1) alake company is a manufacturing firm that uses job-order costing. at the beginning

of the year, the company’s inventory balances were as follows:

the company applies overhead to jobs using a predetermined overhead rate based on

machine-hours. at the beginning of the year, the company estimated that it would work

36,000 machine-hours and incur $216,000 in manufacturing overhead cost. the

following transactions were recorded for the year:

a. raw materials were purchased, $443,000.

b. raw materials were requisitioned for use in production, $450,000 ($435,000 direct

and $15,000 indirect).

c. the following employee costs were incurred: direct labor, $229,000; indirect labor,

$54,000; and administrative salaries, $117,000.

d. selling costs, $119,000.

e. factory utility costs, $21,000.

f. depreciation for the year was $121,000 of which $114,000 is related to factory

operations and $7,000 is related to selling, general, and administrative activities.

g. manufacturing overhead was applied to jobs. the actual level of activity for the year

was 38,000 machine-hours.

h. the cost of goods manufactured for the year was $910,000.

i. sales for the year totaled $1,173,000 and the costs on the job cost sheets of the goods

that were sold totaled $895,000.

j. the balance in the manufacturing overhead account was closed out to cost of goods

sold.

required:

prepare the appropriate journal entry for each of the items above (a. through j.). you can

assume that all transactions with employees, customers, and suppliers were conducted

in cash.

