The net pension liability (PBO minus plan assets) is decreased by:A. Service cost.

B. Expected return on plan assets.

C. Amortization of net gain-AOCI.

D. Prior service cost.

Answer:

In a postretirement health care plan, prior service cost is attributed to the service of

active employees from the date of the amendment to: A. The partial eligibility date.

B. The retirement date.

C. The full eligibility date.

D. The date of death.

Answer:

Compensating balances represent: A. Funds in a bank account that can’t be spent.

B. Balances in a payroll checking account.

C. Accounts that are subject to bank service charges.

D. Accounts on which banks pay interest, e.g., NOW accounts.

Answer:

Long-term notes receivable issued for noncash assets at an unrealistically low interest

rate will be: A. Discounted at an imputed interest rate.

B. Recorded at the contract amount.

C. Recorded at an amount equal to the future cash flows.

D. Accounted for on the installment basis.

Answer:

Paul Company issues a product recall due to an apparently preexisting and material

defect discovered after the end of its fiscal year. Financial statements have not yet been

issued. The action required of Paul Company for this reasonably estimable contingency

for the year just ended is: A. To disclose it in a note to the financial statements.

B. To accrue a long-term liability.

C. To accrue the liability and explain it in a note to the financial statements.

D. To do nothing relative to the contingency.

Answer:

Listed below are reporting classifications for a statement of cash flows using the

indirect method for reporting operating cash flows. Indicate the reporting classification

that would apply to each of the five transactions described below by placing the letter of

the reporting classification in the space provided by each transaction. 1) Operating

activity, no adjustment to net income

2) Operating activity, positive adjustment to net income

3) Operating activity, negative adjustment to net income

4) Financing cash inflow

5) Investing cash outflow

A. Payment of semi-annual interest on bonds payable

B. Issuance of bonds at a discount for cash

C. Acquisition of a building for cash

D. Decrease in account payable

E. Depreciation expense

Answer:

All of the following but one represent collections for third parties. Which one of the

following is not a collection for a third party? A. Sales tax payable.

B. Customer deposits.

C. Employee insurance deductions.

D. Social security taxes deductions.

Answer:

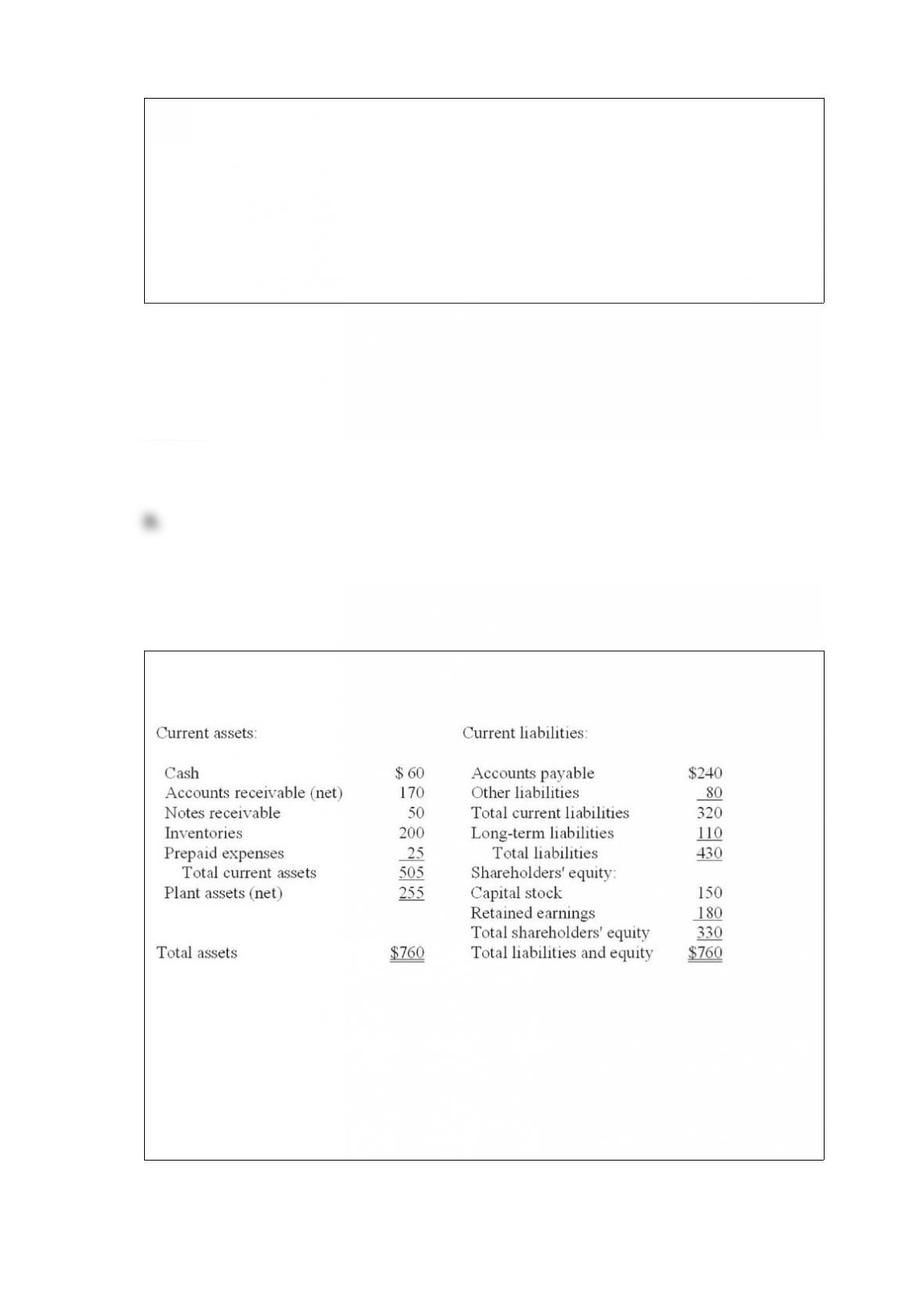

The following partial balance sheet ($ in thousands) for Paisano Seafood Inc. is shown

below.

Quick assets total: A. $60.

B. $230.

C. $280.

D. $305.

Answer:

An exception that is so serious that even a qualified opinion is not justified would result

in: A. A disclaimer.

B. An unqualified opinion.

C. An adverse opinion.

D. A consistency exception.

Answer:

When a property dividend is declared, the reduction in retained earnings is for: A. The

book value of the property on the date of declaration.

B. The book value of the property on the date of distribution.

C. The fair value of the property on the date of distribution.

D. The fair value of the property on the date of declaration.

Answer:

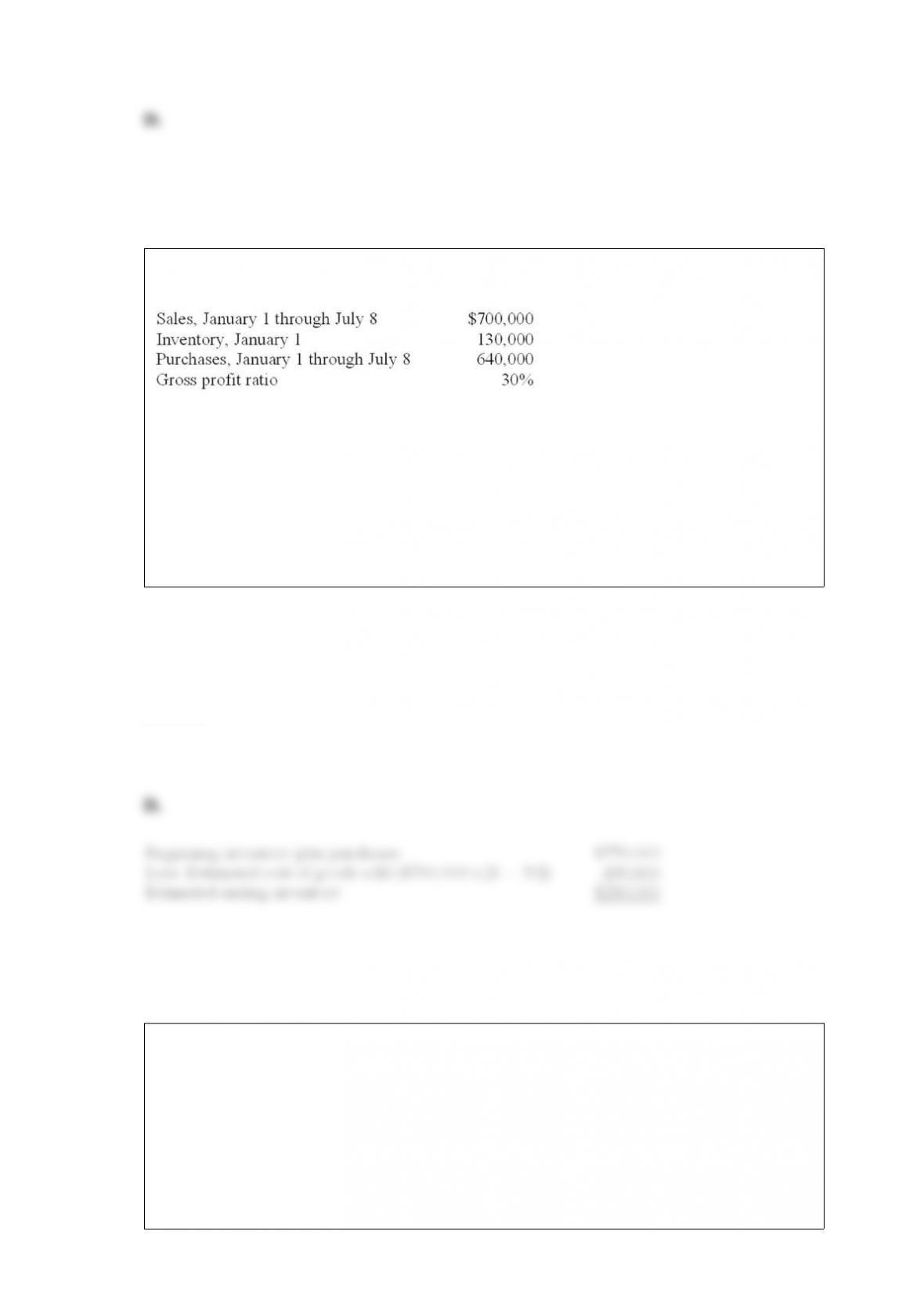

On July 8, a fire destroyed the entire merchandise inventory on hand of Larrenaga

Wholesale Corporation. The following information is available:

What is the estimated inventory on July 8 immediately prior to the fire? A. $192,000.

B. $490,000.

C. $510,000.

D. $280,000.

Answer:

The difference between single-step and multiple-step income statements is primarily an

issue of: A. Consistency.

