For a period during which the quantity of inventory at the end was larger than that at the

beginning, income from operations reported under variable costing will be larger than

income from operations reported under absorption costing.

a. True

b. False

Answer:

The ratio of the sum of cash, receivables, and marketable securities to current liabilities

is referred to as the current ratio.

a. True

b. False

Answer:

In a lean environment, the journal entry to record raw materials purchases would

include a debit to the raw and in process inventory account.

a. True

b. False

Answer:

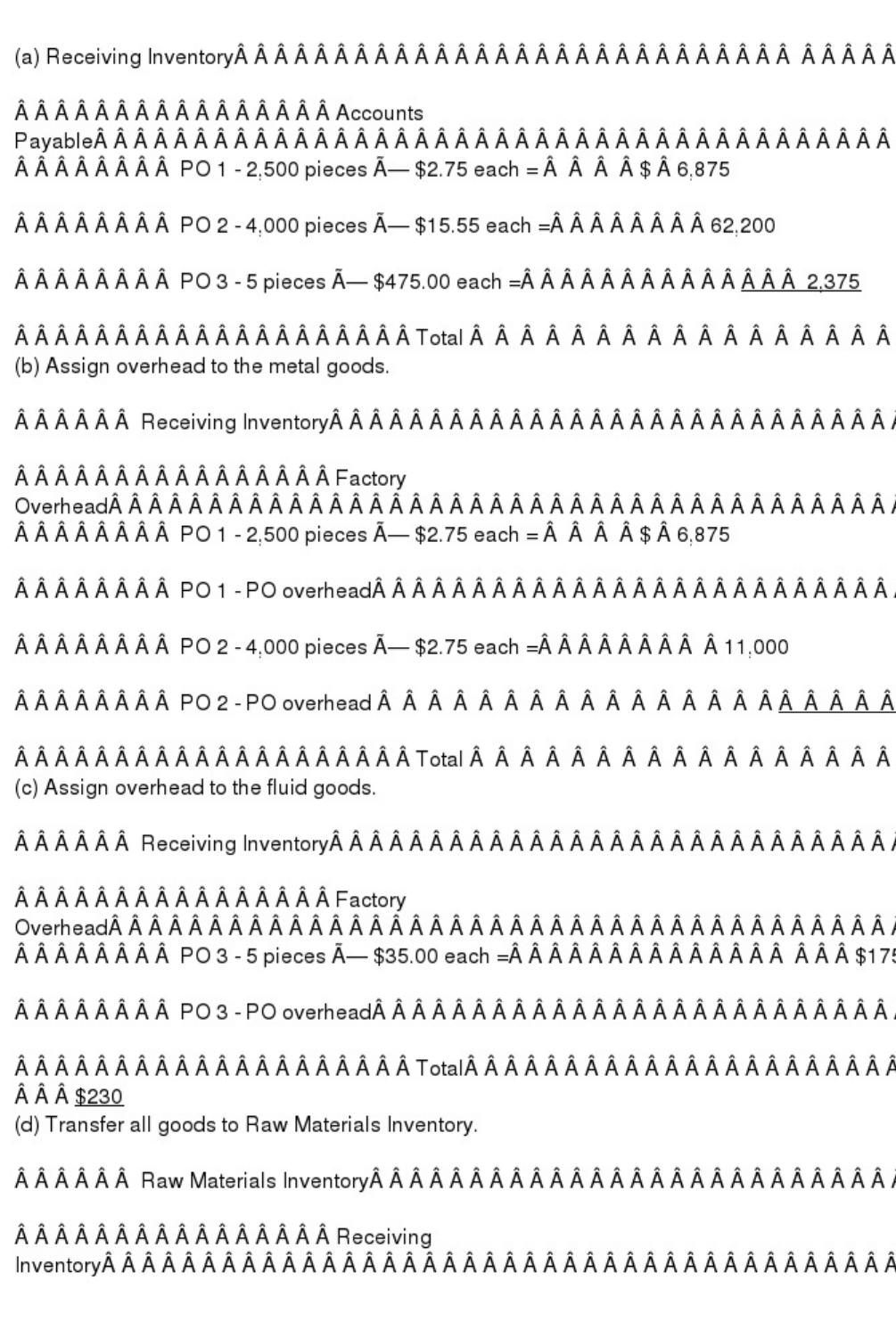

Tough Hardware purchases raw materials and processes those purchases through a

receiving/inspection process prior to stocking for production. Tough places 3 purchase

orders for materials for production and receives the goods that day. The first PO is for

2,500 1/2′ × 96′ milling blanks at $2.75 each. The second is for 4,000 pieces of 48′ × 96′

× 1′ sheet steel at $15.55 each. The third PO is for five 5 gallon drums of milling

lubrication oil at $475.00 per barrel.

The receiving/inspection process is completed and the goods are transferred from

Receiving Inventory to Raw Materials. The Receiving/Inspection Department assigns

manufacturing overhead of $55.00 per purchase order as well as $2.75 per piece on

metal goods and $35.00 per container on fluids. All labor is allocated through overhead.

(a) Write the journal entry to purchase and receive these items to Receiving Inventory

on account.

(b) Assign overhead to the metal goods.

(c) Assign overhead to the fluid goods.

(d) Transfer all goods to Raw Materials Inventory.

Answer:

The cost of materials transferred into the Bottling Department of Mountain Springs

Water Company is $32,400, with $26,000 from the Purifying Department, plus

additional $6,400 from the materials storeroom. The conversion cost for the period in

the Bottling Department is $8,750 ($3,750 factory applied and $5,000 direct labor). The

total costs transferred to finished goods for the period was $31,980. The Bottling

Department had a beginning inventory of $1,860.

a. Journalize the cost of transferred-in materials, conversion costs, and the cost

transferred out to finished goods.

b. Determine the balance of Work in Process’”bottling at the end of the period.

Answer:

In applying the first-in, first-out method of costing inventories, if 8,000 units which are

30% completed are in process at June 1, 28,000 units are completed during June, and

4,000 units were 75% completed at June 30, the number of equivalent units of

production for June was 33,400.

a. True

b. False

Answer:

Work in process inventory on December 31 of the current year is $44,000. Work in

process inventory increased by 60% during the year. Cost of goods manufactured

amounts to $275,000. What are the total manufacturing costs incurred in the current

year?

a. $291,500

b. $302,000

c. $275,750

d. $233,750

Answer:

The amount of increase or decrease in revenue that is expected from a particular course

of action as compared with an alternative is

a. manufacturing margin

b. contribution margin

c. differential cost

d. differential revenue

Answer:

Materials used by the Layton Company’s Division 1 are currently purchased from

outside supplier at $58 per unit. Division 2 is able to supply Division 1 with 22,000

units at a variable cost of $46 per unit. The two divisions have recently negotiated a

transfer price of $50 per unit for the 20,000 units.

(a) By how much will each division’s income increase as a result of this transfer?

(b) What is the total increase in income for Layton?

Answer:

Materials inspection

Identify the following quality control activities as either value-added or

non-value-added.

a. Value-added

b. Non-value-added

Answer:

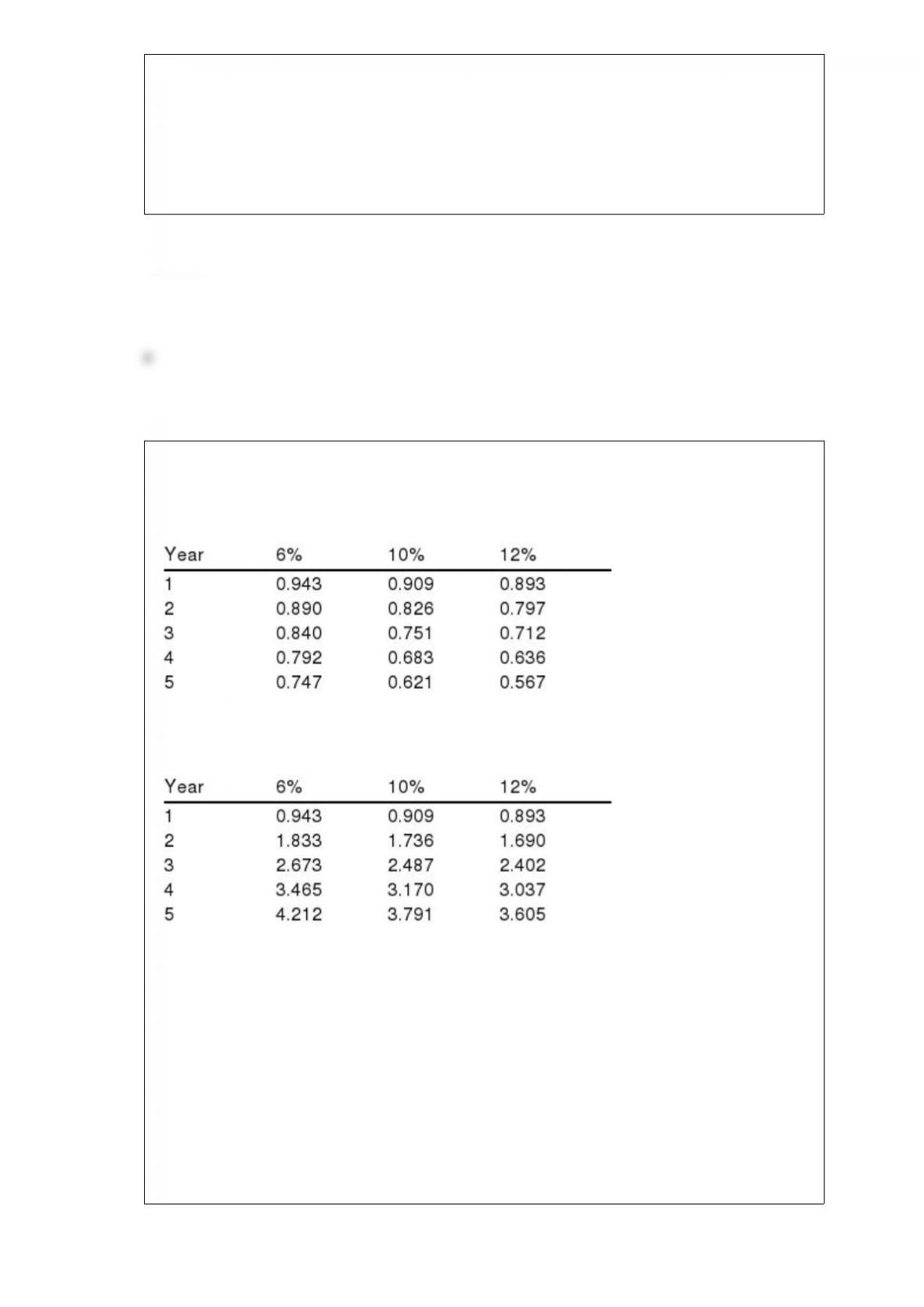

Below is a table for the present value of $1 at compound interest.

Below is a table for the present value of an annuity of $1 at compound interest.

Using the tables above, what would be the present value of $15,000 to be received at

the end of each of the next 2 years, assuming an earnings rate of 6%?

a. $27,495

b. $26,040

c. $30,000

d. $25,350

Answer:

A budget procedure that provides for the maintenance at all times of a twelve-month

projection into the future is called master budgeting.

a. True

b. False

Answer:

The closer a company moves towards just-in-time processing, the differences in unit

costs between average costing and FIFO will be reduced.

a. True

b. False

Answer:

Harley Company has sales of $500,000, variable costs are 75% of sales, and operating

income is $40,000. What is Harley’s operating leverage?

a. 0.0

b. 1.2

c. 1.3

d. 3.1

Answer:

Zorn Co. budgeted $600,000 of factory overhead cost for the coming year. Its plantwide

allocation base, machine hours, is budgeted at 100,000 hours. Budgeted units to be

produced are 200,000 units. Zorn’s plantwide factory overhead rate is $00 per unit.

