Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

126)

Which of the following events would cause a bank to debit a depositor's account?

A)

There are deposits in transit on the account at month-end.

B)

The bank corrects an error from previous month by adding $75 to the depositor account.

C)

The depositor orders new checks through the bank at a cost of $50.

D)

There are outstanding checks drawn on the account at month-end.

E)

The bank collects a note receivable and related interest on the depositor's behalf.

127)

A seller (or provider) of goods or services to a business organization is known as a:

A)

Payee. B) Vendee. C) Creditor. D) Debtor. E) Vendor.

128)

The internal document prepared by a department manager that informs the purchasing department

of its merchandise needs and requests that the merchandise be purchased is the:

A)

Purchase order.

B)

Receiving report.

C)

Purchase requisition.

D)

Invoice approval.

E)

Invoice.

129)

The document that the purchasing department prepares and sends to the vendor to place an order is

called the:

A)

Purchase order.

B)

Invoice approval.

C)

Invoice.

D)

Purchase requisition.

E)

Receiving report.

130)

The itemized statement of goods prepared by a vendor listing the customer's name, items sold,

sales prices, and terms of the sale is called the:

A)

Purchase requisition.

B)

Invoice approval.

C)

Purchase order.

D)

Invoice.

E)

Receiving report.

131)

The internal document prepared to notify the appropriate persons that goods ordered have been

received, describing the quantities and condition of the goods is the:

A)

Purchase requisition.

B)

Invoice.

C)

Purchase order.

D)

Invoice approval.

E)

Receiving report.

132)

The checklist of steps necessary for approving an invoice for recording and payment, also known

as the check authorization, is the:

A)

Receiving report.

B)

Purchase order.

C)

Invoice approval.

D)

Invoice.

E)

Purchase requisition.

133)

A voucher system is a set of procedures and approvals:

A)

Designed to determine if the company is operating profitably.

B)

Used almost exclusively by small companies.

C)

Designed to eliminate the need for subsidiary ledgers.

D)

Used to ensure that the company sells on credit only to creditworthy customers.

E)

Designed to control cash disbursements and the acceptance of obligations.

65

134)

Internal controls are crucial to companies that convert from U.S. GAAP to IFRS because of all of

the following risks except:

A)

Ineffective communication of the change to investors, creditors, and others.

B)

Possible misstatement of financial information.

C)

Management's inability to certify the effectiveness of the controls.

D)

Possible fraud.

E)

Controls are significantly different across the globe.

135)

All of the following are considered effective cash management principles except:

A)

Keeping only necessary levels of assets.

B)

Planning expenditures.

C)

Delaying payment of liabilities until the last possible day.

D)

Encouraging collection of receivables by offering discounts for early payments.

E)

Retaining excess cash for unexpected expenditures.

136)

Ryan Company deposits all cash receipts on the day they are received and makes all cash payments

by check. Ryan's June bank statement shows $18,361 on deposit in the bank. Ryan's comparison of

the bank statement to its cash account revealed the following:

Deposit in transit

1,450

Outstanding checks

837

Additionally, a $29 check written and recorded by the company correctly was recorded by the bank

as a $92 deduction.

The adjusted cash balance per the bank records should be:

A) $18,974 B) $20,711 C) $19,037 D) $18,911 E) $16,137

137)

Clayborn Company deposits all cash receipts on the day they are received and makes all cash

payments by check. At the close of business on May 31, its Cash account shows a debit balance of

$17,025. Clayborn's May bank statement shows $15,800 on deposit in the bank. Determine the

adjusted cash balance using the following information:

Deposit in transit

$5,200

Outstanding checks

$4,600

Bank service fees, not yet recorded by company

$25

A NSF check from a customer, not yet recorded by the company

$600

The adjusted cash balance should be:

A) $17,000 B) $16,400 C) $16,425 D) $11,200 E) $21,000

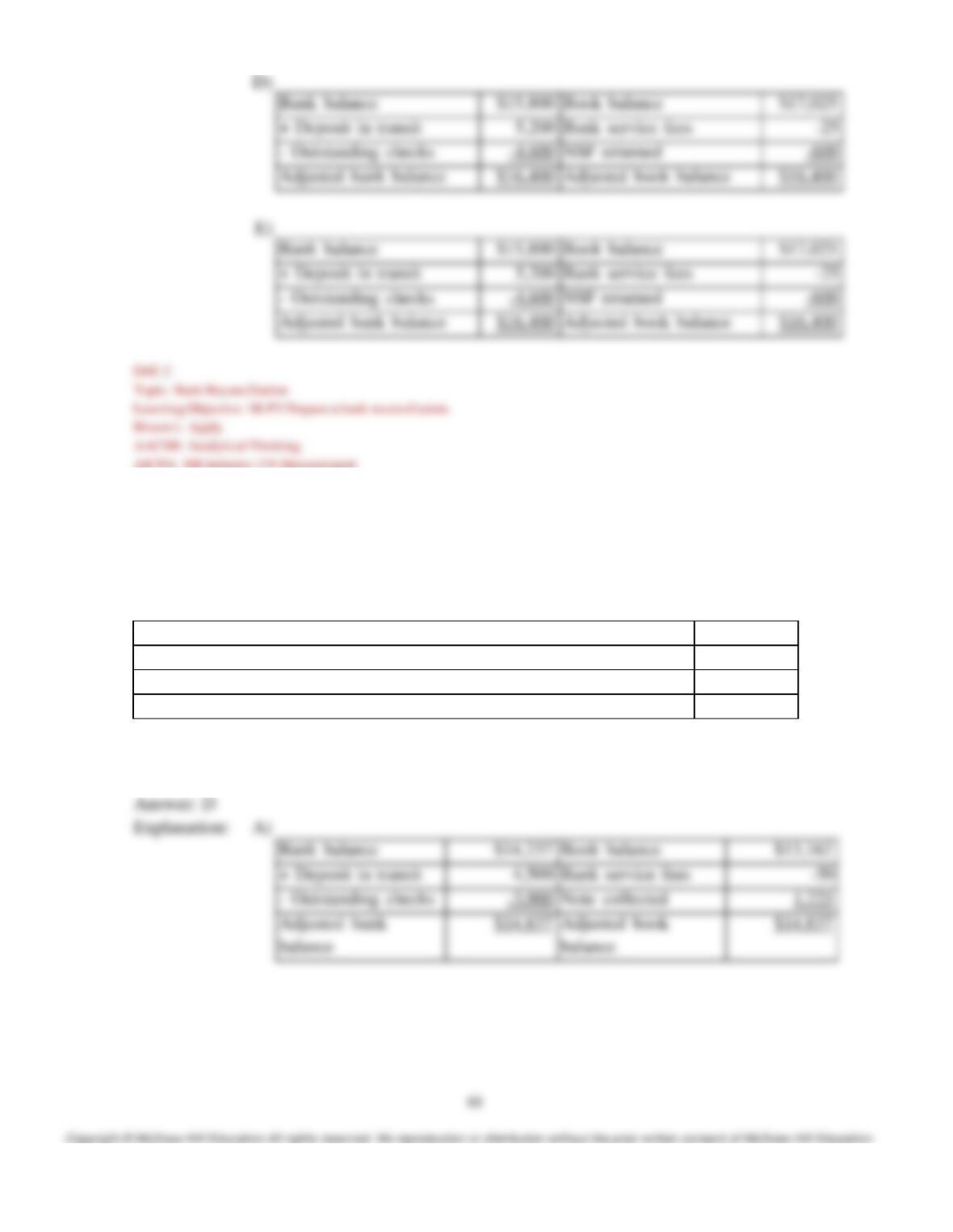

138)

Franklin Company deposits all cash receipts on the day they are received and makes all cash

payments by check. At the close of business on August 31, its Cash account shows a debit balance of

$13,162. Franklin's August bank statement shows $14,237 on deposit in the bank. Determine the

adjusted cash balance using the following information:

Deposit in transit

$4,500

Outstanding checks

$3,900

Bank service fees, not yet recorded by company

$50

The bank collected on a note receivable, not yet recorded by the company

$1,725

The adjusted cash balance should be:

A) $10,337 B) $18,737 C) $14,887 D) $14,837 E) $13,112

139)

Clayborn Company' bank reconciliation as of May 31 is shown below.

Bank balance

$15,800

Book balance

$17,025

+ Deposit in transit

5,200

Bank service fees

-25

- Outstanding checks

-4,600

NSF returned

-600

Adjusted bank balance

$16,400

Adjusted book balance

$16,400

One of the adjusting journal entries that Clayborn must record as a result of the bank reconciliation

includes:

A)

A credit to Cash of $4,600

B)

A debit to Cash of $625

C)

A credit to Cash of $600

D)

A debit to cash of $25

E)

A debit to Cash of $5,200

140)

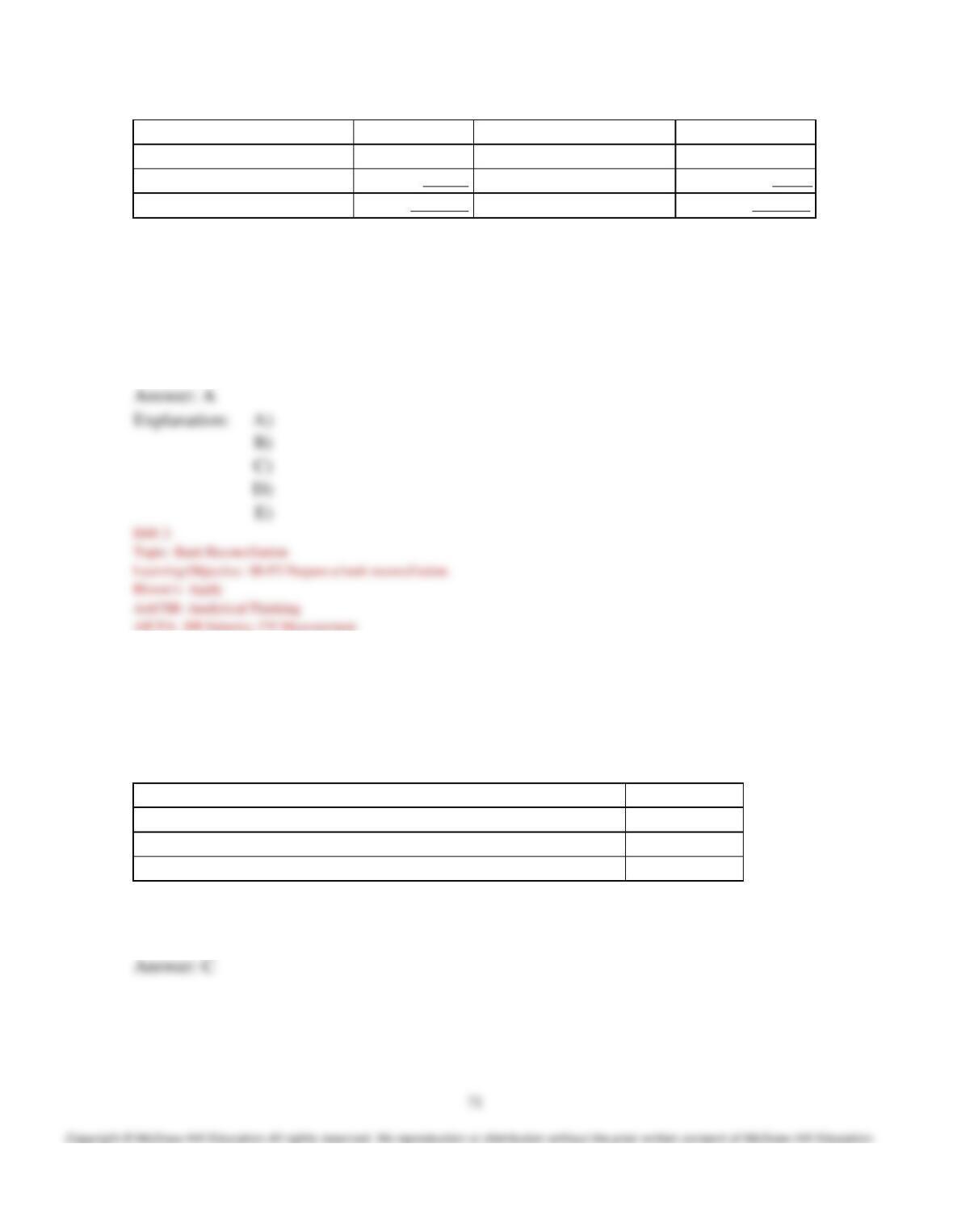

Franklin Company's bank reconciliation as of August 31 is shown below.

Bank balance

$14,237

Book balance

$13,162

+ Deposit in transit

4,500

Bank service fees

-50

- Outstanding checks

-3,900

Note collected

1,725

Adjusted bank balance

$14,837

Adjusted book balance

$14,837

The adjusting journal entries that Clayborn must record as a result of the bank reconciliation include:

A)

Debit Cash $1,725; credit Notes Receivable $1,725.

B)

Debit Cash $4,500; credit Sales $4,500.

C)

Debit Notes Receivable $1,725; credit Cash $1,725.

D)

Debit Misc. Expense $3,900; credit Cash $3,900.

E)

Debit Cash $50; credit Bank Service Fee Expense $50.

141)

Easton Co. deposits all cash receipts on the day they are received and makes all cash payments by

check. At the close of business on June 30, its Cash account shows a debit balance of $60,209.

Easton's June bank statement shows $58,349 on deposit in the bank. Determine the adjusted cash

balance using the following information:

Deposit in transit

$3,800

Outstanding checks

$1,925

Check printing fee, not yet recorded by company

$15

Interest earned on account, not yet recorded by the company

$30

The adjusted cash balance should be:

A) $62,149 B) $60,194 C) $60,224 D) $56,424 E) $60,239

142)

Great Falls Co.'s bank reconciliation as of February 28 is shown below.

Bank balance

$37,643

Book balance

$38,153

+ Deposit in transit

2,950

Note collection

+745

- Outstanding checks

-1,730

Check printing

-35

Adjusted bank balance

$38,863

Adjusted book balance

$38,863

One of the adjusting journal entries that Great Falls must record as a result of the bank reconciliation

includes:

A)

Debit Miscellaneous Expense $35; credit Accounts Payable $35.

B)

Debit Note Payable $745; credit Cash $745.

C)

Debit Cash $2,950; credit Accounts Receivable $2,950.

D)

Debit Cash $2,950; credit Sales $2,950.

E)

Debit Cash $745; credit Note Receivable $745.

143)

Havermill Co. establishes a $250 petty cash fund on September 1. On September 30, the fund is

replenished. The accumulated receipts on that date represent $73 for Office Supplies, $137 for

merchandise inventory, and $22 for miscellaneous expenses. The fund has a balance of $18. On

October 1, the accountant determines that the fund should be increased by $50. The journal entry to

record the establishment of the fund on September 1 is:

A)

Debit Miscellaneous Expense $250; credit Cash $250.

B)

Debit Cash $250; credit Petty Cash $250.

C)

Debit Cash $250; credit Accounts Payable $250.

D)

Debit Petty Cash $250; credit Accounts Payable $250.

E)

Debit Petty Cash $250; credit Cash $250.

144)

Havermill Co. establishes a $250 petty cash fund on September 1. On September 30, the fund is

replenished. The accumulated receipts on that date represent $73 for Office Supplies, $137 for

merchandise inventory, and $22 for miscellaneous expenses. The fund has a balance of $18. On

October 1, the accountant determines that the fund should be increased by $50. The journal entry to

record the reimbursement of the fund on September 30 includes a:

A)

Credit to Cash for $250.

B)

Credit to Cash for $18.

C)

Debit to Office Supplies for $73.

D)

Debit Petty Cash for $232.

E)

Credit to Merchandise Inventory for $137.

145)

Havermill Co. establishes a $250 petty cash fund on September 1. On September 30, the fund is

replenished. The accumulated receipts on that date represent $73 for Office Supplies, $137 for

merchandise inventory, and $22 for miscellaneous expenses. The fund has a balance of $18. On

October 1, the accountant determines that the fund should be increased by $50. The journal entry to

record the increase in the fund balance on October 1 is:

A)

Debit Cash $50; credit Petty Cash $50.

B)

Debit Petty Cash $50; credit Cash $50.

C)

Debit Petty Cash $300; credit Cash $300.

D)

Debit Miscellaneous Expense $50; credit Cash $50.

E)

Debit Petty Cash $50; credit Accounts Payable $50.

146)

Meng Co. maintains a $300 petty cash fund. On January 31, the fund is replenished. The

accumulated receipts on that date represent $80 for office supplies, $160 for merchandise

inventory, and $20 for miscellaneous expenses. There is a cash shortage of $8. Based on this

information, the amount of cash in the fund before the replenishment is:

A) $32. B) $40. C) $260. D) $300. E) $48.

147)

Meng Co. maintains a $300 petty cash fund. On January 31, the fund is replenished. The

accumulated receipts on that date represent $80 for office supplies, $160 for merchandise

inventory, and $20 for miscellaneous expenses. There is a cash shortage of $8. The journal entry to

replenish the fund on January 31 is:

A)

Dr. Office Supplies, $80; Dr. Merchandise inventory, $160; Dr. Miscellaneous expenses, $20;

Cr. Cash over and short, $8; Cr. Petty cash, $400.

B)

Dr. Office Supplies, $80; Dr. Merchandise inventory, $160; Dr. Miscellaneous expenses, $20;

Dr. Cash over and short, $8; Cr. Petty cash, $268.

C)

Dr. Office Supplies, $80; Dr. Merchandise inventory, $160; Dr. Miscellaneous expenses, $20;

Cr. Cash over and short, $8; Cr. Cash, $252.

D)

Dr. Office Supplies, $80; Dr. Merchandise inventory, $160; Dr. Miscellaneous expenses, $20;

Dr. Cash over and short, $8; Cr. Cash, $268.

E)

Dr. Office Supplies, $80; Dr. Merchandise inventory, $160; Dr. Miscellaneous expenses, $20;

Cr. Cash over and short, $8; Cr. Petty cash, $252.

148)

Pelcher Co. maintains a $400 petty cash fund. On January 31, the fund is replenished. The

accumulated receipts on that date represent $110 for office supplies, $140 for merchandise

inventory, and $70 for miscellaneous expenses. There is a cash overage of $4. Based on this

information, the amount of cash in the fund before the replenishment is:

A) $400. B) $320. C) $84. D) $76. E) $80.

149)

Pelcher Co. maintains a $400 petty cash fund. On January 31, the fund is replenished. The

accumulated receipts on that date represent $110 for office supplies, $140 for merchandise

inventory, and $70 for miscellaneous expenses. There is a cash overage of $4. The journal entry to

replenish the fund on January 31 is:

A)

Dr. Office Supplies, $110; Dr. Merchandise inventory, $140; Dr. Miscellaneous expenses,

$70; Cr. Cash over and short, $4; Cr. Cash, $316.

B)

Dr. Office Supplies, $110; Dr. Merchandise inventory, $140; Dr. Miscellaneous expenses,

$70; Cr. Cash over and short, $4; Cr. Petty cash, $316.

C)

Dr. Office Supplies, $110; Dr. Merchandise inventory, $140; Dr. Miscellaneous expenses,

$70; Dr. Cash over and short, $4; Cr. Cash, $324.

D)

Dr. Office Supplies, $110; Dr. Merchandise inventory, $140; Dr. Miscellaneous expenses,

$70; Dr. Cash over and short, $4; Cr. Petty cash, $324.

E)

Dr. Office Supplies, $110; Dr. Merchandise inventory, $140; Dr. Miscellaneous expenses,

$70; Dr. Cash over and short, $4; Cr. Petty cash, $400.

80

SHORT ANSWER QUESTIONS

150)

Match each of the following terms with the appropriate definitions.

1. Fundamental guidelines applicable to all companies established to minimize the risk of

fraud and theft and to increase the reliability and accuracy of the accounting records.

2. A method of initially recording purchases at the full invoice price ignoring any cash

discount.

3. A document used within the company to notify the appropriate persons that ordered goods have

been received and to describe the quantity and condition of the goods.

4. An income statement account used to record the income effects of cash overages and cash

shortages arising from missing petty cash receipts or errors in making change.

5. A measure of how quickly a company can convert its accounts receivable into cash.

6. A document the purchasing department uses to place an order with a supplier.

7. A set of procedures and approvals designed to control cash disbursements and the acceptance of

obligations.

8. A method of initially recording purchases at the invoice price less any purchase discounts offered

by the seller.

9. A report explaining any differences between the checking account balance according to the

depositor's records and the balance reported on the bank statement.

10. The ability of a company to pay for its near-term obligations.