1) A company’s current ratio and an acid-test ratio are both greater than 1. Payment of

an account payable would:

A.increase the current ratio but the acid-test ratio would not be affected.

B.increase the acid-test ratio but the current ratio would not be affected.

C.increase both the current and acid-test ratios.

D.decrease both the current and acid-test ratios.

2) Thoen Nuptial Bakery makes very elaborate wedding cakes to order. The company

has an activity-based costing system with three activity cost pools. The activity rate for

the Size-Related activity cost pool is $0.96 per guest. (The greater the number of guests,

the larger the cake.) The activity rate for the Complexity-Related cost pool is $54.24 per

tier. (Cakes with more tiers are more complex.) Finally, the activity rate for the

Order-Related activity cost pool is $56.44 per order. (Each wedding involves one order

for a cake.) The activity rates include the costs of raw ingredients such as flour, sugar,

eggs, and shortening. The activity rates do not include the costs of purchased

decorations such as miniature statues and wedding bells, which are accounted for

separately.

Data concerning two recent orders appear below:

Assuming that the company charges $584.18 for the Strobl wedding cake, what would

be the overall margin on the order?

A.$157.83

B.$101.39

C.$132.70

D.$482.79

3) Foster Company makes 20,000 units per year of a part it uses in the products it

manufactures. The unit product cost of this part is computed as follows:

An outside supplier has offered to sell the company all of these parts it needs for $51.80

a unit. If the company accepts this offer, the facilities now being used to make the part

could be used to make more units of a product that is in high demand. The additional

contribution margin on this other product would be $44,000 per year.

If the part were purchased from the outside supplier, all of the direct labor cost of the

part would be avoided. However, $5.10 of the fixed manufacturing overhead cost being

applied to the part would continue even if the part were purchased from the outside

supplier. This fixed manufacturing overhead cost would be applied to the company’s

remaining products.

Required:

a. How much of the unit product cost of $56.70 is relevant in the decision of whether to

make or buy the part?

b. What is the net total dollar advantage (disadvantage) of purchasing the part rather

than making it?

c. What is the maximum amount the company should be willing to pay an outside

supplier per unit for the part if the supplier commits to supplying all 20,000 units

required each year?

4) The management of Shastri Corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity rather than on the

estimated amount of activity for the year. The company’s controller has provided an

example to illustrate how this new system would work. In this example, the allocation

base is machine-hours and the estimated amount of the allocation base for the upcoming

year is 69,000 machine-hours. In addition, capacity is 76,000 machine-hours and the

actual activity for the year is 71,600 machine-hours. All of the manufacturing overhead

is fixed and is $3,461,040 per year. For simplicity, it is assumed that this is the

estimated manufacturing overhead for the year as well as the manufacturing overhead at

capacity and the actual amount of manufacturing overhead for the year. Job Z67J,

which required 330 machine-hours, is one of the jobs worked on during the year.

Required:

a. Determine the predetermined overhead rate if the predetermined overhead rate is

based on the estimated amount of the allocation base.

b. Determine how much overhead would be applied to Job Z67J if the predetermined

overhead rate is based on estimated amount of the allocation base.

c. Determine the underapplied or overapplied overhead for the year if the predetermined

overhead rate is based on the estimated amount of the allocation base.

d. Determine the predetermined overhead rate if the predetermined overhead rate is

based on the amount of the allocation base at capacity.

e. Determine how much overhead would be applied to Job Z67J if the predetermined

overhead rate is based on the amount of the allocation base at capacity.

f. Determine the underapplied or overapplied overhead for the year if the predetermined

overhead rate is based on the amount of the allocation base at capacity.

5) Assume that after introducing the new product, the company finds that it has excess

capacity. A foreign dealer has offered to purchase 2,000 units at a special price of $36

per unit. This sale would not disturb regular business. If the special price is accepted on

the 2,000 units, the company’s overall net income for the year should:

A.decrease by $24,000

B.increase by $20,000

C.increase by $8,000

D.increase by $32,000

6) Meyer Corporation has two sales areas: North and South. During April, the

contribution margin in the North was $90,000, or 30% of sales. The segment margin in

the South was $25,000, or 10% of sales. Traceable fixed expenses were $30,000 in the

North and $15,000 in the South. Meyer Corporation reported a total net operating

income of $52,000.

The variable costs for the South area were:

A.$180,000

B.$210,000

C.$225,000

D.$120,000

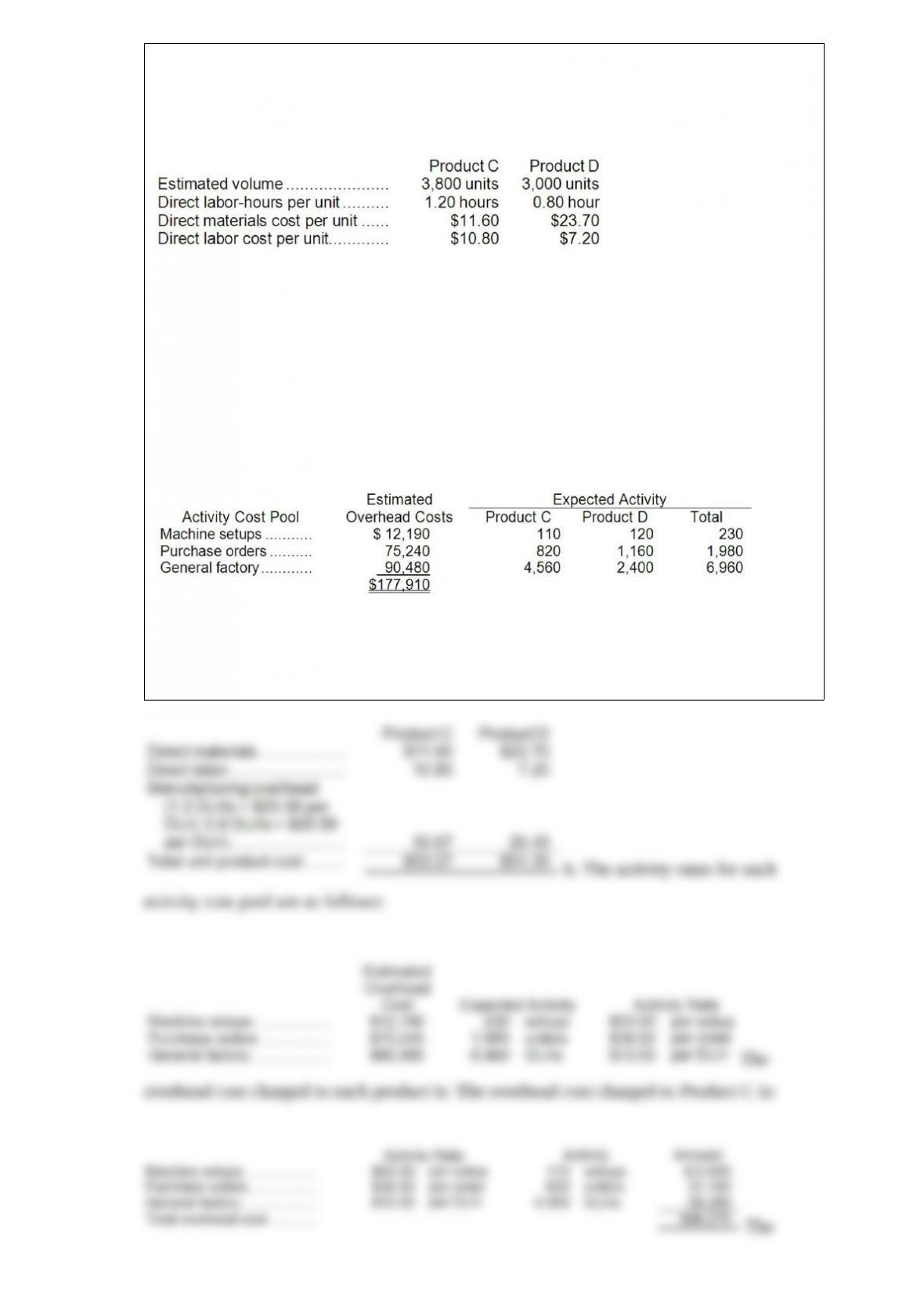

7) Cabat Company manufactures two products, Product C and Product D. The company

estimated it would incur $177,910 in manufacturing overhead costs during the current

period. Overhead currently is applied to the products on the basis of direct labor-hours.

Data concerning the current period’s operations appear below:

Required:

a. Compute the predetermined overhead rate under the current method, and determine

the unit product cost of each product for the current year.

b. The company is considering using an activity-based costing system to compute unit

product costs for external financial reports instead of its traditional system based on

direct labor-hours. The activity-based costing system would use three activity cost

pools. Data relating to these activities for the current period are given below:

Determine the unit product cost of each product for the current period using the

activity-based costing approach. General factory overhead is allocated based on direct

labor-hours.

8) The company’s book value per share at the end of the year is closest to:

A.$11.37 per share

B.$7.37 per share

C.$0.19 per share

D.$16.81 per share

9) ( The management of Helberg Corporation is considering a project that would require

an investment of $203,000 and would last for 6 years. The annual net operating income

from the project would be $103,000, which includes depreciation of $30,000. The scrap

value of the project’s assets at the end of the project would be $23,000. The cash

inflows occur evenly throughout the year. The payback period of the project is closest

to:

A.1.5 years

B.2.0 years

C.1.4 years

D.1.7 years

10) Dori Castings is a job order shop that uses a standard cost system. Manufacturing

overhead costs are applied on the basis of standard direct labor-hours. A volume

variance will exist for Dori in a month where:

A.production volume differs from sales volume.

