The audit plan includes the nature, timing and extent of audit procedures for the

purposes of risk assessment, including those that are linked to the individual audit

assertions, as well as any other audit procedures that are considered necessary. At what

point in the audit process is the audit plan finalized? When

A) the auditor has finished documenting internal controls.

B) the client risk profile has been completed.

C) risk assessments are complete.

D) inherent risk information has been gathered.

The normal starting point for the audit of notes payable is

A) a discussion with management of any new notes payable for the year.

B) a schedule of notes payable and accrued interest obtained from the client.

C) the assessment of materiality.

D) the minutes of the board of directors.

Which of the following is an example of subjective evidence?

A) a positive confirmation of an account receivable

B) a bank confirmation

C) inquiries of the credit manager about the collectability of noncurrent accounts

receivable

D) the physical count of securities and cash

A) Step one in the auditor’s study and evaluation of internal control is obtain

understanding of internal control for audit planning purposes. List each of the

remaining steps.

B) Once the auditor has an understanding of internal control, two assessments are made.

List each assessment that must be made prior to testing controls.

C) Describe five common procedures an auditor can use to obtain an understanding of

internal control design.

A review engagement includes

A) obtaining an understanding of the internal controls.

B) tests of controls or transactions.

C) inquiry, analytical procedures and discussion.

D) independent confirmation or physical examination.

A) Discuss the methodology for designing tests of details of balances for cash in the

bank.

B) An effective monthly bank reconciliation by client personnel includes nine

procedures. List these nine bank reconciliation procedures.

C) Discuss two analytical procedures commonly performed during the audit of the cash

account.

Most companies recognize sales when

A) a customer order is received.

B) the merchandise is shipped.

C) the merchandise is received by the customer.

D) cash is received on account.

What is the purpose of an auditor reporting on the effectiveness of internal control over

financial reporting? To

A) attest to the effectiveness and efficiency of internal controls at an organization.

B) state an opinion on management’s assessment of the effectiveness of internal

controls.

C) provide an alternative to the operational audits conducted by internal auditors.

D) state that the controls are in conformity with standards with respect to internal

controls.

A) What are the different business organization structures that an accountant may use?

What are the advantages of these structures?

B) What is the difference between auditors and lawyers with respect to privileged

information?

Locker Building is a new apartment building in a Vancouver suburb. In order to receive

a subsidy from the municipality, it needs to prove that it has complied with the city’s

new rules about “green efficiency”. The “green efficiency” rules are described on the

municipality’s website and list the requirements a building must meet to be considered

green and efficient. Your firm, with the help of an environmental scientist, has been

asked to perform a direct reporting engagement for Locker building. The suitable

criteria in this case are the

A) green efficiency rules.

B) auditor’s judgment.

C) environmental scientist’s judgment.

D) federal environmental laws.

A substantive procedure is used to

A) assess the likelihood of material misstatement in the financial statements.

B) obtain an understanding of internal controls.

C) analyze the account balance to see if there are potential errors.

D) quantify the amount of potential error in an account or transaction stream.

The most important internal control for petty cash is

A) the use of an imprest fund that is the responsibility of one individual.

B) keeping it in a safe or locked drawer.

C) keeping the amount of cash to a minimum.

D) accessibility so that cheques won’t have to be written for small amounts.

When labour is a material factor in inventory valuation, the auditor should place special

emphasis on testing the internal controls concerning

A) proper classification of transactions.

B) authorization of wage rates.

C) fictitious employees.

D) completeness of recorded transactions.

When errors are found, a common and standard assumption in practice is to assume

A) a 100% assumption for all errors.

B) that the actual sample errors are representative of the population errors.

C) that the population errors are larger than the sample errors.

D) that the population errors are smaller than the sample errors.

As part of the review for subsequent events, the auditor will review financial statements

prepared after the balance sheet date. The statements should be discussed with

management to determine whether they

A) were approved by the controller prior to your review.

B) are mathematically correct, including calculation of depreciation.

C) are prepared on the same basis as the current-period statements.

D) were completed on a comparative basis, showing the last three years.

The test of details of balances procedure which requires the auditor to recalculate

accrued interest will satisfy the audit objective of

A) existence.

B) completeness.

C) classification.

D) accuracy

Your audit client has many different types of accounts receivable: Canadian, American,

and other international accounts, short term and long-term. There are also some sales on

consignment. The company has used forward exchange contracts to reduce its exposure

due to foreign exchange fluctuations. How will this affect the audit engagement?

A) control risk will increase

B) inherent risks of error will decrease

C) risk of material misstatement increases

D) audit risk will be increased

If the auditor were responsible for making certain that all the assertions of management

in the statements were correct,

A) bankruptcies could no longer occur.

B) bankruptcies would be reduced to a very small number.

C) audits would be much easier to complete.

D) audits would not be economically feasible.

The purchase order, usually in writing, is a legal document that is

A) a non-binding agreement between client and vendor.

B) an offer to buy.

C) not enforceable if it is not in writing.

D) an acceptance of a vendor’s catalogue offer to sell.

The auditor should review the preparation of at least one of each type of payroll tax

form the client is responsible for filing, as a part of the auditor’s responsibility for

A) understanding internal controls.

B) doing tests of controls.

C) doing analytical procedures.

D) doing tests of balances.

Control risk for notes payable is usually assessed as low. This occurs because internal

controls are normally good for notes payable and

A) creditors would complain if the notes are not paid.

B) interest expense can easily be distinguished from bank service charges.

C) there are a small number of large transactions or this type of transaction.

D) inclusion in the accounts payable listing helps track the notes.

A set of records for each piece of equipment that includes descriptive information, date

of acquisition, original cost, current year amortization, and accumulated amortization is

the

A) capital asset master file.

B) file of purchase requisitions.

C) amortization schedule.

D) acquisitions journal.

There is an increasing demand for assurance about computer controls surrounding

financial information transacted electronically and the security of the information

related to the transaction. This is in large part due to

A) the increasing presence of internet sales in many businesses.

B) the use of computer assisted auditing tools.

C) the many transactions and information shared online and in real time by companies.

D) client’s uncertainty about the proper functioning of their computer system.

When the auditor has properly planned and performed the audit to reduce risk to an

acceptably low level that is consistent with the objective of the audit, this means that

the auditor has conducted enough work to

A) reduce inherent risks to an acceptable level.

B) increase detection risk to a satisfactory level.

C) detect errors in internal controls so that control risk can be set higher.

D) detect material misstatements to the targeted level of assurance.

Danford, PA, is setting up his accounting firm as a sole practitioner. Which of the

following is an important way that Danford can reduce legal liability with respect to the

work completed by his office?

A) participate in the standard setting process for audit engagements

B) find out when his practice is due for practice inspection

C) hire only qualified personnel and train them well

D) sanction other PAs who engage in improper conduct

Which of the following substantive tests would the auditor conduct as a search for

contingent liabilities?

A) select an attribute sample of legal expenses for matching to invoices

B) select a dollar unit sample of legal expenses, for matching to invoices

C) inspect legal expense invoices, doing a census test of legal expenses

D) review a sample of legal invoices, looking for appropriate authorization for payment

Many companies have inventory that is easy to steal and is readily marketable. Which

of the following controls help to prevent theft and misuse of inventory?

A) physical control of inventory from time of receipt until use

B) proper access controls over the inventory master and transaction files

C) dual signatures required on all purchase orders over $10,000

D) purchase requisitions are to be approved by the production manager

When a physical count of inventory is permitted at an interim date, the auditor observes

it at that time, and also tests the perpetual inventory for transactions

A) throughout the year.

B) which are a representative sample of the period under audit.

C) from the date of the count to year-end.

D) from the date of the count to the end of the audit field work.

The audit of Simcoe Transports Inc. was completed three months ago so the PA firm

proceeded to the file archive stage in accordance with Canadian Audit Standards. If the

audit firm receives additional information related to the audit but the information does

not affect the audit conclusions, the information should be

A) disregarded as it the file archive was already done.

B) added to the audit file in the section to which it pertains.

C) separately identified and added at the front of the audit file.

D) added to the audit file and request that the reviewing partner reviews the new

information.

When considering pricing of inventory, three things are important. The first two are that

the method must be in accordance with an acceptable financial accounting framework,

and the application of the method must be consistent from year to year. What is the

third? The

A) input edits over the data entry of prices must be robust.

B) cut-off testing for the use of supplier invoices should be carefully done.

C) cost versus market value must be considered.

D) freight should always be included in the cost of the inventory.

Most international and national accounting firms in Canada are comprised of

professional accountants with the designations

A) CGA or CMA.

B) CMA or CIA.

C) CA [CPA] or CGA.

D) CIA or CISA.

In an effort to satisfy the completeness objective, the auditor could perform which of

the following test of details of balance procedures?

A) Trace the book balance on the reconciliation to the general ledger.

B) Trace outstanding cheques to subsequent period bank statements.

C) Obtain and test a cut-off bank statement.

D) Review financial statements to make sure that material savings accounts and

certificates of deposit are disclosed separately.

Describe the purpose of

i) a forecast

ii) a projection, and

iii) prospective financial statements

State the six functions that make up the inventory and distribution cycle and, for each

function, identify the related documents and/or records that would be used by a

manufacturing company.

The Canadian Auditing Standards state the the auditor must develop an audit plan. List

and explain the components that must be included in the auditor’s plan.

Describe the three objectives of the auditor’s examination of owners’ equity.

State the five specific balance-related audit objectives as applied to accounts receivable.

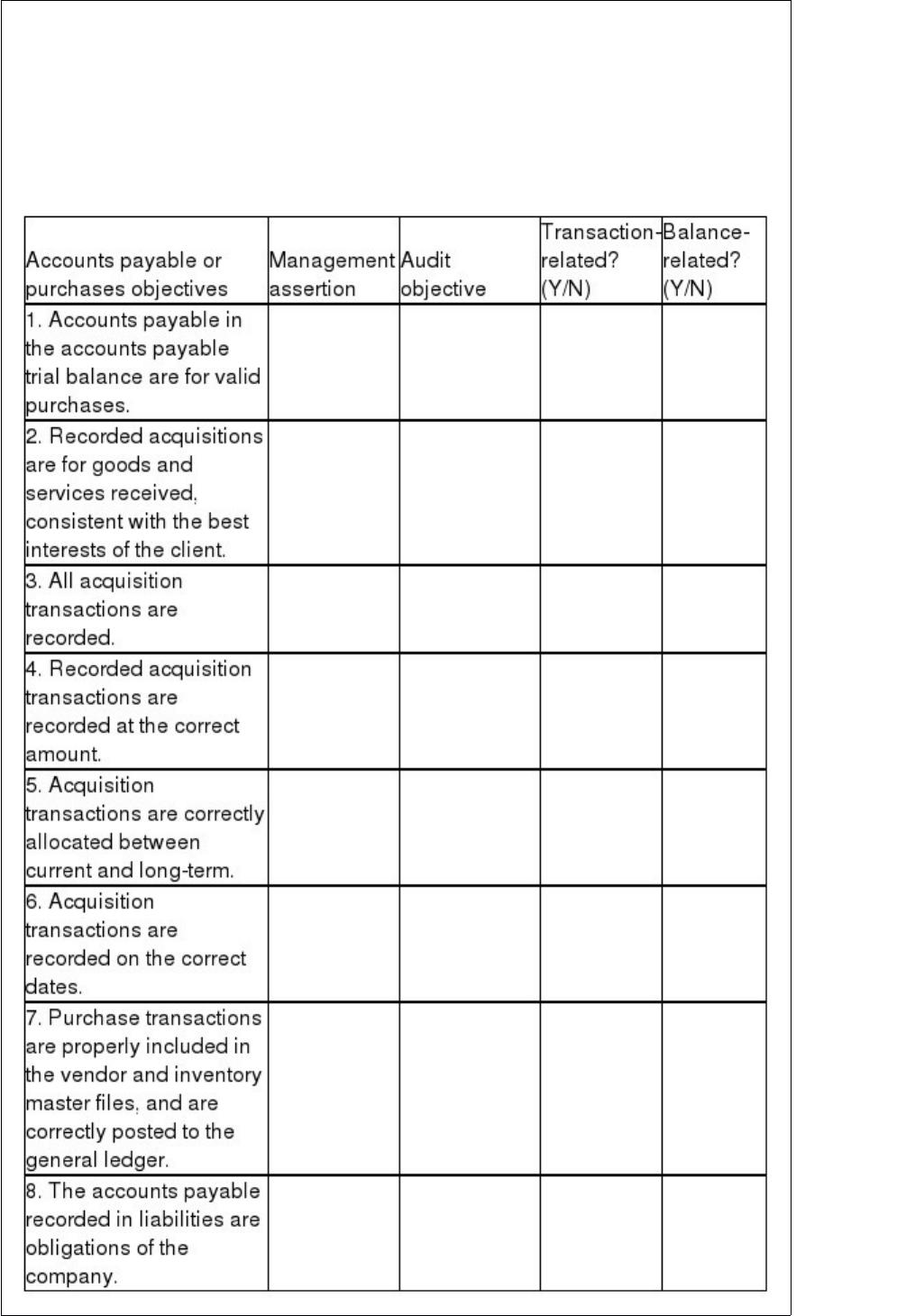

In the following table, there are listed common audit objectives for accounts payable or

purchases. For each procedure, list the management assertion, and the related general

audit objective. State whether the audit objective is transaction-related or

balance-related.

Describe the risks of error and fraud in the debt or equity accounts.

Your PA firm audits the Barney Bloke Parts company, which manufactures plastic

bumpers and other automobile parts in eight factories scattered across southern Ontario.

The company has a December year end. It is now November 14.

The planning file indicates that internal controls in the accounts receivable area are

poor, as there has been significant employee turnover. A review of the prior year’s

working paper file indicates that there was a poor response to the accounts receivable

and accounts payable confirmation requests. There were several errors in inventory

pricing and problems with obsolescence.

Required:

List the financial statement cycles that need to be tested. For each cycle, identify at least

one transaction that needs to be examined. For that transaction, identify a management

assertion that may have a high risk of error associated with it and explain why you

believe the risk of error is high.

Describe the major risks of error or fraud in the inventory and distribution cycle, using

the headings of (i) risks of error, (ii) risks of misappropriation of assets, other fraud or

illegal acts, and (iii) risks of inadequate disclosure or incorrect presentation of financial

information, including fraudulent financial reporting.

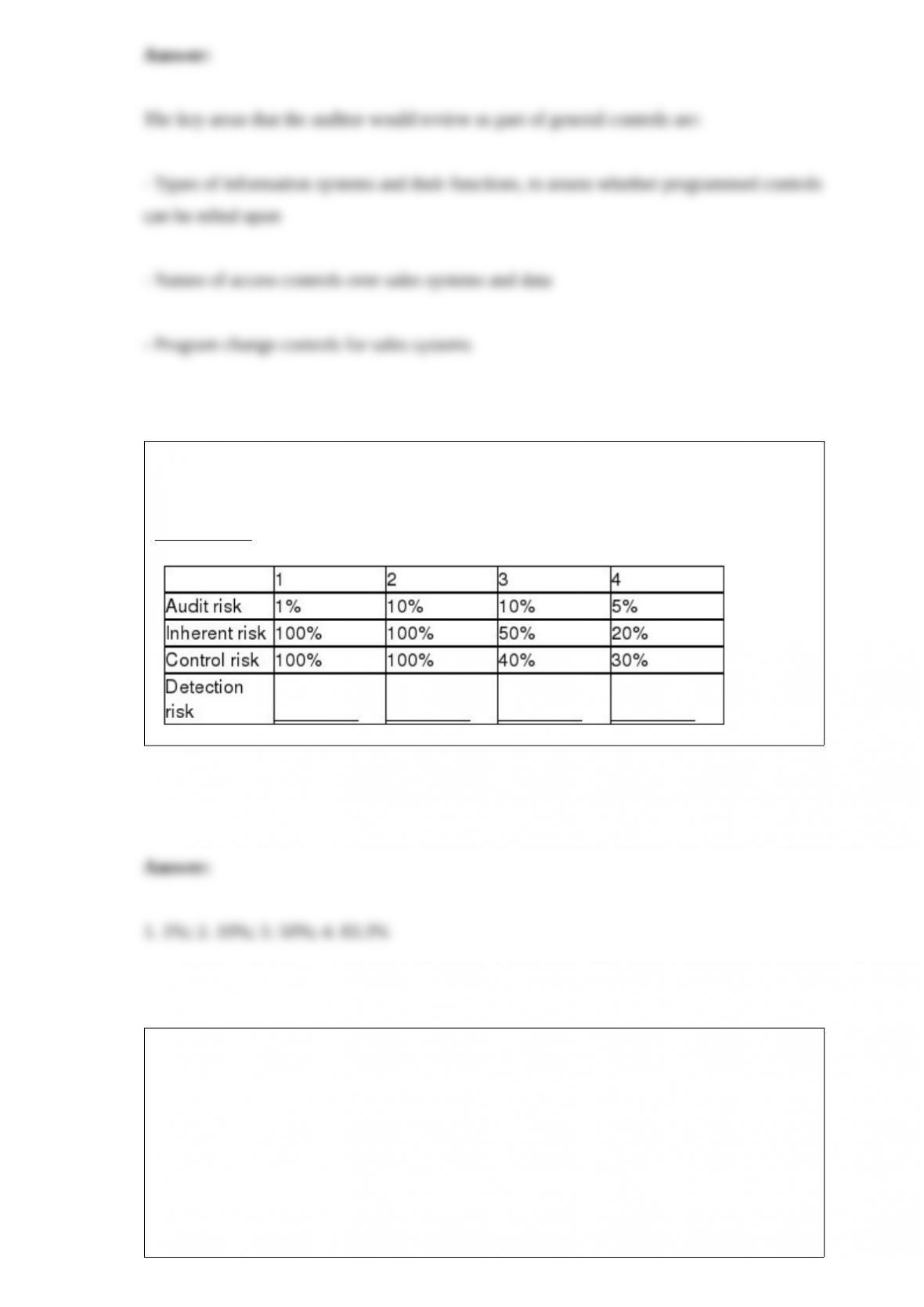

Outline the key areas that the auditor would review as part of general controls.

Below are four situations that involve the audit risk model as it is used for planning

audit evidence requirements in the audit of inventory. For each situation, calculate

planned detection risk.

SITUATION

Following are examples of evidence that could be collected during an audit of financial

statements.

1. Duplicate copies of sales invoices.

2. Inspection of new $100,000 cutting machine.

3. Bank confirmation.

4 Remittance advices.

5. Vendor’s invoices.

6. Standard letter from lawyer to auditor.

7. Auditor inventory count sheets.

8. Shipping documents.

9. Payroll cheques.

10. Long-term debt agreements review notes.

11. Auditor interest expense calculation worksheet.

12. Observation by auditor of computer error message (invalid supplier number).

13. Gross margin calculation.

14. Interview notes from interview with credit manager.

Required:

Classify each type of evidence as to its reliability (1 – high, 2 – moderate, 3 – low).

Justify your classification.

Describe the two objectives that are most important in auditing accumulated

amortization. Explain why these objectives are important.

Discuss the three key controls over notes payable.

State the three conditions required for a contingent liability to exist.

Describe the items the auditor is required to report to the audit committee.