s common stock increased from $15 to $18.

Earnings per share of common stock remained unchanged. The company’s

price-earnings ratio would:

A.increase.

B.decrease.

C.remain unchanged.

D.impossible to determine.

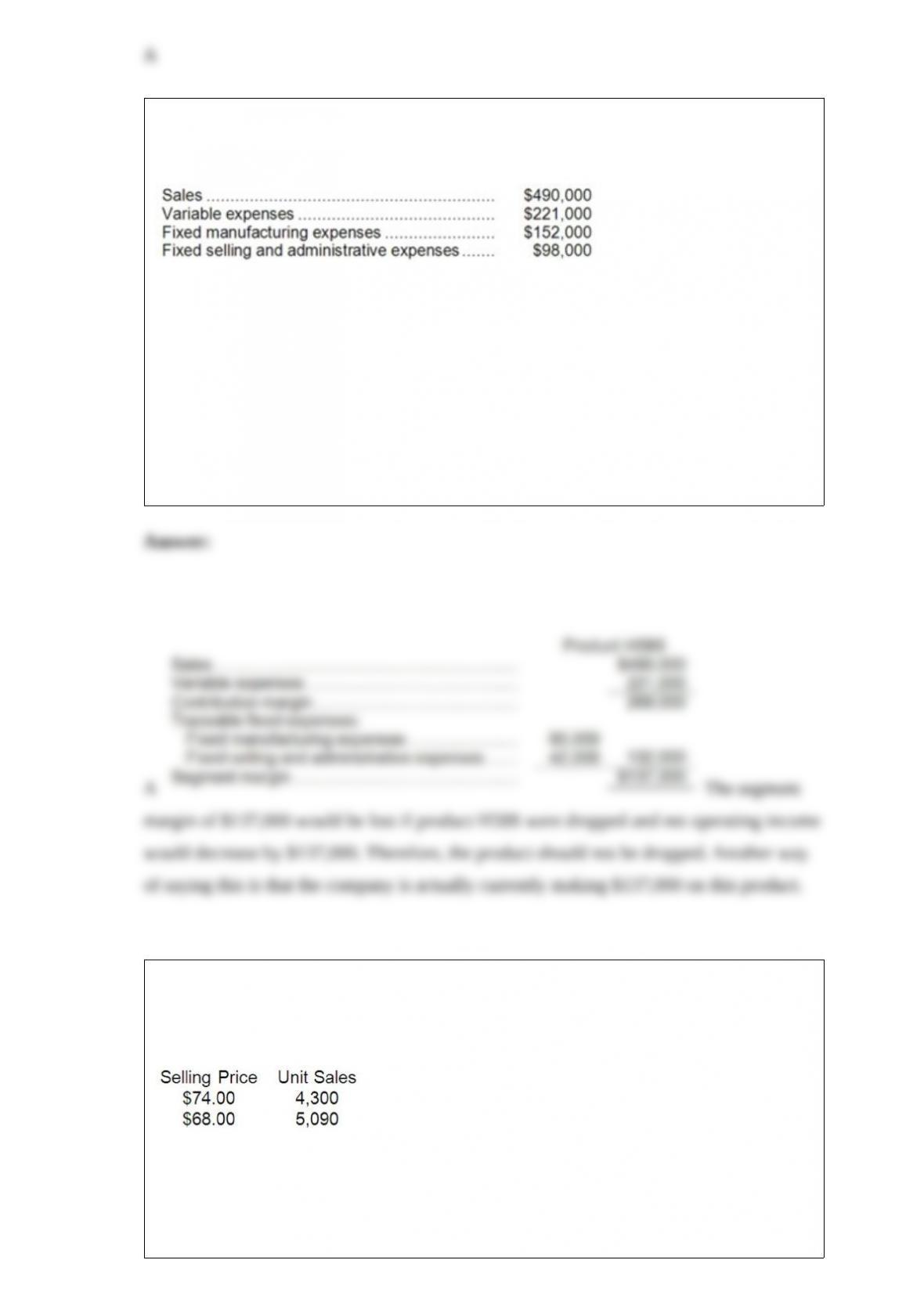

13) The management of Fannin Corporation is considering dropping product H58S.

Data from the company’s accounting system appear below:

In the company’s accounting system all fixed expenses of the company are fully

allocated to products. Further investigation has revealed that $90,000 of the fixed

manufacturing expenses and $42,000 of the fixed selling and administrative expenses

are avoidable if product H58S is discontinued. What would be the effect on the

company’s overall net operating income if product H58S were dropped?

A.Overall net operating income would decrease by $137,000.

B.Overall net operating income would increase by $137,000.

C.Overall net operating income would decrease by $151,000.

D.Overall net operating income would increase by $151,000.

14) Ingham Corporation recently changed the selling price of one of its products. Data

concerning sales for comparable periods before and after the price change are presented

below.

The product’s variable cost is $16.40 per unit.

According to the formula in the text, the product’s profit-maximizing price is closest to:

A.$35.82

B.$32.89

C.$35.23

D.$20.74

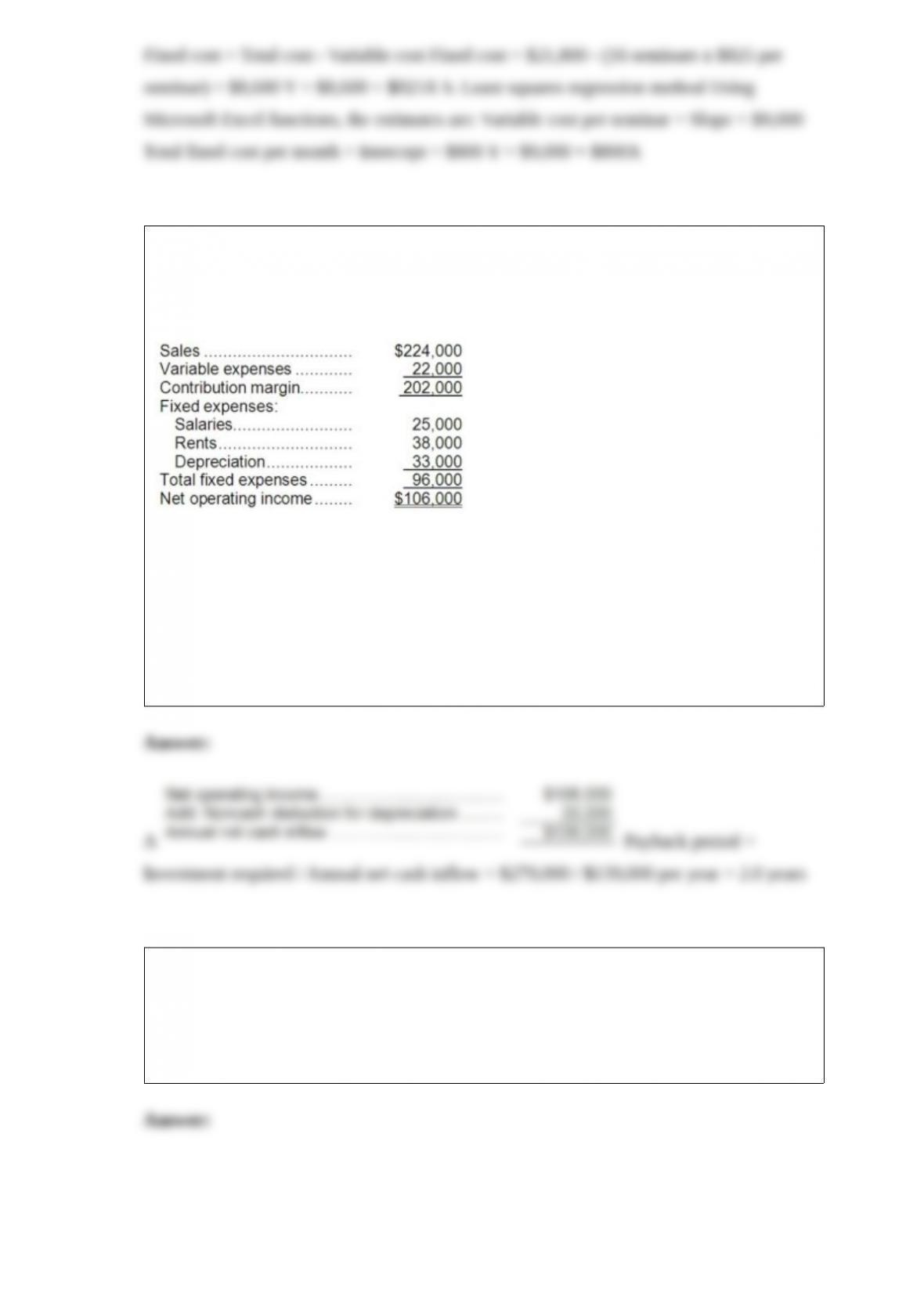

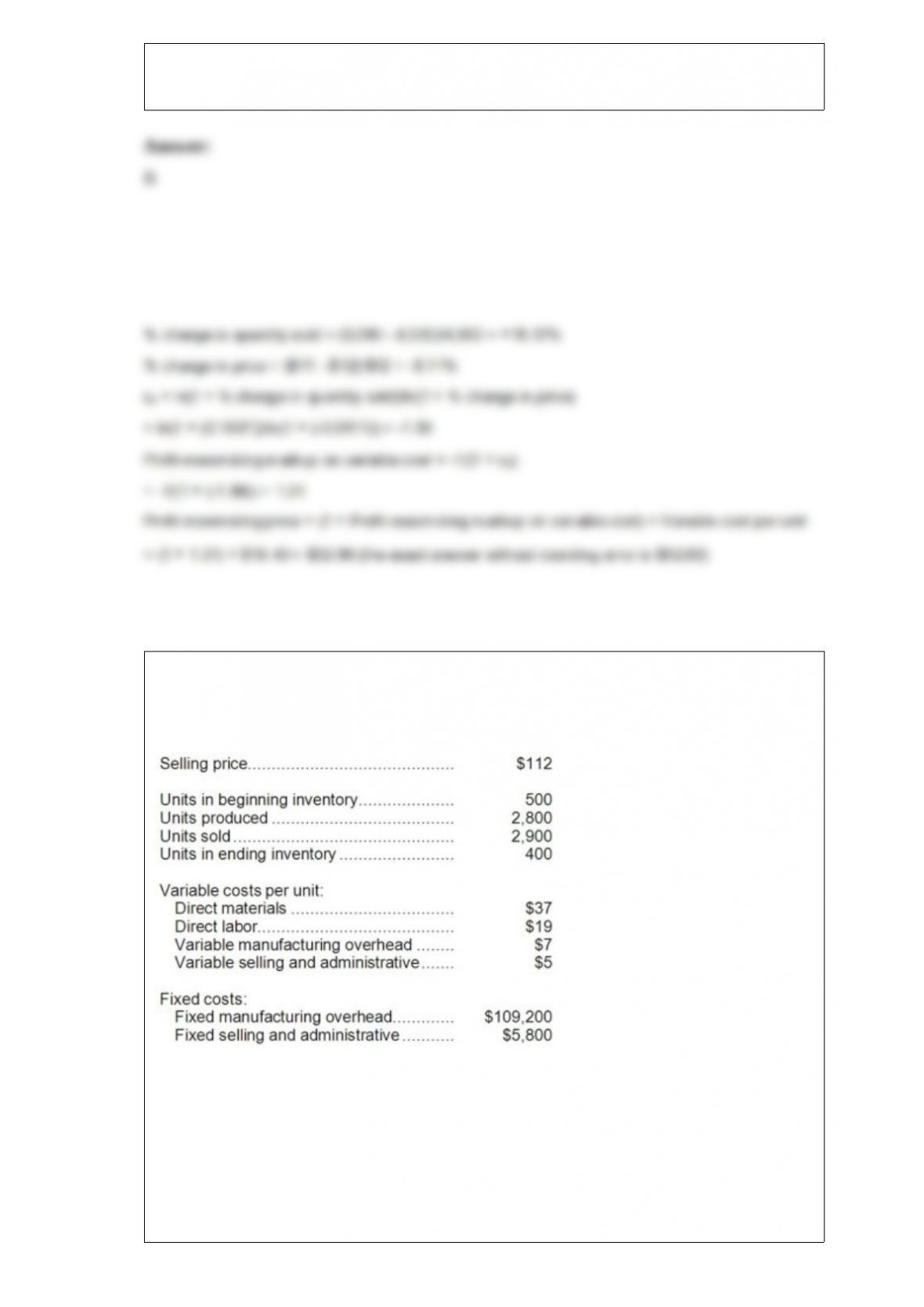

15) Pabbatti Corporation, which has only one product, has provided the following data

concerning its most recent month of operations:

The company produces the same number of units every month, although the sales in

units vary from month to month. The company’s variable costs per unit and total fixed

costs have been constant from month to month.

Required:

a. What is the unit product cost for the month under variable costing?

b. Prepare a contribution format income statement for the month using variable costing.

c. Without preparing an income statement, determine the absorption costing net

operating income for the month. (Hint: Use the reconciliation method.)