B.actual direct labor-hours differ from standard hours allowed.

C.there is a budget variance in fixed manufacturing overhead costs.

D.the fixed manufacturing overhead applied to units of product on the basis of standard

hours allowed differs from the budgeted fixed manufacturing overhead.

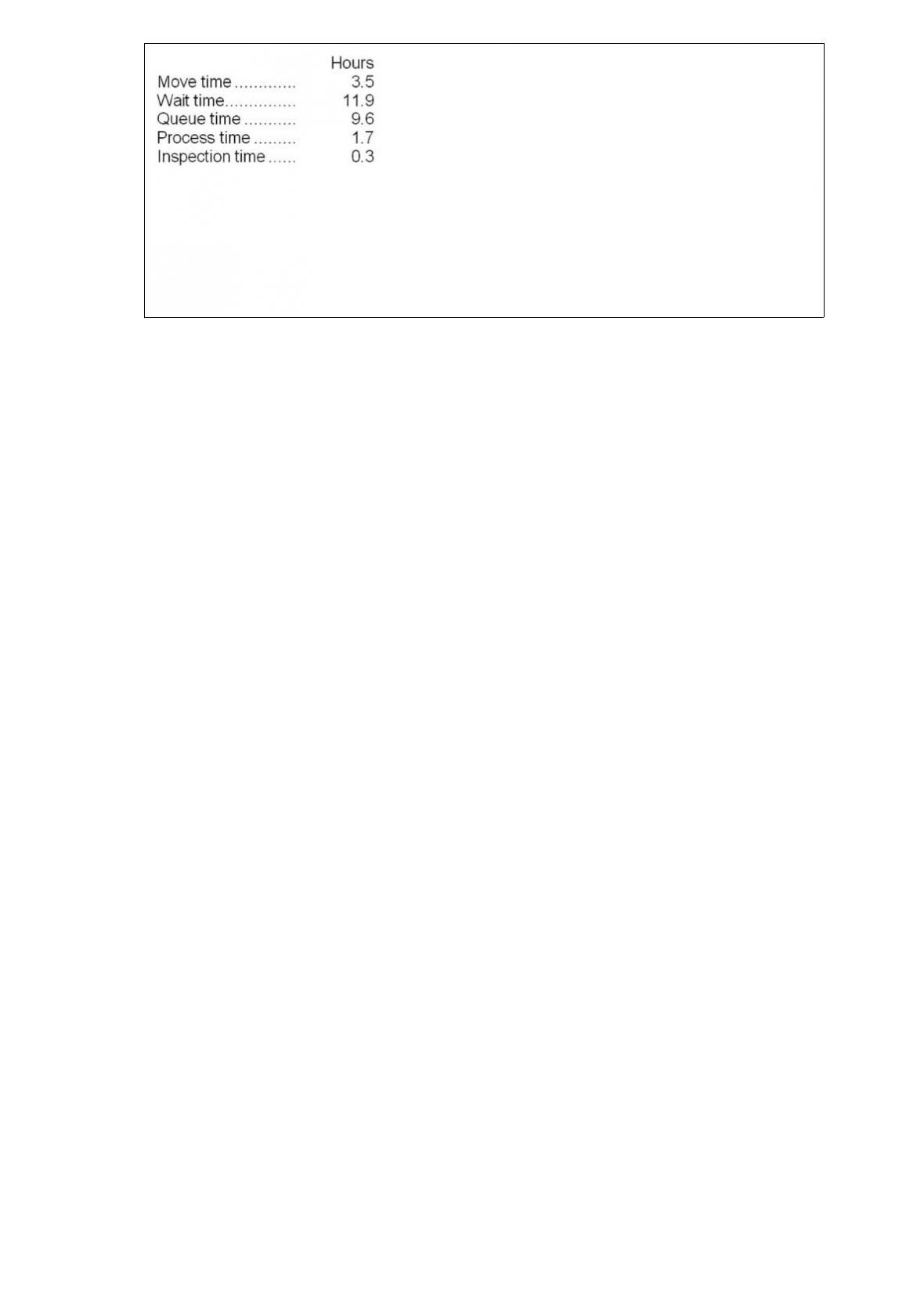

11) Mccubbin Corporation keeps careful track of the time required to fill orders. The

times recorded for a particular order appear below:

The delivery cycle time was:

A.25.0 hours

B.13.1 hours

C.27.0 hours

D.3.5 hours