a. True

b. False

Answer:

Depreciation expense on store equipment for a department store is an indirect expense.

a. True

b. False

Answer:

president’s salary

Match the costs that follow to the type of product cost (a-c) or designate as not a

product cost (d).

a. direct labor

b. direct materials

c. factory overhead

d. not a product cost

Answer:

Decisions to install new equipment, replace old equipment, and purchase or construct a

new building are examples of

a. sales mix analysis

b. variable cost analysis

c. capital investment analysis

d. variable cost analysis

Answer:

Period costs can be found on both the balance sheet and the income statement.

a. True

b. False

Answer:

O’Boyle Co.’s fixed costs are $256,000, the unit selling price is $36, and the unit

variable costs are $20, what is the break-even sale (units)?

a. 12,800 units

b. 4,571 units

c. 16,000 units

d. 7,111 units

Answer:

A present value index can be used to rank competing capital investment proposals when

the net present value method is used.

a. True

b. False

Answer:

If the profit margin for a division is 11% and the investment turnover is 1.5, the rate of

return on investment is 7.3%.

a. True

b. False

Answer:

Which method of evaluating capital investment proposals uses present value concepts

to compute the rate of return from the net cash flows?

a. internal rate of return method

b. cash payback method

c. net present value method

d. average rate of return method

Answer:

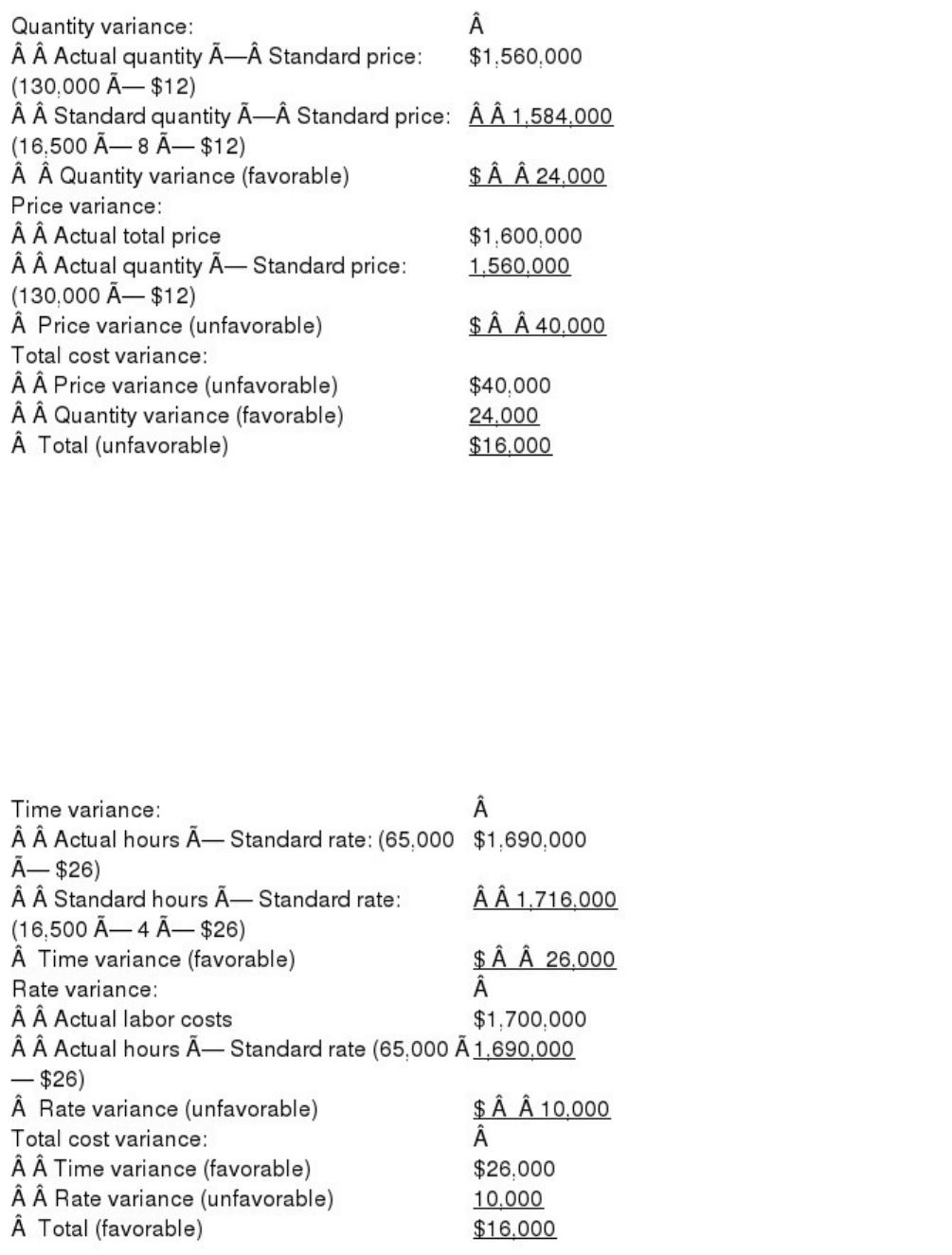

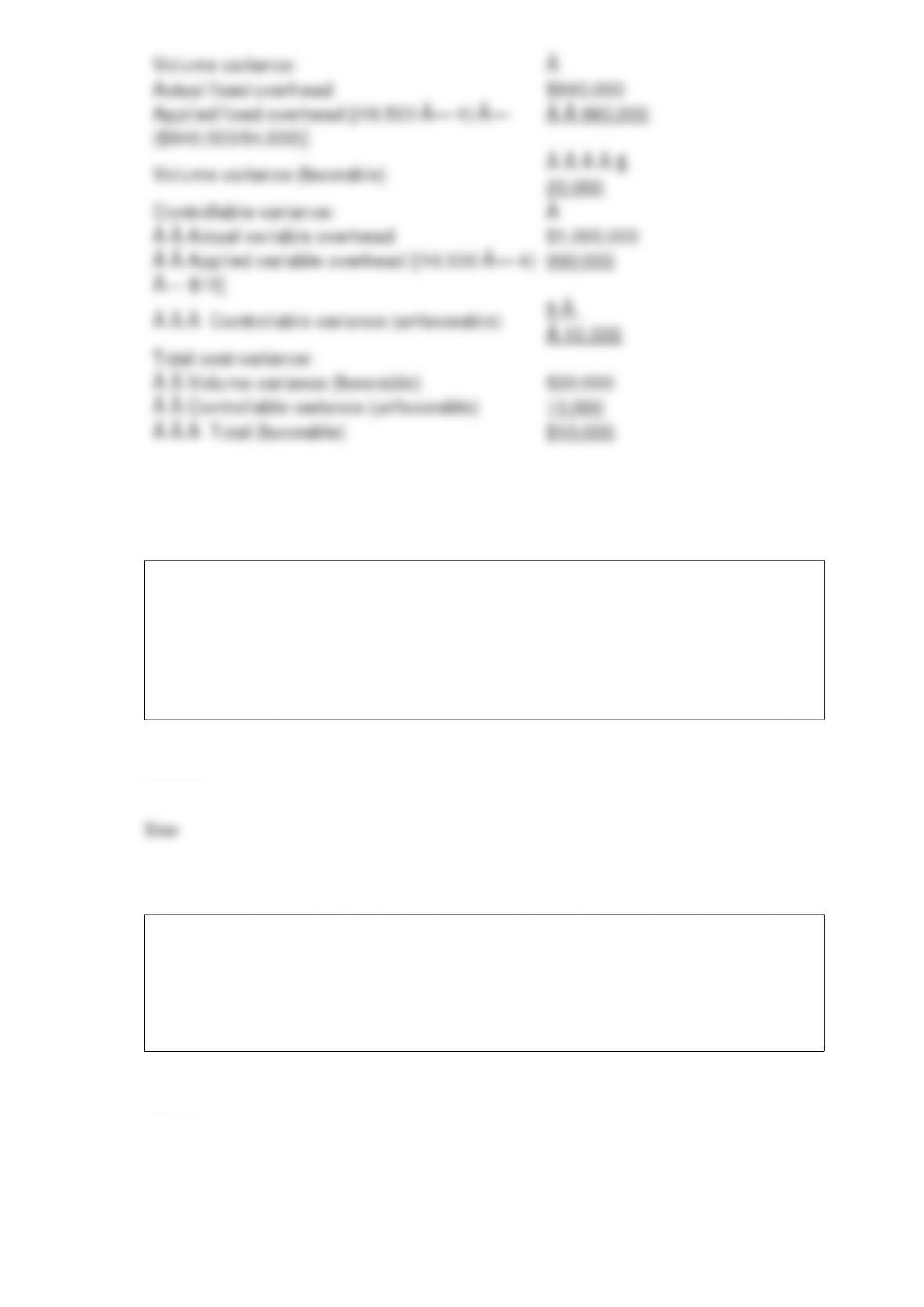

The following information is for the standard and actual costs for the Happy

Corporation:

Standard Costs:

Budgeted units of production – 16,000 [80% (or normal) capacity]

Standard labor hours per unit – 4

Standard labor rate – $26 per hour

Standard material per unit – 8 lbs.

Standard material cost – $12 per pound

Standard variable overhead rate – $15 per labor hour

Budgeted fixed overhead – $640,000

Fixed overhead rate is based on budgeted labor hours at 80% (or normal) capacity.

Actual Cost:

Actual production – 16,500 units

Actual material purchased and used – 130,000 pounds

Actual total material cost – $1,600,000

Actual labor – 65,000 hours

Actual total labor costs – $1,700,000

Actual variable overhead – $1,000,000

Actual fixed overhead – $640,000

Determine: (a) the direct materials quantity variance, price variance, and total cost

variance; (b) the direct labor time variance, rate variance, and total cost variance; and

(c) the factory overhead volume variance, controllable variance, and total factory

overhead cost variance. (Note: If following text formulas, do not round interim

calculations.)

Answer:

A formal written statement of management’s plans for the future, expressed in financial

terms, is called a budget.

a. True

b. False

Answer:

Good Eats Inc. manufactures flatware sets. The budgeted production is for 80,000 sets

this year. Each set requires

2.5 hours to polish the material. If polishing labor costs $15.00 per hour, determine the

