1) Which of the following is an advantage of systematic sample selection over random

number sampling?

A) It provides a stronger basis for statistical conclusions

B) It enables the auditor to use the more efficient ‘sampling with replacement” tables

C) There may be correlation between the location of items in the population, the feature

of sampling interest, and the sampling interval

D) It does not require establishment of correspondence between random numbers and

items in the population

2) A qualified report is issued when all auditing conditions have been met, no

significant misstatements have been discovered, and it is the auditor’s opinion that the

financial statements are fairly stated in accordance with GAAP.

A) True

B) False

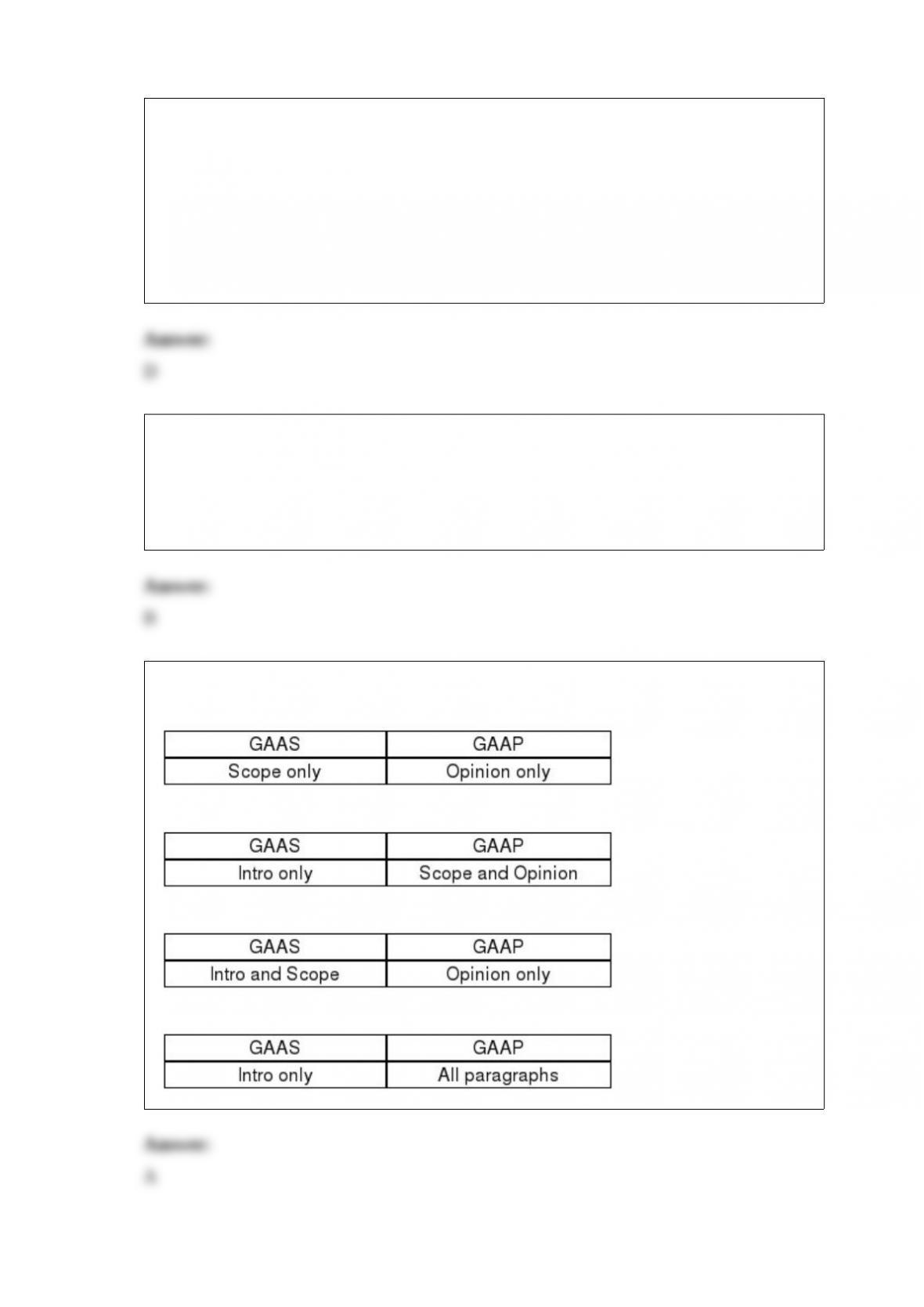

3) The standard audit report refers to GAAS and GAAP in which paragraphs?

A)

B)

C)

D)

4) When an employee who is authorized to make customer entries in the accounts

receivable subsidiary ledger, purposefully enters cash received into the wrong

customers account that employee may be suspected of:

A) kiting

B) lapping

C) floating

D) shorting

5) An audit procedure that would most likely be used by an auditor in performing tests

of control procedures in which the segregation of functions and that leaves no “audit”

trail is:

A) inspection

B) observation

C) reperformance

D) reconciliation

6) Internal controls can never be regarded as completely effective. Even if company

personnel could design an ideal system, its effectiveness depends on the:

A) adequacy of the computer system

B) proper implementation by management

C) ability of the internal audit staff to maintain it

D) competency and dependability of the people using it

7) When the client uses a computer but the auditor chooses to use only the non-IT

segment of internal control to assess control risk, it is referred to as auditing around the

computer. Which one of the following conditions need not be present to audit around

the computer?

A) Application controls need to be integrated with general controls

B) The source documents must be available in a non-machine language

C) The documents must be filed in a manner that makes it possible to locate them

D) The output must be listed in sufficient detail to enable the auditor to trace individual

transactions

8) The direct receipt of a confirmation from every bank with which the client does

business is:

A) required by auditing standards for every audit

B) not necessary unless material fraud is suspected

C) recommended but not required by auditing standards

D) necessary for every audit except when there are an unusually large number of active

accounts

9) The standards which govern the CPA’s association with unaudited financial

statements of private companies are the:

A)

B) Statements on Auditing Standards (SASs)

C) Statements of Standards on Attestation Engagements (SSAEs)

D) Statements on Standards for Accounting and Review Services (SSARS)

10) When a physical count of inventory is performed at an interim date, the auditor

observes it at that time and tests the perpetual records for transactions:

A) throughout the year

B) which are a representative sample of the period under audit

C) from the date of the count to year-end

D) from the date of the count to the end of the audit field work

11) A document that initiates shipment of goods and indicates the description of the

merchandise, the quantity shipped, and customer name and address is the:

A) bill of lading

B) sales invoice

C) picking ticket

D) vendor invoice

12) Statutory laws are laws that have been developed through court decisions rather

than through the U.S. Congress and other governmental units.

A) True

B) False

13) It is important for the CPA to consider the competence of the clients’ personnel

because their competence bears directly and importantly upon the:

A) cost/benefit relationship of the system of internal control

B) achievement of the objectives of internal control

C) comparison of recorded accountability with assets

D) timing of the tests to be performed

14) If an auditor assigns a tolerable misstatement of $1,000 to accounts payable, he or

she would need to obtain more audit evidence for that account than if $100,000 had

been assigned.

A) True

B) False

15) The two primary types of sampling methods used for calculating dollar

misstatements are attribute sampling and monetary unit sampling.

A) True

B) False

16) Match six of the terms (a-k) with the descriptions/definitions provided below (1-6):

a.Bank reconciliation

b.Branch cash account

c.Cash equivalents

d.Cutoff bank statement

e.General cash account

f.Imprest payroll account

g.Imprest petty cash fund

h.Kiting

i.Proof of cash

j.Standard bank confirmation form

k.Lapping

________ 1> A fund of cash maintained within the company for small cash

acquisitions, expenses, or to cash employees’ checks.

________ 2> A form approved by the

________ 3> Excess cash invested in short-term, highly liquid investments such as time

deposits, certificates of deposit, and money market funds.

________ 4> The primary bank account for most organizations.

________ 5> The transfer of money from one bank account to another and improperly

recording the transfer so that the amount is recorded as an asset in both accounts.

________ 6> The document usually prepared by client personnel of the differences

between the cash balance recorded in the general ledger and the amount in the bank

account.

17) If the client fails to record disposals of property, plant, and equipment, both the

original cost of the asset account and the net book value will be incorrect. What will the

effect be of this misstatement on the original cost and the book value?

A) Both will be overstated indefinitely

B) The original cost will be overstated indefinitely, and the net book value will be

overstated until the asset is fully depreciated

C) The original cost will be overstated indefinitely, and the net book value will be

understated indefinitely

D) The original cost will be overstated indefinitely, and the net book value will be

understated until the asset is fully depreciated

18) If a nonpublic company asks an accountant to perform a review engagement, and

the accountant has an immaterial direct financial interest in the company, the accountant

is:

A) independent because the financial interest is immaterial and, therefore, may issue a

review report

B) not independent and, therefore, may not issue a review report

C) not independent and, therefore, may not be associated with the financial statements

D) not independent and, therefore, may issue a review report, but may not issue an

auditor’s opinion

19) The detail tie-in objective is not concerned that the details in the account balance:

A) agree with related subsidiary ledger amounts

B) are properly disclosed in accordance with GAAP

C) foot to the total in the account balance

D) agree with the total in the general ledger

20) The auditor’s responsibility for “reviewing the subsequent events” of a public

company that is about to issue new securities is normally limited to the period of time:

A) beginning with the balance sheet date and ending with the date of the auditor’s report

B) beginning with the start of the fiscal year under audit and ending with the balance

sheet date

C) beginning with the start of the fiscal year under audit and ending with the date of the

auditor’s report

D) beginning with the balance sheet date and ending with the date the registration

statement becomes effective

21) How might the auditor determine whether a client has limited rights to accounts

receivable?

A)

B)

C)

D)

22) The effect of a violation of the completeness transaction-related audit objective for

cash disbursements transactions would be an overstatement of cash disbursements.

A) True

B) False

23) If the board of accountancy in the state in which a CPA firm is licensed has rules

that are different than the

A) whichever rules are less restrictive

B) whichever rules are more restrictive

C) the rules of the

D) the rules of the state’s board of accountancy

24) If an auditor is requested to perform nonaudit services for a public company audit

client, who is responsible for agreeing to those services with the audit firm?

A) the client’s management

B) the client’s chief executive officer

C) the client’s chief financial officer

D) the client’s audit committee

25) Integrity is one of the IIA’s ethical principles.

A) True

B) False

26) Peprah Company pays its accounts payable 45 days after receipt of the goods or

services. In this case which audit procedure should be used to detect any unrecorded

liabilities?

A) examine cash disbursements for several weeks after the balance sheet date

B) reconcile purchase orders to requisition orders

C) reconcile purchase orders to receiving reports

D) reconcile purchase orders to vendor invoices

27) State four types of assurance services that fall within the auditing standards but are

not audits, reviews, or compilations of financial statements in accordance with GAAP.

28) Auditor’s allocate the preliminary judgment about materiality to financial statement

segments rather than by financial statements as a whole. What is the term for the

auditor’s allocation of preliminary misstatement to account balances? What are three

difficulties auditor’s face when allocating materiality to balance sheet accounts?

29) There are several key internal controls over the payment of payroll function that

should be present. For example, the payroll should be distributed by someone who is

not involved in the other payroll functions. Discuss other key internal controls over the

payment of payroll function.

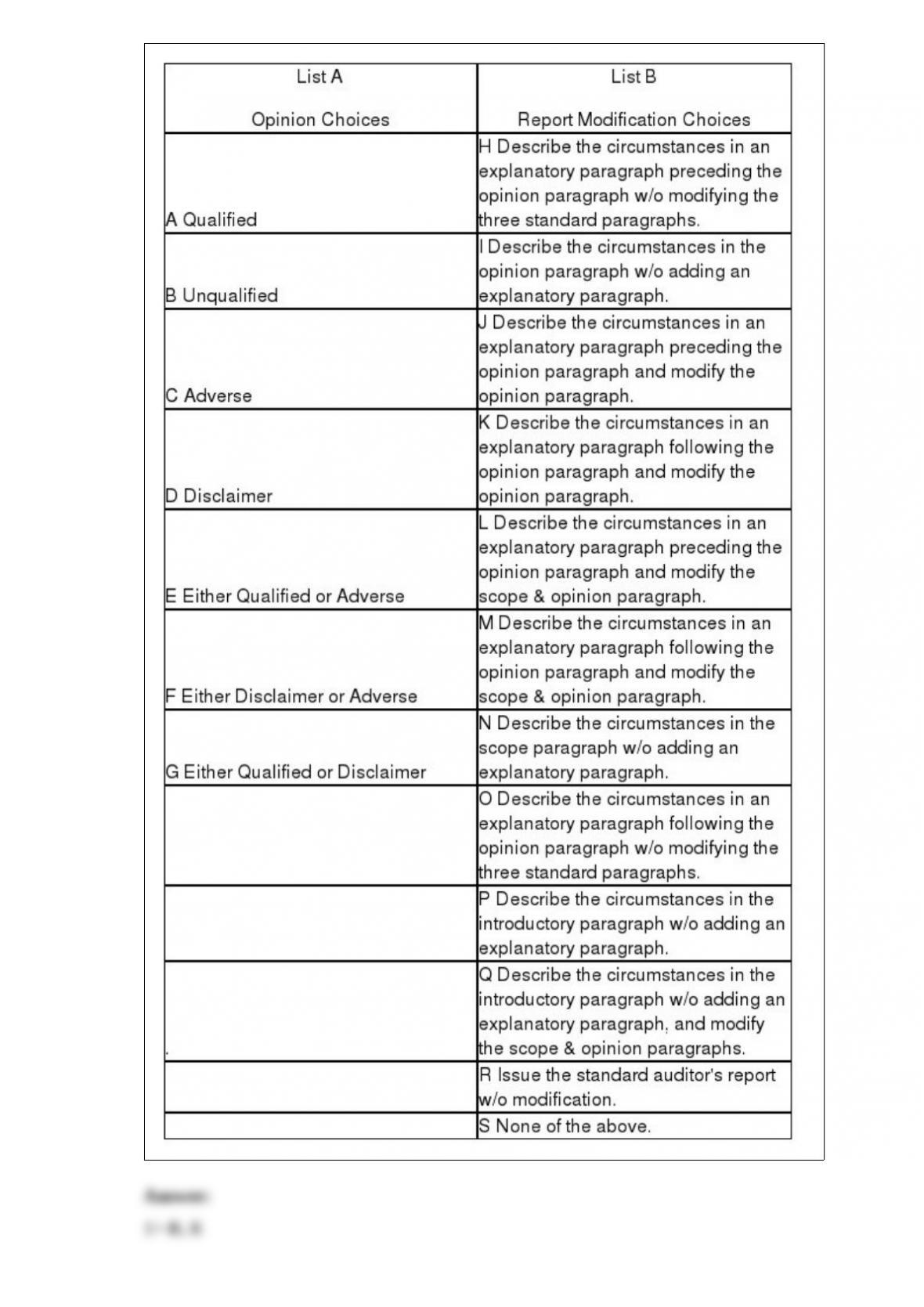

30) Audit situations 1 through 10 present various independent factual situations an

auditor might encounter in conducting an audit. List A represents the types of opinions

the auditor ordinarily would issue, and List B represents the report modifications (if

any) that would be necessary. For each situation, select one response from List A and

one from List B. Select, as the best answer for each item, the action the auditor

normally would take. Items from either list may be selected once, more than once, or

not at all.

Assume the following:

The auditor is independent

The auditor previously expressed an unqualified opinion on the prior-year financial

statements unless otherwise noted

Only single-year (not comparative) statements are presented for the current year (unless

otherwise stated)

The conditions for an unqualified opinion exist unless contradicted in the factual

scenario

The conditions stated in the factual scenario are material

No report modifications are to be made except in response to the factual scenario

Factual Scenario

1> The financial statements present fairly, in all material respects, the financial position,

results of operations, and cash flows in conformity with GAAP.

2> In auditing the Long-Term Investments account, an auditor is unable to obtain

audited F/S for an investee located in a foreign country. The auditor concludes that

sufficient competent evidential matter regarding this investment cannot be obtained but

it is not pervasive to the financials as a whole.

3> Due to recurring operating losses and working capital deficiencies the auditor has

substantial doubt about an entity’s ability to continue as a going concern for a

reasonable period of time. However, the F/S disclosures are adequate.

4> The principal auditor decides to refer to the work of another auditor, who audited a

wholly owned subsidiary of the entity and issued an unqualified opinion.

5> An entity issues F/S that present financial position and results of operations but

omits the related statement of cash flows. Management discloses in the notes to the F/S

that it does not believe the statement of cash flows to be useful.

6> An entity changes its depreciation method for production equipment from SL to

units of production based on hours of utilization. The auditor concurs with the change,

although it has a material effect on the comparability of the entity’s F/S.

7> An entity is a defendant in a lawsuit alleging infringement of certain patent rights.

However, management. cannot reasonably estimate the ultimate outcome of the

litigation. The auditor believes that there is a reasonable possibility of a significant

material loss, but the lawsuit is adequately disclosed in the notes to the F/S.

8> An entity discloses certain lease obligations in the notes to the F/S. The auditor

believes that the failure to capitalize these leases is a departure from GAAP.

9> The entity wishes to show comparative F/S and include the prior year. However, the

prior year F/S contained a qualification due to an inappropriate method of GAAP.

Accordingly, management. corrected the prior year GAAP deficiency and included the

updated numbers in the comparative financials for the current year.

10> The entity wishes to show comparative F/S and include the prior year. However,

the prior year F/S were audited by another auditor who refuses to reissue his opinion.

31) Why are analytical procedures essential for notes payable?

32) Discuss how materiality affects audit reporting decisions.

33) What are the two software testing strategies that companies typically use? Which

strategy is more expensive?