B. Presentation.

C. Measurement.

D. Valuation.

Answer:

How many acceptable approaches are there for changes in accounting principles? A.

One.

B. Two.

C. Three.

D. Four.

Answer:

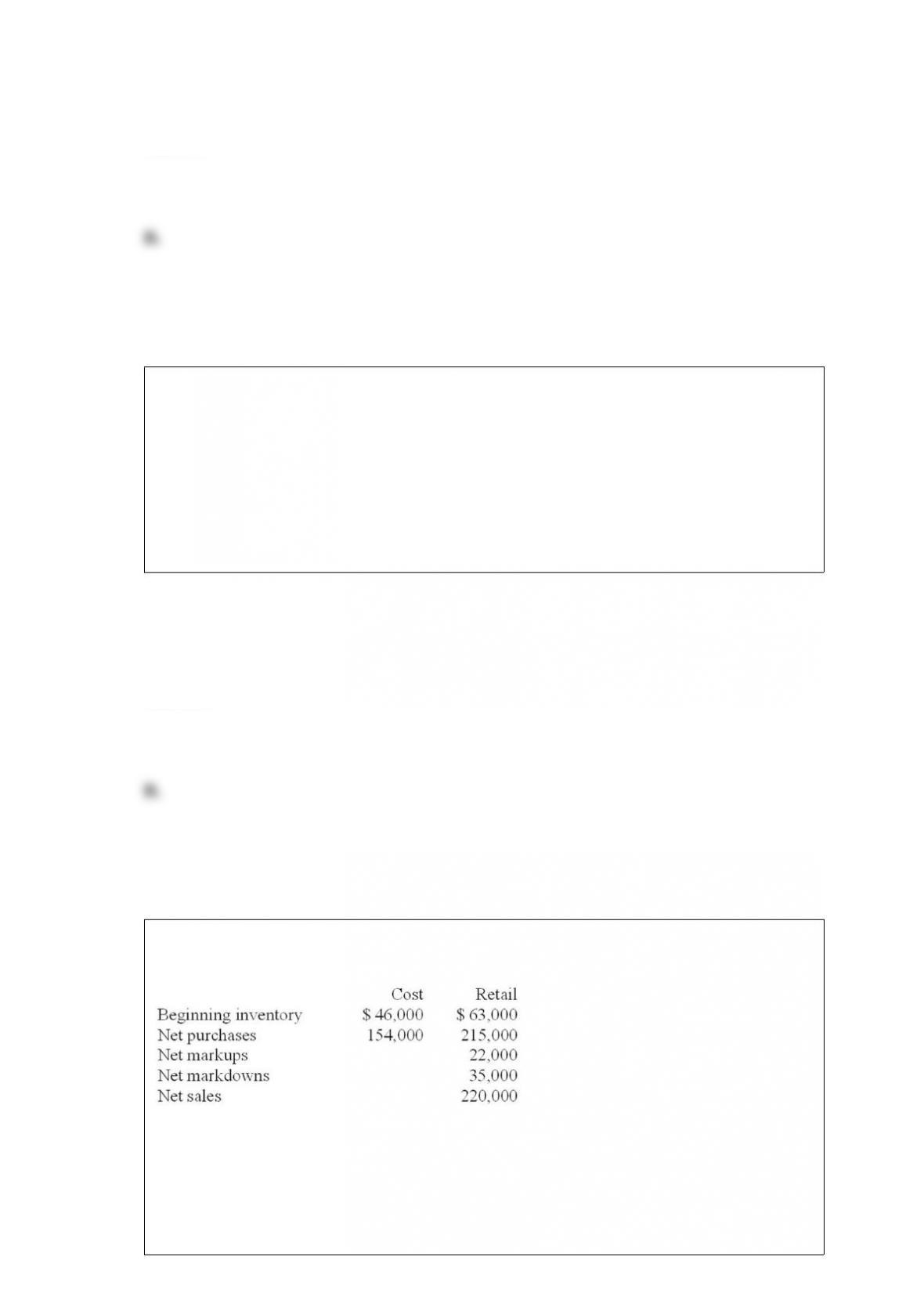

Willie Nelson’s Boots uses the conventional retail method to estimate ending inventory.

Cost data for the most recent quarter is shown below:

To the nearest thousand, estimated ending inventory using the conventional retail

method is: A. $37,000.

B. $32,000.

C. $34,000.

D. $30,000.

Answer:

According to International Financial Reporting Standards, the revaluation of equipment

when fair value exceeds book value, results in: A. An increase in net income.

B. A decrease in net income.

C. An increase in other comprehensive income.

D. A decrease in other comprehensive income.

Answer:

The postretirement benefit obligation is the: A. Future value of the estimated benefits

during retirement.

B. Present value of the estimated benefits during retirement.

C. Fair value of the estimated benefits during retirement.

D. Actual value of estimated benefits during retirement.

Answer:

JFS Co. changed from straight-line to DDB depreciation. The journal entry to record

the change includes: A. A credit to accumulated depreciation.

B. A debit to accumulated depreciation.

C. A debit to a depreciable asset.

D. The change does not require a journal entry.

Answer:

Summary data for Benedict Construction Co.’s (BCC) Job 1227, which was completed

in 2013, are presented below:

Assuming BCC uses the percentage-of-completion method of revenue recognition, the

gross profit recognized in 2012 would be (rounded to the nearest thousand): A. $33,000.

B. $36,000.

C. $69,000.

D. $30,000.

Answer:

The conventional retail inventory method is based on: A. Average cost.

B. LIFO cost.

C. Average, lower of cost or market.

D. LIFO, lower of cost or market.

Answer:

When treasury stock is purchased for an amount greater than its par value, what is the

effect on total shareholders’ equity? A. Increase.

B. Decrease.

C. No effect.

D. Cannot tell from the given information.

Answer:

Funzy Cereal includes one coupon in each package of Wheatos that it sells and offers a

toy car in exchange for $1.00 and three coupons. The cars cost Funzy $1.50 each.

Experience indicates that 40% of the coupons eventually will be redeemed. During the

last month of 2013, the first month of the offer, Funzy sold 12 million boxes of Wheatos

and 2.4 million of the coupons were redeemed. What amount should Funzy report as a

promotional expense for coupons on its December 31, 2013, income statement? A. $0.

B. $400,000.

C. $800,000.

D. $1,200,000.

Answer:

A company has cumulative preferred stock. When computing earnings per share, the

current year’s dividends not declared on the preferred stock should be: A. Deducted

from earnings for the year.

B. Deducted, net of tax effect, from earnings for the year.

C. Added to earnings for the year.

D. Ignored.

Answer:

Eagle Company issued 10-year bonds at 96 during the current year. In the year-end

financial statements, the discount should be: A. Deducted from bonds payable.

B. Added to bonds payable.

C. Included as an expense in the year of issue.

D. Reported as a deferred charge.

Answer:

Archie Co. purchased a framing machine for $45,000 on January 1, 2013. The machine

is expected to have a four-year life, with a residual value of $5,000 at the end of four

years.

Using the double-declining balance method, depreciation for 2013 and book value at

December 31, 2013, would be: A. $22,500 and $22,500.

B. $22,500 and $17,500.

C. $20,000 and $25,000.

D. $20,000 and $20,000.

Answer:

The Hamada Company sales for 2013 totaled $150,000 and purchases totaled $95,000.

Selected January 1, 2013, balances were: accounts receivable, $18,000; inventory,

$14,000; and accounts payable, $12,000. December 31, 2013, balances were: accounts

receivable, $16,000; inventory, $15,000; and accounts payable, $13,000. Net cash flows

from these activities were: A. $45,000.

B. $55,000.

C. $58,000.

D. $74,000.

Answer:

Charlene Company sold a printer with a cost of $68,000 and accumulated depreciation

of $23,000 for $20,000 cash. This transaction would be reported as: A. An operating

activity.

B. An investing activity.

C. A financing activity.

D. None of the above is correct.

Answer:

Montgomery & Co., a well-established law firm, provided 500 hours of its time to Fink

Corporation in exchange for 1,000 shares of Fink’s $5 par common stock.

Montgomery’s usual billing rate is $700 per hour, and Fink’s stock has a book value of

$250 per share. By what amount will Fink’s paid-in capitalexcess of par increase for this

transaction? A. $345,000.

B. $295,000.

C. $350,000.

D. $300,000.

Answer:

Cash equivalents have each of the following characteristics except: A. Little risk of loss.

B. Highly liquid.

C. Maturity of at least three months.

D. Short-term.

Answer:

Shively Mfg. Co. sold for $18,000 equipment that cost $40,000 and had a book value of

$30,000. Shively would report: A. Operating cash inflows of $18,000.

B. Operating cash inflows of $8,000.

C. Financing cash inflows of $18,000.

D. Investing cash inflows of $18,000.

Answer:

Nontrade receivables do not include: A. Sales to customers.

B. Loans to employees.

C. Income tax refund receivable.

D. Advances to affiliated companies.

Answer:

If a stock split occurred, when calculating the current year’s EPS, the shares are treated

as issued: A. At the end of the year.

B. On the first day of the next fiscal year.

C. At the beginning of the year.

D. On the date of distribution.

Answer:

Which of the following is considered a sale of receivables? A. Pledging receivables.

B. Assigning receivables.

C. Factoring receivables without recourse.

D. None of the above.

Answer:

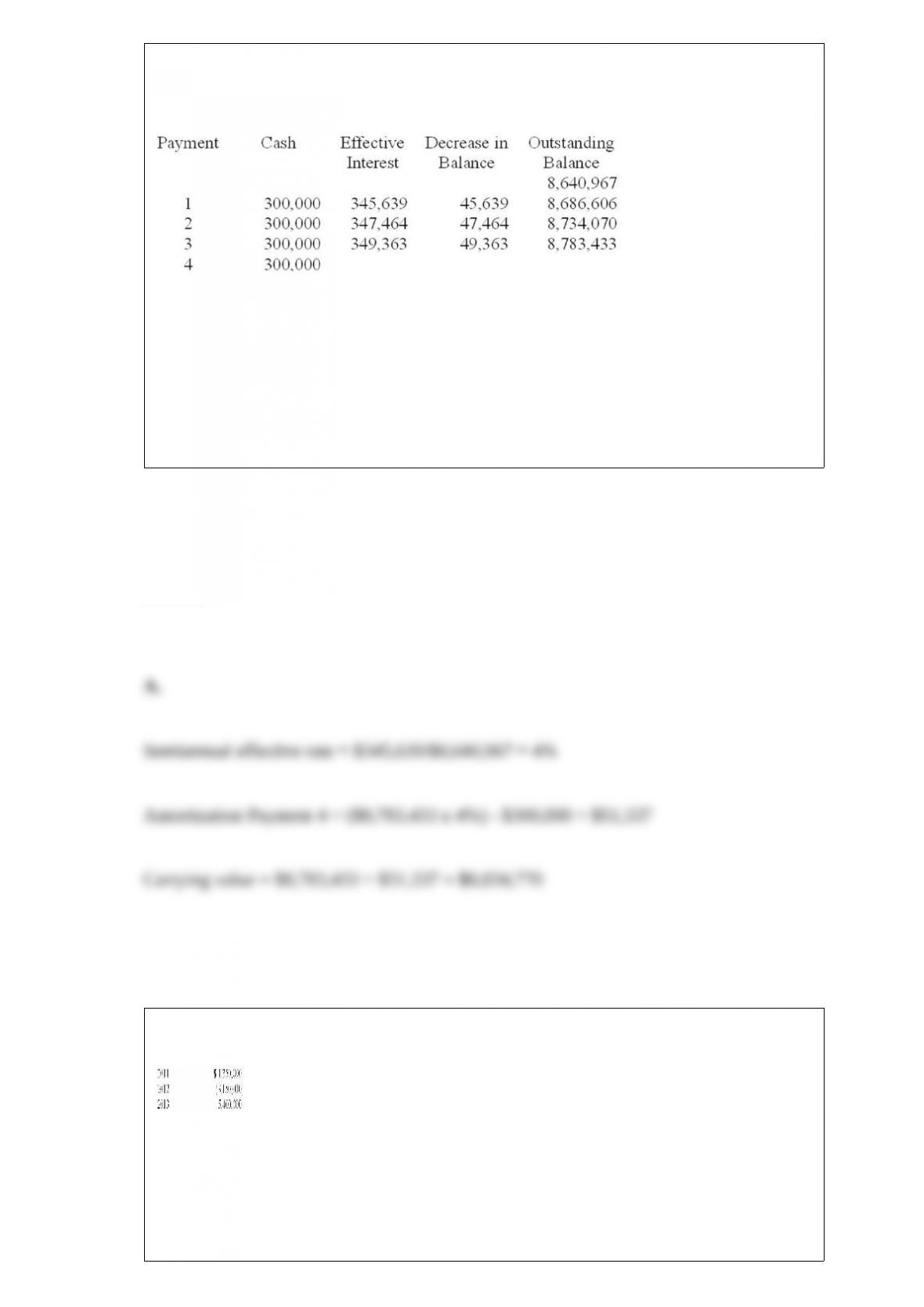

Discount-Mart issued ten thousand $1,000 bonds on January 1, 2013. The bonds have a

10-year term and pay interest semiannually. This is the partial bond amortization

schedule for the bonds.

What is the carrying value of the bonds as of December 31, 2014? A. $8,834,770.

B. $8,686,606.

C. $8,734,070.

D. $8,783,433.

Answer:

In its first three years of operations Sharp Chairs reported the following operating

income (loss) amounts:

There were no deferred income taxes in any year. In 2012, Sharp elected to carry back

its operating loss. The enacted income tax rate was 35% in 2011 and 40% thereafter. In

its 2013 balance sheet, what amount should Sharp report as current income tax payable?

A. $900,000.

B. $1,260,000.

C. $1,440,000.

D. $2,160,000.

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1)Dollar-value LIFO retail

method

2)Markdown

3)NRV

4)Change to LIFO from FIFO

5)Disposal costs

•Usually impossible to calculate the effect on prior years’ financial statements

•Requires base year retail to be converted to layer year retail and then to cost

•Reduction in selling price

•Deducted from selling price when calculating ceiling

•Upper limit or ceiling in LCM approach

•

Answer:

Bernard Corporation has an unfunded postretirement health care benefit plan. Life

insurance and medical care benefits are provided to employees who render 12 years of

service and attain age 55 while in service to the company. At the end of 2013, Teri Clark

is 35. She was hired by Bernard five years ago at age 30 and is expected to retire at the

age of 62. The expected postretirement benefit obligation for Teri is $50,000 at the end

of 2013 and $60,000 at the end of

Required:

Calculate the accumulated postretirement benefit obligation at the end of 2013 and

2014 and the service cost for 2013 and 2014 pertaining to Teri.

Answer:

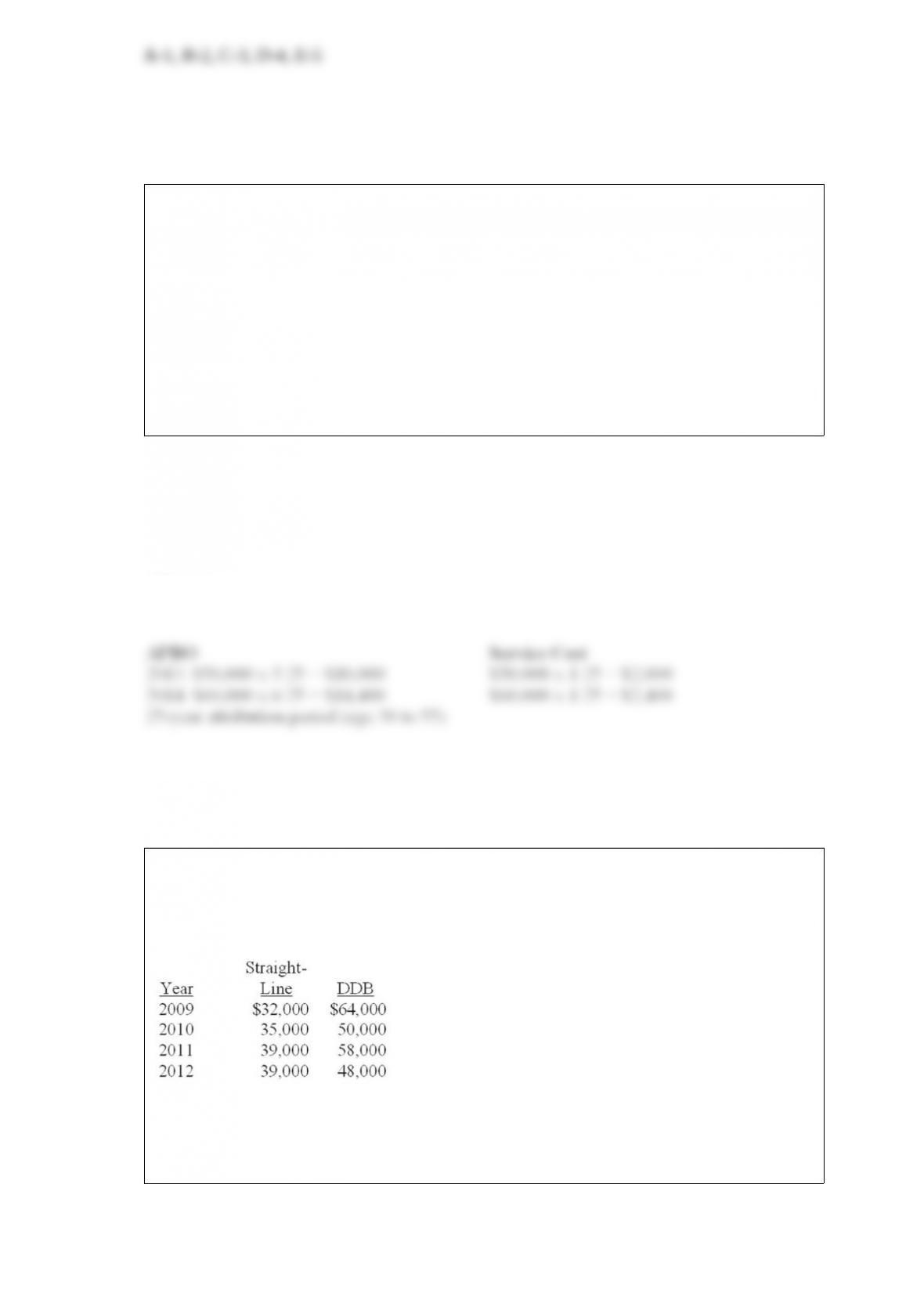

Gonzaga Company has used the double-declining-balance method for depreciation

since it started business in 2009. At the beginning of 2013, the company decided to

change to the straight-line method. Depreciation as reported and what it would have

been reported if the company had always used straight-line is listed below:

Required:

What journal entry, if any, should Gonzaga make to record the effect of the accounting

change (ignore income taxes)? Explain.

Answer:

Discuss the following questions.

Required:

What securities must be classified within one of the three categories of held to maturity,

available for sale, and trading? (Do not describe how to determine how securities are

classified among these three categories.) Identify the four primary recording activities

related to investments in securities.

Answer:

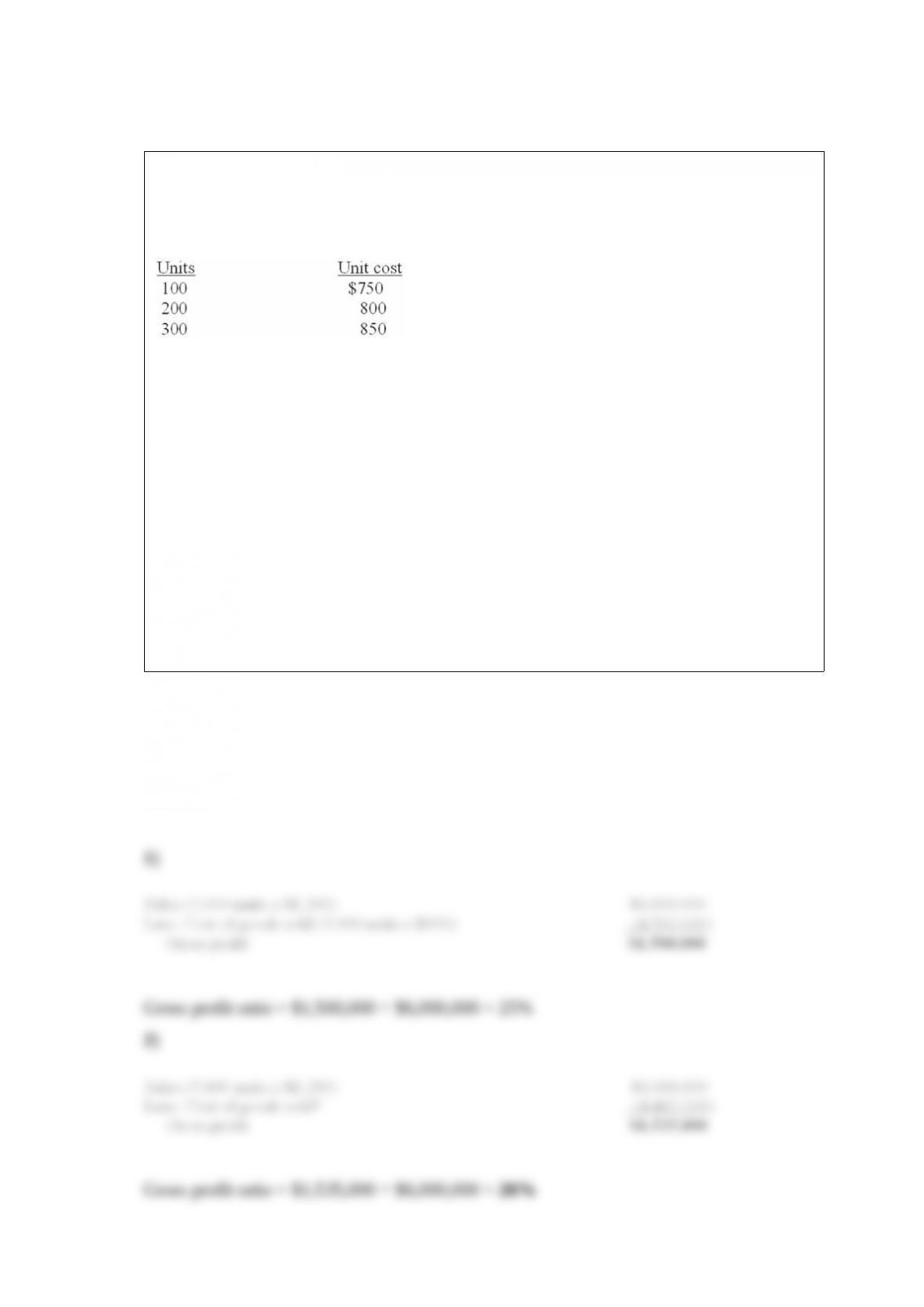

Modern Day Appliances, Inc. is a wholesaler of kitchen appliances. The company uses

a periodic inventory system and the LIFO cost method. Modern Day’s December 31,

2013, fiscal year-end inventory of its main product, double-door stainless steel

refrigerators, consisted of the following (listed in chronological order of acquisition):

The replacement cost of the refrigerators throughout 2014 was $900. Modern Day sold

5,000 of these refrigerators during 2014. The company’s selling price throughout 2014

was $1,200.

Required:

1) Compute the gross profit (sales minus cost of goods sold) and the gross profit ratio

for 2014 assuming that Modern Day purchased 5,200 units during the year.

2) Repeat requirement 1 assuming that Modern Day purchased only 4,500 units.

3) For requirements 1 and 2, what amount of before-tax LIFO liquidation profit or loss

would Modern Day report in its 2014 disclosure notes, if any, assuming any calculated

amount is material?

Answer:

On December 31, 2012, Heffner Company had 100,000 shares of common stock

outstanding and 30,000 shares of 7%, $100 par, cumulative preferred stock outstanding.

On February 28, 2013, Heffner purchased 24,000 shares of common stock on the open

market as treasury stock paying $45 per share. Heffner sold 6,000 of the treasury shares

on September 30, 2013, for $47 per share. Net income for 2013 was $540,000. The

income tax rate is 40%. Also outstanding at December 31, 2012, were fully vested

incentive stock options giving key personnel the option to buy 50,000 common shares

at $40. The market price of the common shares averaged $50 during 2013. Five

thousand 6% bonds were issued at par on January 1, 2013. Each $1,000 bond is

convertible into 125 shares of common stock. None of the bonds had been converted by

December 31, 2013, and no stock options were exercised during the year.

Required:

Compute basic and diluted earnings per share (rounded to 2 decimal places) for Heffner

Company for 2013.

Answer:

McCombs Contractors received a contract to construct a mental health facility for

$2,500,000. Construction was begun in 2012 and completed in 2013. Cost and other

data are presented below:

Assume that McCombs uses the completed contract method for revenue recognition.

Required: Compute the amount of gross profit recognized by McCombs during 2012

and 2013.

Answer:

Missoula Inc. reported the following selected financial statement data:

Required: Compute the profit margin on sales for 2013.

Answer:

Paul Company had 100,000 shares of common stock outstanding on January 1, On

September 30, 2013, Paul sold 48,000 shares of common stock for cash. Paul also had

10,000 shares of convertible preferred stock outstanding throughout 2013. The

preferred stock is $100 par, 6%, and is convertible into 3 shares of common for each

share of preferred. Paul also had 500, 8%, convertible bonds outstanding throughout

2013. Each $1,000 bond is convertible into 30 shares of common stock. The bonds sold

originally at face value. Reported net income for 2013 was $300,000 with a 40% tax

rate. Common shareholders received $2 per share dividends after preferred dividends

were paid in

Required:

Compute basic and diluted earnings per share (rounded to 2 decimal places) for 2013.

Answer:

•Synthetic Fuels Corporation prepares its financial statements according to IFRS.

On June 30, 2013, the company purchased equipment for $350,000. The equipment

is expected to have a seven-year useful life with no residual value. Synthetic uses

the straight-line depreciation method for all depreciable assets. On December 31,

2013, the end of the company’s fiscal year, Synthetic chooses to revalue the

machinery to its fair value of $299,000.

Required:

1) Calculate depreciation for 2013.

2) Prepare the journal entry at the end of 2013 to record the revaluation of the

equipment.

3) Calculate depreciation for 2014.

4) Repeat requirement 2 assuming that the fair value of the equipment at the end of

2013 is $338,000.

Answer:

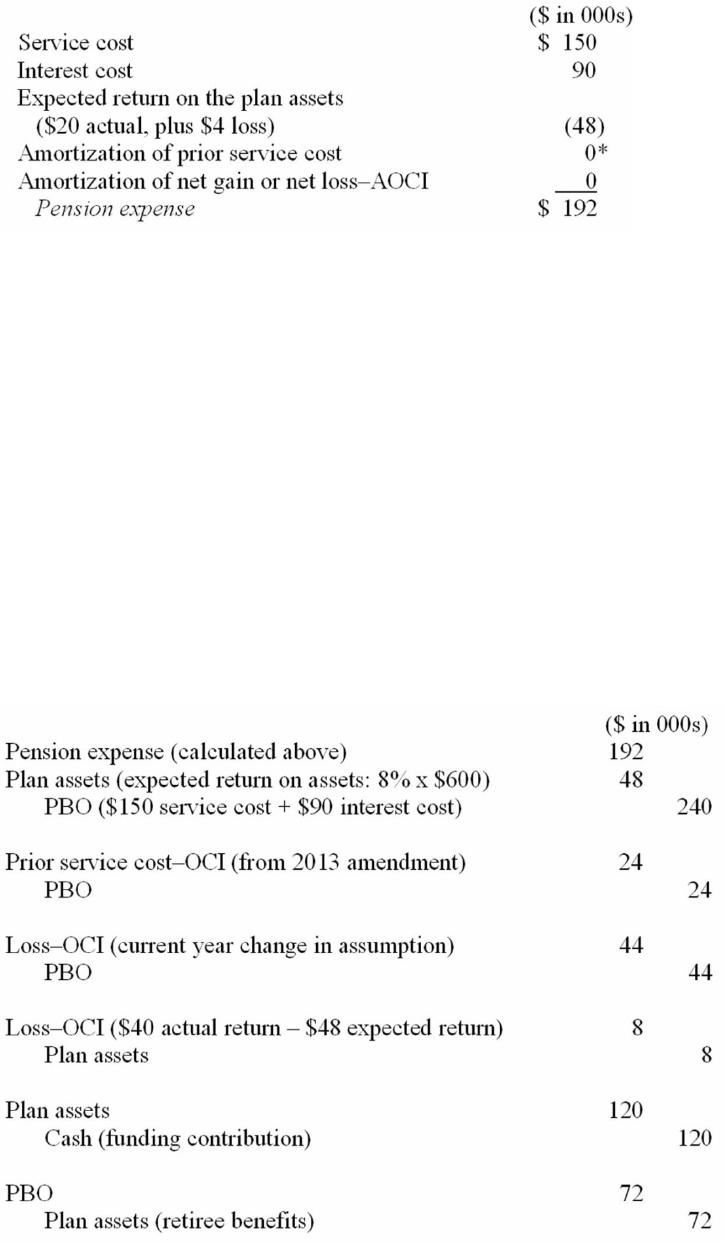

Dharma Initiative, Inc., has a defined benefit pension plan. Characteristics of the plan

during 2013 are as follows:

The expected long-term rate of return on plan assets was 8%. There were no AOCI

balances related to pensions on January 1, 2013, but at the end of 2013, the company

amended the pension formula creating a prior service cost of $24 million.

Required:

1) Calculate the pension expense for 2013.

2) Prepare the journal entry to record pension expense, gains or losses, past service cost,

funding, and payment of benefits for 2013.

3) What amount will Dharma Initiative report in its 2013 balance sheet as a net pension

asset or net pension liability?

Answer:

You are reviewing O’Brian Co.’s adjusted trial balance for the year ended 12/31/13. You

notice several omissions and incorrect items during your review, some of which are

noted below. For each one, you are to determine what effect, if any, these items would

have on the stated components of O’Brian Co.’s 2013 Income Statement and 12/31/13

Balance Sheet if they are not corrected or updated. Assume no income taxes.

Use the following code for your answers. You need not include any dollar amounts.

N = No Effect

O = Overstated

U = Understated

Answer:

Elf Leasing purchased a machine for $500,000 and leased it to IGA, Inc., on January 1,

2013.

Collectibility of the rental payments is reasonably assured, and there are no lessor costs

yet to be incurred.

Required:

Prepare appropriate entries for both IGA and Elf Leasing from the inception of the lease

through the second rental payment on April 1, 2013. Depreciation is recorded at the end

of each fiscal year (December 31).

Answer:

The gross profit method and retail method are both ways of estimating ending

inventory. Briefly explain how the two methods differ.

Answer:

Describe the use of depreciation for an asset leased under a capital lease. Include a

discussion of the depreciation period.

Answer:

In 2013, the internal auditors of KJI Manufacturing discovered the following material

errors made in prior years:

1. Equipment was purchased on June 30, 2011, for $100,000. The purchase was

incorrectly recorded as a debit to repair and maintenance expense. The equipment has a

useful life of five years and no residual value.

2. On March 31, 2012, $50,000 was paid to a contractor to landscape the area around a

manufacturing plant including the installation of a sprinkler system. The expenditure

was debited to the Land account. The landscaping is expected to have a 20-year useful

life and no residual value.

KJI uses the straight-line method of depreciation for all depreciable assets.

Required:

1. Prepare the journal entries at December 31, 2013, to correct the errors (ignore income

taxes).

2. Prepare the journal entries to record 2013 depreciation for any assets recorded in

requirement 1.

Answer: