1) Paglia Corporation owns 80% of Aburn Corporation and has separate net income of

$200,000 for 2010 . Aburn Corporation has separate net income of $100,000 and owns

70% of the outstanding stock of Badley Corporation. Badley Corporation has separate

net income of $80,000. (Separate net incomes exclude investment income.) The cost of

each investment was equal to book value and fair value. The controlling interest share

of consolidated net income for 2010 is

A) $324,800

B) $328,800

C) $344,800

D) $344,800

2) Pied Imperial Corporation acquired a 90% interest in Somest Corporation in 2009

when Somest’s book values were equivalent to fair values. Somest sold equipment with

a book value of $80,000 to Pied for $130,000 on January 1, 2011 . Pied is fully

depreciating the equipment over a 4-year period by using the straight-line method.

Somest reported net income for 2011 was $320,000. Pied’s 2011 income from Somest

was

A) $249,250

B) $250,500

C) $254,250

D) $288,000

3) An increase in the riskiness of corporate bonds will ________ the yield on corporate

bonds and ________ the yield on Treasury securities, everything else held constant

A) increase; increase

B) reduce; reduce

C) increase; reduce

D) reduce; increase

4) Corporate bonds are not as liquid as government bonds because

A) fewer corporate bonds for any one corporation are traded, making them more costly

to sell

B) the corporate bond rating must be calculated each time they are traded

C) corporate bonds are not callable

D) corporate bonds cannot be resold

5) If the expected path of one-year interest rates over the next five years is 4 percent, 5

percent, 7 percent, 8 percent, and 6 percent, then the expectations theory predicts that

today’s interest rate on the five-year bond is

A) 4 percent

B) 5 percent

C) 6 percent

D) 7 percent

6) Which pronouncements have the highest level of authority for state and local

governments?

A) Financial Accounting Standards Board Statements

B) GASB Statements

C) Consensus Positions of GASB Emerging Issues Task Force

D) GASB Technical Bulletins

7) Plenty Corporation issued six thousand, $1,000 par, 6% bonds on January 1, 2010, at

par. Interest is paid on January 1 and July 1 of each year; the bonds mature on January

1, 2015 . On January 2, 2012, Scrawn Corporation, a 75%-owned subsidiary of Plenty,

purchased 3,000 of the bonds on the open market at 102.50 . Plenty’s separate net

income for 2012 included the annual interest expense for all 3,000 bonds. Scrawn’s

separate net income for 2012 was $400,000, which included the bond interest received

on July 1 as well as the accrual of bond interest revenue earned on December 31 . Both

companies use straight-line amortization of bond discounts/premiums.

Using the original information, the balances for the Bonds Payable and Bond Interest

Payable accounts, respectively, on the consolidated balance sheet for December 31,

2013 were

A) $3,000,000 and $ 90,000

B) $3,000,000 and $180,000

C) $6,000,000 and $ 90,000

D) $6,000,000 and $180,000

8) Gains or losses on foreign currency transactions are recorded before the related

receivable or payable is settled when

A) the government cannot set an exchange rate for the foreign currency

B) the foreign currency is unknown

C) the fiscal year ends after the settlement of the receivable or payable

D) the fiscal year ends before the settlement of the receivable or payable

9) The spread between the interest rates on bonds with default risk and default-free

bonds is called the

A) risk premium

B) junk margin

C) bond margin

D) default premium

10) What method of accounting will generally be used when one company purchases

between 20% to 50% of the outstanding stock of another company?

A) Only the fair value method may be used

B) Only the equity method may be used

C) Either the fair value method or the equity method may be used, depending upon the

relationship between the companies

D) Neither the fair value method nor the equity method may be used, regardless of the

level of ownership

11) For an operating segment to be considered a reporting segment under the revenue

threshold, its reported revenue must be 10% or more of

A) the combined enterprise revenues, eliminating all relevant intracompany transfers

and balances

B) the combined revenues, excluding intersegment revenues, of all operating segments

C) the combined revenues, including intersegment revenues, of all operating segments

D) the consolidated revenue of all operating segments

12) Paggle Corporation owns 80% of Spillway Inc.’s common stock that was purchased

at its underlying book value. At the time of purchase, the book value and fair value of

Spillway’s net assets were equal. The two companies report the following information

for 2011 and 2012 .

