106. A contingent liability is recorded only if a loss is at least reasonably possible and the

amount can be reasonably estimated.

107. The balance in the Warranty Liability account is always equal to Warranty Expense.

108. A gain contingency is an existing uncertain situation that might result in a gain, which

often is the flip side of loss contingencies.

109. We record gain contingencies when the gain is probable and can be reasonably

estimated.

110. A company is said to be liquid if it has sufficient cash to pay currently maturing debts.

111. The current ratio is calculated by dividing current liabilities by current assets.

112. The acid-test ratio, or quick ratio, is similar to the current ratio but is based on a more

conservative measure of current assets available to pay current liabilities.

113. Quick assets include only cash, short-term investments, and accounts receivable.

114. A lower current ratio or acid-test ratio generally indicates a greater ability to pay current

liabilities on a timely basis.

115. Listed below are several terms and phrases associated with current liabilities. Pair each

item in the first column (by number) with the item in the second column that is most

appropriately associated with it.

1. Informal agreement that permits a company to

borrow up to a prearranged limit.

2. Amount of note payable x annual interest rate x

fraction of the year.

3. FICA and FUTA.

4. Classifying liabilities as either current or long-

term helps investors and creditors assess this.

5. Long-term debt maturing within one year.

(A) Current portion of

long-term debt

(B) Payroll taxes

(C) Line of credit

(D)The riskiness of a

business’s obligations

(E) Interest on debt

116. Listed below are several terms and phrases associated with current liabilities. Pair each

item in the first column (by number) with the item in the second column that is most

appropriately associated with it.

1. Classifying liabilities as either current or long-

term helps investors and creditors assess this.

2. Incurred on a notes payable.

3. Long-term debt maturing within one year.

4. Unsecured notes sold in minimum

denominations of $25,000 with maturities up to

270 days.

5. Social Security and Medicare.

6. Loss is reasonably possible and can be

reasonably estimated.

7. Cash, short-term investments, and accounts

receivable all divided by current liabilities.

8. Interest expense is recorded in the period

interest is incurred rather than in the period interest

is paid.

9. Gift cards.

10. Loss is probable and can be reasonably

estimated.

(A) Acid-test ratio

(B) Recording a contingent

liability

(C) Unearned revenues

(D) Current portion of

long-term debt

(E) FICA

(F) Accrual accounting

(G) Disclosure of a

contingent liability

(H) Interest expense

(I) Commercial paper

(J) The riskiness of a

business’s obligations

117. Listed below are several terms and phrases associated with current liabilities. Pair each

item in the first column (by number) with the item in the second column that is most

appropriately associated with it.

1. Loss is probable and can be reasonably

estimated.

2. Loss is reasonably possible and can be

reasonably estimated.

3. Debt that will be paid within the next year.

4. A liability that requires the sacrifice of

something other than cash.

5. A written promise to repay the amount

borrowed plus interest.

(A) Notes payable

5

(B) Disclosure of a

contingent liability

2

(C) Current portion of

long-term debt

3

(D) Recording a contingent

liability

1

(E) Unearned revenues

4

118. On November 1, Vacation Desinations borrows $1.5 million and issues a six-month, 8%

note payable. Interest is payable at maturity. Record the issuance of the note and the

appropriate adjusting entry for interest expense at December 31, the end of the reporting

period.

119. On September 1, 2012, Allied Moving Corp. borrows $100,000 cash from First National

Bank. Allied signs a six-month, 6% note payable. Interest is payable at maturity. Allied’s

year-end is December 31.

1. Record the note payable by Allied Moving Corp.

2. Record the appropriate adjusting entry for the note by Allied Moving Corp. on December

31, 2012.

3. Record the payment of the note at maturity.

120. On November 1, 2012, Dual Systems borrows $200,000 to expand operations. Dual

Systems signs a six-month, 9% promissory note. Interest is payable at maturity. Dual System’s

year-end is December 31.

1. Record the issuance of the note by Dual Systems.

2. Record the appropriate adjusting entry for the note by Dual Systems on December 31,

2012.

3. Record the payment of the note by Dual Systems at maturity on April 30, 2013.

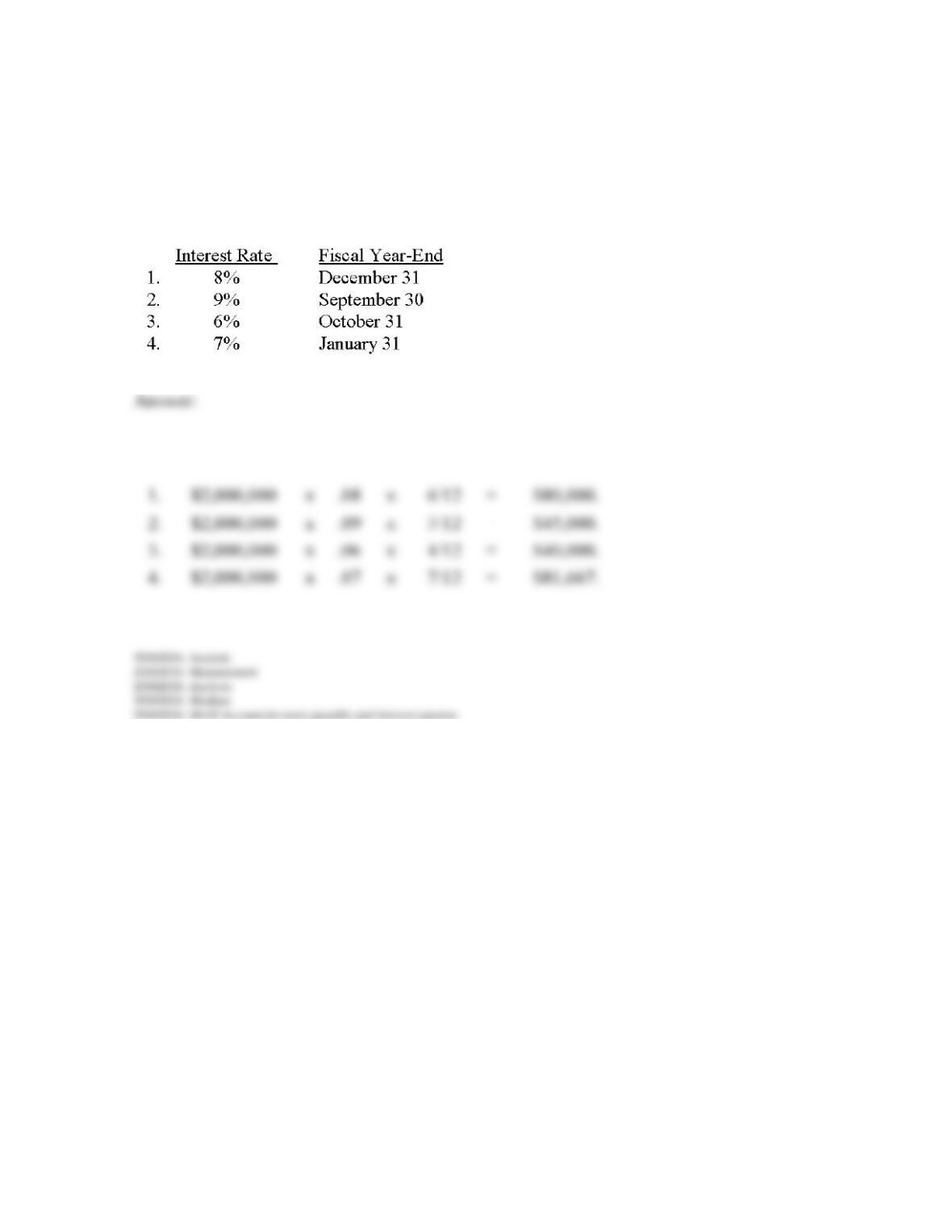

121. Assume that on July 1, 2012, Togo’s issues a $2 million, one-year note. Interest is

payable at maturity. Determine the amount of interest expense that should be recorded in a

year-end adjusting entry under each of the following independent assumptions:

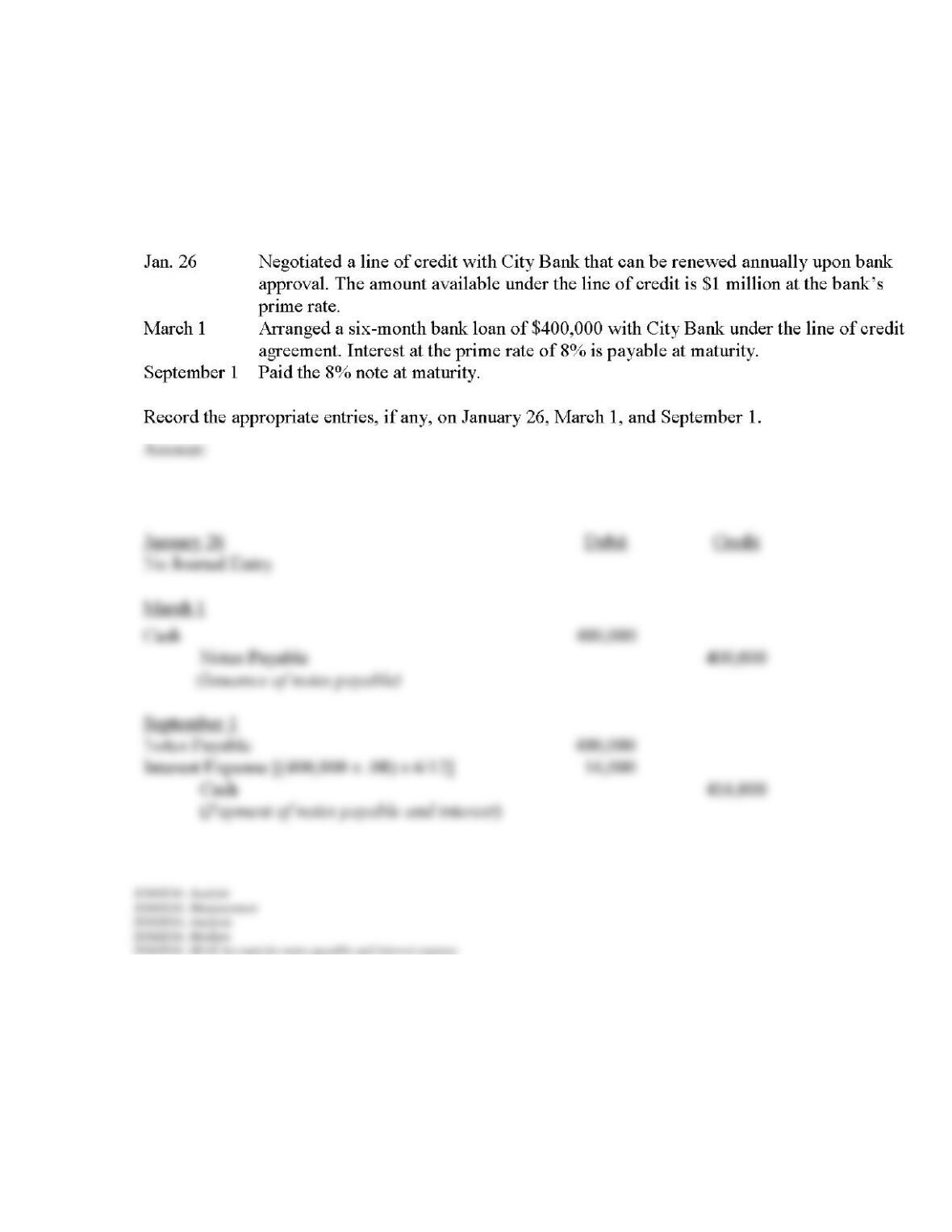

122. The following selected transactions relate to liabilities of Deco Emporium whose fiscal

year ends on December 31.

123. Match (by number) the correct reporting method for each of the items listed below.

Reporting Method

C. Current liability

L. Long-term liability

D. Disclosure note only

N. Not reported

124. Match (by number) the correct reporting method for each of the items listed below.

Reporting Method

C. Current liability

L. Long-term liability

D. Disclosure note only

N. Not reported

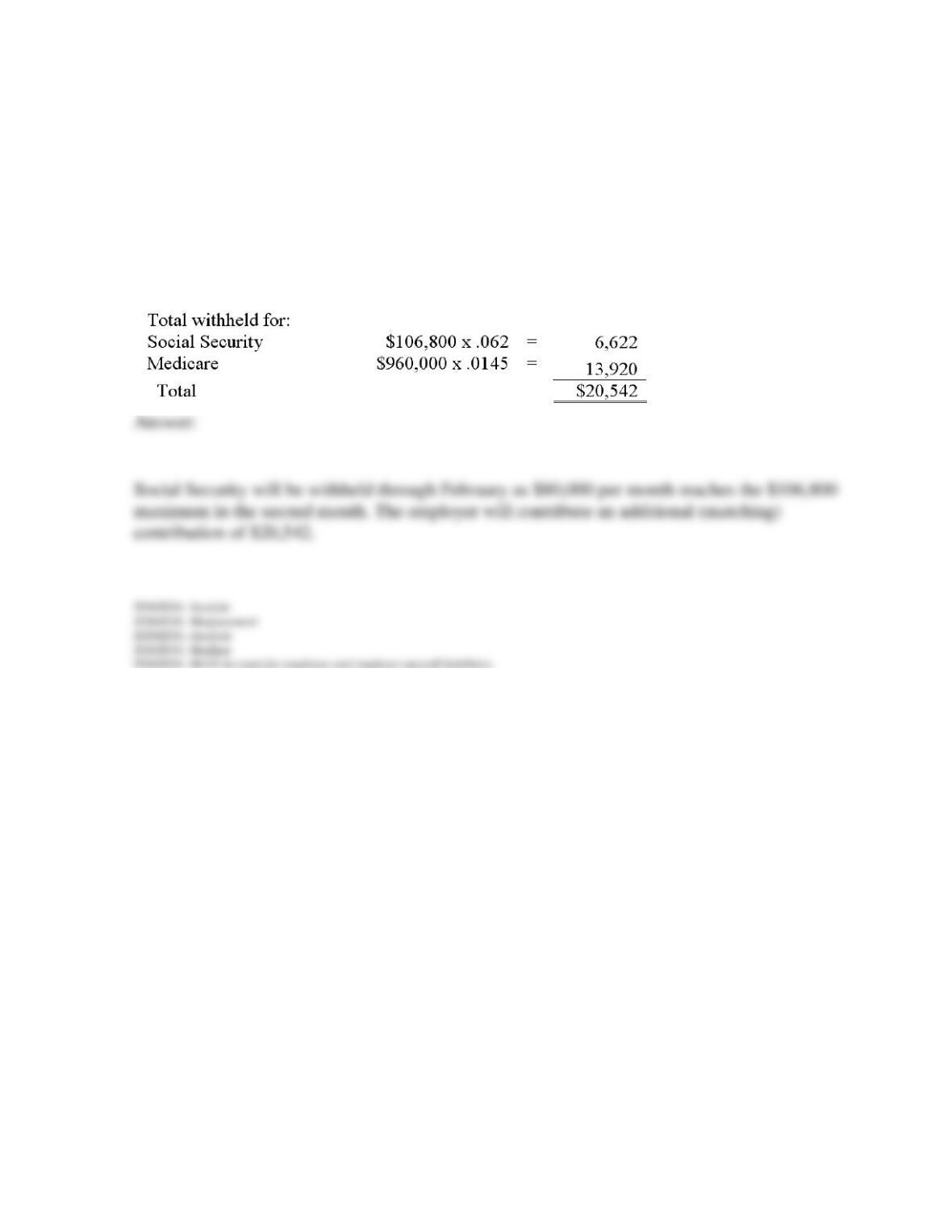

125. Mike Smith is a college football coach making a base salary of $960,000 a year ($80,000

per month). Employers are required to withhold a 6.2% Social Security tax up to a maximum

base amount and a 1.45% Medicare tax with no maximum. Assuming the FICA base amount

is $106,800, compute how much will be withheld during the year for Coach Smith’s Social

Security and Medicare. Through what month will Social Security be withheld? What

additional amount will the employer need to contribute?

126. Accurate Reports has 50 employees each working 40 hours per week and earning $25 an

hour. Federal income taxes are withheld at 15% and state income taxes at 6%. FICA taxes are

7.65% of the first $106,800 earned per employee and 1.45% thereafter. Unemployment taxes

are 3.8% of the first $7,000 earned per employee.

1. Compute the total salaries expense, the total withholdings from employee salaries, and the

actual direct deposit of payroll for the first week of January.

2. Compute the total payroll tax expense Accurate Reports will pay for the first week of

January.