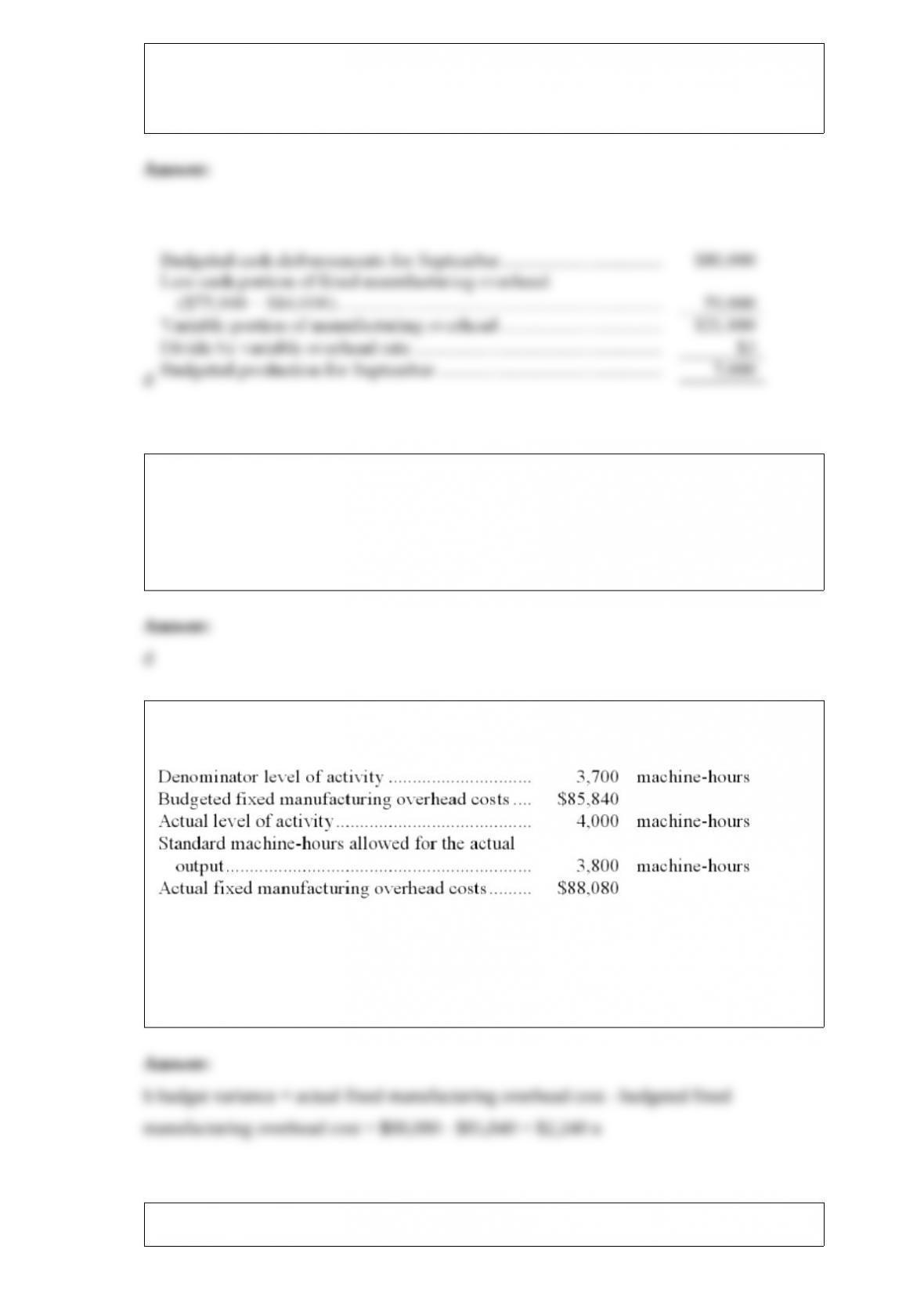

2) the culver company is preparing its manufacturing overhead budget for the third

quarter of the year. budgeted variable factory overhead is $3.00 per unit produced;

budgeted fixed factory overhead is $75,000 per month, with $16,000 of this amount

being factory depreciation.

if the budgeted cash disbursements for factory overhead for september are $80,000,

then the budgeted production for september must be:

a.7,400 units

b.6,200 units

c.6,500 units

d.7,000 units

3) an example of a period cost is:

a.fire insurance on a factory building

b.salary of a factory supervisor

c.direct materials

d.rent on a headquarters building

4) the following data for august has been provided by mirabelli corporation.

the budget variance for august is:

a.$6,960 f

b.$2,240 u

c.$2,240 f

d.$6,960 u

5) scott company’s variable expenses are 72% of sales. the company’s break-even point

in dollar sales is $2,450,000. if sales are $60,000 below the break-even point, the

company would report a:

a.$43,200 loss

b.$60,000 loss

c.$16,800 loss

d.cannot be determined from the data given

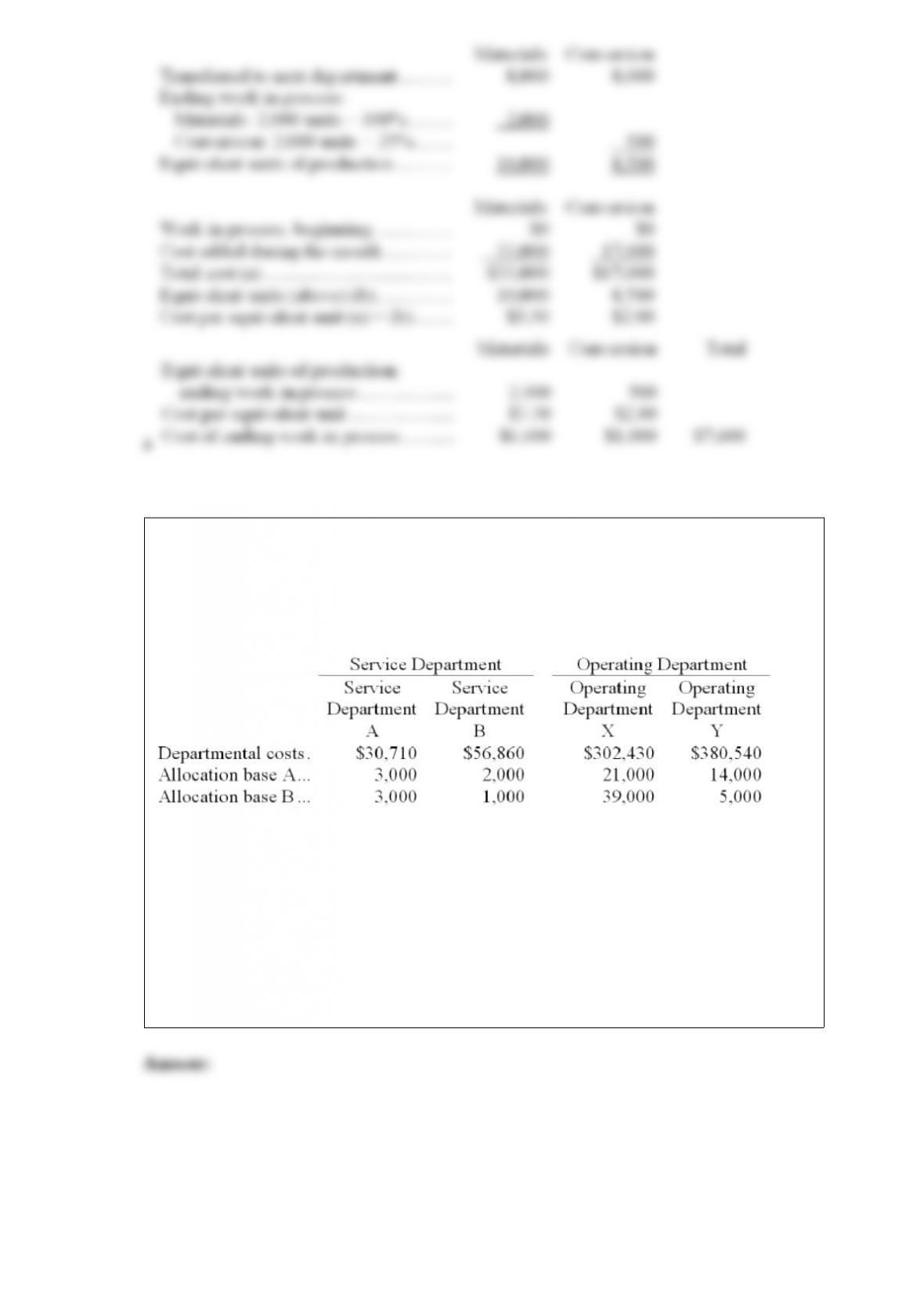

6) a sporting goods manufacturer buys wood as a direct material for baseball bats. the

forming department processes the baseball bats, and the bats are then transferred to the

finishing department where a sealant is applied. there was no beginning work in process

inventory in the forming department in may. the forming department began

manufacturing 10,000 casey slugger baseball bats during may. costs for the forming

department for the month of may were as follows:

a total of 8,000 bats were completed and transferred to the finishing department during

may. the ending work in process inventory was 100% complete with respect to direct

materials and 25% complete with respect to conversion costs. the company uses the

weighted-average method of process costing.

the cost of the work in process inventory in the finishing department at the end of may

was:

a.$7,600

b.$10,000

c.$2,500

d.$4,000

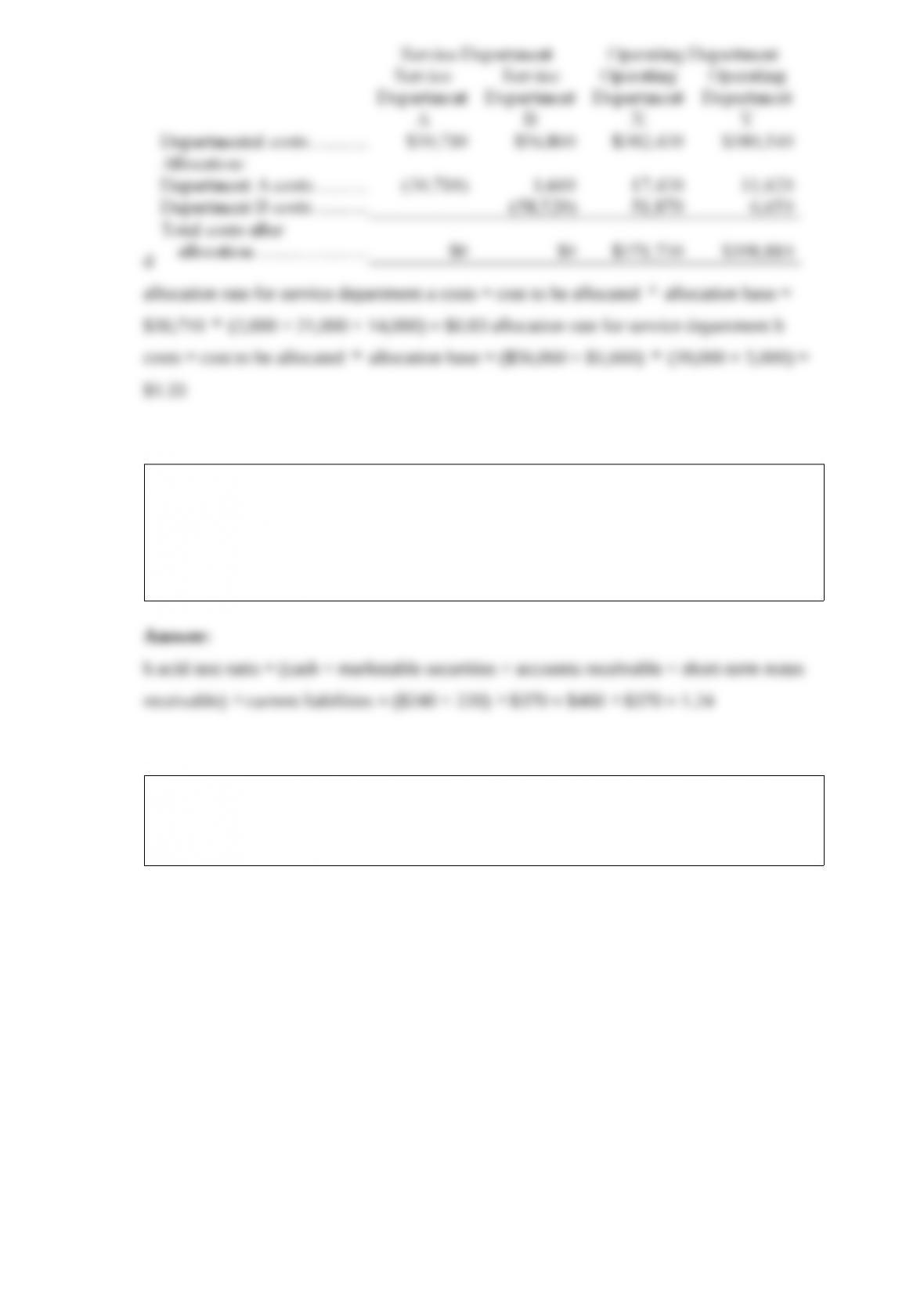

7) karnofski corporation uses the step-down method to allocate service department costs

to operating departments. the company has two service departments, service department

a and service department b, and two operating departments, operating department x and

operating department y. data concerning those departments follow:

service department a costs are allocated first on the basis of allocation base a and

service department b costs are allocated second on the basis of allocation base b.

in the first step of the allocation, the amount of service department a cost allocated to

the operating department x is closest to:

a.$13,599

b.$18,426

c.$16,123

d.$17,430

8) the acid-test ratio at the end of year 2 is closest to:

a.1.76

b.1.24

c.1.05

d.1.41

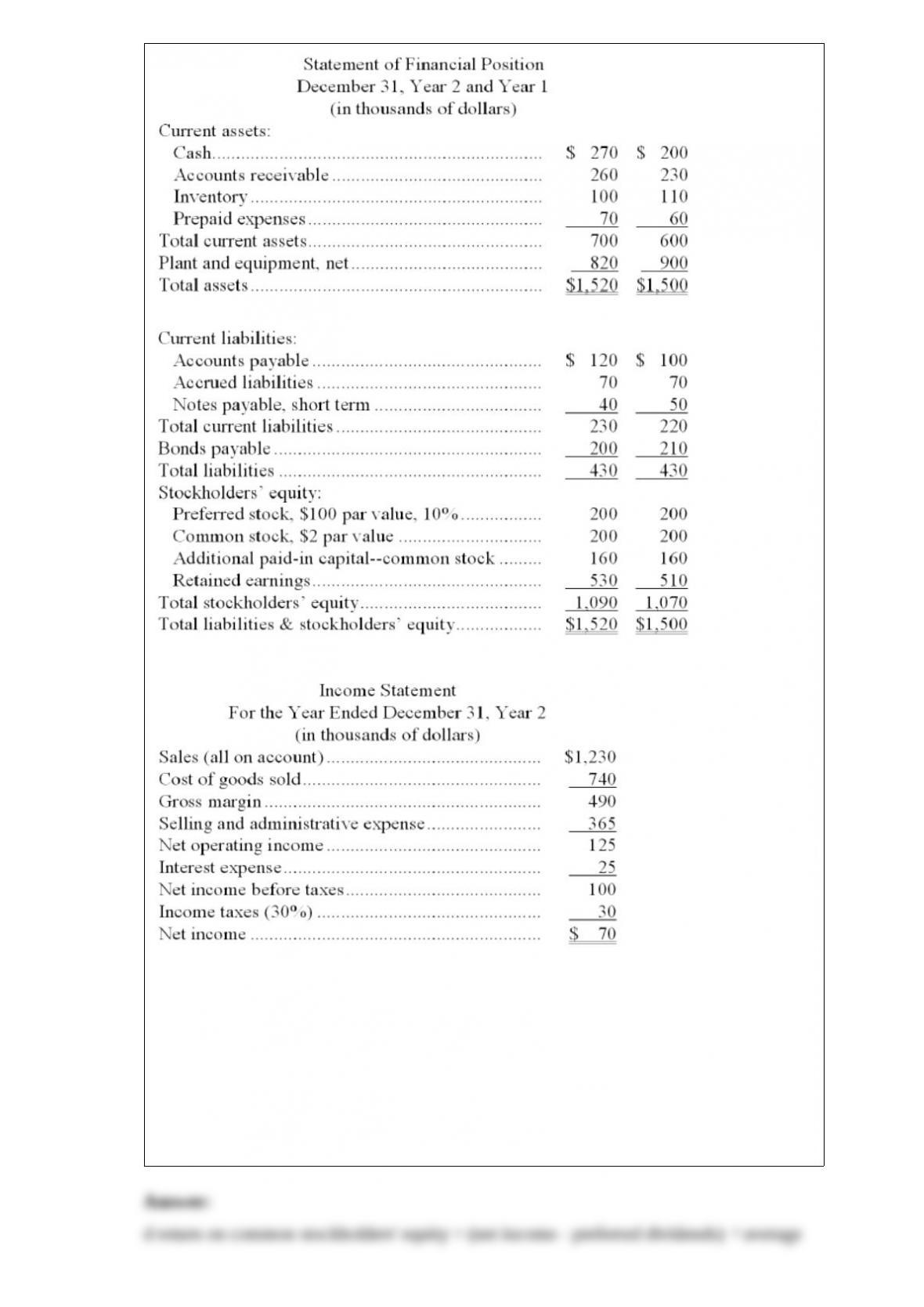

9) dadisman corporation’s most recent balance sheet and income statement appear

below:

dividends on common stock during year 2 totaled $30 thousand. dividends on preferred

stock totaled $20 thousand. the market price of common stock at the end of year 2 was

$6.75 per share.

the return on common stockholders’ equity for year 2 is closest to:

a.7.95%

b.4.63%

c.6.48%

d.5.68%

10) (ignore income taxes in this problem.) noe corporation has entered into a 8 year

lease for a building it will use as a warehouse. the annual payment under the lease will

be $2,520. the first payment will be at the end of the current year and all subsequent

payments will be made at year-ends. what is the present value of the lease payments if

the discount rate is 12%?

a.$8,142

b.$12,519

c.$20,160

d.$18,000

11) noskey corporation’s budgeted total cash receipts in august are:

a.$240,000

b.$294,000

c.$299,400

d.$239,400

12) witczak company has a single product and currently has a degree of operating

leverage of 5. which of the following will increase witczak’s degree of operating

leverage?

a.choice a

b.choice b

c.choice c

d.choice d