In a good system of internal control, the person who initiates a transaction should be

allowed to effectively control the processing of the transaction through its final

inclusion in the accounting records.

According to International Financial Reporting Standards (IFRS), the impairment loss

for an indefinite-life intangible asset other than goodwill is the difference between book

value and the recoverable amount.

With an ordinary annuity, a payment is made or received on the date the agreement

begins.

Assets classified as property, plant, and equipment include machinery, equipment, and

inventories.

All securities considered available for sale should be reported as current assets in a

classified balance sheet.

Under IFRS, accounts receivable can be accounted for at fair value whenever company

management wants to do so.

Amortizing prior service cost for pension plans will:

a. Decrease assets.

b. Increase liabilities.

c. Increase shareholders’ equity.

d. Decrease retained earnings.

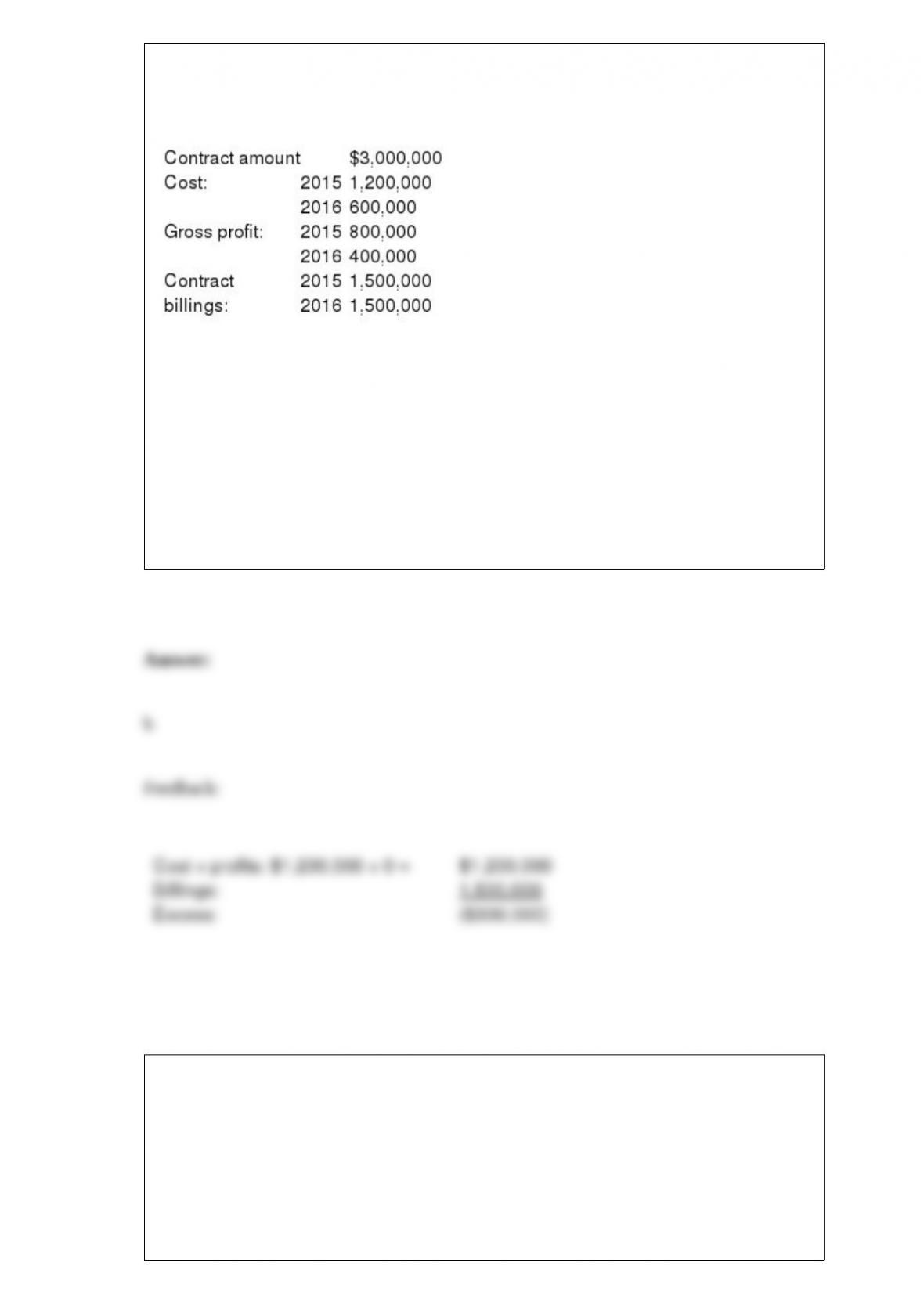

Sahara Desert Homes (SDH) reports under IFRS and constructed a new subdivision

during 2015 and 2016 under contract with Cactus Development Co. Relevant data are

summarized below:

SDH uses the cost recovery method under IFRS to recognize revenue. In its December

31, 2015, balance sheet, SDH would report:

a. The asset, cost and profits in excess of billings, of $500,000.

b. The liability, billings in excess of cost, of $300,000.

c. The asset, contract amount in excess of billings, of $1,500,000.

d. The asset, deferred profit, of $400,000.

Cutter Enterprises purchased equipment for $72,000 on January 1, 2016. The equipment

is expected to have a five-year life and a residual value of $6,000. Using the

straight-line method, the book value at December 31, 2016, would be:

a. $57,600.

b. $51,600.

c. $58,800.

d. $52,800.

Intraperiod income tax presentation is primarily a matter of:

a. Valuation.

b. Going concern.

c. Periodicity.

d. Allocation.

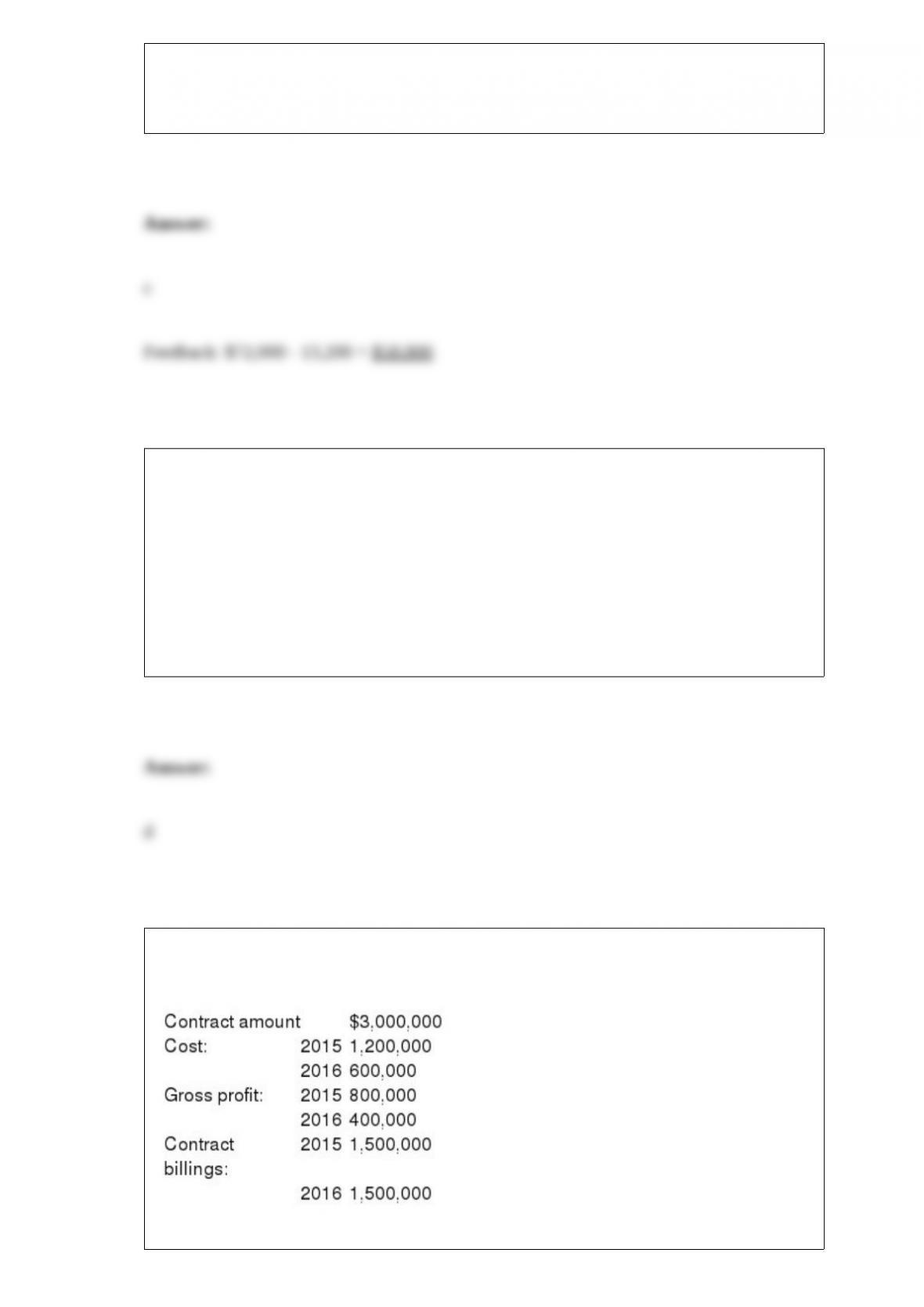

Arizona Desert Homes (ADH) constructed a new subdivision during 2015 and 2016

under contract with Cactus Development Co. Relevant data are summarized below:

ADH recognizes revenue over time with respect to these contracts.

In its December 31, 2015, balance sheet, ADH would report:

a. The contract asset, cost and profits in excess of billings, of $500,000.

b. The contract liability, billings in excess of cost, of $300,000.

c. The contract asset, contract amount in excess of billings, of $1,500,000.

d. The contract asset, deferred profit, of $400,000.

Archie Co. purchased a framing machine for $45,000 on January 1, 2016. The machine

is expected to have a four-year life, with a residual value of $5,000 at the end of four

years. Using the double-declining balance method, depreciation for 2017 and book

value at December 31, 2017, would be:

a. $10,000 and $5,000.

b. $10,000 and $10,000.

c. $11,250 and $6,250.

d. $11,250 and $11,250.

If a stock dividend were distributed, when calculating the current year’s EPS, the shares

distributed are treated as having been issued:

a. At the end of the year.

b. At the beginning of the year.

c. On the declaration date.

d. On the date of distribution.

The rate of return on shareholders’ equity indicates:

a. The margin of safety provided to creditors.

b. The extent of “trading on the equity” or financial leverage.

c. Profitability without regard to how resources are financed .

d. The effectiveness of employing resources provided by owners.

A company’s investment in receivables is influenced by several variables, including:

a. The level of sales.

b. The nature of the product or service sold.

c. The credit and collection policies.

d. All of these answer choices are correct.

Cendant Corporation’s results for the year ended December 31, 2016, include the

following material items:

Cendant Corporation’s income from continuing operations before income taxes for 2016

is:

a. $900,000.

b. $880,000.

c. $820,000

d. $320,000.

On January 1, 2016, Badger Inc. adopted the dollar-value LIFO method. The inventory

cost on this date was $100,000. The 2016 ending inventory, valued at year-end costs,

was $126,000. The relative cost index for this inventory in 2016 was 1.05. Suppose that

Badger’s 2017 ending inventory, valued at year-end costs, was $143,000 and that the

relative cost index for this inventory in 2017 was 1.10. In determining the inventory

balance should Badger report in its 12/31/17 balance sheet:

a. An additional layer of $23,000 is added to the 1/1/17 balance.

b. An additional layer of $22,000 is added to the 1/1/17 balance.

c. An additional layer of $11,000 is added to the 1/1/17 balance.

d. None of the above is correct.

Texas Petrochemical reported the following April activity for its VC-30 lubricant,

which had a balance of 300 qts. @ $2.40 on April 1.

The ending inventory assuming LIFO and a periodic inventory system is:

a. $1,580.

b. $1,510.

c. $1,575.

d. $1,470.

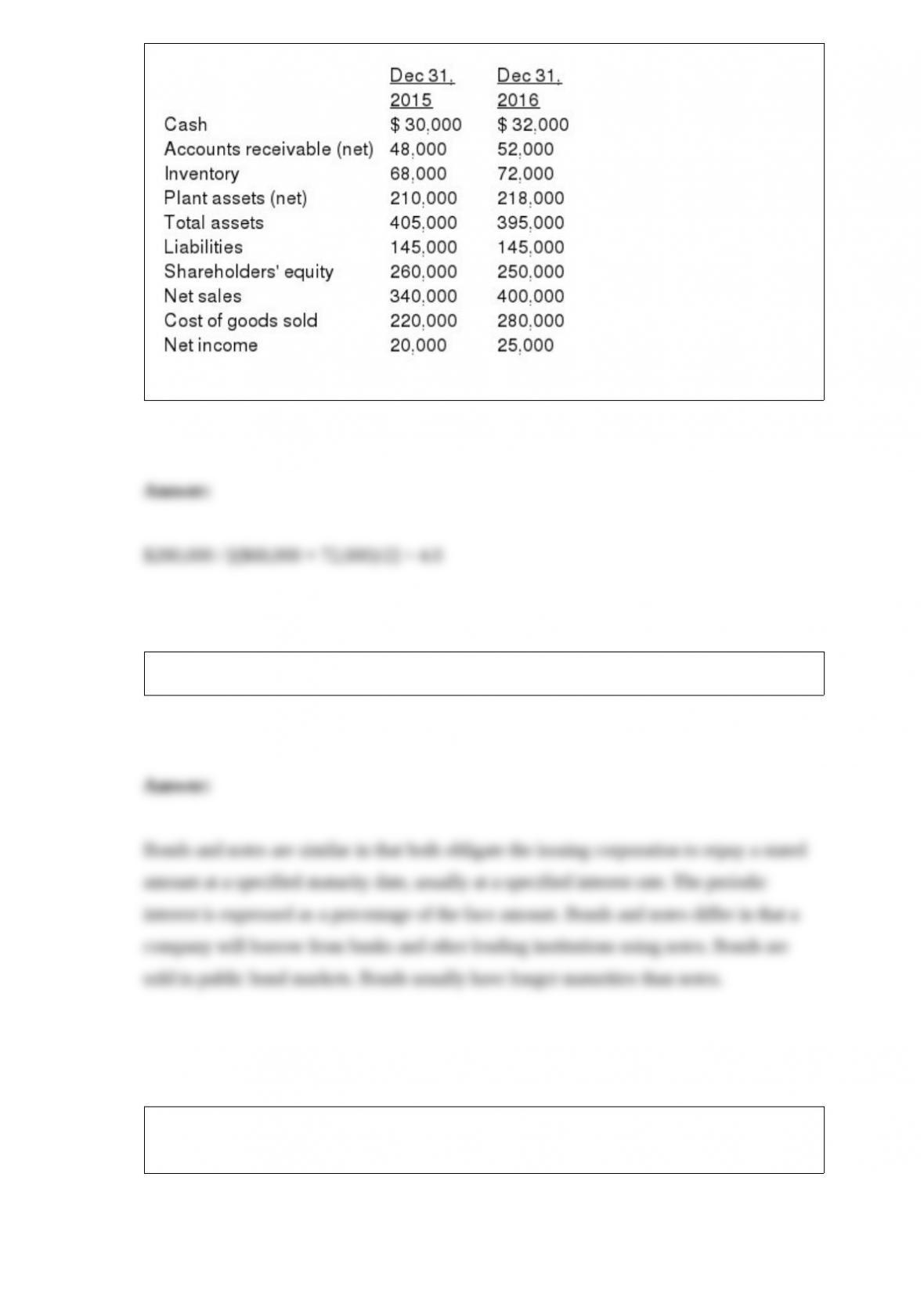

Missoula Inc. reported the following selected financial statement data:

Required: Compute the inventory turnover ratio for 2016.

How are bonds and notes the same? How do they differ?

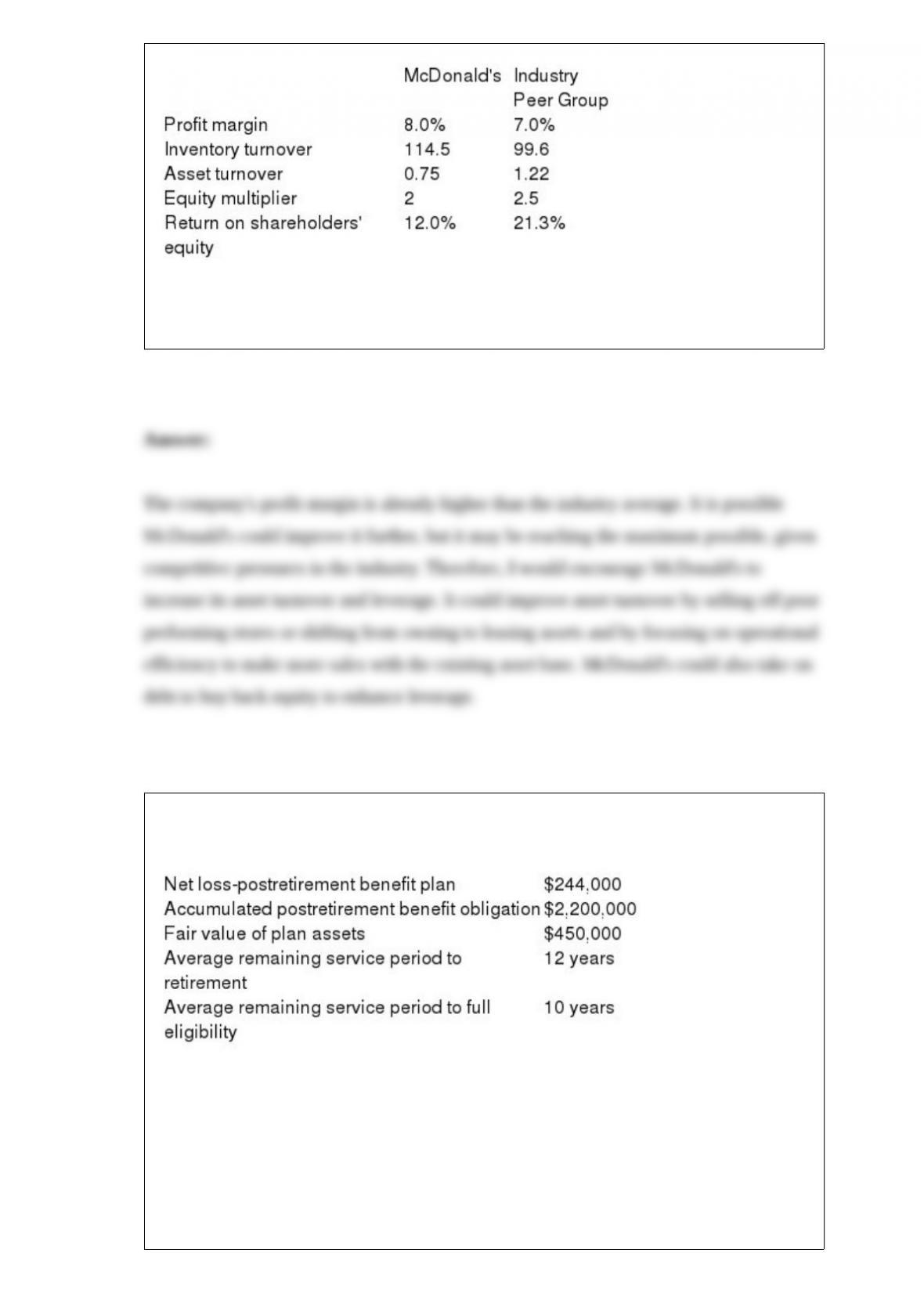

The following table presents a summary of ratio analysis for McDonald’s and averages

for their peer group:

Based on this information, if you were going to advise McDonald’s about how it could

enhance return on shareholders’ equity, what would you suggest? Be as specific as

possible in the operational or financial changes you would recommend.

Bazerman Inc. has a postretirement health care benefit plan. On January 1 of the current

calendar year, the following plan-related data were available.

The rate of return on plan assets during the year was 12%. The expected return was

10%. The actuary revised assumptions regarding the APBO at the end of the year,

resulting in a $42,000 increase in the estimate of the obligation.

Required:

1) Calculate any amortization of net loss that should be included as a component of

postretirement benefit expense for the current year.

2) Determine the net loss or gain as of December 31 of the current year.

Parsley Corporation had 250,000 shares of common stock and 5,000 shares of 8%,

$100 par, preferred stock outstanding on December 31, 2015. The preferred stock is

cumulative, nonconvertible preferred stock. On June 1, 2016, Parsley sold 36,000

shares of common stock for cash. No cash dividends were declared for 2016. Parsley

reported a net loss of $320,000 for the year ended December 31, 2013.

Required:

Calculate Parsley’s loss per share (rounded to 2 decimal places) for the year ended

December 31, 2016.

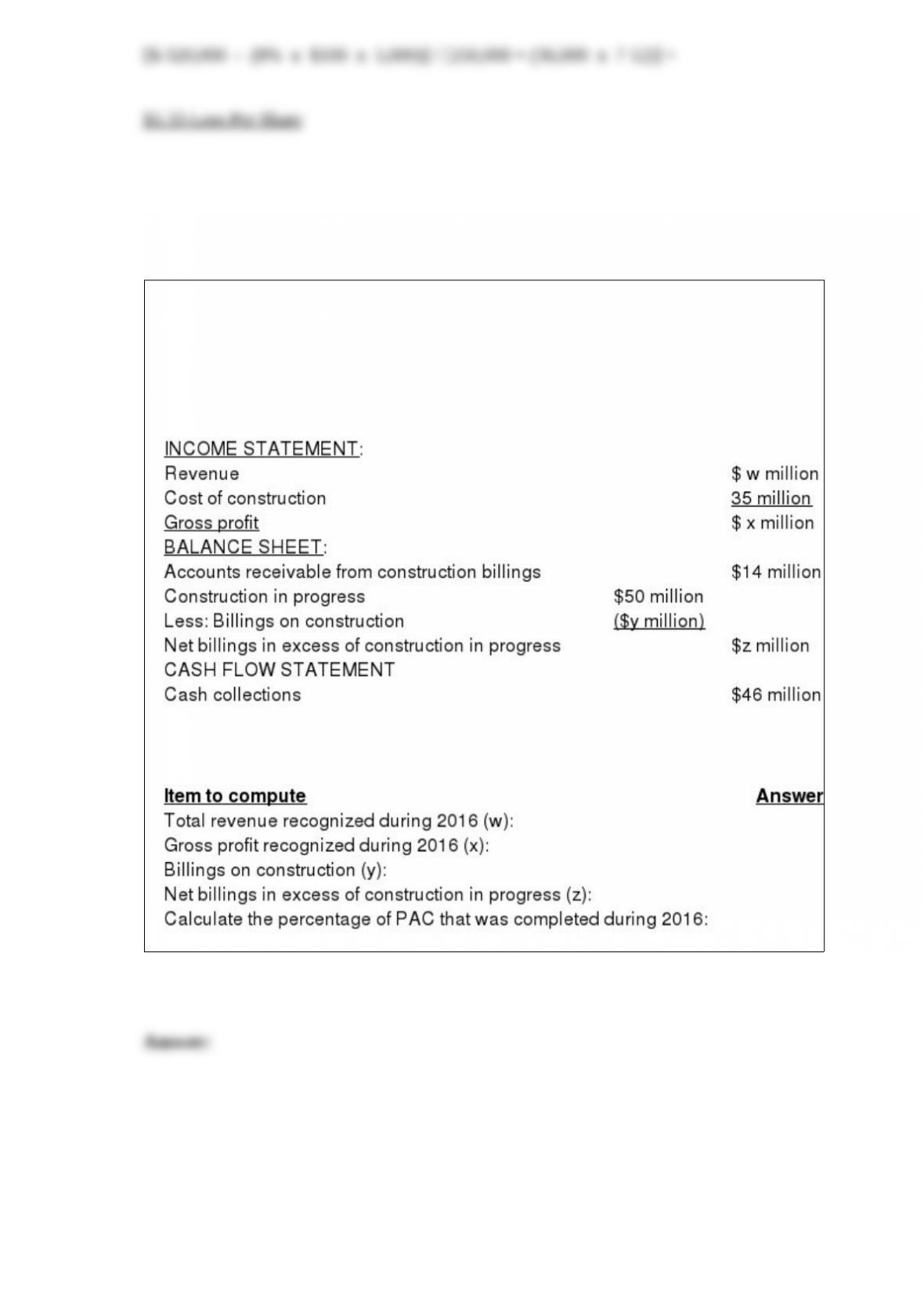

In 2016, Chicago Construction began work on a three-year construction project to build

a new performing arts complex (the PAC). The PAC contract price is $150 million.

Chicago recognizes revenue on this contract over time according to percentage of

completion. At the end of 2016, the following financial statement information indicates

the results to date for the PAC (missing items denoted by letter):

Required: Compute the following, placing your answer in the spaces provided and

showing supporting computations below:

The inventories disclosure note in the 2014 financial statements for SUPERVALU Inc.,

one of the largest grocery chains in the United States, included the following ($ in

millions):

“Inventories are valued at the lower of cost or market. Substantially all of the

Company’s inventory consists of finished goods. As of February 22, 2014 and

February 23, 2013, approximately 57 percent and 60 percent, respectively, of the

Company’s inventories were valued under the LIFO method. If the FIFO method had

been used to determine cost of inventories for which the LIFO method is used, the

Company’s inventories would have been higher by approximately $202 and $211 as of

February 22, 2014 and February 23, 2013, respectively.” Cost of goods sold for the

fiscal year ended February 22, 2014 was $14,623 million.Required:

If SUPERVALU had used FIFO for all of its LIFO inventories, what would its cost of

goods sold have been for 2014?