9-81

98.

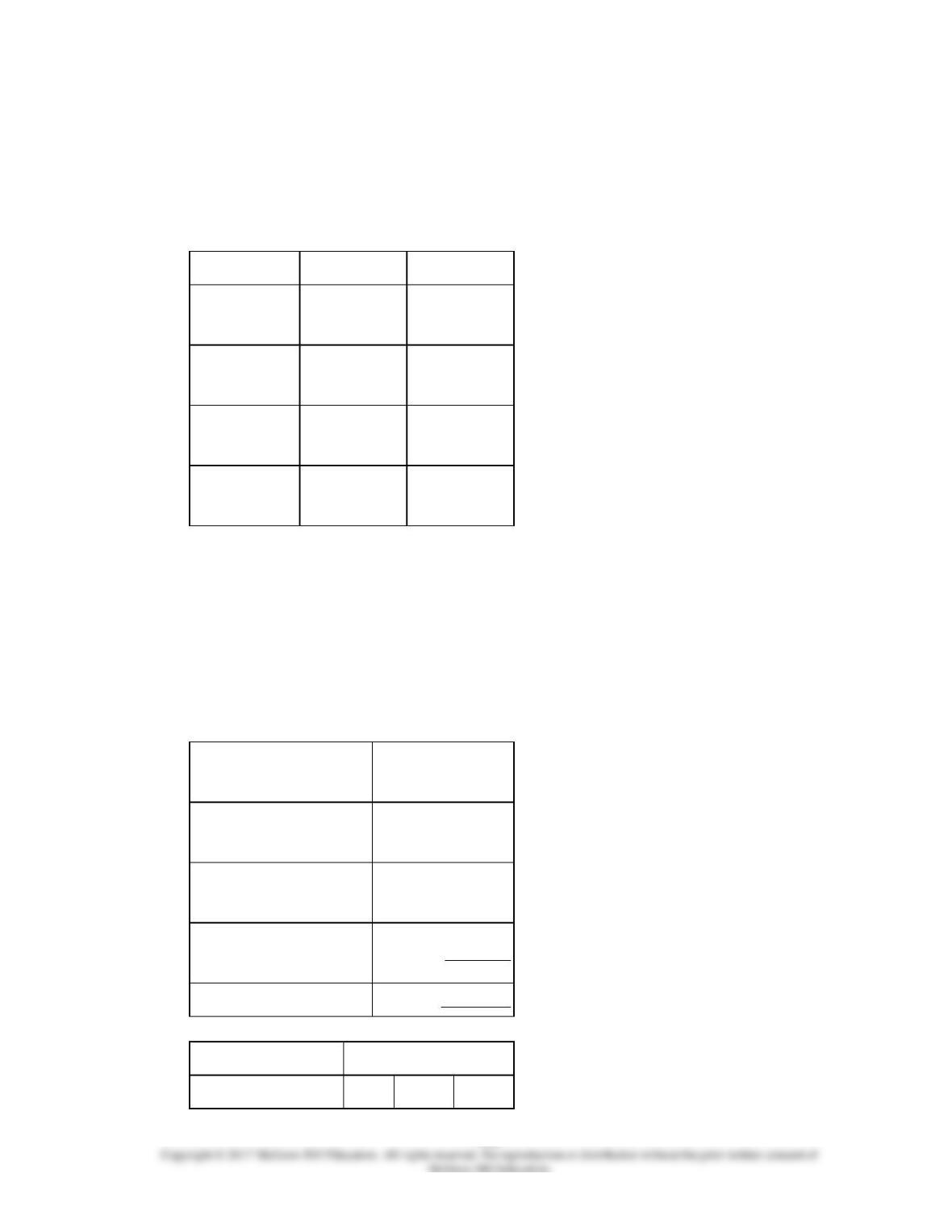

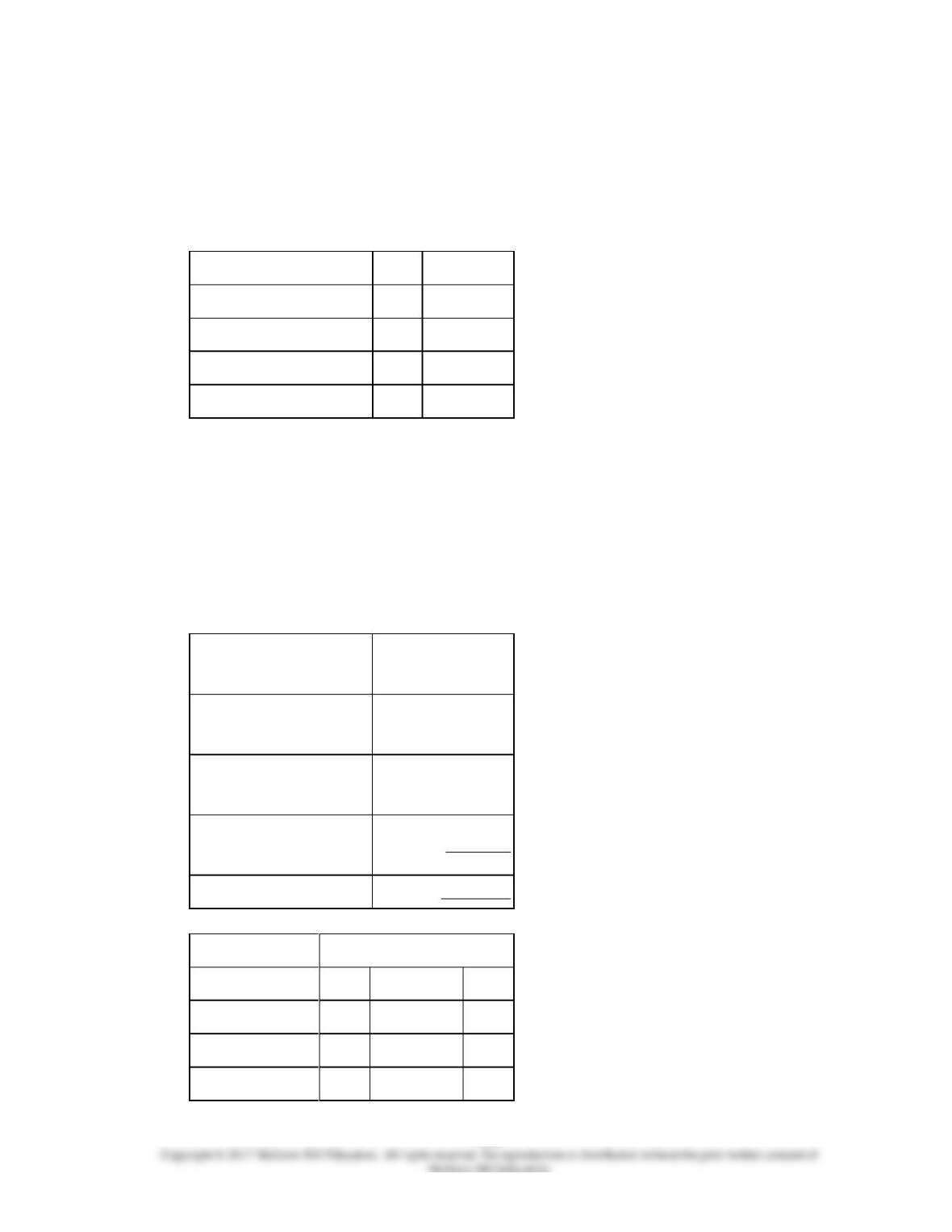

Russell Manufacturing Corporation has a traditional costing system in which it applies

manufacturing overhead to its products using a predetermined overhead rate based on

direct labor-hours (DLHs). The company has two products, Slow and Fast, about which it

has provided the following data:

Slow

Fast

Direct materials

per unit

$14.10

$43.40

Direct labor per

unit

$3.20

$25.60

Direct labor-

hours per unit

0.20

1.60

Annual

production

30,000

15,000

The company’s estimated total manufacturing overhead for the year is $1,526,700 and the

company’s estimated total direct labor-hours for the year is 30,000.

The company is considering using a variation of activity-based costing to determine its

unit product costs for external reports. Data for this proposed activity-based costing

system appear below:

Activities and Activity

Measures

Estimated

Overhead Cost

Assembling products

(DLHs)

$720,000

Preparing batches

(batches)

362,700

Product support (product

variations)

444,000

Total

$1,526,700

Expected Activity

Slow

Fast

Total

DLHs

6,000

24,000

30,000

Batches

1,380

1,410

2,790

Product variations

570

540

1,110

Total direct labor-hours

9-83

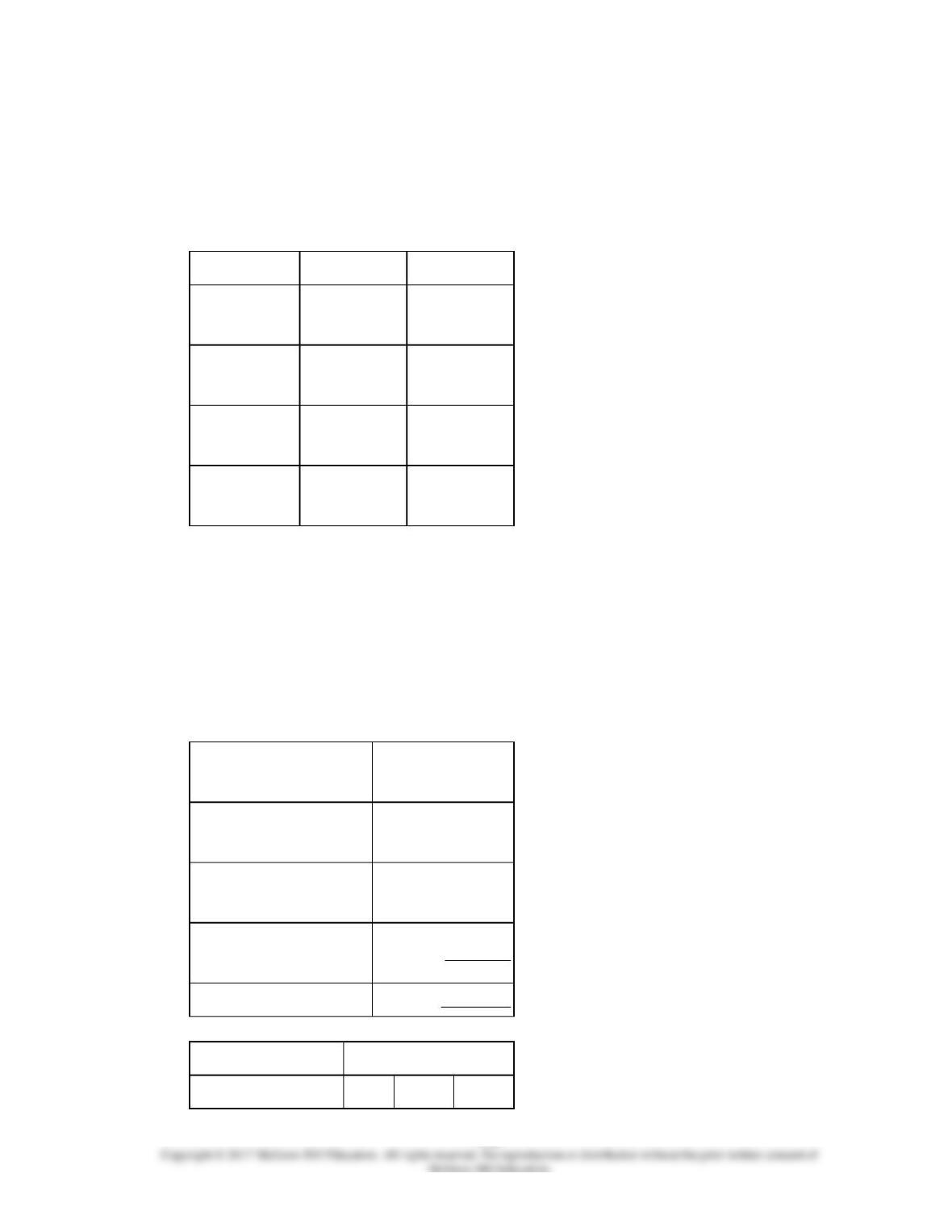

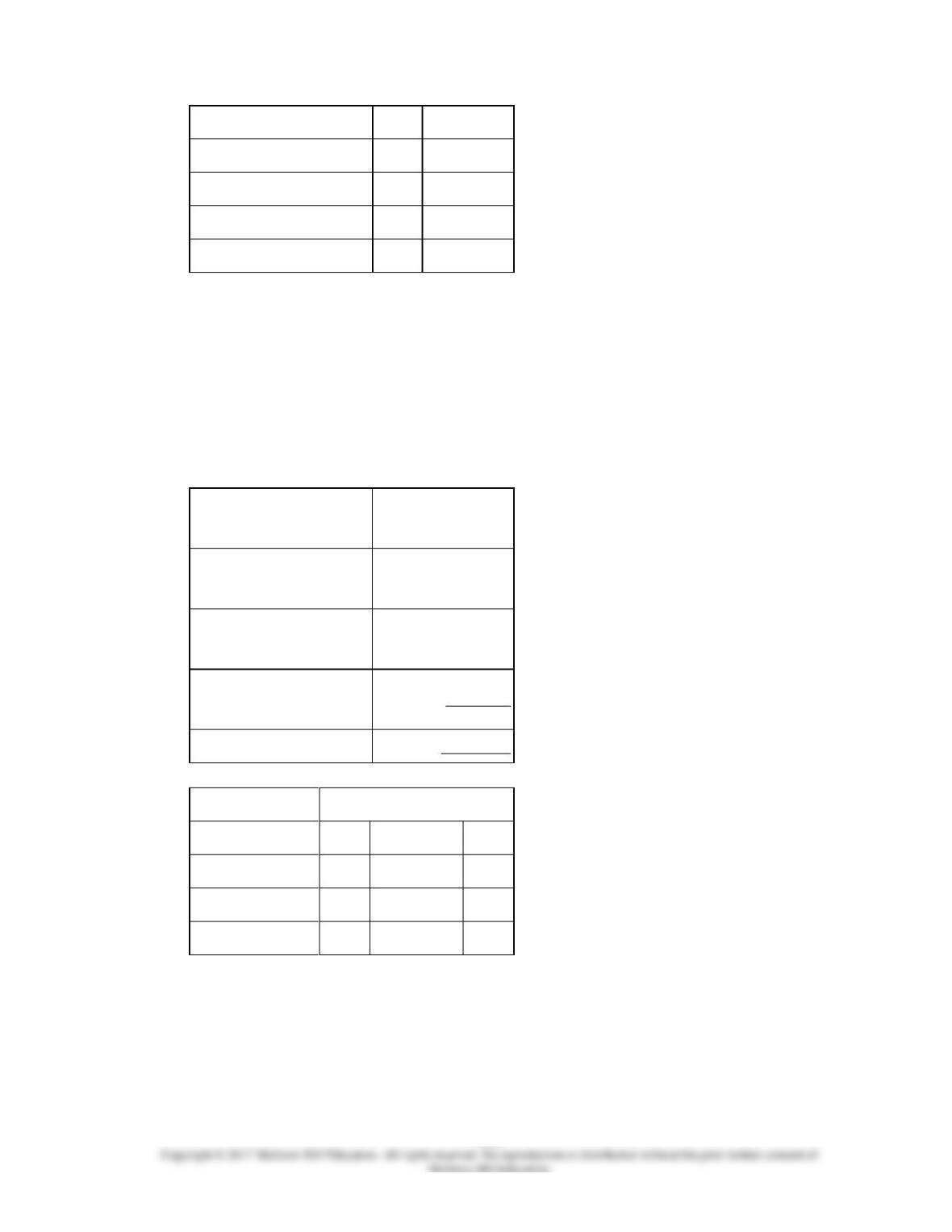

99.

Russell Manufacturing Corporation has a traditional costing system in which it applies

manufacturing overhead to its products using a predetermined overhead rate based on

direct labor-hours (DLHs). The company has two products, Slow and Fast, about which it

has provided the following data:

Slow

Fast

Direct materials

per unit

$14.10

$43.40

Direct labor per

unit

$3.20

$25.60

Direct labor-

hours per unit

0.20

1.60

Annual

production

30,000

15,000

The company’s estimated total manufacturing overhead for the year is $1,526,700 and the

company’s estimated total direct labor-hours for the year is 30,000.

The company is considering using a variation of activity-based costing to determine its

unit product costs for external reports. Data for this proposed activity-based costing

system appear below:

Activities and Activity

Measures

Estimated

Overhead Cost

Assembling products

(DLHs)

$720,000

Preparing batches

(batches)

362,700

Product support (product

variations)

444,000

Total

$1,526,700

Expected Activity

Slow

Fast

Total

9-84

DLHs

6,000

24,000

30,000

Batches

1,380

1,410

2,790

Product variations

570

540

1,110

9-86

100.

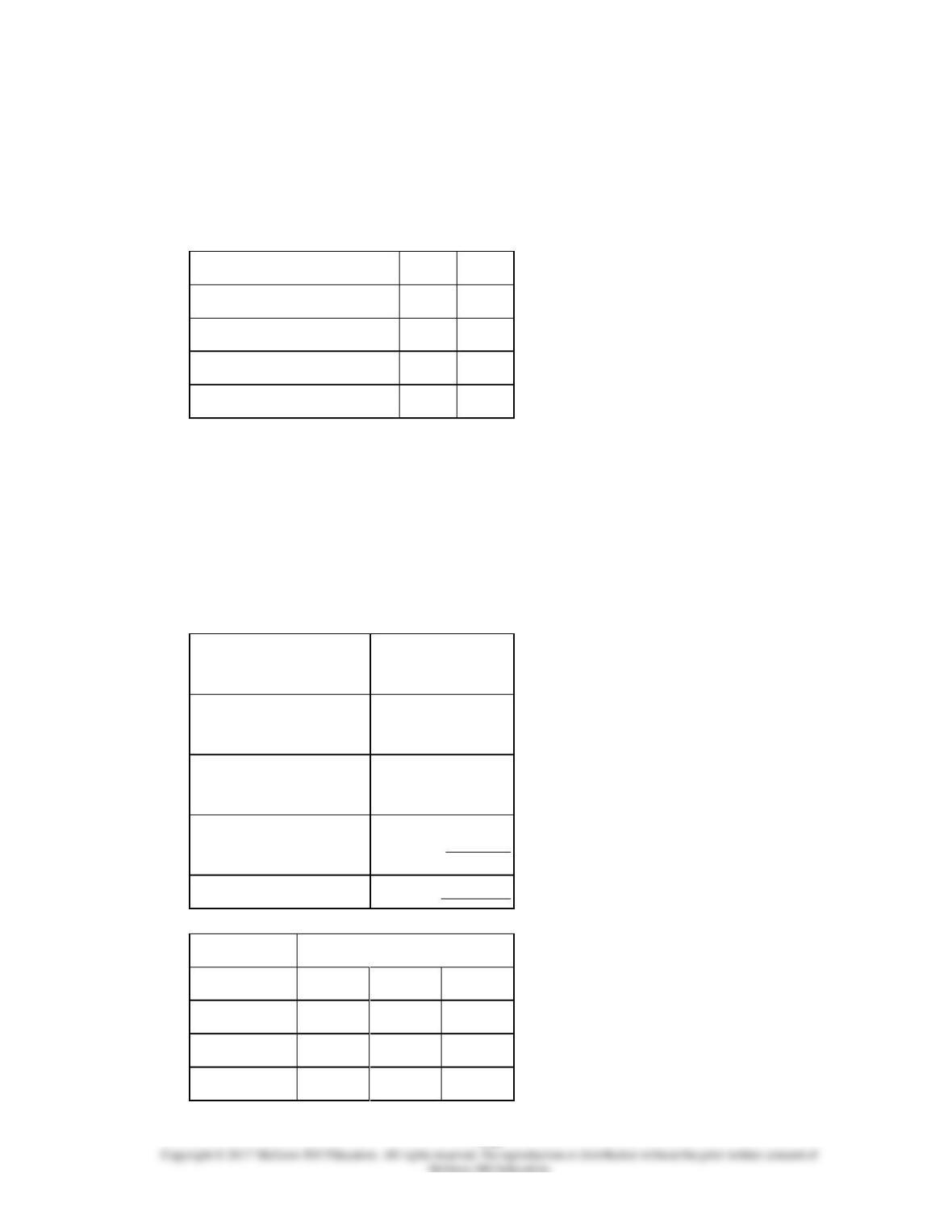

Upton Manufacturing Corporation has a traditional costing system in which it applies

manufacturing overhead to its products using a predetermined overhead rate based on

direct labor-hours (DLHs). The company has two products, Long and Short, about which it

has provided the following data:

Long

Short

Direct materials per unit

$14.20

$48.30

Direct labor per unit

$16.80

$50.40

Direct labor-hours per unit

0.80

2.40

Annual production

45,000

10,000

The company’s estimated total manufacturing overhead for the year is $3,170,400 and the

company’s estimated total direct labor-hours for the year is 60,000.

The company is considering using a variation of activity-based costing to determine its

unit product costs for external reports. Data for this proposed activity-based costing

system appear below:

Activities and Activity

Measures

Estimated

Overhead Cost

Direct labor support

(DLHs)

$1,740,000

Setting up machines

(setups)

422,400

Part administration (part

types)

1,008,000

Total

$3,170,400

Expected Activity

Long

Short

Total

DLHs

36,000

24,000

60,000

Setups

1,140

1,500

2,640

Part types

900

2,460

3,360

9-87

101.

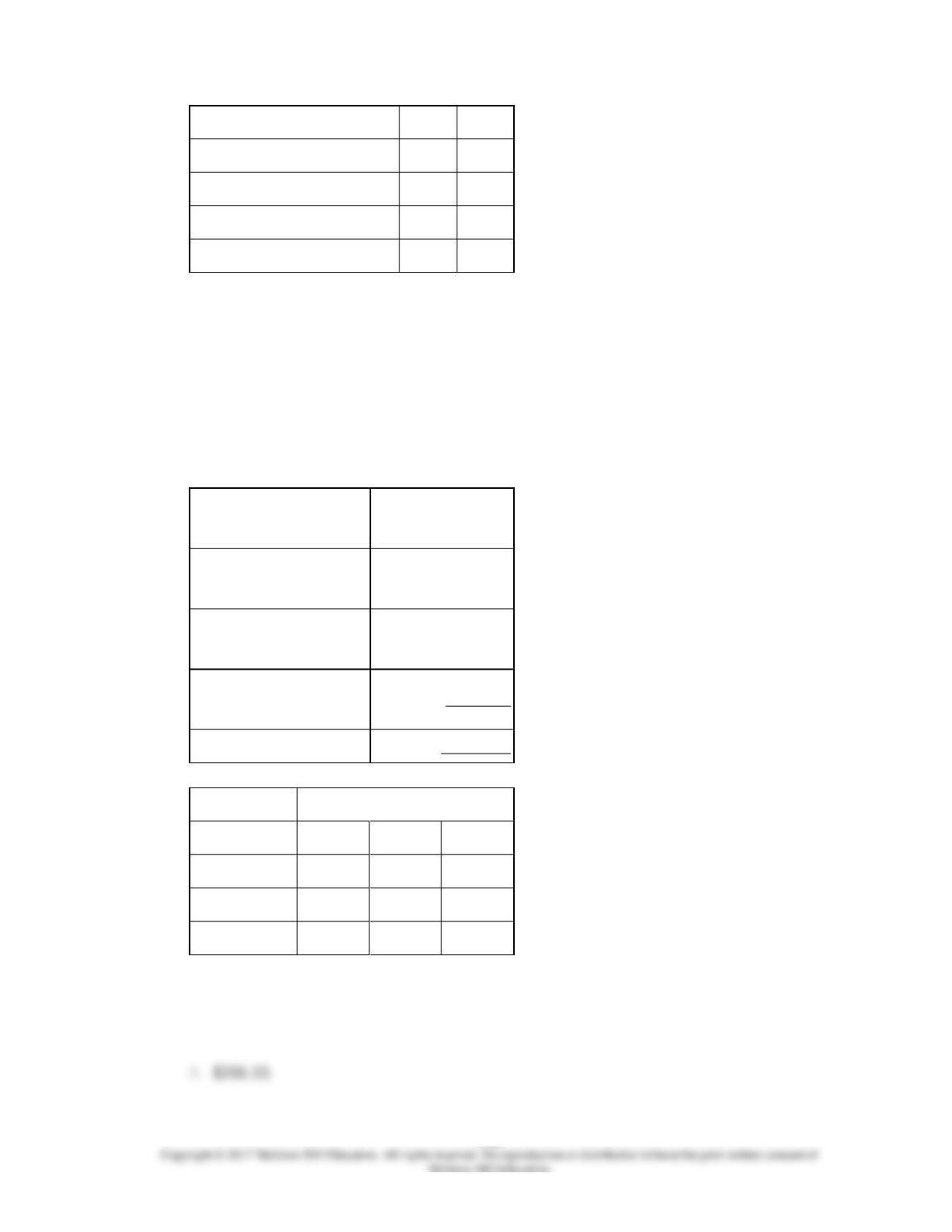

Upton Manufacturing Corporation has a traditional costing system in which it applies

manufacturing overhead to its products using a predetermined overhead rate based on

direct labor-hours (DLHs). The company has two products, Long and Short, about which it

has provided the following data:

9-88

Long

Short

Direct materials per unit

$14.20

$48.30

Direct labor per unit

$16.80

$50.40

Direct labor-hours per unit

0.80

2.40

Annual production

45,000

10,000

The company’s estimated total manufacturing overhead for the year is $3,170,400 and the

company’s estimated total direct labor-hours for the year is 60,000.

The company is considering using a variation of activity-based costing to determine its

unit product costs for external reports. Data for this proposed activity-based costing

system appear below:

Activities and Activity

Measures

Estimated

Overhead Cost

Direct labor support

(DLHs)

$1,740,000

Setting up machines

(setups)

422,400

Part administration (part

types)

1,008,000

Total

$3,170,400

Expected Activity

Long

Short

Total

DLHs

36,000

24,000

60,000

Setups

1,140

1,500

2,640

Part types

900

2,460

3,360

9-91

102.

Cassidy Manufacturing Corporation has a traditional costing system in which it applies

manufacturing overhead to its products using a predetermined overhead rate based on

direct labor-hours (DLHs). The company has two products, VIP and Kommander, about

which it has provided the following data:

VIP

Kommander

Direct materials per unit

$27.50

$62.10

Direct labor per unit

$15.60

$52.00

Direct labor-hours per unit

0.60

2.00

Annual production

40,000

15,000

The company’s estimated total manufacturing overhead for the year is $2,449,440 and the

company’s estimated total direct labor-hours for the year is 54,000.

The company is considering using a variation of activity-based costing to determine its

unit product costs for external reports. Data for this proposed activity-based costing

system appear below:

Activities and Activity

Measures

Estimated

Overhead Cost

Assembling products

(DLHs)

$918,000

Preparing batches

(batches)

397,440

Product support (product

variations)

1,134,000

Total

$2,449,440

Expected Activity

VIP

Kommander

Total

DLHs

24,000

30,000

54,000

Batches

1,458

1,026

2,484

Product variations

2,592

1,188

3,780

9-92

103.

Cassidy Manufacturing Corporation has a traditional costing system in which it applies

manufacturing overhead to its products using a predetermined overhead rate based on

direct labor-hours (DLHs). The company has two products, VIP and Kommander, about

which it has provided the following data:

9-93

VIP

Kommander

Direct materials per unit

$27.50

$62.10

Direct labor per unit

$15.60

$52.00

Direct labor-hours per unit

0.60

2.00

Annual production

40,000

15,000

The company’s estimated total manufacturing overhead for the year is $2,449,440 and the

company’s estimated total direct labor-hours for the year is 54,000.

The company is considering using a variation of activity-based costing to determine its

unit product costs for external reports. Data for this proposed activity-based costing

system appear below:

Activities and Activity

Measures

Estimated

Overhead Cost

Assembling products

(DLHs)

$918,000

Preparing batches

(batches)

397,440

Product support (product

variations)

1,134,000

Total

$2,449,440

Expected Activity

VIP

Kommander

Total

DLHs

24,000

30,000

54,000

Batches

1,458

1,026

2,484

Product variations

2,592

1,188

3,780

The unit product cost of Product Kommander under the activity-based costing system is

closest to:

9-94

104.

Miracle Consulting Corporation has its headquarters in Chicago and operates from three

branch offices in Portland, Dallas, and Miami. Two of the company’s activity cost pools are

General Service and Research Service. These costs are allocated to the three branch

offices using an activity-based costing system. Information for next year follows:

Activity Cost

Pool

Activity Measure

Estimated

Cost

General

service

% of time devoted

to branch

$700,000

Research

service

Computer time

$140,000

Estimated branch data for next year is as follows:

% of time

Computer time

Portland

30%

200,000 minutes

Dallas

60%

150,000 minutes

Miami

10%

50,000 minutes

How much of the headquarters cost allocation should the Dallas office expect to receive

next year?

Total

105.

A basic assumption of activity based costing (ABC) is that:

106.

In an activity-based costing (ABC) system, what should be used to assign departmental

manufacturing overhead costs to products produces in varying lot sizes?

107.

Mission Company is preparing its annual profit plan. As part of its analysis of the

profitability of individual products, the controller estimates the amount of overhead that

should be allocated to the individual product lines from the information provided below.

(CMA based)

Wall

Mirrors

Specialty

Windows

Units Produced

40

20

Material moves per

product line

5

15

Direct labor hours per

product line

200

300

Budgeted material handling costs: $50,000

Under a traditional costing system that allocates overhead on the basis of direct labor

hours, the materials handling costs allocated to one unit of wall mirrors would be:

108.

Mission Company is preparing its annual profit plan. As part of its analysis of the

profitability of individual products, the controller estimates the amount of overhead that

should be allocated to the individual product lines from the information provided below.

(CMA based)

Wall

Mirrors

Specialty

Windows

Units Produced

40

20

Material moves per

product line

5

15

Direct labor hours per

product line

200

300

Budgeted material handling costs: $50,000

Under a traditional costing system that allocates overhead on the basis of direct labor

hours, the materials handling costs allocated to one unit of specialty windows would be:

109.

Mission Company is preparing its annual profit plan. As part of its analysis of the

profitability of individual products, the controller estimates the amount of overhead that

should be allocated to the individual product lines from the information provided below.

(CMA based)

Wall

Mirrors

Specialty

Windows

Units Produced

40

20

Material moves per

product line

5

15

Direct labor hours per

product line

200

300

Budgeted material handling costs: $50,000

Under an activity-based costing (ABC) system, the materials handling costs allocated to

one unit of wall mirrors would be: