Which of the following is not a true statement about a multiple-step income statement?

a. Operating expenses are similar for merchandising and service enterprises.

b. There may be a section for nonoperating activities.

c. There may be a section for operating assets.

d. There is a section for cost of goods sold.

Answer:

Each of the following is used in computing revised annual depreciation for a change in

estimate except

a. book value.

b. cost.

c. depreciable cost.

d. remaining useful life.

Answer:

Closing entries may be prepared from all of the following except

a. Adjusted balances in the ledger

b. Income statement and balance sheet columns of the worksheet

c. Balance sheet

d. Income and retained earnings statements

Answer:

Alfalfa Company developed the following information about its inventories in applying

the lower-of-cost-or-market (LCM) basis in valuing inventories:

If Alfalfa applies the LCM basis, the value of the inventory reported on the balance

sheet would be

a. $343,000.

b. $347,000.

c. $358,000.

d. $362,000.

Answer:

Which accounts in the general ledger are affected when the monthly posting is made

from the sales journal?

a. Accounts Receivable; accounts receivable subsidiary accounts

b. Accounts receivable subsidiary accounts; Sales Revenue

c. Accounts Receivable; Sales Revenue

d. Accounts Receivable; Inventory

Answer:

Net income results when

a. Assets > Liabilities.

b. Revenues = Expenses.

c. Revenues > Expenses.

d. Revenues < Expenses.

Answer:

The use of a cash register for cash receipts is an example of the internal control

principle of

a. documentation procedures.

b. physical controls.

c. independent internal verification.

d. segregation of duties.

Answer:

Fugazi City College sold season tickets for the 2015 football season for $240,000. A

total of 8 games will be played during September, October and November. In

September, two games were played. In October, three games were played. The balance

in Unearned Ticket Revenue at October 31 is

a. $0.

b. $60,000.

c. $90,000.

d. $150,000.

Answer:

In order to be considered extraordinary, an item must be

a. frequent and uninsured.

b. unusual and uninsured.

c. uninsured and infrequent.

d. infrequent and unusual.

Answer:

The following information is available for Everett Company at December 31, 2015:

beginning inventory $80,000; ending inventory $120,000; cost of goods sold

$1,050,000; and sales $1,800,000. Everett’s inventory turnover in 2015 is

a. 8.7 times.

b. 10.5 times.

c. 13.2 times.

d. 18 times.

Answer:

A legal document which summarizes the rights and privileges of bondholders as well as

the obligations and commitments of the issuing company is called

a. a bond indenture.

b. a bond debenture.

c. trading on the equity.

d. a term bond.

Answer:

Preparing tax returns and engaging in tax planning is performed by

a. public accountants only.

b. private accountants only.

c. both public and private accountants.

d. IRS accountants only.

Answer:

All of the following statements about the post-closing trial balance are correct except it

a. shows that the accounting equation is in balance.

b. provides evidence that the journalizing and posting of closing entries have been

properly completed.

c. contains only permanent accounts.

d. proves that all transactions have been recorded.

Answer:

Deane Company has income from continuing operations of $520,000 for the year ended

December 31, 2015. It also has the following items (before considering income taxes):

(1) An extraordinary fire loss of $140,000.

(2) A gain of $80,000 on the discontinuance of a major segment.

(3) A correction of an error in last year’s financial statement that resulted in a $60,000

overstatement of 2014 net income.

Assume all items are subject to income taxes at a 25% tax rate.

Instructions

(a) Prepare an income statement, beginning with income from continuing operations.

(b) Indicate the statement presentation of any item not included in (a) above.

Answer:

Storing cash in a company safe is an application of which internal control principle?

a. Segregation of duties

b. Documentation procedures

c. Physical controls

d. Establishment of responsibility

Answer:

Stockholders’ equity is often referred to as

a. residual equity.

b. leftovers.

c. spoils.

d. second equity.

Answer:

Financing activities involve

a. lending money.

b. acquiring investments.

c. issuing debt.

d. acquiring long-lived assets.

Answer:

In calculating net cash provided by operating activities using the indirect method, an

increase in prepaid expenses during a period is

a. deducted from net income.

b. added to net income.

c. ignored because it does not affect income.

d. ignored because it does not affect expenses.

Answer:

In its first year of operations, Arid Corporation had the following transactions

pertaining to its $20 par value preferred stock.

Instructions

(a) Journalize the transactions.

(b) Indicate the amount to be reported for (1) preferred stock, and (2) paid-in capital in

excess of par ‘” preferred stock at the end of the year.

Answer:

Which statement about long-term investments is not true?

a. They will be held for more than one year.

b. They are not currently used in the operation of the business.

c. They include investments in stock of other companies and land held for future use.

d. They can never include cash accounts.

Answer:

An item is considered material if

a. it doesn’t cost a lot of money.

b. it is of a tangible good.

c. it is likely to influence the decision of an investor or creditor.

d. the cost of reporting the item is greater than its benefits.

Answer:

Under the allowance method, Bad Debts Expense is debited when an account is deemed

uncollectible and must be written off.

Answer:

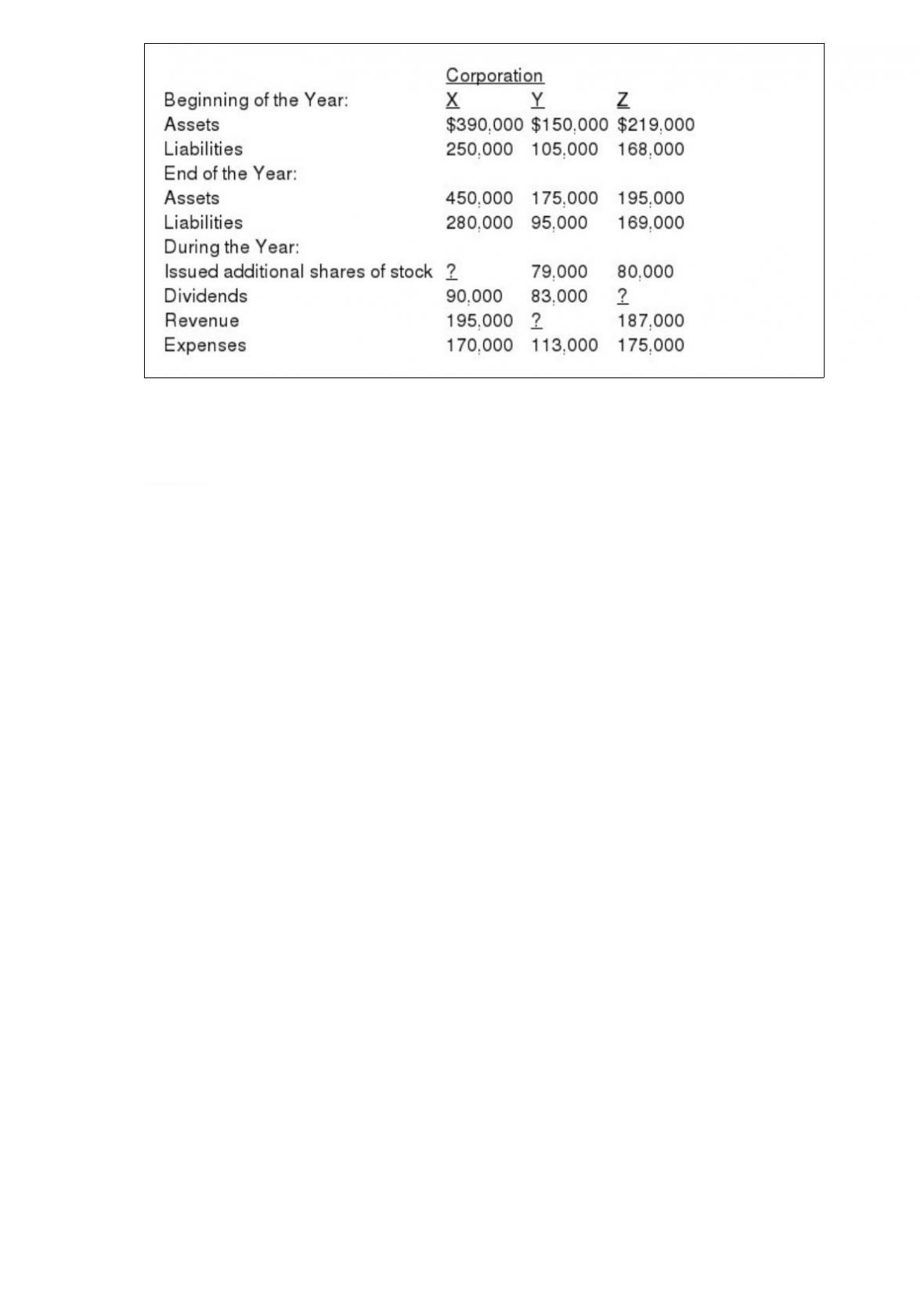

One item is omitted in each of the following summaries of balance sheet and income

statement data for three different sole corporations, X, Y, and Z. Determine the amounts

of the missing items, identifying each corporation by letter.

Answer:

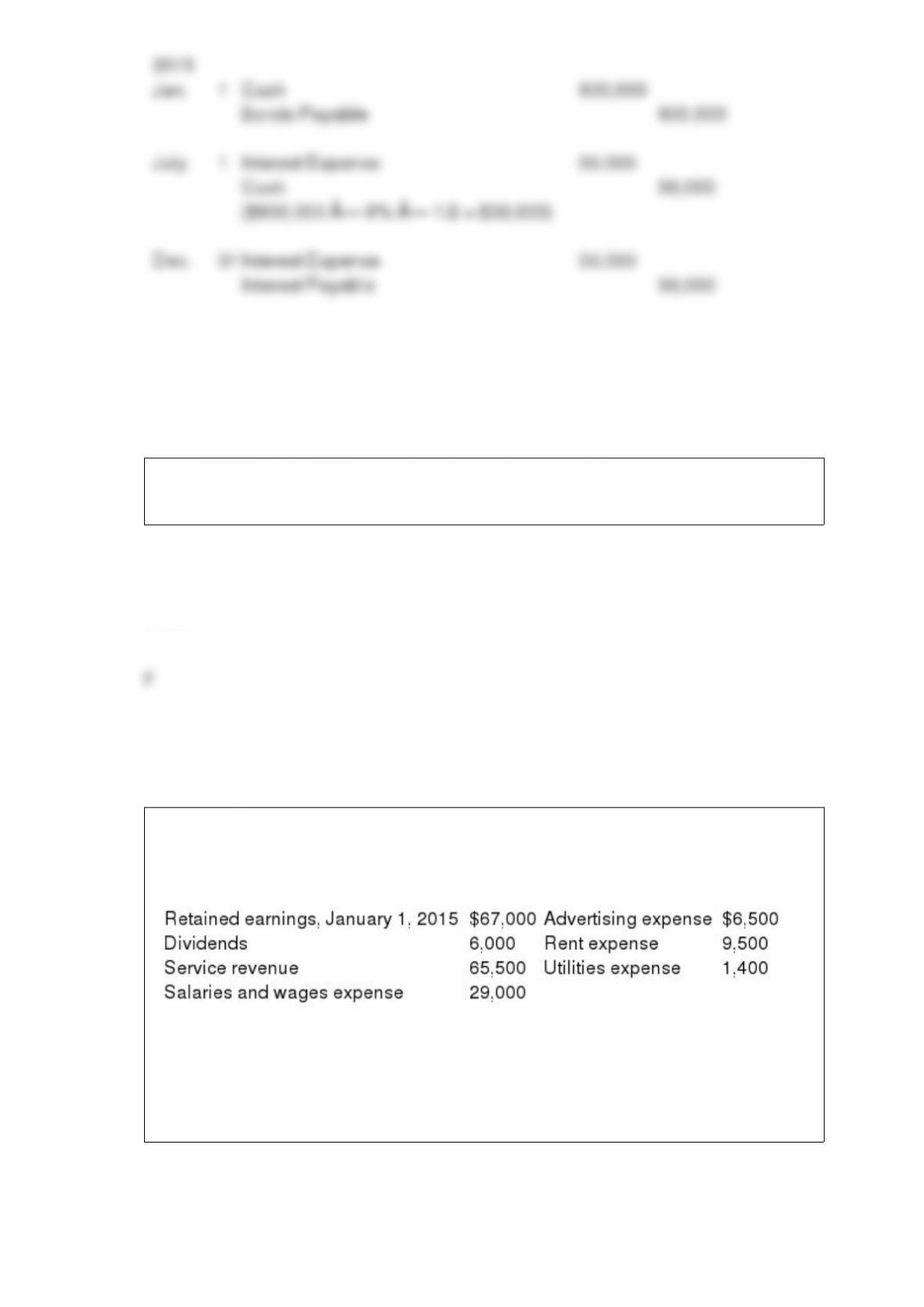

On January 1, 2015, Lost Corporation issued $900,000, 8%, 10-year bonds at face

value. Interest is payable semiannually on July 1 and January Lost Corporation has a

calendar year end.

Instructions

Prepare all entries related to the bond issue for 2015.

Answer:

Revenue received before services are performed and expenses paid before being used or

consumed are both initially recorded as liabilities.

Answer:

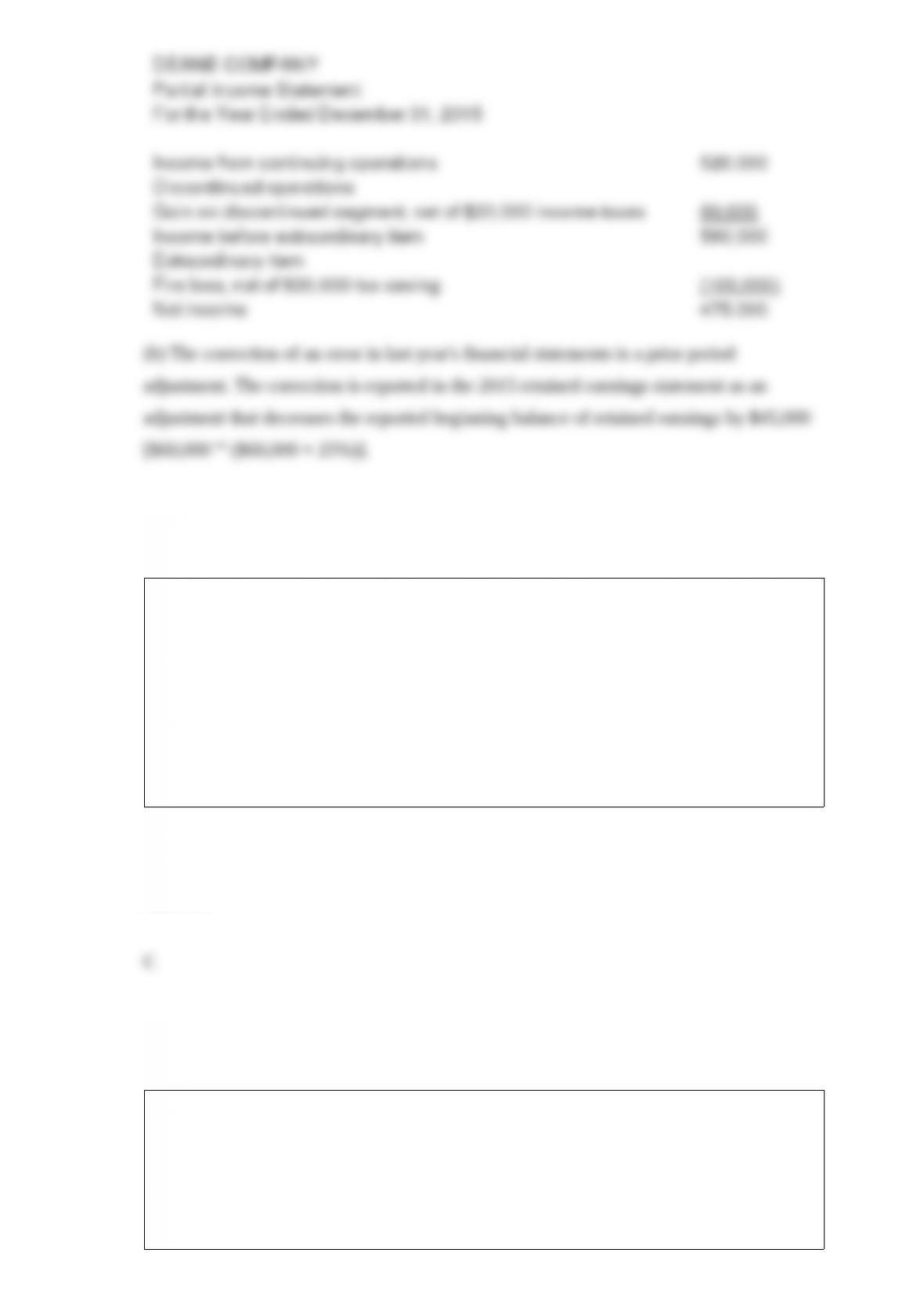

The following information relates to Bonnie Billy Co. for the year 2015.

Instructions

After analyzing the data, prepare an income statement and a retained earnings statement

for the year ending December 31, 2015

Answer: