86.

Allure Company manufactures and distributes two products, M and XY. Overhead costs

are currently allocated using the number of units produced as the allocation base. The

controller has recommended changing to an activity-based costing (ABC) system. She has

collected the following information:

Activity

Cost

Driver

Amount

M

XY

Production

setups

Number of

setups

$82,000

8

12

Material

handling

Number of

parts

48,000

56

24

Packaging

costs

Number of

units

130,000

80,000

50,000

$260,000

87.

Allure Company manufactures and distributes two products, M and XY. Overhead costs

are currently allocated using the number of units produced as the allocation base. The

controller has recommended changing to an activity-based costing (ABC) system. She has

collected the following information:

Activity

Cost

Driver

Amount

M

XY

Production

setups

Number of

setups

$82,000

8

12

Material

handling

Number of

parts

48,000

56

24

Packaging

costs

Number of

units

130,000

80,000

50,000

$260,000

What is the total overhead per unit allocated to Product M using activity-based costing

(ABC)?

88.

Allure Company manufactures and distributes two products, M and XY. Overhead costs

are currently allocated using the number of units produced as the allocation base. The

controller has recommended changing to an activity-based costing (ABC) system. She has

collected the following information:

Activity

Cost

Driver

Amount

M

XY

Production

setups

Number of

setups

$82,000

8

12

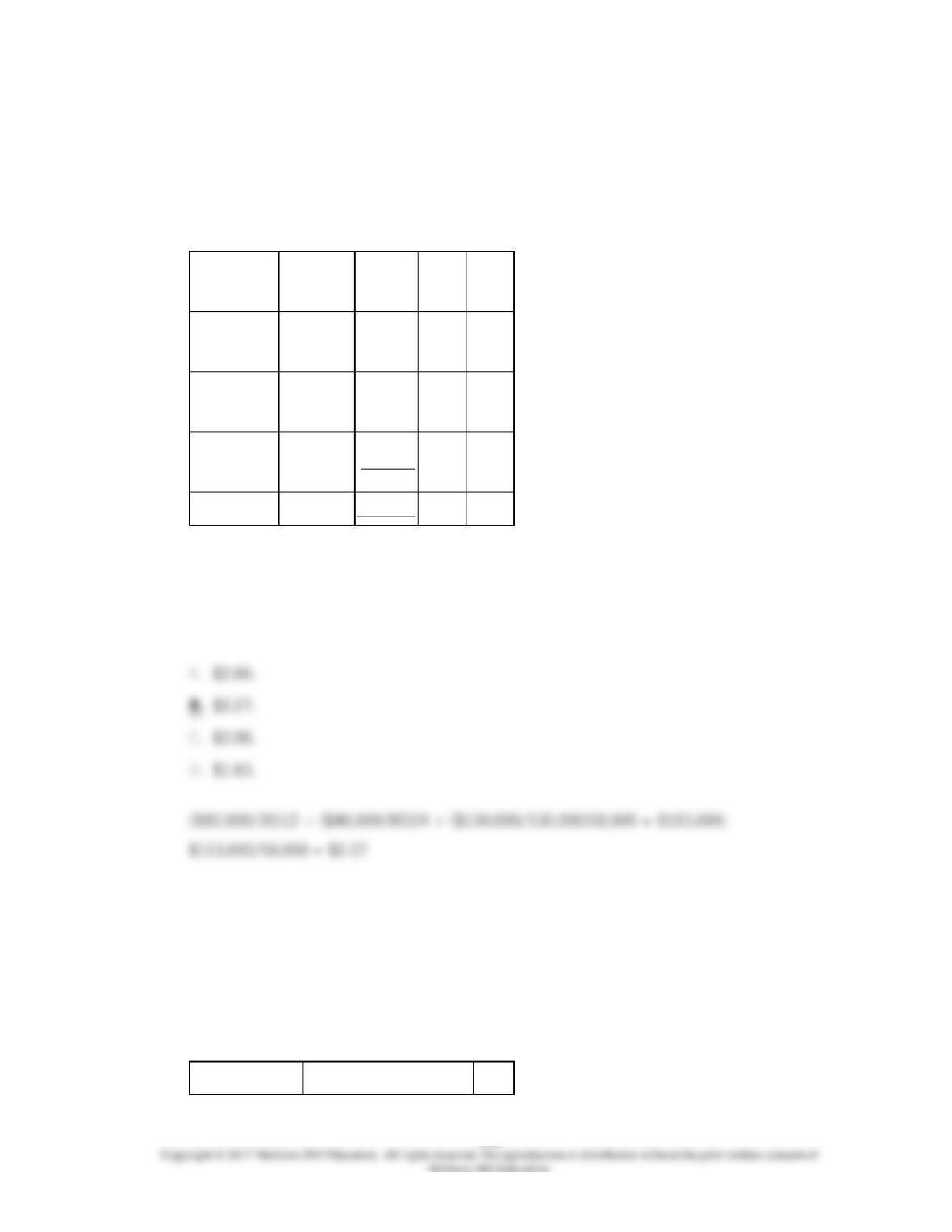

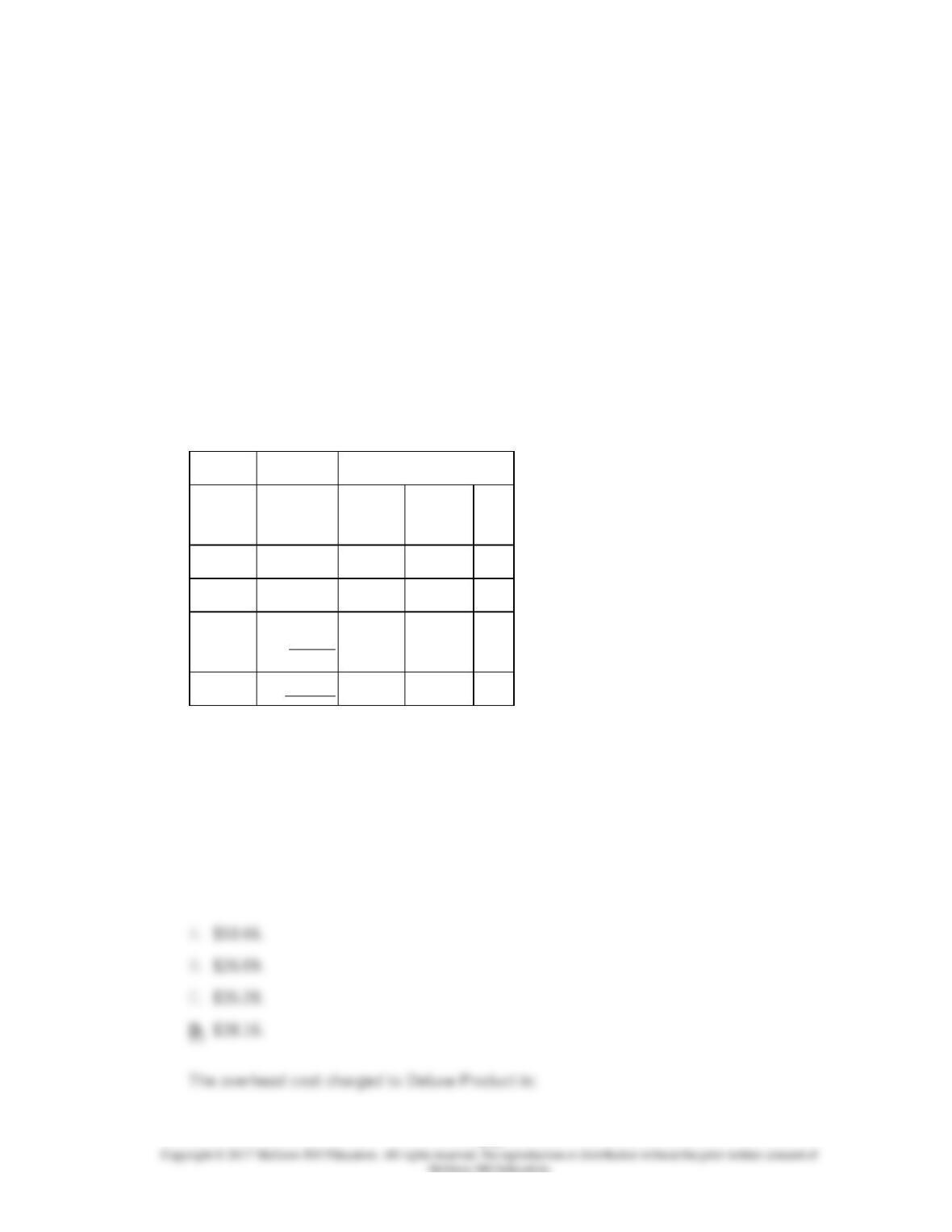

Material

handling

Number of

parts

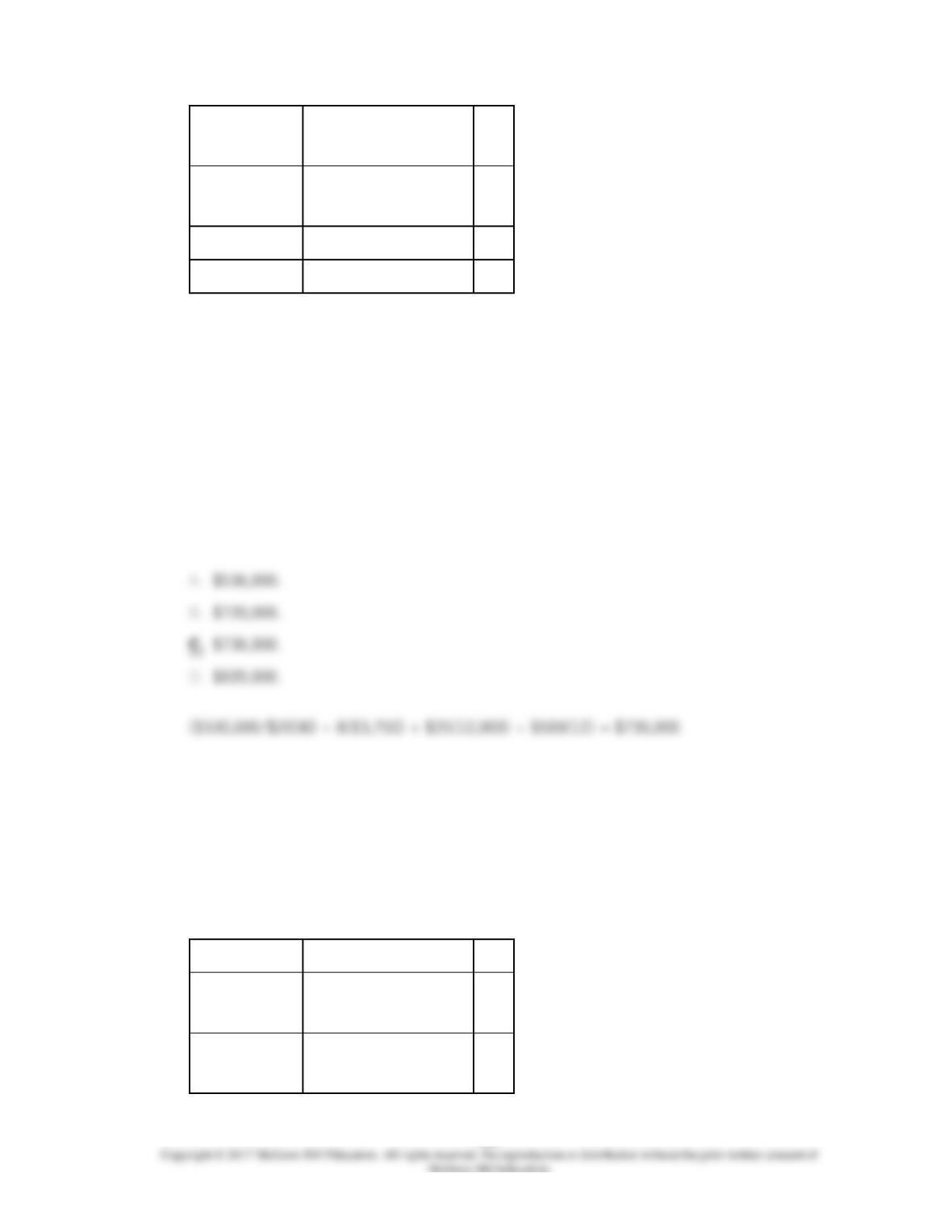

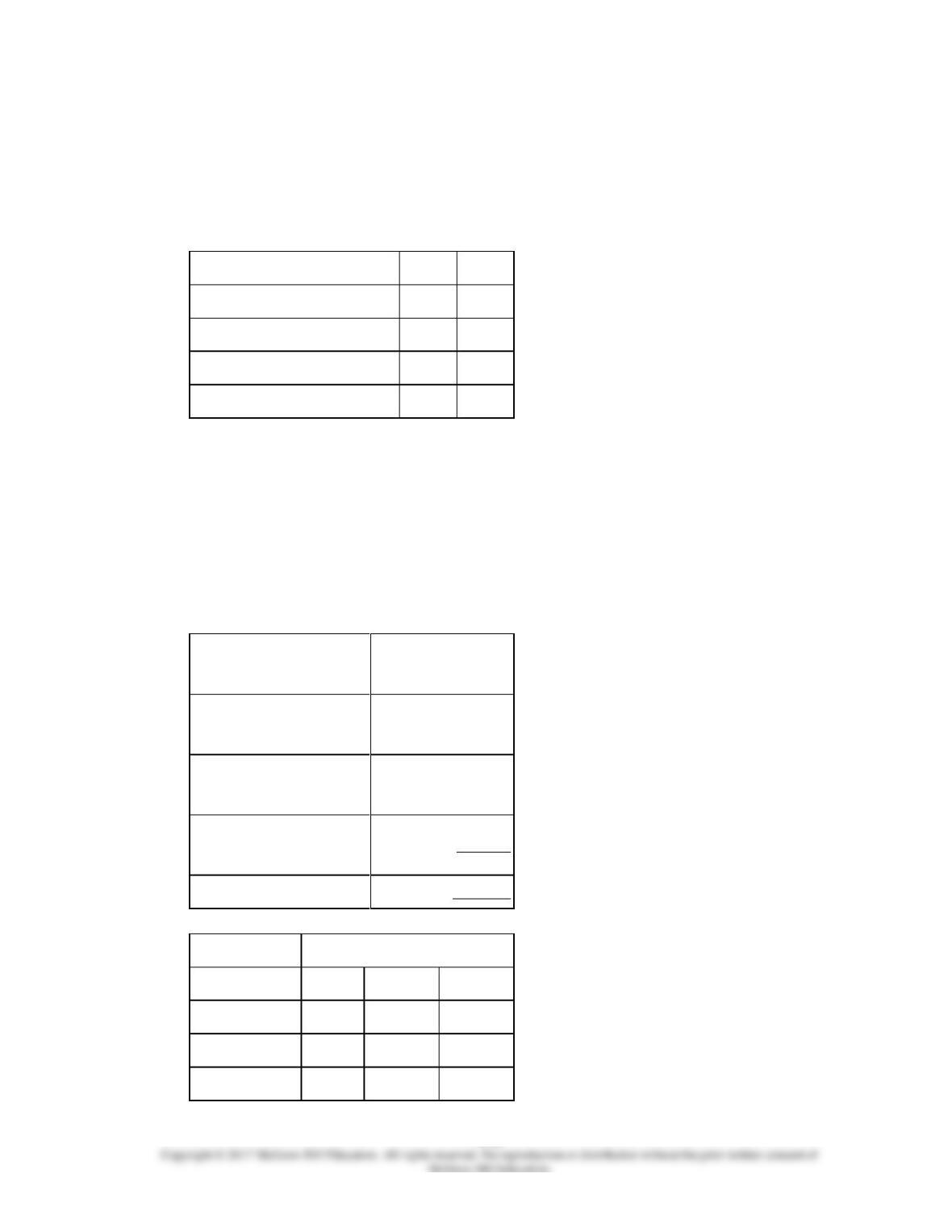

48,000

56

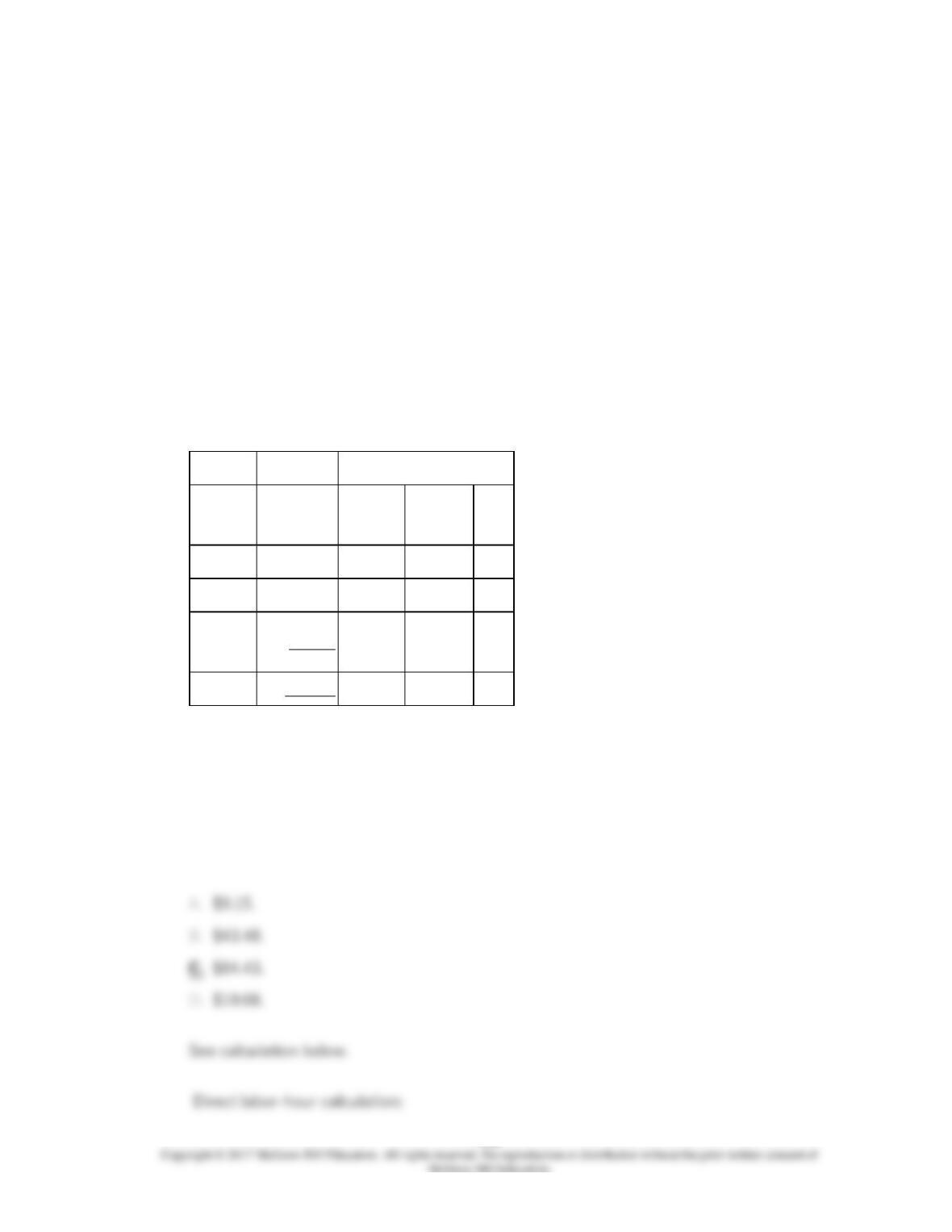

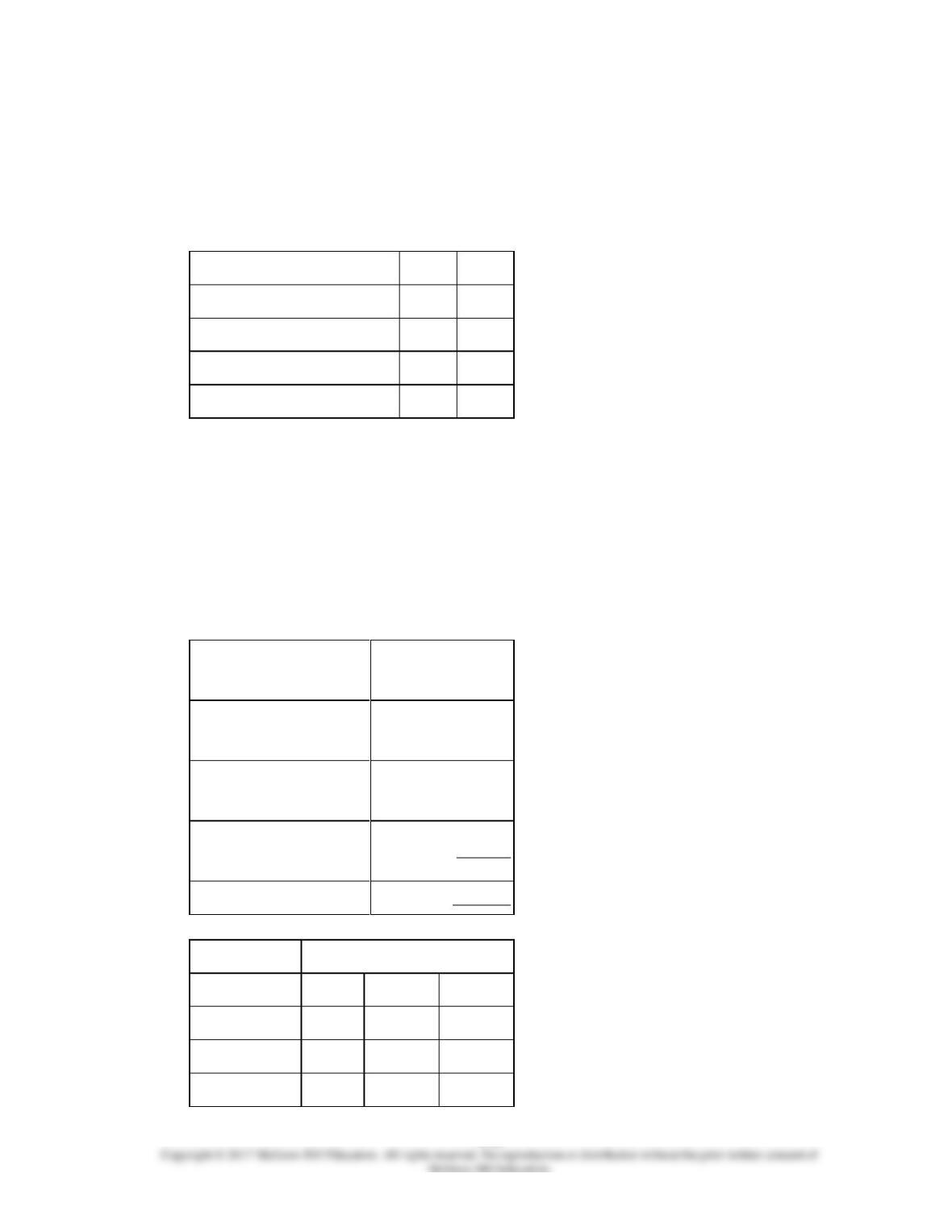

24

Packaging

costs

Number of

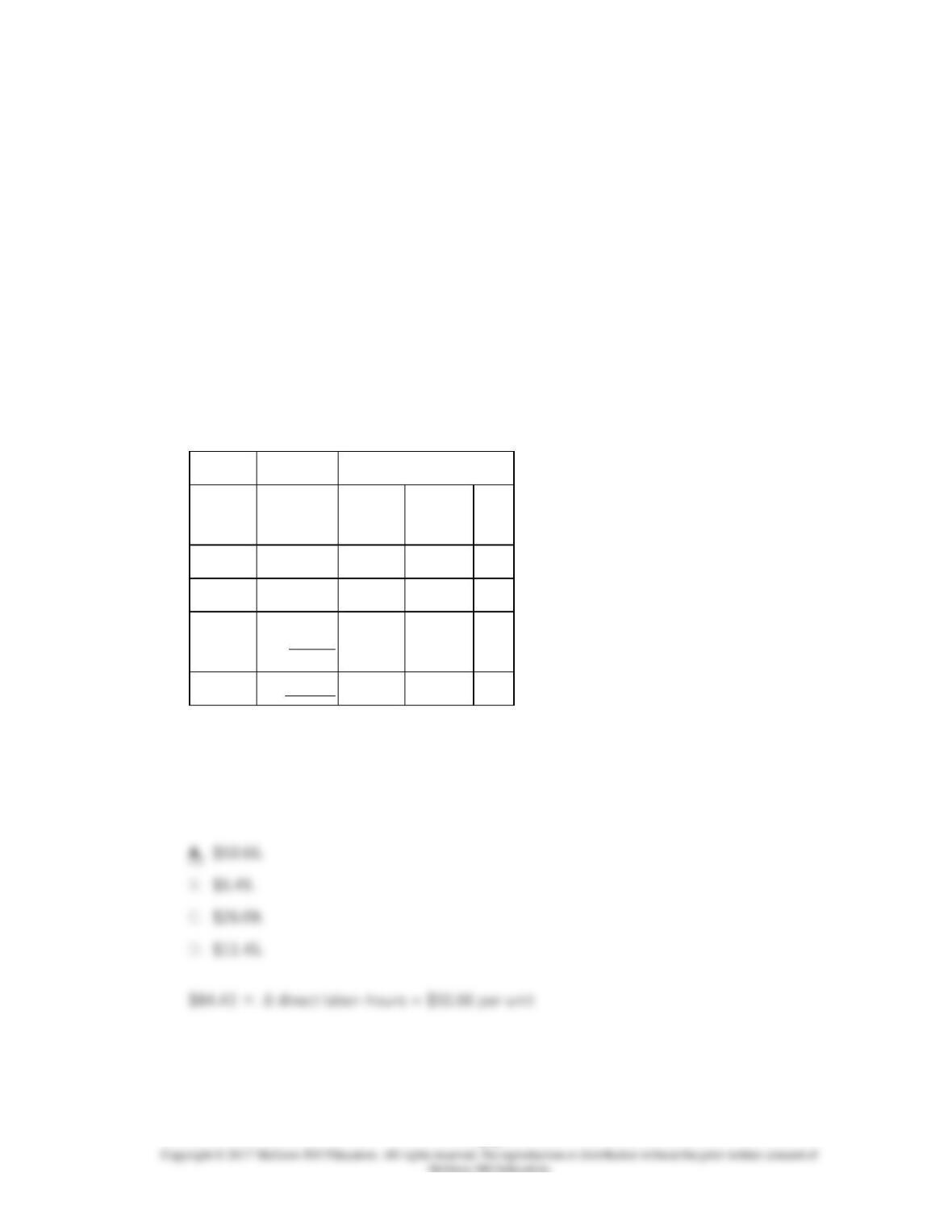

units

130,000

80,000

50,000

$260,000

9-66

89.

Allure Company manufactures and distributes two products, M and XY. Overhead costs

are currently allocated using the number of units produced as the allocation base. The

controller has recommended changing to an activity-based costing (ABC) system. She has

collected the following information:

Activity

Cost

Driver

Amount

M

XY

Production

setups

Number of

setups

$82,000

8

12

Material

handling

Number of

parts

48,000

56

24

Packaging

costs

Number of

units

130,000

80,000

50,000

$260,000

90.

The Mega Construction Company recently switched to activity-based costing (ABC) from

the department allocation method. The department method allocated overhead costs at a

rate of $60 per machine hour. The cost accountant for the Finishing Department has

gathered the following data:

Activity

Cost Drivers

Rate

9-67

Material

handling

Tons of material handled

$80

Machine setups

Number of production

runs

3,750

Utilities

Machine hours

25

Quality control

Number of inspections

500

91.

The Mega Construction Company recently switched to activity-based costing (ABC) from

the department allocation method. The department method allocated overhead costs at a

rate of $60 per machine hour. The cost accountant for the Finishing Department has

gathered the following data:

Activity

Cost Drivers

Rate

Material

handling

Tons of material handled

$80

Machine setups

Number of production

runs

3,750

Utilities

Machine hours

25

Quality control

Number of inspections

500

9-69

92.

Markham Company makes two products: Basic Product and Deluxe Product. Annual

production and sales are 1,700 units of Basic Product and 1,100 units of Deluxe Product.

The company has traditionally used direct labor-hours as the basis for applying all

manufacturing overhead to products. Basic Product requires 0.3 direct labor hours per unit

and Deluxe Product requires 0.6 direct labor hours per unit. The total estimated overhead

for next period is $98,785.

The company is considering switching to an activity-based costing system for the purpose

of computing unit product costs for external reports. The new activity-based costing

system would have three overhead activity cost pools—Activity 1, Activity 2, and General

Factory—with estimated overhead costs and expected activity as follows:

Estimated

Expected Activity

Activity

Cost Pool

Overhead

Costs

Basic

Product

Deluxe

Product

Total

Activity 1

$30,528

1,000

600

1,600

Activity 2

17,385

1,700

200

1,900

General

Factory

50,872

510

660

1,170

Total

$98,785

9-71

93.

Markham Company makes two products: Basic Product and Deluxe Product. Annual

production and sales are 1,700 units of Basic Product and 1,100 units of Deluxe Product.

The company has traditionally used direct labor-hours as the basis for applying all

manufacturing overhead to products. Basic Product requires 0.3 direct labor hours per unit

and Deluxe Product requires 0.6 direct labor hours per unit. The total estimated overhead

for next period is $98,785.

The company is considering switching to an activity-based costing system for the purpose

of computing unit product costs for external reports. The new activity-based costing

system would have three overhead activity cost pools—Activity 1, Activity 2, and General

Factory—with estimated overhead costs and expected activity as follows:

Estimated

Expected Activity

Activity

Cost Pool

Overhead

Costs

Basic

Product

Deluxe

Product

Total

Activity 1

$30,528

1,000

600

1,600

Activity 2

17,385

1,700

200

1,900

General

Factory

50,872

510

660

1,170

Total

$98,785

94.

Markham Company makes two products: Basic Product and Deluxe Product. Annual

9-72

production and sales are 1,700 units of Basic Product and 1,100 units of Deluxe Product.

The company has traditionally used direct labor-hours as the basis for applying all

manufacturing overhead to products. Basic Product requires 0.3 direct labor hours per unit

and Deluxe Product requires 0.6 direct labor hours per unit. The total estimated overhead

for next period is $98,785.

The company is considering switching to an activity-based costing system for the purpose

of computing unit product costs for external reports. The new activity-based costing

system would have three overhead activity cost pools—Activity 1, Activity 2, and General

Factory—with estimated overhead costs and expected activity as follows:

Estimated

Expected Activity

Activity

Cost Pool

Overhead

Costs

Basic

Product

Deluxe

Product

Total

Activity 1

$30,528

1,000

600

1,600

Activity 2

17,385

1,700

200

1,900

General

Factory

50,872

510

660

1,170

Total

$98,785

9-74

95.

Markham Company makes two products: Basic Product and Deluxe Product. Annual

production and sales are 1,700 units of Basic Product and 1,100 units of Deluxe Product.

The company has traditionally used direct labor-hours as the basis for applying all

manufacturing overhead to products. Basic Product requires 0.3 direct labor hours per unit

and Deluxe Product requires 0.6 direct labor hours per unit. The total estimated overhead

for next period is $98,785.

The company is considering switching to an activity-based costing system for the purpose

of computing unit product costs for external reports. The new activity-based costing

system would have three overhead activity cost pools—Activity 1, Activity 2, and General

Factory—with estimated overhead costs and expected activity as follows:

Estimated

Expected Activity

Activity

Cost Pool

Overhead

Costs

Basic

Product

Deluxe

Product

Total

Activity 1

$30,528

1,000

600

1,600

Activity 2

17,385

1,700

200

1,900

General

Factory

50,872

510

660

1,170

Total

$98,785

9-76

96.

Chang Manufacturing Corporation has a traditional costing system in which it applies

manufacturing overhead to its products using a predetermined overhead rate based on

direct labor-hours (DLHs). The company has two products, Plain and Fancy, about which

it has provided the following data:

Plain

Fancy

Direct materials per unit

$24.50

$59.30

Direct labor per unit

$5.00

$25.00

Direct labor-hours per unit

0.20

1.00

Annual production

45,000

15,000

The company’s estimated total manufacturing overhead for the year is $985,440 and the

company’s estimated total direct labor-hours for the year is 24,000.

The company is considering using a variation of activity-based costing to determine its

unit product costs for external reports. Data for this proposed activity-based costing

system appear below:

Activities and Activity

Measures

Estimated

Overhead Cost

Supporting direct labor

(DLHs)

$384,000

Setting up machines

(setups)

255,840

Parts administration (part

types)

345,600

Total

$985,440

Expected Activity

Plain

Fancy

Total

DLHs

9,000

15,000

24,000

Setups

1,032

936

1,968

Part types

624

240

864

9-78

97.

Chang Manufacturing Corporation has a traditional costing system in which it applies

manufacturing overhead to its products using a predetermined overhead rate based on

direct labor-hours (DLHs). The company has two products, Plain and Fancy, about which

it has provided the following data:

Plain

Fancy

Direct materials per unit

$24.50

$59.30

Direct labor per unit

$5.00

$25.00

Direct labor-hours per unit

0.20

1.00

Annual production

45,000

15,000

The company’s estimated total manufacturing overhead for the year is $985,440 and the

company’s estimated total direct labor-hours for the year is 24,000.

The company is considering using a variation of activity-based costing to determine its

unit product costs for external reports. Data for this proposed activity-based costing

system appear below:

Activities and Activity

Measures

Estimated

Overhead Cost

Supporting direct labor

(DLHs)

$384,000

Setting up machines

(setups)

255,840

Parts administration (part

types)

345,600

Total

$985,440

Expected Activity

Plain

Fancy

Total

DLHs

9,000

15,000

24,000

Setups

1,032

936

1,968

Part types

624

240

864

9-79