direct labor cost budget for polishing for the year.

Answer:

Aquatic Corp.’s standard material requirement to produce one Model 2000 is 15 pounds

of material @ $110.00 per pound. Last month, Aquatic purchased 170,000 pounds of

material at a total cost of $17,850,000. It used 162,000 pounds to produce 10,000 units

of Model 2000.

Calculate the materials price variance and materials quantity variance, and indicate

whether each variance is favorable or unfavorable.

Answer:

An unfinished desk is produced for $36.00 and sold for $65.00. A finished desk can be

sold for $75.00. The additional processing cost to complete the finished desk is $5.95.

Provide a differential analysis for further processing.

Answer:

Tipper Co. is considering a 10-year project that is estimated to cost $700,000 and has

no residual value. Tipper seeks to earn an average rate of return of 15% on all capital

projects. Determine the necessary average annual income (using straight-line

depreciation) that must be achieved on this project for it to be acceptable to Tipper

Company.

Answer:

Describe the flow of materials in a process cost accounting system.

Answer:

The Tough Jeans Company produces two different styles of jeans, Working Life and

Social Life. The company sales budget estimates that 400,000 of the Working Life jeans

and 250,000 of the Social Life jeans will be sold during the year. The company begins

with 9,000 pairs of Working Life and 18,000 pairs of Social Life. The company desires

ending inventory of 7,500 of Working Life and 10,000 Social Life. Prepare a production

budget for the year.

Answer: