Objective 8.5

1) Which of the following statements is true of variable overhead costs?

A) Variable overhead costs always have unused capacity.

B) Variable overhead costs have no production-volume variance.

C) Variable overhead costs have no spending variance.

D) Variable overhead costs have no efficiency variance.

2) Fixed overhead costs ________.

A) never have any unused capacity

B) have no spending variance

C) have no efficiency variance

D) have no production-volume variance

3) When variable overhead spending variance is unfavorable, it can be safely assumed that ________.

A) actual rate per unit of cost-allocation base is higher than budgeted rate

B) actual quantity of cost-allocation base used is higher than budgeted quantity

C) actual rate per unit of cost-allocation base is lower than budgeted rate

D) actual quantity of cost-allocation base used is lower than budgeted quantity

4) When fixed overhead spending variance is unfavorable, it can be safely assumed that ________.

A) flexible budget amount is higher than actual costs incurred

B) fixed overhead allocated for actual output is lower than actual costs incurred

C) flexible budget amount is lower than actual costs incurred

D) fixed overhead allocated for actual output is higher than actual costs incurred

5) Which of the following statements is true of fixed overhead cost variances?

A) The difference between actual costs and flexible budget costs will give the production volume

variance.

B) The difference between actual costs and static budget costs will give the production volume variance.

C) The difference between flexible budget costs and allocated overhead costs will give the production

volume variance.

D) The difference between static budget costs and flexible budget costs will give the production volume

variance.

Answer the following questions using the information below:

Skizone Company’s 4-Variance Analysis:

Spending Variance

Efficiency Variance

Production-Volume

Variance

Variable overhead

$6,500 F

$12,000 U

No variance

Fixed overhead

(a)

No variance

$46,000 U

6) If Skizone’s combined 4-Variance Analysis shows an unfavorable spending variance of $2,300, what is

the fixed overhead spending variance (a)?

A) $8,800 favorable

B) $4,200 unfavorable

C) $8,800 unfavorable

D) $4,200 favorable

7) Which of the following statements is true of Skizone’s overhead variances?

A) Budgeted variable overhead rate is higher than actual variable overhead rate.

B) Static fixed overhead amount is higher than flexible fixed overhead amount.

C) Budgeted variable overhead rate is lower than actual variable overhead rate.

D) Static fixed overhead amount is lower than flexible fixed overhead amount.

Production-

Variances Spending Efficiency Volume

Variable manufacturing overhead $ 7,500 F $30,000 U (B)

Fixed manufacturing overhead $28,000 U (A) $80,000 U

8) The above table is a ________.

A) 4-variance analysis

B) 3-variance analysis

C) 2-variance analysis

D) 1-variance analysis

9) In the above table, the amounts for (A) and (B), respectively, are ________.

A) $22,500 U; $110,000 U

B) $22,500 U; Zero

C) Zero; $110,000 U

D) Zero; Zero

10) In a combined 3-variance analysis, the total spending variance would be ________.

A) $20,500 F

B) $22,500 U

C) $20,500 U

D) $37,500 F

11) The total production-volume variance should be ________.

A) $80,000 F

B) $80,000 U

C) $108,000 F

D) $108,000 U

12) The total overhead variance should be ________.

A) $145,500 F

B) $130,500 U

C) $145,500 U

D) $130,500 F

13) Fixed overhead has no production-volume variance.

14) The accounting for 3-variance analysis is simpler than the 4-variance analysis, but some

information is lost because the variable and fixed overhead spending variances are combined

into a single total overhead spending variance.

15) Variance analysis of fixed nonmanufacturing costs, such as distribution costs, can also be useful when

planning for capacity.

44

16) At the end of the fiscal year, the fixed overhead spending variance is always prorated among work-in–

process control, finished goods control, and cost of goods sold on the basis of the fixed overhead

allocated to these accounts.

17) Lungren has budgeted construction overhead for August of $260,000 for variable costs and $435,000

for fixed costs. Actual costs for the month totaled $275,000 for variable and $445,000 for fixed. Allocated

fixed overhead totaled $440,000. The company tracks each item in an overhead control account before

allocations are made to individual jobs. Spending variances for August were $10,000 unfavorable for

variable and $10,000 unfavorable for fixed. The production-volume overhead variance was $5,000

favorable.

Required:

a. Make journal entries for the actual costs incurred.

b. Make journal entries to record the variances for August.

45

18) Different management levels in Bates, Inc., require varying degrees of managerial accounting

information. Because of the need to comply with the managers’ requests, four different variances for

manufacturing overhead are computed each month. The information for the September overhead

expenditures is as follows:

Budgeted output units 3,200 units

Budgeted fixed manufacturing overhead $20,000

Budgeted variable manufacturing overhead $5 per direct labor hour

Budgeted direct manufacturing labor hours 2 hours per unit

Fixed manufacturing costs incurred $26,000

Direct manufacturing labor hours used 7,200

Variable manufacturing costs incurred $35,600

Actual units manufactured 3,400

Required:

a. Compute a 4-variance analysis for the plant controller.

b. Compute a 3-variance analysis for the plant manager.

c. Compute a 2-variance analysis for the corporate controller.

d. Compute the flexible-budget variance for the manufacturing vice president.

19) Explain why managers of small businesses prefer 3-variance analysis over 4-variance analysis.

Objective 8.6

1) The fixed overhead cost variance can be further subdivided into the ________.

A) price variance and the efficiency variance

B) spending variance and flexible-budget variance

C) production-volume variance and the efficiency variance

D) flexible-budget variance and the production-volume variance

2) The production-volume variance may also be referred to as the ________.

A) flexible-budget variance

B) denominator-level variance

C) spending variance

D) efficiency variance

3) Which of the following is a component of sales-volume variance?

A) Net-income volume variance

B) Operating-income volume variance

C) Taxable-income volume variance

D) Budgeted revenue variance

4) Under standard costing, ________.

A) fixed overhead costs are treated as if they are a variable cost

B) fixed overhead costs are treated as if they are a fixed cost

C) variable overhead costs are treated as if they are a fixed cost

D) fixed overhead costs are treated as if they are a sunk cost

5) An unfavorable production-volume variance ________.

A) is not a good measure of a lost production opportunity

B) indicates that the company had reduced its per unit fixed overhead cost to improve sales

C) measures the amount of extra fixed costs planned for but not used

D) takes into account the effect of additional revenues due to maintaining higher prices

6) The difference between budgeted fixed manufacturing overhead and the fixed manufacturing

overhead allocated to actual output units achieved is called the fixed overhead ________.

A) efficiency variance

B) flexible-budget variance

C) combined-variance analysis

D) production-volume variance

7) The production volume variance arises only for variable overhead costs.

8) The production-volume variance is a component of the sales-volume variance.

9) Under standard costing, fixed overhead costs are treated as if they are a variable cost.

10) A favorable production-volume variance arises when manufacturing capacity planned for is NOT

used.

11) An unfavorable production-volume variance always infers that management made a bad planning

decision regarding the plant capacity.

12) What are the two components of sales-volume variance? Explain why sales-volume variance could be

helpful to managers.

Objective 8.7

Answer the following questions using the information below:

Munoz, Inc., produces a special line of plastic toy racing cars. Munoz, Inc., produces the cars in batches.

To manufacture a batch of the cars, Munoz, Inc., must set up the machines and molds. Setup costs are

batch-level costs because they are associated with batches rather than individual units of products. A

separate Setup Department is responsible for setting up machines and molds for different styles of car.

Setup overhead costs consist of some costs that are variable and some costs that are fixed with respect to

the number of setup-hours. The following information pertains to June 2015:

Actual Static-budget

Amounts Amounts

Units produced and sold 15,000 11,250

Batch size (number of units per batch) 250 225

Setup-hours per batch 5 5.25

Variable overhead cost per setup-hour $40 $38

Total fixed setup overhead costs $12,000 $9,975

1) Calculate the efficiency variance for variable overhead setup costs.

A) $1,900 unfavorable

B) $600 unfavorable

C) $1,900 favorable

D) $600 favorable

2) Calculate the spending variance for variable overhead setup costs.

A) $1,900 unfavorable

B) $1,900 favorable

C) $600 unfavorable

D) $600 favorable

3) Calculate the flexible-budget variance for variable overhead setup costs.

A) $600 favorable

B) $1,300 favorable

C) $600 unfavorable

D) $1,300 unfavorable

4) Calculate the spending variance for fixed setup overhead costs.

A) $3,200 unfavorable

B) $2,025 unfavorable

C) $3,600 unfavorable

D) $2,025 favorable

5) Calculate the production-volume variance for fixed overhead setup costs.

A) $3,325 unfavorable

B) $400 unfavorable

C) $3,325 favorable

D) $400 favorable

Answer the following questions using the information below:

Lukehart Industries, Inc., produces air purifiers. Lukehart, Inc., produces the air purifiers in batches. To

manufacture a batch of the purifiers, Lukehart, Inc., must set up the machines and assembly line tooling.

Setup costs are batch-level costs because they are associated with batches rather than individual units of

products. A separate Setup Department is responsible for setting up machines and tooling for different

models of the air purifiers.

Setup overhead costs consist of some costs that are variable and some costs that are fixed with respect to

the number of setup-hours. The following information pertains to June 2015:

Budget Actual

Amounts Amounts

Units produced and sold 10,000 9,000

Batch size (number of units per batch) 400 375

Setup-hours per batch 6 5.5

Variable overhead cost per setup-hour $50 $52

Total fixed setup overhead costs $18,000 $17,750

6) Calculate the efficiency variance for variable overhead setup costs.

A) $150 favorable

B) $114 favorable

C) $264 unfavorable

D) $264 favorable

7) Calculate the spending variance for variable overhead setup costs.

A) $150 unfavorable

B) $150 favorable

C) $264 unfavorable

D) $264 favorable

8) Calculate the flexible-budget variance for variable overhead setup costs.

A) $114 favorable

B) $264 favorable

C) $264 unfavorable

D) $114 unfavorable

9) Calculate the spending variance for fixed overhead setup costs.

A) $250 unfavorable

B) $150 unfavorable

C) $250 favorable

D) $150 favorable

10) Calculate the production-volume variance for fixed overhead setup costs.

A) $1,800 favorable

B) $1,800 unfavorable

C) $250 unfavorable

D) $250 favorable

11) One possible reason for unfavorable variable overhead efficiency variance for materials handling is

________.

A) inefficient layout of product distribution channels

B) loosely budgeted standard hours

C) very low wait time at work centers

D) experienced but unmotivated employees

12) The fixed setup overhead flexible-budget variance is calculated as actual costs – flexible-budget

variance.

13) An unfavorable price variance for materials-handling labor indicates that the actual cost per

materials-handling labor-hour is less than the budgeted cost per materials-handling labor-hour.

14) Possible reasons for the larger actual materials-handling labor-hours per batch include the possibility

of unmotivated, inexperienced, and underskilled employees

15) Casey Corporation produces a special line of basketball hoops. Casey Corporation produces the

hoops in batches. To manufacture a batch of the basketball hoops, Casey Corporation must set up the

machines and molds. Setup costs are batch-level costs because they are associated with batches rather

than individual units of products. A separate Setup Department is responsible for setting up machines

and molds for different styles of basketball hoops.

Setup overhead costs consist of some costs that are variable and some costs that are fixed with respect to

the number of setup-hours. The following information pertains to January 2005.

Static-budget Actual

Amounts Amounts

Basketball hoops produced and sold 30,000 28,000

Batch size (number of units per batch) 200 250

Setup-hours per batch 5 4

Variable overhead cost per setup hour $10 $9

Total fixed setup overhead costs $22,500 $21,000

Required:

a. Calculate the efficiency variance for variable overhead setup costs.

b. Calculate the spending variance for variable overhead setup costs.

c. Calculate the flexible-budget variance for variable overhead setup costs.

d. Calculate the spending variance for fixed overhead setup costs.

e. Calculate the production-volume variance for fixed overhead setup costs.

56

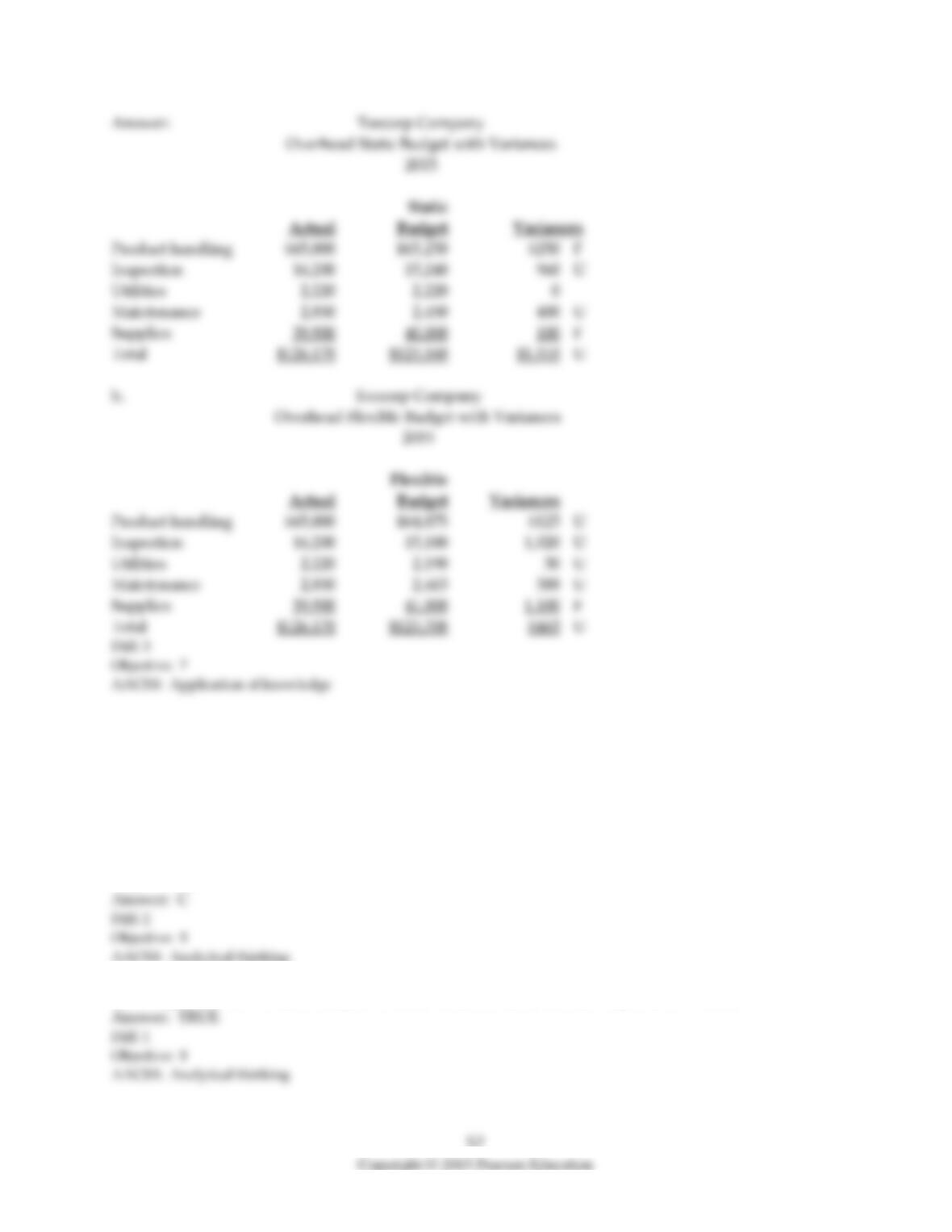

16) Teecorp Company uses a flexible budget for its indirect manufacturing costs. For 2015, the company

anticipated that it would produce 27,000 units with 4,800 machine-hours and 8,000 employee days. The

costs and cost drivers were to be as follows:

Fixed Variable Cost driver

Product handling $45,000 $0.75 per unit

Inspection 12,000 12.00 per 100 unit batch

Utilities 600 6.00 per 100 unit batch

Maintenance 1,250 0.25 per machine-hour

Supplies 5.00 per employee day

During the year, the company processed 26,500 units, worked 8,200 employee days, and had 4,850

machine-hours. The actual costs for 2015 were:

Actual costs

Product handling $65,000

Inspection 16,200

Utilities 2,220

Maintenance 2,850

Supplies 39,900

Required:

a. Prepare the static budget using the overhead items above and then compute the static-budget

variances.

b. Prepare the flexible budget using the overhead items above and then compute the flexible-budget

variances.

Objective 8.8

1) Standard costing can provide managers with reliable and timely information on variable distribution

overhead ________.

A) efficiency variances and production variances

B) production-volume variances and spending variances

C) efficiency variances and spending variances

D) production-volume variances and sales variances

2) Managers can use variance analysis to make decisions about the mix of products to make.

3) Service-sector companies have no use of variance analysis as only few costs can be traced to their

outputs in a cost effective way.

4) Explain how service-sector companies can benefit from variance analysis.