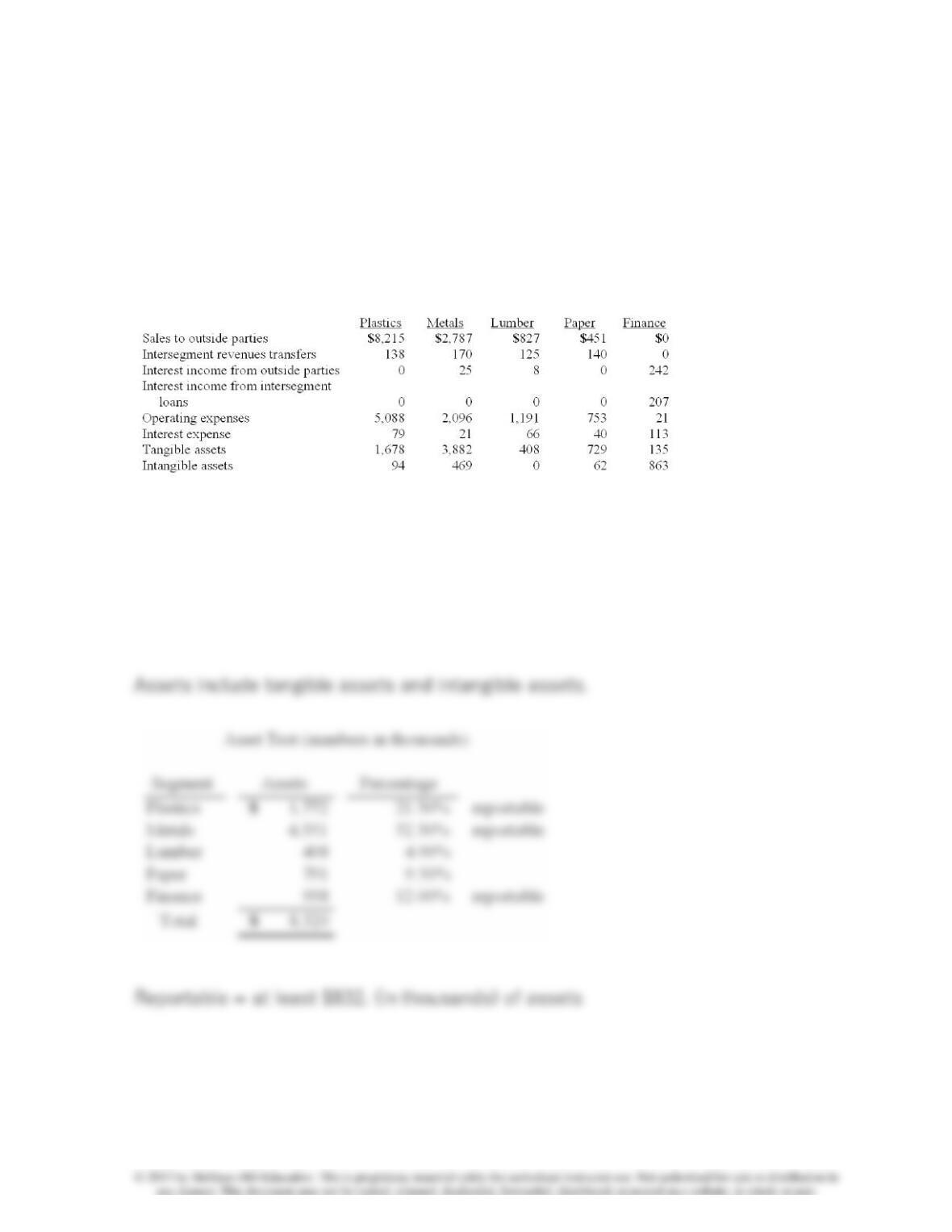

105. Faru Co. identified five industry segments: (1) plastics, (2) metals, (3)

lumber, (4) paper, and (5) finance. Each of these segments had been

consolidated appropriately by the company in producing its annual financial

statements. Information describing each segment is presented below (in

thousands).

Prepare the

asset test

and determine which of these segments was separately

reportable.

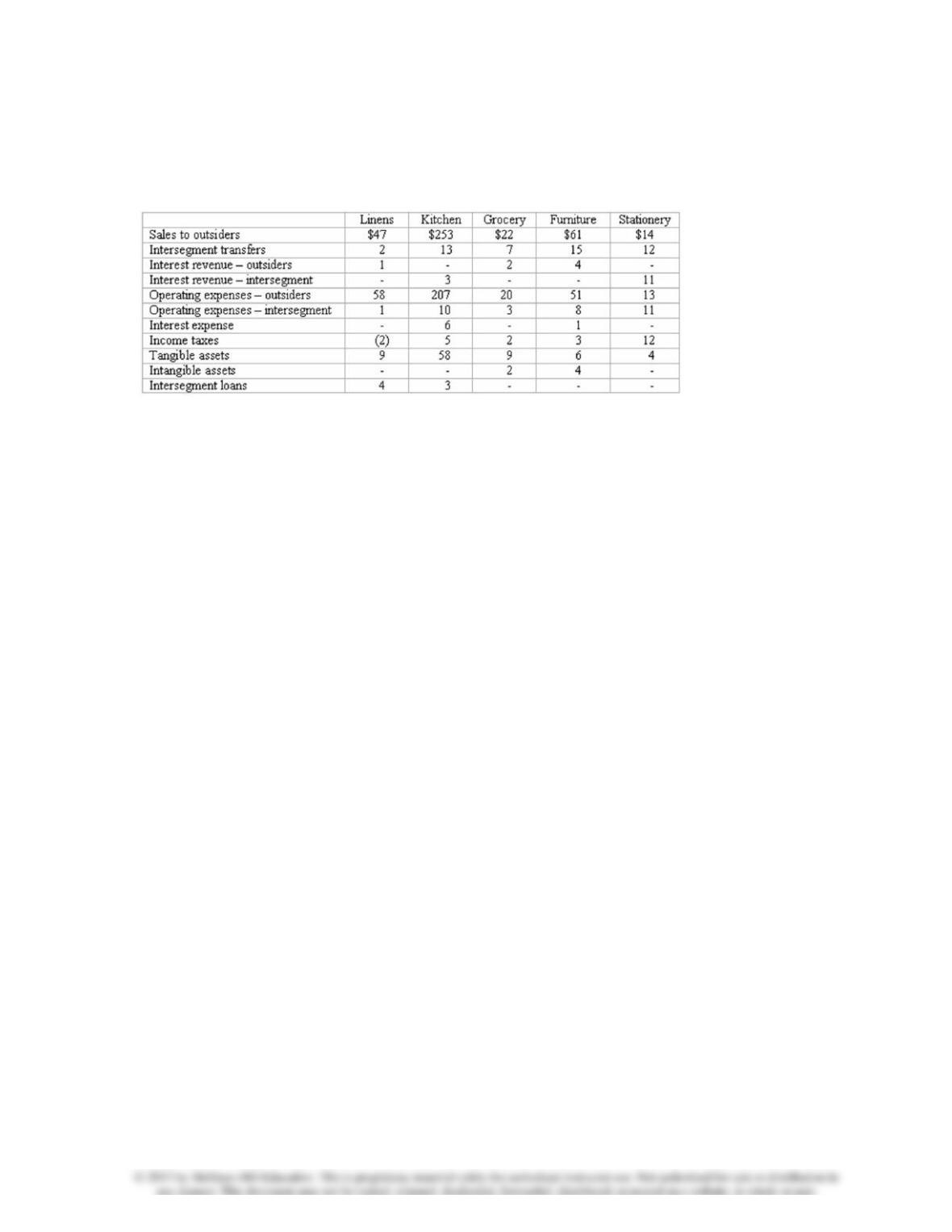

106. Blanton Corporation is comprised of five operating segments. Information

about each of these segments is as follows (in thousands):

Required:

(a.) Which operating segments are reportable under the revenue test?

(b.) What is the total amount of revenues in applying the revenues test?

(c.) Which operating segments are reportable under the profit or loss test?

(d.) In applying the profit or loss test, what is the minimum amount an operating

segment must have in order to meet the profit or loss test for a reportable

segment?

(e.) Which operating segments are reportable under the asset test?

(f.) In applying the asset test, what is the minimum amount an operating segment

must have in order to meet the asset test for a reportable segment?

(g.) Which operating segments are reportable?

(h.) According to the test results for reportable segments, is there a sufficient

number of reported segments or should any additional segments also be

disclosed? Explain the reason for your conclusion.

107. On February 23, 2011, Cleveland, Inc. paid property taxes of $300,000 for

the calendar year 2011.

How much of this expense should be included in Cleveland’s net income for the

quarter ending March 31, 2011?

108. On February 23, 2011, Cleveland, Inc. paid property taxes of $300,000 for

the calendar year 2011.

109. Gregor Inc. uses the LIFO cost-flow assumption to value inventory.

Inventory for Gregor on January 1, 2011 was 100 units at a LIFO cost of $25 per

unit. During the first quarter of 2011, 200 units were purchased costing an

average of $40 per unit, and sales of 265 units at a retail price of $50 per unit

were made.

Assuming Gregor does not expect to replace the units of beginning inventory sold,

what is the amount of cost of goods sold for the quarter ended March 31, 2011?

110. Gregor Inc. uses the LIFO cost-flow assumption to value inventory.

Inventory for Gregor on January 1, 2011 was 100 units at a LIFO cost of $25 per

unit. During the first quarter of 2011, 200 units were purchased costing an

average of $40 per unit, and sales of 265 units at a retail price of $50 per unit

were made.

Assuming Gregor expects to replace the units of beginning inventory sold before

the year-end at a cost of $41, what is the amount of cost of goods sold for the

quarter ended March 31, 2011?

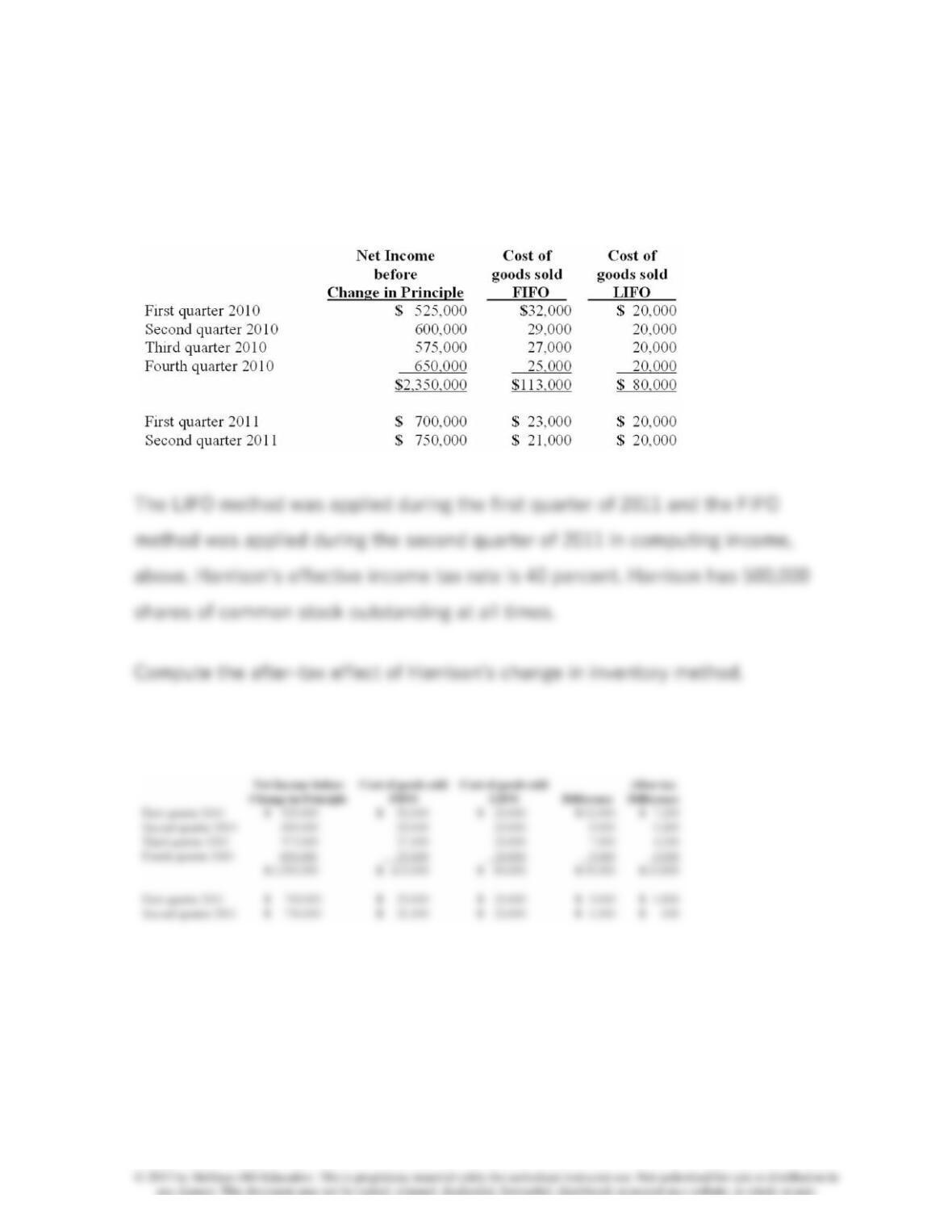

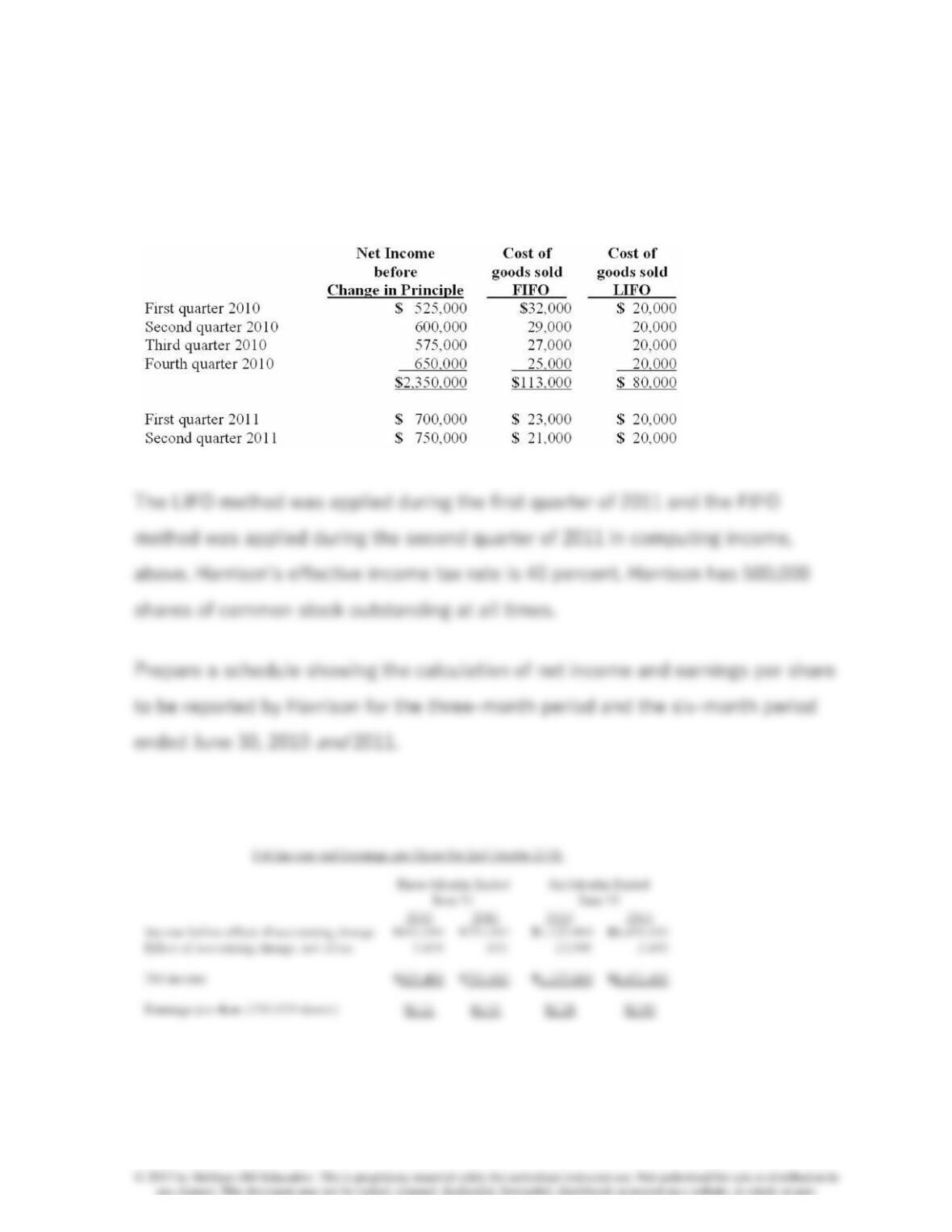

111. Harrison Company, Inc. began operations on January 1, 2010, and applied

the LIFO method for inventory valuation. On June 10, 2011, Harrison adopted the

FIFO method of accounting for inventory. Additional information is as follows:

112. Harrison Company, Inc. began operations on January 1, 2010, and applied

the LIFO method for inventory valuation. On June 10, 2011, Harrison adopted the

FIFO method of accounting for inventory. Additional information is as follows:

113. The following information for Urbanski Corporation relates to the three

months ending June 30, 2011:

Urbanski uses the LIFO method to account for inventory, and expects at least

15,000 units to be on hand in the ending inventory at year-end. Purchases made

in the last six months are expected to cost an average of $18 per unit.

114. The following information for Urbanski Corporation relates to the three

months ending June 30, 2011:

115. The following information for Urbanski Corporation relates to the three

months ending June 30, 2011:

116. For each of the following situations, select the best answer concerning

segment disclosures of reportable segments.

(A.) Required to be disclosed by an operating segment, but not a geographical

segment.

(B.) Required to be disclosed by a geographical segment, but not an operating

segment.

(C.) Required to be disclosed by both an operating segment and a geographical

segment.

(D.) Not required to be disclosed by either an operating segment or a

geographical segment.

___ 1. Factors used to identify segments.

___ 2. Revenues from external customers.

___ 3. Types of products and services from which each segment derives its

revenues.

___ 4. Names of major customers.

___ 5. Revenues from transactions with other segments.

___ 6. Interest revenue.

___ 7. Long-lived assets.

___ 8. Discontinued operations and extraordinary items, when applicable.

___ 9. Income tax expense or benefit.

___10. Revenues for the domestic country.

___11. Cash flow information