During 2011, one company sold inventory to the other company for $50,000 which cost

the transferor $40,000. As of the end of 2011, 30% of the inventory was unsold. In

2012, the remaining inventory was resold outside the consolidated entity.

2011 Selected Data:PaggleSpillway

Sales Revenue $600,000 $320,000

Cost of Goods Sold320,000155,000

Other Expenses100,00089,000

Net Income $180,000 $76,000

Dividends Paid19,0000

2012 Selected Data:PaggleSpillway

Sales Revenue$580,000 $445,000

Cost of Goods Sold300,000180,000

Other Expenses130,000171,000

Net Income$150,000 $94,000

Dividends Paid16,0005,000

If the sale referred to above was a downstream sale, the total sales revenue reported in

the consolidated income statement for 2011 would be

A) $870,000

B) $880,000

C) $920,000

D) $970,000

13) Pew Corporation acquired 80% ownership of Sordid Incorporated, at a time when

Pew’s investment cost was equal to 80% of Sordid’s book value. At the time of

acquisition, the book values and fair values of Sordid’s assets and liabilities were equal.

Pew uses the equity method. During 2011, Pew sold goods to Sordid for $160,000

making a gross profit percentage of 20%. Half of these goods remained unsold in

Sordid’s inventory at the end of the year. Income statement information for Pew and

Sordid for 2011 were as follows:

Pew Sordid

Sales Revenue$800,000 $300,000

Cost of Goods Sold500,000160,000

Operating Expenses200,00080,000

Separate incomes$100,000$60,000

What is Pew’s income from Sordid for 2011?

A) $32,000

B) $48,000

C) $60,000

D) $75,000

14) Packer Corporation owns 100% of Abel Corporation, Abel Corporation owns 95%

of Bacon Corporation and Bacon Corporation owns 80% of Cab Corporation. The

separate net incomes (excluding investment income) of Packer, Abel, Bacon, and Cab

are $300,000, $100,000, $200,000, and $300,000, respectively. All of the investments

were made at times when the investee’s book values were equal to their fair values.

There were no cost/book value differentials for each investment.

Required:

Determine the controlling interest share of consolidated net income and noncontrolling

interest shares for Packer Corporation and Subsidiaries for the current year.

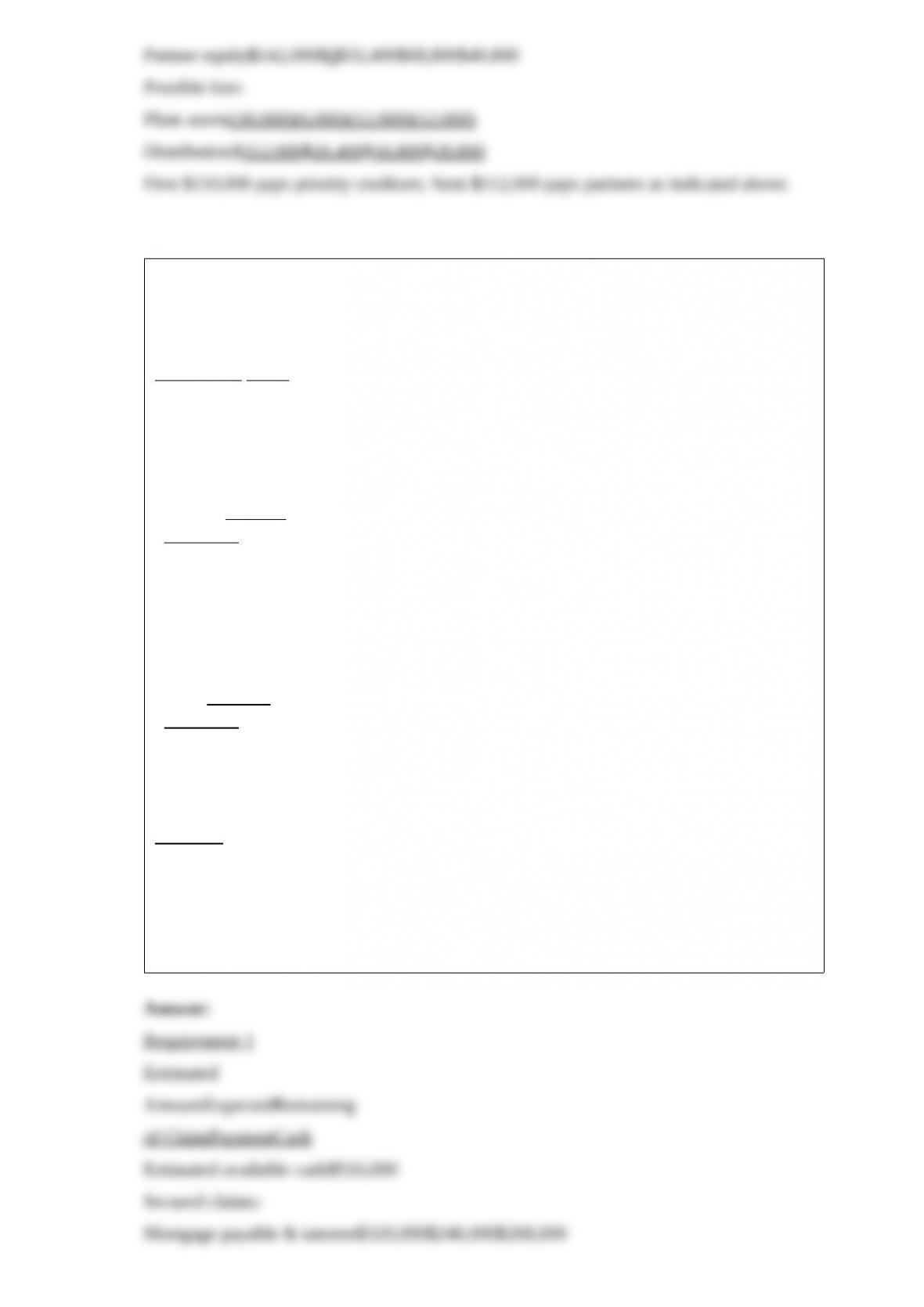

15) A cash distribution plan for the Jonah, Krispy, and Lemon partnership was as

follows:

Priority

CreditorsJonahKrispyLemon

First $100,000100%

Next $180,00044%10%46%

Next $270,0002/91/92/3

Remainder11%44%45%

Required:

If $700,000 of cash was distributed by the partnership, how much was received

respectively by the priority creditors, Jonah, Krispy, and Lemon?

16) Salli Corporation regularly purchases merchandise from their 90%-owner, Playtime

Corporation. Playtime purchased the 90% interest at a cost equal to 90% of the book

value of Salli’s net assets. At the time of acquisition, the book values and fair values of

Salli’s assets and liabilities were equal. Playtime makes their sales to Salli at 120% of

cost. In 2012, Salli reported net income of $460,000, and made purchases totaling

$172,000 from Playtime. Although Salli had no inventory on hand at the beginning of

2012 that they had purchased from Playtime, at year end, they had $51,600 of this

merchandise in inventory.

Required:

1>Determine the unrealized profit in Salli’s inventory at December 31, 2012 .

2>Compute Playtime’s income from Salli for 2012 .

17) The balance sheet of the Park, Quid, and Reggie partnership on November 1, 2011

(before commencement of partnership liquidation) was as follows:

Cash$60,000Accounts payable$110,000

Accounts Receivable130,000Loan from Quid40,000

Loan to Park16,000Park, capital (20%)60,000

Loan to Reggie22,000Quid, capital (40%)52,000

Plant assets-net120,000Reggie, capital (40%)86,000

Total assets$348,000Total liab./equity$348,000

Liquidation events in November were as follows:

– All receivables were settled for $110,000;

– Plant assets with a book value of $90,000 were sold for $52,000.

Required:

Determine how the available cash on November 31, 2011 should be distributed.

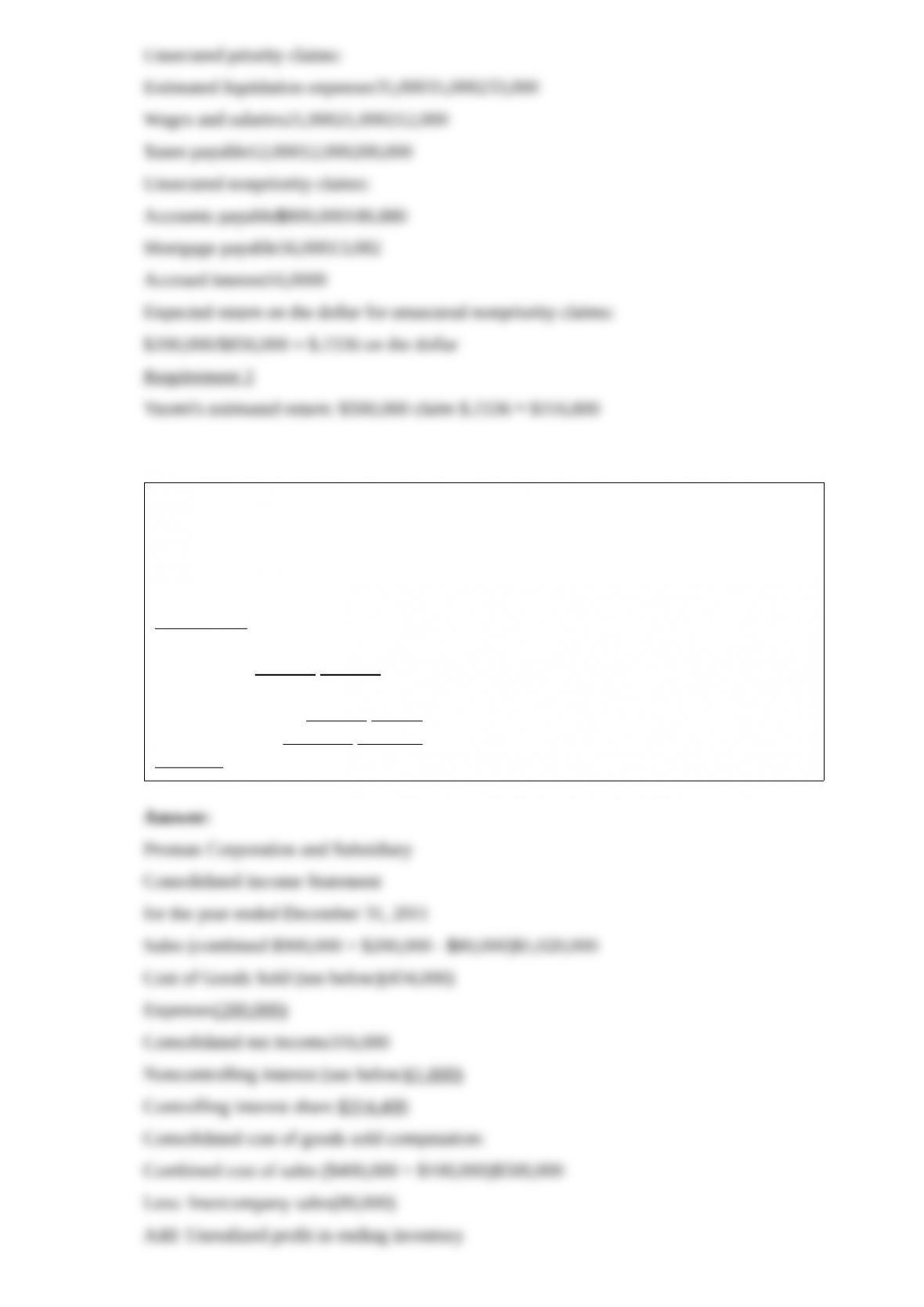

18) Pasten Corporation is liquidating under Chapter 7 of the Bankruptcy Act. The

accounts of Pasten at the time of filing are summarized as follows:

Estimated

Realizable

Book Value Value

Cash$65,000$65,000

Accounts receivable-net15,00013,000

Inventory280,000190,000

Land20,00028,000

Building210,000220,000

Goodwill595,0000

$1,185,000

Accounts payable$800,000

Wages and salaries21,000

Taxes payable12,000

Accrued mortgage interest payable16,000

Mortgage payable304,000

Capital stock100,000

Deficit(68,000)

$1,185,000

The land and building are pledged as security for the mortgage payable as well as any

accrued interest on the mortgage. Wages and salaries were earned within 90 days of

filing the bankruptcy petition and do not exceed $10,000 per employee. Liquidation

expenses are expected to be $35,000.

Required:

1>Prepare a schedule showing the priority rankings of the creditors and the expected

payouts.

2>Yuomi Corporation was a supplier to Pasten Corporation and at the time of Pasten’s

bankruptcy filing, Yuomi’s account receivable from Pasten was $500,000. On the basis

of the estimates, how much can Yuomi expect to receive?

19) Proman Manufacturing owns a 90% interest in Sipp Company, purchased at a time

when the book values of Sipp’s recorded assets and liabilities were equal to fair values.

During 2011, Sipp sold merchandise to Proman for $80,000 at a 20% gross profit. At

December 31, 2011, 25% of this merchandise is still in Proman’s inventory. Separate

incomes for Proman and Sipp are summarized as follows:

PromanSipp

Sales$900,000$200,000

Cost of sales 400,000 100,000

Gross profit 500,000 100,000

Operating expenses 200,000 80,000

Separate income $300,000 $ 20,000

Required: Prepare a consolidated income statement for 2011 for Proman and subsidiary.

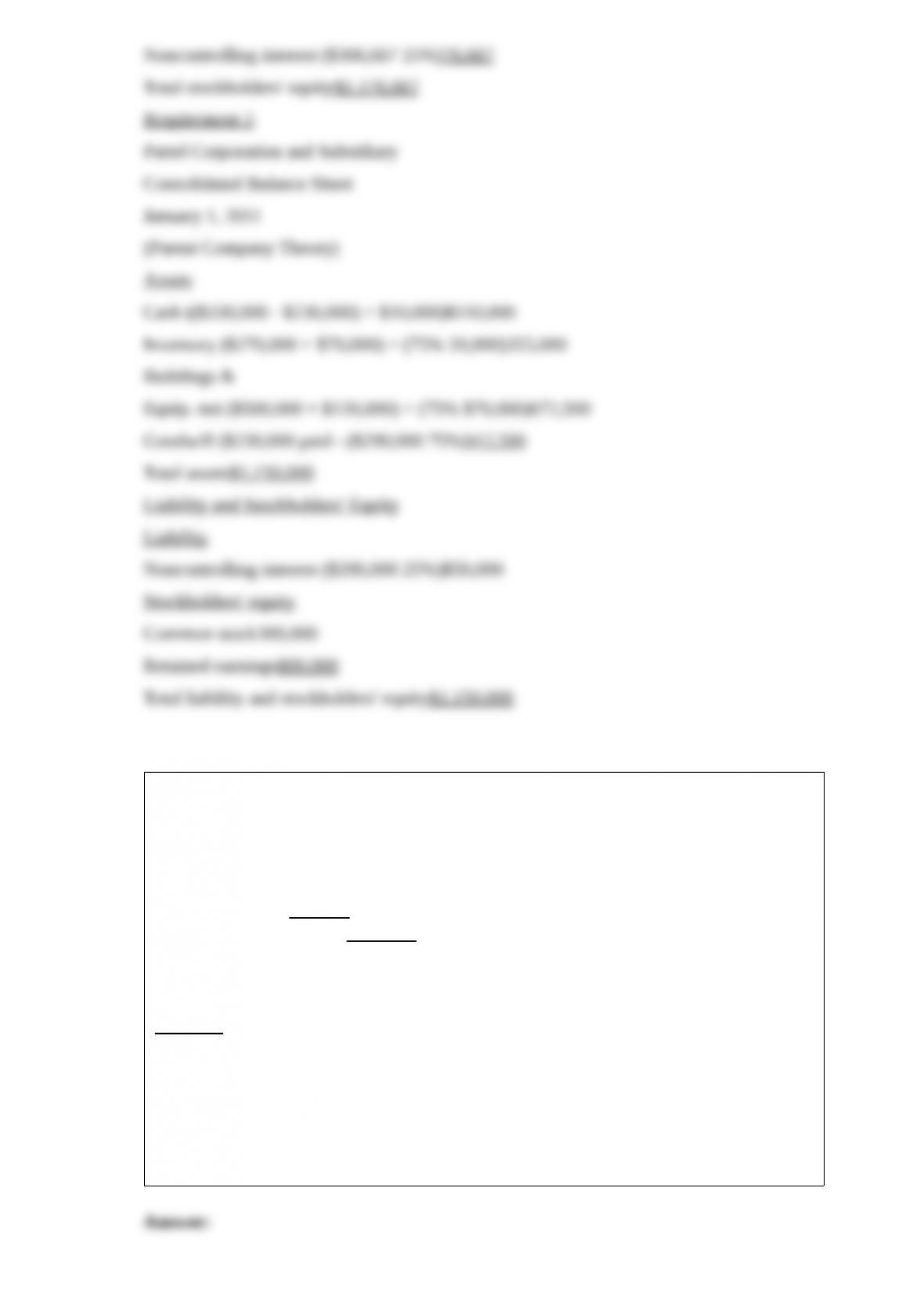

20) Partel Corporation purchased 75% of Sandford Corporation on January 1, 2011, for

$230,000. Balance sheets for the two companies on this date, prepared just prior to the

purchase, are provided below.

PartelSandfordSandford

Book ValuesBook ValuesFair Values

Cash$330,000$10,000$10,000

Inventory270,00070,00090,000

Buildings & equipment-net500,000120,000190,000

Total assets$1,100,000$200,000$290,000

Common stock$300,00095,000

Retained earnings800,000105,000

Total equities$1,100,000$200,000

Required:

1> Prepare a consolidated balance sheet using the entity theory of consolidation.

2> Prepare a consolidated balance sheet using the parent company theory of

consolidation.

21) Saito Corporation’s stockholders’ equity on December 31, 2010 was as follows:

10% cumulative preferred stock, $100 par value,

callable at $105, with one year dividends in arrears$10,000

Common stock, $1 par value50,000

Additional paid-in capital150,000

Retained earnings160,000

Total stockholders’ equity$370,000

On January 1, 2011, Panata Corporation paid $300,000 for a 70% interest in Saito’s

common stock. On January 1, 2011, the book values of Saito’s assets and liabilities

were equal to fair values.

Required:

1> Determine the book value of the common stockholders’ equity for Saito Corporation

on January 1, 2011 .

2> What is the amount of goodwill reported on the consolidated balance sheet for

Panata Corporation (and Subsidiary) at January 2, 2011?

3> What is the noncontrolling interest that appeared on a consolidated balance sheet for

Panata Corporation (and Subsidiary) on January 2, 2011?