81

151)

Match the following terms with the appropriate definition.

1. The set of policies and procedures managers use to monitor and control business

activities.

2. The supplier (seller) of goods or services.

3. An expense used under the net method of accounting for purchases resulting from failure to take

advantage of cash discounts offered.

4. Currency, coins, and amounts on deposit in bank accounts.

5. An asset such as cash that can be readily used to settle near-term obligations.

6. Regulation requiring public companies to document and certify their system of internal controls.

7. An internal document listing the goods needed by a department and requesting that the goods be

purchased.

8. Short-term, highly liquid investments that are readily convertible to a known cash amount and are

sufficiently close to their maturity date so that the market value is not sensitive to interest rate

changes.

9. A bill sent from the supplier to the buyer.

10. A device that perforates the amount of a check into its face, making it difficult to alter.

82

152)

Match each of the following transactions with the applicable internal control principle that is being

violated listed.

A. Establish responsibility

B. Maintain adequate records

C. Insure assets and bond employees

D. Separate recordkeeping from custody of assets

E. Divide responsibility for related transactions

F. Apply technological controls

G. Perform regular and independent reviews

_____ 1. Cashiers have access to the cash register recorded tape or file.

_____ 2. A company uses a voucher system, but the cash disbursement clerk pays directly from

invoices received.

3. Only sales clerks use the cash registered, but they all share the same cash drawer.

_____ 4. The bookkeeper prepares and signs checks and completes the bank reconciliation.

5. A restaurant allows servers to keep cash collected in their aprons and ring in all sales at the

end of the night.

___ 6. A company fails to hire a CPA to perform an annual audit.

_____ 7. A company does not bond its key cash-handling employees.

_____ 8. A company has a single department that handles purchasing, receiving, and inventory

management.

_____ 9. A large company has no internal auditor on staff.

_____ 10. A company manager keeps pre-signed checks in his desk drawer for employees to hand

write when the accountant is out of the office.

153)

Identify each of the following items 1 through 10 as either (A) cash or (B) cash equivalent.

1. Coins

_____ 2. Petty cash

_____ 3. Three-month certificate of deposit

4. Commercial paper

_____ 5. Currency

6. Certified check

7. Cashier’s check

_____ 8. Money market accounts

9. Money orders

_____ 10. U.S. treasury bills

154)

Identify whether each of the following items 1 through 10 would on appear on the bank side or the

book side of a bank reconciliation.

_____ 1. Bank service charges

_____ 2. Outstanding checks

_____ 3. Deposits in transit

_____ 4. NSF check

_____ 5. Interest on a checking account

_____ 6. The company properly wrote a check for $95.80 that the bank incorrectly paid as $9.58.

7. The bank printed checks for the depositor for a fee.

_____ 8. Bank debit memorandum

_____ 9. Bank credit memorandum

_____ 10. The bank collected a $1,000 note for the depositor.

ESSAY QUESTIONS

155)

Define an internal control system and describe its purpose.

156)

List the principles of internal control.

157)

Explain the difference between cash and cash equivalents.

158)

Describe the basic bank services that contribute to the control of cash and identify at least two

internal control objectives served by the banking activities.

159)

What is the purpose of the days’ sales uncollected ratio?

160)

What is a voucher system and what are the two areas for which it establishes control procedures?

161)

Discuss how the principles of internal control apply to cash receipts over-the-counter by giving

several examples of good control measures that should be implemented.

162)

Discuss how the principles of internal control apply to cash receipts through the mail by giving

several examples of good control measures that should be implemented.

163)

Describe a petty cash account and its purpose.

164)

Describe a bank reconciliation and discuss its purpose.

165)

When using a voucher system, what are the steps on the invoice approval checklist that must be

completed before an invoice approval is complete and a voucher prepared?

166)

Describe the net method of accounting for purchases. Why might companies use the net method?

167)

The Sarbanes-Oxley Act (SOX) requires managers and auditors of companies whose stock is

traded on an exchange to document and certify the system of internal controls. What are the

specific requirements for auditors set forth by SOX?

168)

The treasurer of a company is responsible for cash management. List five cash management

principles that are essential for effective cash management.

169)

For each of the independent cases below, identify the principle of internal control that is violated, and

recommend what should be done to remedy the violation.

1. In order to save money, Indigo Company has decided to drop its property insurance on assets; and

stop bonding the cashiers who handle upwards of $5,000 in cash each day.

2. Jobs Company records each sale on a preprinted invoice. Because invoices are sometimes

damaged in the process of preparation, the invoices are not prenumbered. Instead, the sales clerk

writes the next number on each invoice as it is prepared.

3. Keegan Company is a very small business. Dylan Epps, one of the two office clerks, opens the

mail each day and removes the cash receipts that come in the mail. Dylan also records the receipts in

the cash records and the customer’s account and deposits the cash in the bank.

4. Ludwig Company prides itself on hiring only the most competent employees. The owner, Jeremy

Ludwig, believes that since the employees are highly competent he can show he trusts them

completely by not checking up on their performance.

5. Maple Industries is a small business with three accounting employees. Each employee is

well-trained and able to perform any of the accounting tasks, including handling cash receipts and

cash disbursements, and preparing the bank reconciliation. Because of this cross-training, the

employees share responsibilities for all of the tasks.

170)

At the end of the current period, a company reported $725,000 in net credit sales and $100,000 in

ending accounts receivable. Calculate this company’s days’ sales uncollected at the end of the

current period.

171)

Norman Co. had $5,925 million in sales and $1,155 million in ending accounts receivable for the

current period. For the same period, Opal Co. reported $5,885 million in sales and $790 million in

ending accounts receivable. Calculate the days’ sales uncollected for both companies as of the end

of the current period and indicate which company is doing a better job in managing the collection

of its receivables.

172)

A company reported net sales for 2014 of $265,000 and $545,000 for 2015. The year-end balances

of accounts receivable were $39,000 for 2014 and $92,000 for 2015. Calculate the days’ sales

uncollected at the end of each year for this company and describe any changes in the apparent

liquidity of the company’s receivables.

173)

At the end of the day on March 15, the cash register’s record shows $1,957, but the count of cash in

the register is $1,965. Prepare the general journal entry to record the day’s cash sales.

174)

Plenty Co. established a petty cash fund of $150 on October 1. On October 10, the petty cash fund

was replenished when there was $49 remaining and there were petty cash receipts for: office

supplies, $47; transportation-in on inventory purchased, $32; and postage, $22. On October 15, the

petty cash fund was decreased to $125 in total. Plenty Co. uses the perpetual inventory system.

Record the above transactions in general journal form.

93

175)

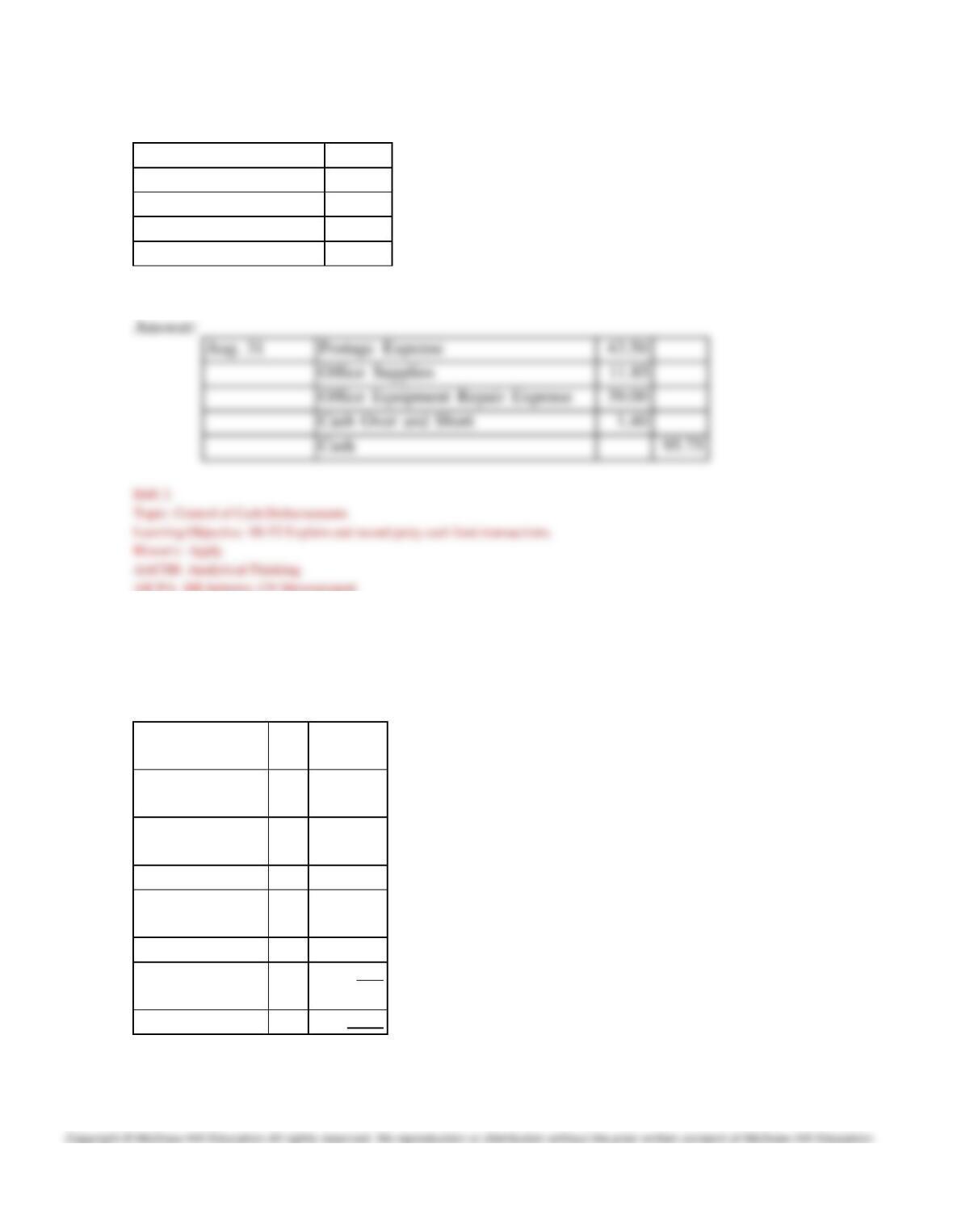

A petty cash fund was originally established with a check for $100. On August 31, which is the

period end, the petty cash fund included the following:

Petty cash receipts:

Postage

$43.50

Office supplies

11.85

Office equipment repair

39.00

Cash

4.25

Prepare the general journal entry to record the replenishment of the petty cash fund on August 31.

Aug. 31

Postage Expense

Office Supplies

Office Equipment Repair Expense

Cash Over and Short

Cash

176)

Quibble Company established a $300 petty cash fund by issuing a check to the custodian on

February 1. On February 15, the petty cash fund was replenished and increased to $800 in total. The

contents of the petty cash fund at the time of the February 15 replenishment were:

Currency and

coins

$12

Petty cash

receipts for:

Transportation-

in for inventory

$39

Delivery expense

88

Repairs to office

equipment

47

Postage

64

Entertainment of

customers

53

291

Total

$303

The company uses the perpetual inventory method. Prepare Quibble’s general journal entry to

record both the reimbursement and the increase of the petty fund on February 15.

177)

On March 1, a company established a $75 petty cash fund. On March 12, the petty cash fund

contains $3 in cash and the following paid petty cash receipts: transportation-in on merchandise

inventory $14.25; postage, $19.50; and office supplies, $36. Give the general journal entry to

reimburse the fund and to increase its amount to $150 on March 12.

Cash

Postage Expense

Merchandise Inventory

Cash Over and Short

178)

On June 1, a company established a $75 petty cash fund. On June 27, the petty cash fund contains

$5.25 in cash and the following paid petty cash receipts: postage, $19.50; office supplies, $36.25;

and miscellaneous expense $14.00. Give the general journal entry to reimburse the fund on June

27.

Jun. 27

Postage expense

Office supplies

179)

A company established a petty cash fund in November of the current year and experienced the

following transactions affecting the fund during November:

Nov. 1

Established a $200 petty cash fund.

5

Paid $55 to acquire office supplies.

8

Reimbursed the company controller for $30 spent on beverages for recruits

(entertainment expense).

18

Paid $45 for postage.

20

Paid $25 for C.O.D. charges on merchandise inventory, terms FOB

shipping point.

25

Paid $40 for janitorial services.

28

When sorting the petty cash receipts to replenish the fund, the custodian

noted that there was $10 cash remaining.

Prepare the journal entries to establish the fund on November 1 and to reimburse the fund on

November 28.

()

()

()

()

()

()

180)

Following are seven items a through g that would cause Rembrandt Company’s book balance of

cash to differ from its bank statement balance of cash.

a. A service charge imposed by the bank.

b. A check listed as outstanding on the previous period’s reconciliation and still outstanding at the end

of this month.

c. A customer’s check returned by the bank is marked “Not Sufficient Funds (NSF)”.

d. A deposit mailed to the bank on the last day of the current month and not recorded on this month’s

bank statement.

e. A check paid by the bank at its correct $190 amount recorded in error in the company’s check

register at $109.

f. An unrecorded credit memorandum indicating that bank collected a note receivable for Rembrandt

Company and deposited the proceeds in the company’s account.

g. A check written in the current period that is not yet paid or returned by the bank.

Indicate where each item, letters a-g, would appear on Rembrandt Company’s bank reconciliation by

placing its identifying letter in the parentheses in the proper section of the form below.

Bank statement cash balance

Book balance of cash

Add:

()

Add:

()

()

()

()

()

Deduct:

()

Deduct:

()

()

()

()

()

Reconciled balance

Reconciled balance

181)

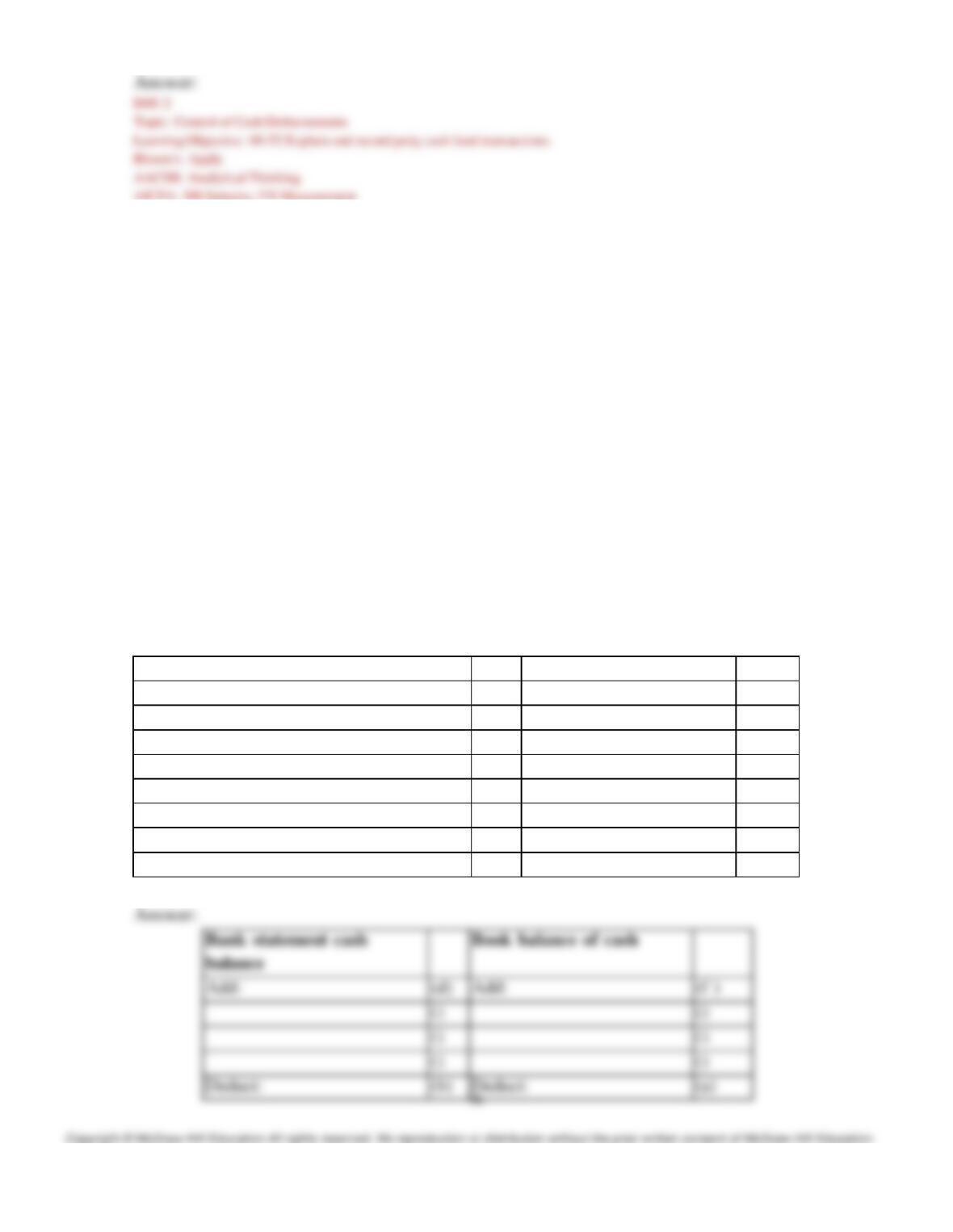

The following information is available for the Savvy Company for the month of June.

a. On June 30, after all transactions have been recorded, the balance in the company’s Cash account

has a balance of $17,202.

b. The company’s bank statement shows a balance on June 30 of $19,279.

c. Outstanding checks at June 30 total $2,984.

d. A credit memo included with the bank statement indicates that the bank collected $770 on a

noninterest-bearing note receivable for Savvy.

e. A debit memo included with the bank statement shows a $67 NSF check from a customer, J.

Maroon.

f. A deposit placed in the bank’s night depository on June 30 totaling $1,675 did not appear on the

bank statement.

g. Comparing the checks on the bank statement with the entries in the accounting records reveals that

check #3445 for the payment of an account payable was correctly written for $2,450, but was

recorded in the accounting records as $2,540.

h. Included with the bank statement was a debit memorandum in the amount of $25 for bank service

charges. It has not been recorded on the company’s books.

1. Prepare the June bank reconciliation for the Savvy Company.

2. Prepare the general journal entries to bring the company’s book balance of cash into conformity

with the reconciled balance as of June 30.

98

182)

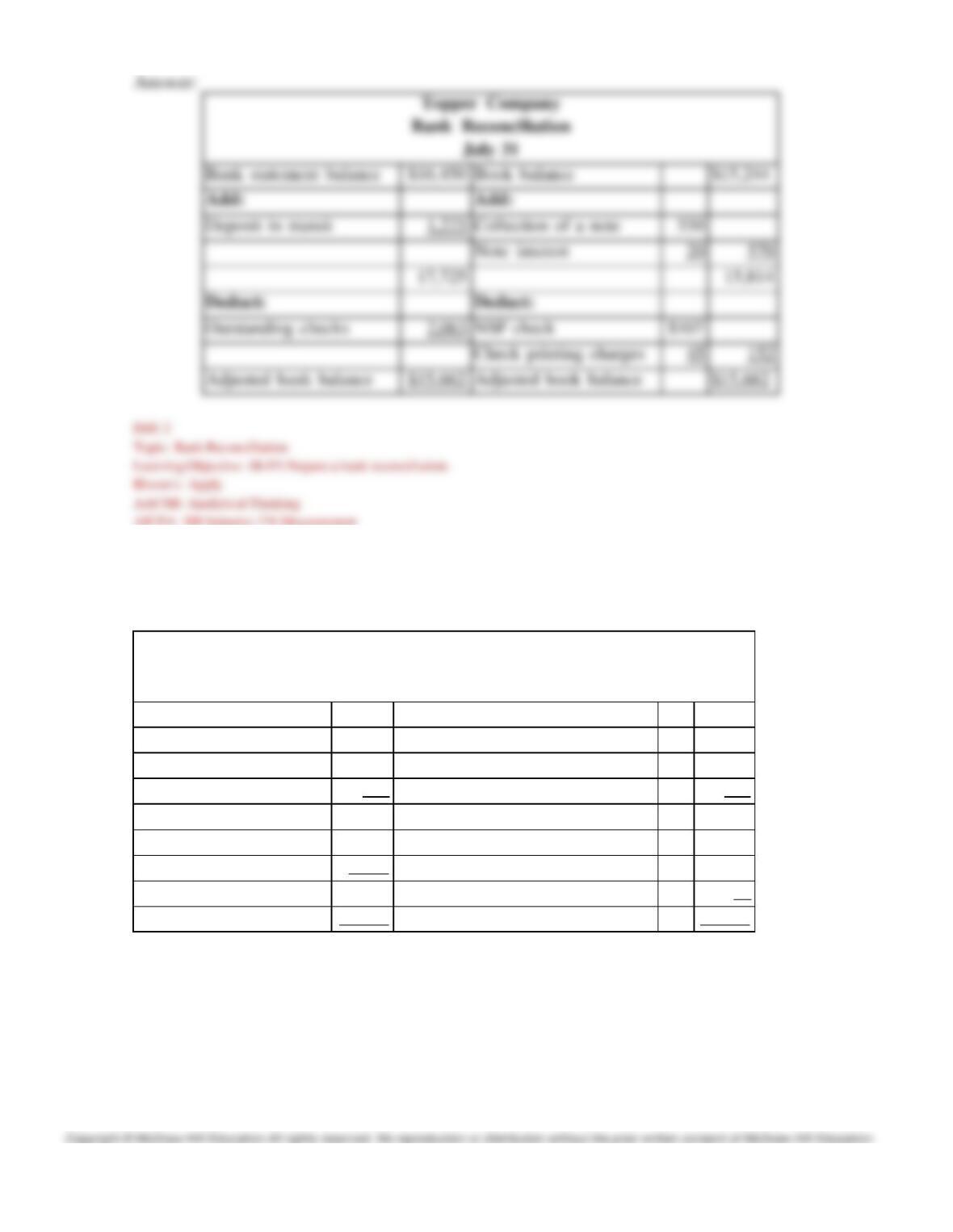

The following information is available for the Topper Company for the month of July.

a. On July 31, after all transactions have been recorded, the balance in the company’s Cash account

has a balance of $15,244.

b. The company’s bank statement shows a balance on July of $16,450.

c. Outstanding checks at July total $2,063.

d. A credit memo included with the bank statement indicates that the bank collected $570 on a note

receivable for Topper. The $570 includes $550 principle and $20 interest.

e. A debit memo included with the bank statement shows a $107 NSF check from a customer, P.

Flank.

f. A deposit placed in the bank’s night depository on July 31 totaling $1,275 did not appear on the

bank statement.

h. Included with the bank statement was a debit memorandum in the amount of $45 for check

printing charges that have not been recorded on the company’s books.

Prepare the July bank reconciliation for the Topper Company.

99

Bank statement balance

$16,450

Book balance

$15,244

Add:

Add:

Deposit in transit

Collection of a note

Note interest

17,725

15,814

Deduct:

Deduct:

Outstanding checks

NSF check

Check printing charges

Adjusted bank balance

$15,662

Adjusted book balance

$15,662

183)

Umber Company’s bank reconciliation for September is presented below. Prepare the necessary

adjusting journal entries based on the reconciliation report.

UMBER COMPANY

Bank Reconciliation

September 30

Bank statement balance

$1,350

Book balance of cash

$995

Add:

Add:

Deposit in transit

1,250

Proceeds of note

900

Bank error

275

Less note collection fee

25

875

$2,875

1,870

Deduct:

Deduct:

Outstanding checks

1,145

NSF check plus processing fee

125

Bank service charge

15

Reconciled balance

$1,730

Reconciled balance

$1,730