7-122

122.

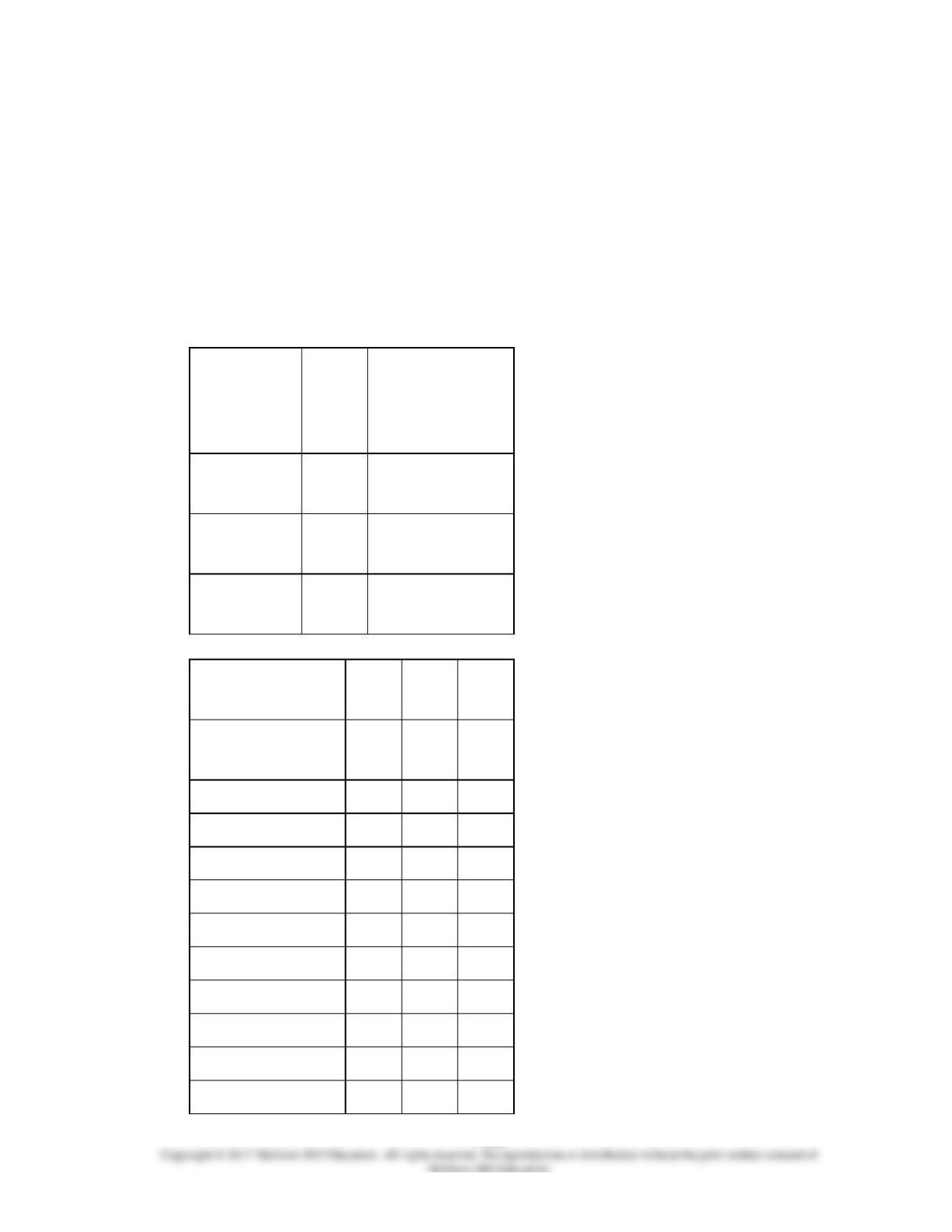

A manufacturing company employs job costing to account for its costs. There are three

production departments, and separate departmental overhead application rates are

employed because the operations of the departments are so different. All jobs generally

pass through all three production departments. Data regarding the hourly direct labor

rates, overhead application rates, and three jobs on which work was done during the

month appear below. Job 101 and Job 102 were completed during the current month. (CIA

Examination adapted)

Production

Departments

Direct

Labor

Rate

Manufacturing

overhead

application rates

Department 1

$12.00

50% of direct

materials

Department 2

$18.00

$8.00 per machine

hour

Department 3

$15.00

75% of direct labor

cost

Job

101

Job

102

Job

103

Beginning Work-in–

Process

$25,500

$32,400

$-0-

Direct materials:

Department 1

$40,000

$26,000

$58,000

Department 2

$3,000

$5,000

$14,000

Department 3

$-0-

$-0-

$-0-

Direct labor hours:

Department 1

500

400

300

Department 2

200

250

350

Department 3

1,500

1,800

2, 500

Machine hours:

Department 1

-0-

-0-

-0-

7-123

Department 2

1,200

1,500

2,700

Department 3

1,500

1,800

2,500

Department 1

40,000

26,000

58,000

Department 1

20,000

13,000

29,000

Department 2

12,000

21,600

123.

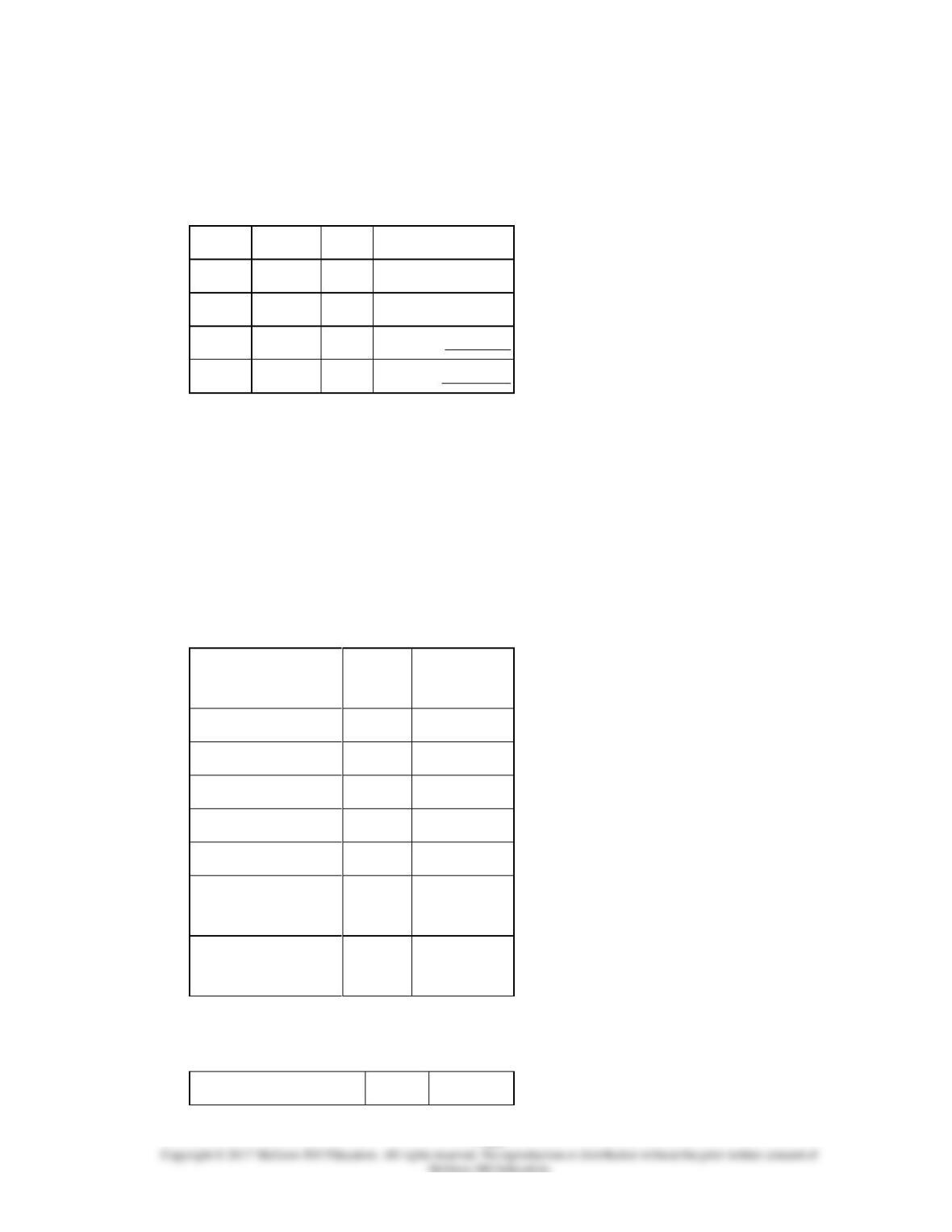

Kid’s World Manufacturing Company is a manufacturer of furnishings for infants and

7-124

children. The company uses job costing and employs a full absorption accounting method

for cost accumulation. Kid’s World Work–in-Process Inventory on April 30 consisted of the

following jobs:

Job No.

Items

Units

Accumulated Cost

CBSI02

Cribs

20,000

$900,000

PLP086

Playpens

15,000

420,000

DRS114

Dressers

25,000

250,000

Total

$1,570,000

Kid’s World applies manufacturing overhead on the basis of direct labor-hours. The

company’s estimated manufacturing overhead for the period ending May 31 totals

$4,500,000; the company estimated it would use 600,000 direct labor-hours during the

year.

At the end of April, the balance in Kid’s World Materials Inventory, which includes both

materials and purchased parts, was $668,000. Additions to, and requisitions from, the

materials inventory during the month of May included the following:

Materials

Purchased

Parts

Purchased

$242,000

$396,000

Requisitions:

Job CBS102

51,000

104,000

Job PLP086

3,000

10,800

Job DRS114

124,000

87,000

Job STR077 (10,000

strollers)

62,000

81,000

Job CRG096 (5,000

carriages)

65,000

187,000

During the month of May, Kid’s World factory payroll consisted of the following:

Hours

Cost

7-125

Job CBS102

12,000

$122,400

Job PLP086

4,400

43,200

Job DRS114

19,500

200,500

Job STR077

3,500

30,000

Job CRG096

14,000

138,000

Indirect supervision

57,600

Total

$591,700

Listed below are the jobs that were completed and the units that were sold during the

month of May.

Job No.

Items

Quantity

Completed

CBS102

Cribs

20,000

PLP086

Playpens

15,000

STR077

Strollers

10,000

CRG096

Carriages

5,000

7-127

124.

125.

The Focus Company does not maintain backup documents for its computer files. In June,

some of the current data were lost, and you have been asked to help reconstruct the data.

The following beginning balances are known:

Direct materials inventory

$24,000

Work-in-process inventory

9,000

Finished goods inventory

22,000

Manufacturing overhead control

33,000

Accounts payable

12,000

7-130

126.

Windham Manufacturing Company employs job costing to account for its costs. There are

three production departments, and separate departmental overhead application rates are

employed. All jobs generally pass through all three production departments. Data

regarding the hourly direct labor rates, overhead application rates, and three jobs on which

work was done during the month appear below. Job 611 and Job 613 were completed

during the current month, Job 612 was still in process. (CIA Examination adapted)

Production

Dept

Direct

Labor

Rate

Manufacturing

overhead application

rate

Cutting

$14.00

40% of direct materials

Machining

$20.00

$10.00 per machine hour

Assembly

$22.00

80% of direct labor cost

Job 611

Job 612

Job 613

Beginning WIP

$52,500

$16,200

$-0-

Direct materials:

Cutting

50,000

32,000

76,000

Machining

4,000

7,000

19,000

Assembly

-0-

-0-

-0-

Direct labor hours:

Cutting

500

400

600

Machining

800

750

850

Assembly

1,100

1,200

3,500

Machine hours:

Cutting

-0-

-0-

-0-

Machining

2,200

1,800

3,400

Assembly

500

800

750

Required:

(a) Compute the completed costs of Job 611 and Job 613.

7-131

127.

Carlson Corporation applies overhead based upon machine-hours. Budgeted factory

overhead was $266,400 and budgeted machine-hours were 18,500. Actual factory

overhead was $287,920 and actual machine-hours were 19,050. Before disposition of over–

or underapplied overhead, the cost of goods sold was $560,000 and ending inventories

were as follows:

Direct materials

$60,000

WIP

190,000

Finished goods

250,000

Total

$500,000

Required:

a. Compute the amount of overhead applied to production.

b. Prepare the journal entry to dispose of the over/under-applied overhead using the

write-off to cost of goods sold approach.

c. Prepare the journal entry to dispose of the over/under-applied overhead using the

proration approach.

(a) $274,320

Cost of goods sold

Finished goods

Cost of goods sold

COGS

128.

Job 7890 was recently completed. The following data have been recorded on its job cost

sheet:

Direct materials

$45,000

Direct labor-hours

630 labor-hours

Direct labor wage rate

$13 per labor-hour

Machine-hours

390 machine-hours

Number of units completed

3,000 units

Total cost

Unit product cost

129.

Job 5432 was recently completed. The following data have been recorded on its job cost

sheet:

Direct materials

$40,610

Direct labor-hours

1,147 DLHs

Direct labor wage rate

$11 per DLH

Number of units completed

3,100 units

Direct materials

1,147 DLHs

130.

131.

132.

7-138

133.

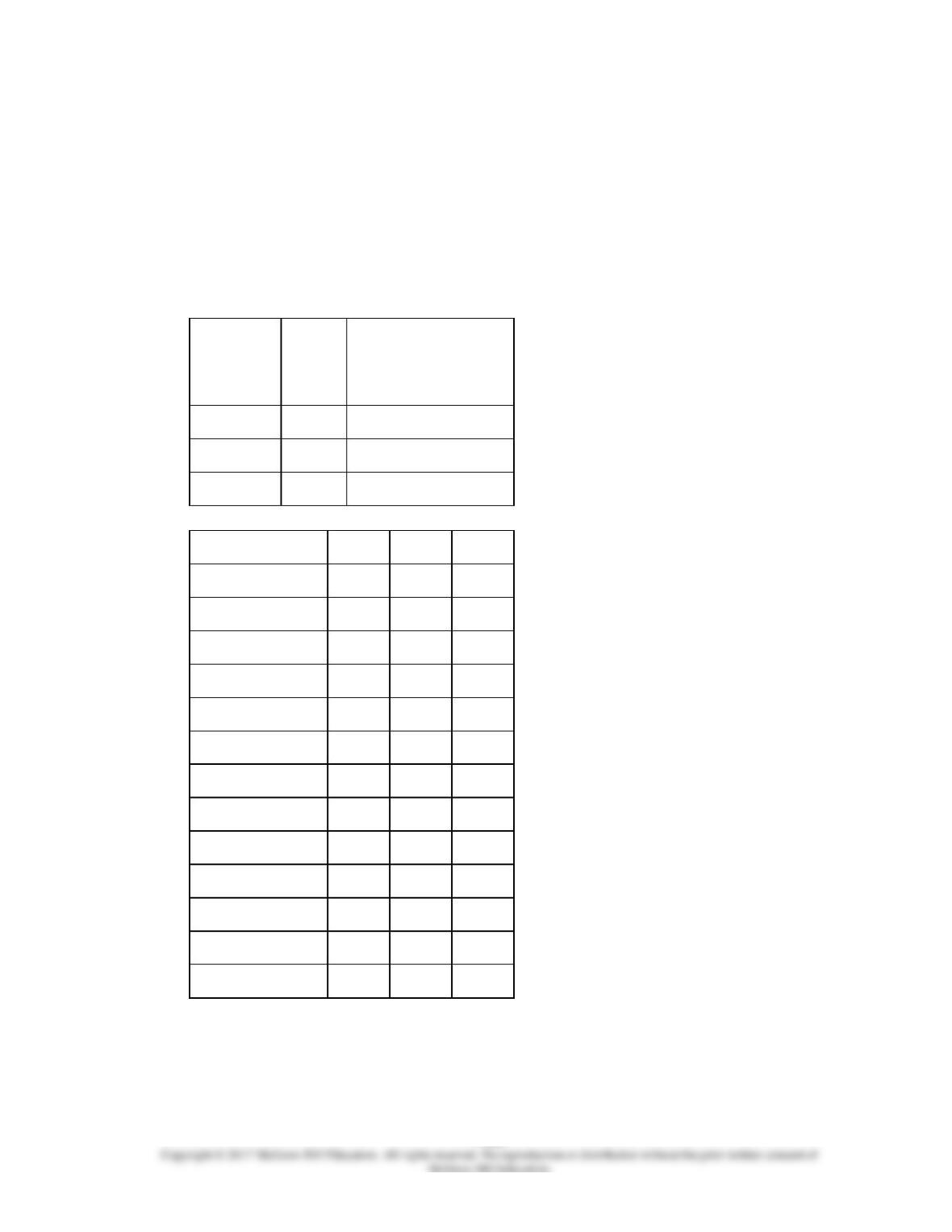

Wang’s Corporation applies overhead based upon machine-hours. Budgeted factory

overhead was $325,000 and budgeted machine-hours were 13,000. Actual factory

overhead was $312,330 and actual machine-hours were 12,660. Before disposition of over–

or underapplied overhead, the cost of goods sold was $725,000 and ending inventories

were as follows:

WIP

$150,000

Finished goods

375,000

Total

$525,000

Cost of goods sold

WIP

Finished goods

Cost of goods sold

134.

Harkin Corporation bases its predetermined overhead rate on the estimated machine–

hours for the upcoming year. Data for the upcoming year appear below:

Estimated machine-hours

73,000

Estimated variable

manufacturing overhead

$3.49

per

machine-

hour

Estimated total fixed

manufacturing overhead

$838,770