7-162

153.

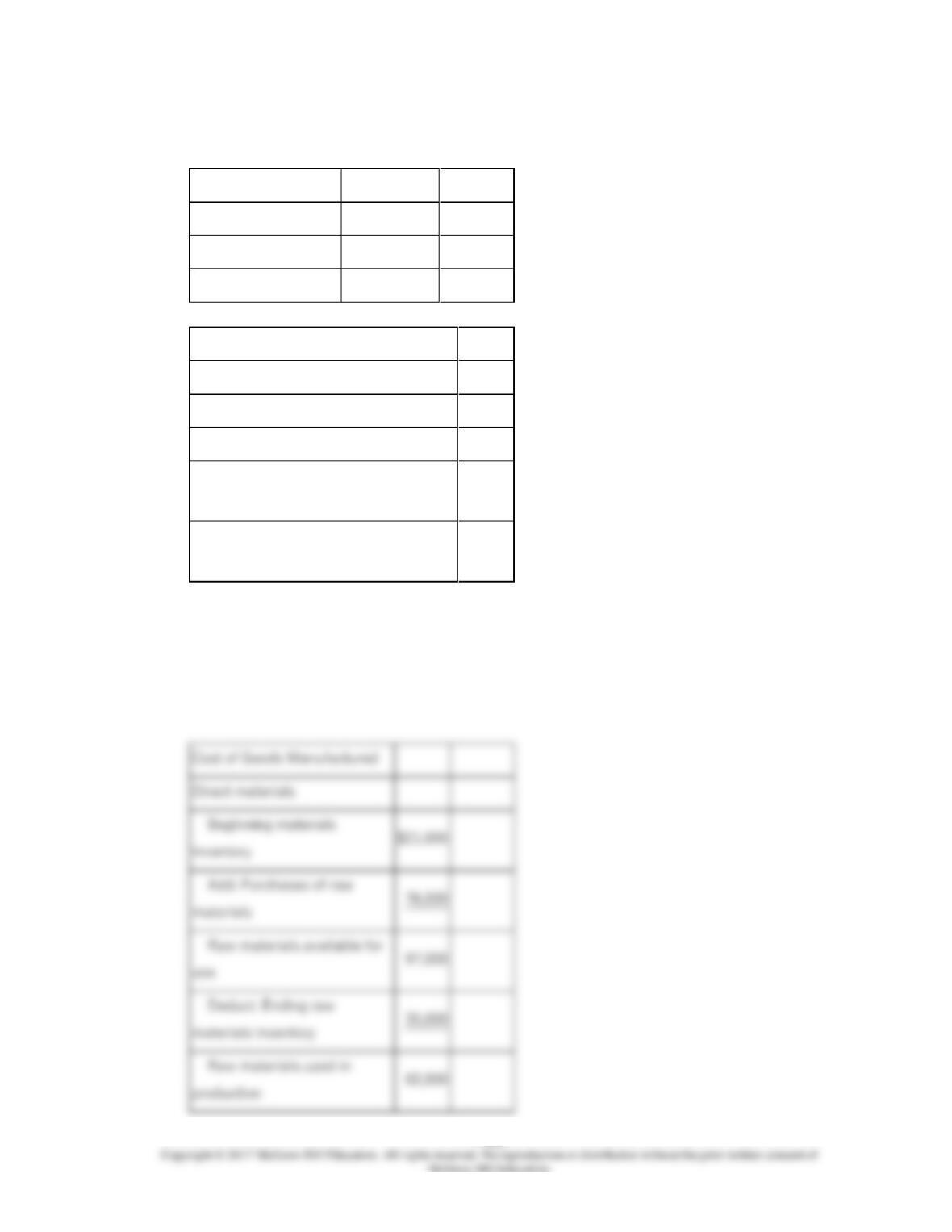

Dickerson Corporation has provided the following data for the month of April:

Inventories:

Beginning

Ending

Raw materials

$21,000

$35,000

Work-in-Process

$17,000

$19,000

Finished goods

$46,000

$38,000

Additional information:

Raw materials purchases

$76,000

Direct labor cost

$81,000

Manufacturing overhead cost incurred

$42,000

Indirect materials included in

manufacturing overhead cost incurred

$6,000

Manufacturing overhead cost applied to

Work-in-Process

$44,000

Cost of Goods Manufactured

Direct materials

Raw materials available for

use

Deduct: Ending raw

materials inventory

production

7-163

Deduct: Ending finished goods

154.

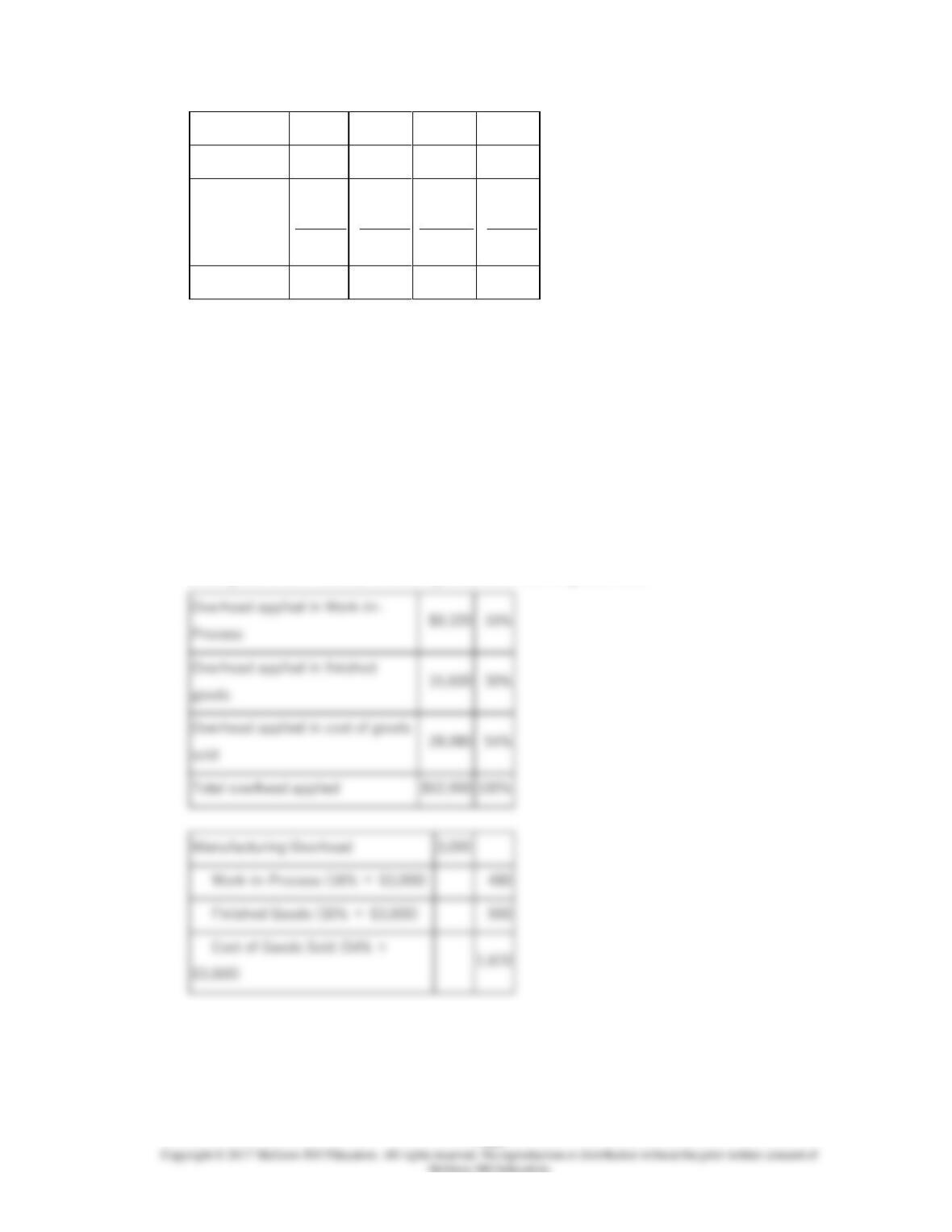

Townley Inc. has provided the following data for the month of February. There were no

beginning inventories; consequently, the direct materials, direct labor, and manufacturing

overhead applied listed below are all for the current month.

Work-

in–

Process

Finished

Goods

Cost of

Goods

Sold

Total

Direct

$7,570

$19,200

$35,280

$62,050

7-164

materials

Direct labor

8,810

24,000

44,100

76,910

Manufacturing

overhead

applied

8,320

15,600

28,080

52,000

Total

$24,700

$58,800

$107,460

$190,960

Manufacturing overhead for the month was overapplied by $3,000.

The company allocates any underapplied or overapplied overhead among Work–in–

Process, finished goods, and cost of goods sold at the end of the month on the basis of

the overhead applied during the month in those accounts.

Required:

Provide the journal entry that would record the allocation of underapplied or overapplied

among Work-in-Process, finished goods, and cost of goods sold.

Process

goods

$52,000

3,000

155.

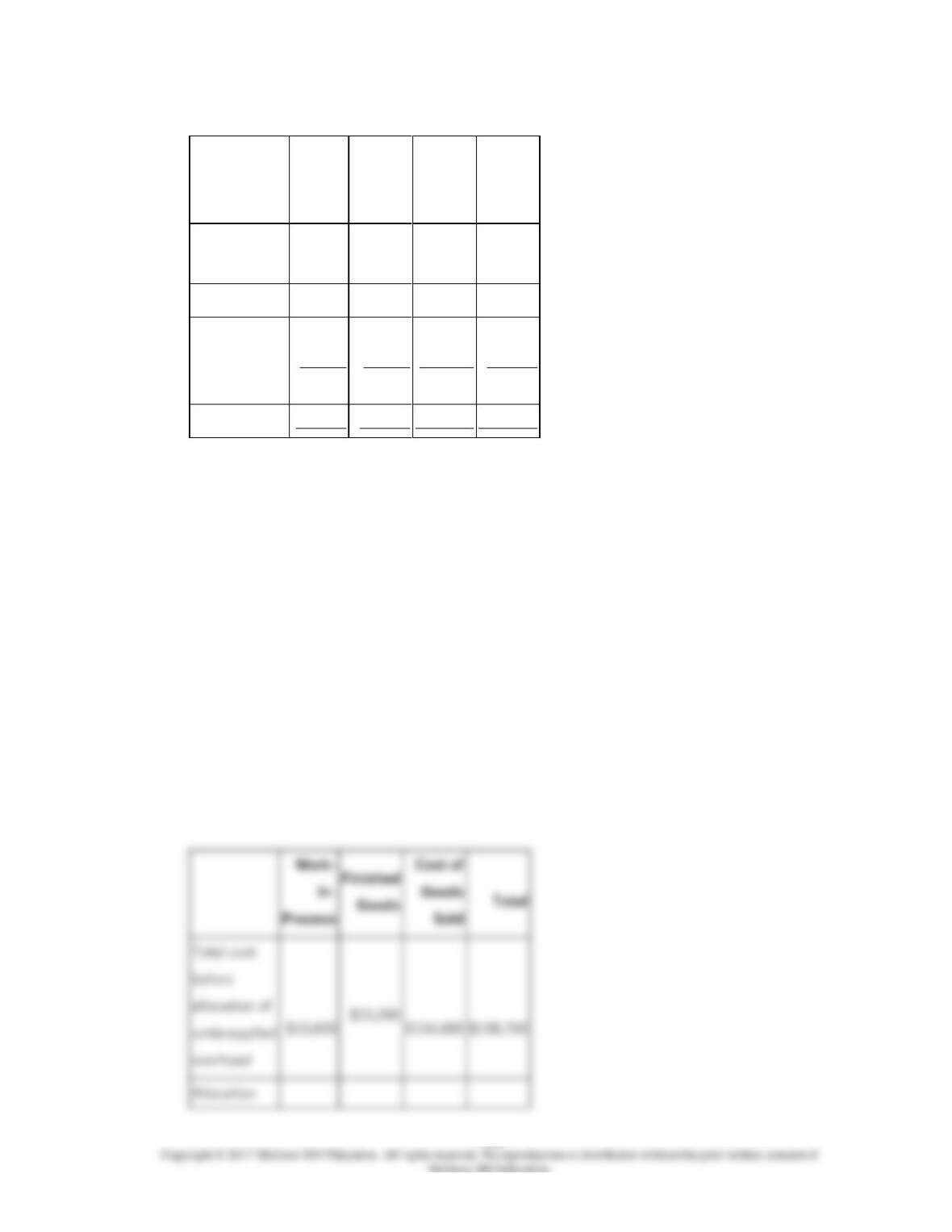

Ardvark Inc. has provided the following data for the month of November. There were no

beginning inventories; consequently, the direct materials, direct labor, and manufacturing

overhead applied listed below are all for the current month.

7-165

Work-

in–

Process

Finished

Goods

Cost of

Goods

Sold

Total

Direct

materials

$3,500

$11,200

$51,800

$66,500

Direct labor

3,260

14,400

66,600

84,260

Manufacturing

overhead

applied

3,840

7,680

36,480

48,000

Total

$10,600

$33,280

$154,880

$198,760

Manufacturing overhead for the month was underapplied by $6,000.

The company allocates any underapplied or overapplied overhead among Work-in–

Process, finished goods, and cost of goods sold at the end of the month on the basis of

the overhead applied during the month in those accounts.

Required:

Determine the cost of Work-in-Process, finished goods, and cost of goods sold AFTER

allocation of the underapplied or overapplied overhead for the period.

overhead

7-167

156.

7-169

157.

The management of Atlas Corporation would like to investigate the possibility of basing its

predetermined overhead rate on activity at capacity rather than on the estimated amount

of activity for the year. The company’s controller has provided an example to illustrate how

this new system would work. In this example, the allocation base is machine-hours and

the estimated amount of the allocation base for the upcoming year is 19,000 machine–

hours. In addition, capacity is 21,000 machine-hours and the actual activity for the year is

18,200 machine-hours. All of the manufacturing overhead is fixed and is $71,820 per year.

For simplicity, it is assumed that this is the estimated manufacturing overhead for the year

as well as the manufacturing overhead at capacity and the actual amount of

manufacturing overhead for the year.

Required:

a. Determine the predetermined overhead rate if the predetermined overhead rate is

based on the estimated amount of the allocation base.

b. Determine the underapplied or overapplied overhead for the year if the predetermined

overhead rate is based on the estimated amount of the allocation base.

c. Determine the predetermined overhead rate if the predetermined overhead rate is based

on the amount of the allocation base at capacity.

d. Determine the underapplied or overapplied overhead for the year if the predetermined

overhead rate is based on the amount of the allocation base at capacity.

7-172

158.

The management of Grainger Corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity rather than on the

estimated amount of activity for the year. The company’s controller has provided an

example to illustrate how this new system would work. In this example, the allocation base

is machine-hours and the estimated amount of the allocation base for the upcoming year

is 48,000 machine-hours. In addition, capacity is 53,000 machine-hours and the actual

activity for the year is 47,700 machine-hours. All of the manufacturing overhead is fixed

and is $1,144,800 per year. For simplicity, it is assumed that this is the estimated

manufacturing overhead for the year as well as the manufacturing overhead at capacity

and the actual amount of manufacturing overhead for the year. Job SUA–600, which

required 40 machine-hours, is one of the jobs worked on during the year.

Required:

a. Determine the predetermined overhead rate if the predetermined overhead rate is

based on the estimated amount of the allocation base.

b. Determine how much overhead would be applied to Job SUA–600 if the predetermined

overhead rate is based on estimated amount of the allocation base.

c. Determine the underapplied or overapplied overhead for the year if the predetermined

overhead rate is based on the estimated amount of the allocation base.

d. Determine the predetermined overhead rate if the predetermined overhead rate is

based on the amount of the allocation base at capacity.

e. Determine how much overhead would be applied to Job SUA-600 if the predetermined

overhead rate is based on the amount of the allocation base at capacity.

f. Determine the underapplied or overapplied overhead for the year if the predetermined

overhead rate is based on the amount of the allocation base at capacity.

7-176

159.

The management of Royal Corporation would like to investigate the possibility of basing

its predetermined overhead rate on activity at capacity rather than on the estimated

amount of activity for the year. The company’s controller has provided an example to

illustrate how this new system would work. In this example, the allocation base is

machine-hours and the estimated amount of the allocation base for the upcoming year is

70,000 machine-hours. In addition, capacity is 82,000 machine-hours and the actual

activity for the year is 72,900 machine-hours. All of the manufacturing overhead is fixed

and is $4,132,800 per year. For simplicity, it is assumed that this is the estimated

manufacturing overhead for the year as well as the manufacturing overhead at capacity

and the actual amount of manufacturing overhead for the year. Job 706H, which required

300 machine-hours, is one of the jobs worked on during the year.

Required:

a. Determine the predetermined overhead rate if the predetermined overhead rate is

based on the amount of the allocation base at capacity.

b. Determine how much overhead would be applied to Job 706H if the predetermined

overhead rate is based on the amount of the allocation base at capacity.

c. Determine the underapplied or overapplied overhead for the year if the predetermined

overhead rate is based on the amount of the allocation base at capacity.

7-178

160.

The management of Philly Corporation would like to investigate the possibility of basing its

predetermined overhead rate on activity at capacity rather than on the estimated amount

of activity for the year. The company’s controller has provided an example to illustrate how

this new system would work. In this example, the allocation base is machine-hours and

the estimated amount of the allocation base for the upcoming year is 37,000 machine–

hours. In addition, capacity is 46,000 machine-hours and the actual activity for the year is

36,900 machine-hours. All of the manufacturing overhead is fixed and is $697,820 per year.

For simplicity, it is assumed that this is the estimated manufacturing overhead for the year

as well as the manufacturing overhead at capacity and the actual amount of

manufacturing overhead for the year.

Required:

a. Determine the underapplied or overapplied overhead for the year if the predetermined

overhead rate is based on the estimated amount of the allocation base.

b. Determine the underapplied or overapplied overhead for the year if the predetermined

overhead rate is based on the amount of the allocation base at capacity.