178.

Watins, Inc.’s 2015 income statement reported net sales of $5,000,000. Watin’s average

accounts receivable during 2015 amounted to $450,000. Using 360 days to a year, Watin’s:

179.

Assuming a 365 day year, Bush Industries calculated an average of 47 days to collect its

accounts receivable in 2015. During 2015, Bush’s accounts receivable turnover rate:

Essay Questions

180.

Financial assets

(a.) Briefly explain what is meant by the term “financial assets.”

(b.) List the three major categories of assets comprising a company’s financial assets. For

each category, indicate the basis for valuation in the balance sheet.

7-103

181.

Match the following terms with the explanations below. If no term fits the explanation

write none

_________ (1) A means of accounting for uncollectibles which does not recognize any

expense until specific receivables are determined to be worthless.

_________ (2) An account showing the amount of estimated uncollectible receivables.

_________ (3) The process of estimating uncollectible accounts by classifying accounts

receivables by age groups.

_________ (4) Dividing net sales by average receivables to create a ratio to measure the

liquidity of accounts receivable.

_________ (5) Very short-term liquid investments which must mature within 90 days of

acquisition.

_________ (6) Cash and assets convertible directly into known amounts of cash.

_________ (7) An account showing the difference between the cost of an investment in

marketable securities and its market value.

_________ (8) The value of a note at its maturity date.

_________ (9) Highly liquid investments that can be sold in organized securities

exchanges.

7-105

182.

Financial assets-effects of transactions

Five events involving financial assets are described below:

(a.) Sold merchandise on account.

(b.) Sold available for sale marketable securities at a gain. Cash proceeds from the sale

were equal to the current market value of the securities reflected in the last balance

sheet.

(c.) Collected an account receivable.

(d.) Adjusted the allowance for doubtful accounts to reflect the portion of accounts

receivable estimated to be uncollectible at year-end.

(e.) Made the fair value accounting adjustment reducing the balance in the available for

sale marketable securities account to reflect a decrease in the market value of securities

owned.

Indicate the effects of each independent transaction or adjusting entry upon the financial

measurements shown in the column headings below. Use the code letters, I for increase,

D for decrease, and NE for no effect.

7-107

183.

Financial assets—effects of transactions

Five events involving financial assets are described below:

(a.) Received dividends earned on investment in marketable securities.

(b.) Invested excess cash in marketable securities.

(c.) Determined that a specific account receivable is worthless and wrote it off against the

allowance for doubtful accounts.

(d.) Made sale of merchandise for cash.

(e.) Sold available for sale marketable securities at a loss. Cash proceeds from the sale

were equal to the current market value reflected in the last balance sheet.

Indicate the effects of each independent transaction or adjusting entry upon the financial

measurements shown in the column headings below. Use the code letters, I for increase,

D for decrease, and NE for no effect.

7-109

184.

Accounting terminology

Listed below are nine technical accounting terms emphasized in this chapter.

Fair value accounting

Factoring

Direct write-off

Financial asset

Cash equivalent

Bank reconciliation

Allowance for doubtful accounts

Accounts receivable turnover

Uncollectible accounts expense

Each of the following statements may (or may not) describe one of these technical terms.

In the space provided below each statement, indicate the accounting term described, or

answer “None” if the statement does not correctly describe any of the terms.

______ a. A transaction in which a business sells its accounts receivables to a financial

institution.

______ b. An estimate of the portion of year-end accounts receivable that ultimately will

turn out to be uncollectible.

______ c. Schedule explaining any differences between cash balances appearing in the

accounting records and in the monthly bank statement.

______ d. Balance sheet valuation standard applicable to investments in marketable

securities.

______ e. Cash and assets convertible directly into known amounts of cash, such as

marketable securities and receivables.

______ f. A ratio, computed by dividing 365 days by average receivables, that indicates the

liquidity of the receivables.

______ g. Method of accounting for uncollectible receivables that fails to match revenues

and expenses.

185.

Cash management

(a.) What is meant by the term “cash management“?

(b.) Identify at least three basic objectives of effective cash management.

7-112

186.

Internal control over cash transactions

Listed below are seven errors or problems that might occur in the processing of cash

transactions. Also shown is a separate list of internal control procedures. Indicate the

internal control procedure that should prevent the error or problem from occurring. If none

of the control procedures would effectively prevent the error, place an X in the space

provided.

Possible Error or Problem

_______ 1. A purchase invoice was paid even though the merchandise was never received.

_______ 2. An employee issued a credit memorandum for a nonexistent sales return in

order to conceal his theft of the amount received in payment of an account receivable.

_______ 3. Management is unaware that blank checks are being issued for unauthorized

expenditures by the official designated to sign checks.

_______ 4. A salesclerk collects the full selling price from a customer but rings up the sale

at less than actual price and pockets the difference.

_______ 5. Several days’ cash receipts are lost in a fire.

_______ 6. A new employee often gives customers an incorrect amount of change.

_______ 7. No one has discovered that amounts deposited in the company’s bank account

by the cashier over the last few years are frequently smaller than amounts forwarded to

him from the mailroom or sales department.

Internal Control Procedures

7-114

187.

Internal control over cash transactions

(a.) Describe two measures contributing to strong internal control over

cash

receipts

.

(b.) Describe two measures contributing to effective internal control over

cash

disbursements

.

188.

Reporting cash in the balance sheet

(a.) The first asset shown in the balance sheet of many companies is labeled “cash and

cash equivalents.” Explain the term “cash equivalent” and give two examples. Why are

cash and cash equivalents listed

first

in the balance sheet?

(b.) The December bank statement for Kowal Publishing Co. reports a balance of

$13,847.59 at December 31, 2015. Kowal’s accounting records, however, show a balance

of $15,245.47 in the same bank account prior to preparation of the bank reconciliation.

Which amount should be included in the amount of cash reported in Kowal’s balance

sheet at December 31, 2015? Explain your answer.

189.

Bank reconciliation—classification

Indicate how the following items would be treated in a bank reconciliation. You may

choose from the following answers:

(A) Deducted from the balance per accounting records.

(B) Added to balance per accounting records.

(C) Deducted from balance per bank statement.

(D) Added to balance per bank statement.

190.

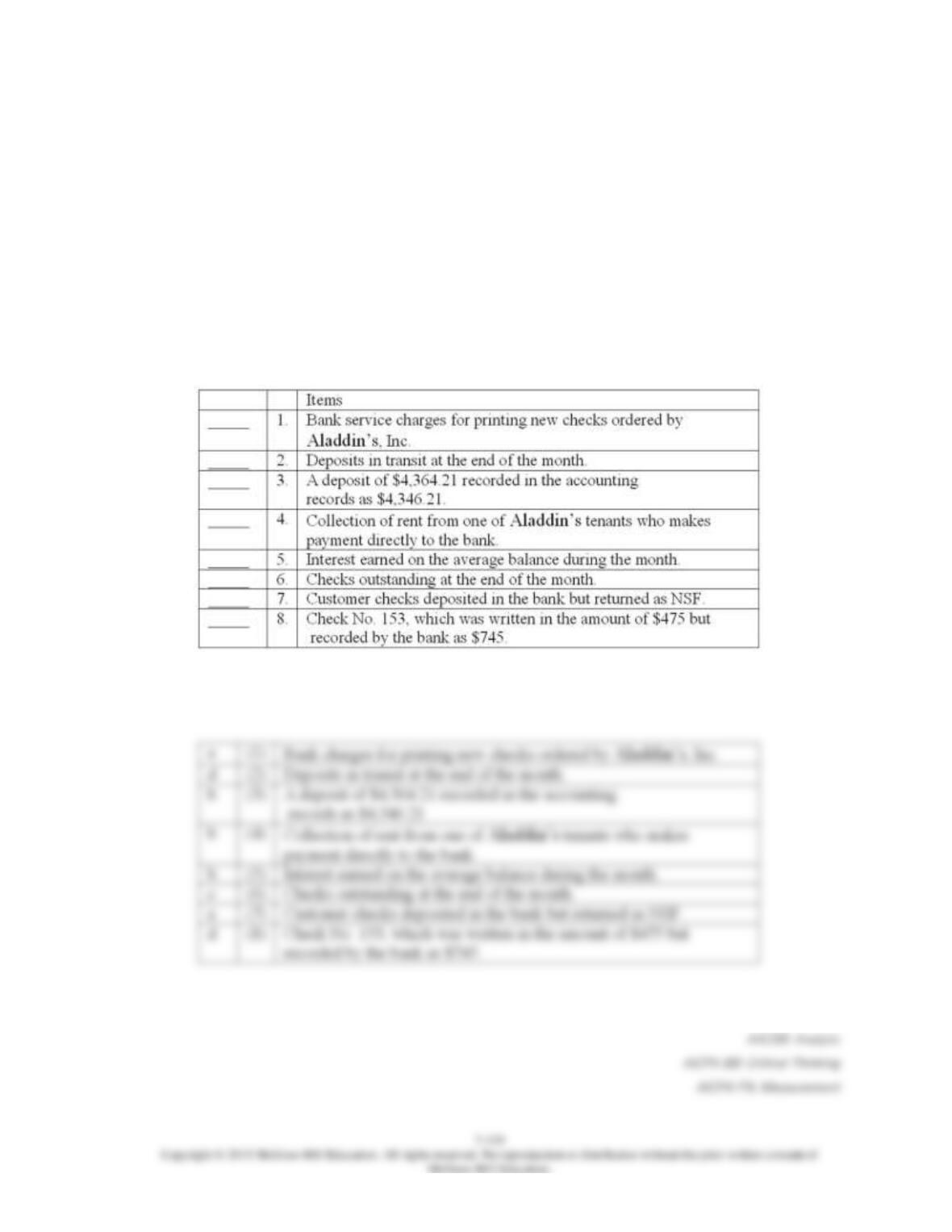

Bank reconciliation—classification

Indicate how the following items would be treated in Aladdin’s, Inc.’s bank reconciliation.

Choose from the following answers:

(a.) Deducted from the balance per accounting records.

(b.) Added to balance per accounting records.

(c.) Deducted from balance per bank statement.

(d.) Added to balance per bank statement.

191.

Bank reconciliation—computation and journal entry

The Cash account in the ledger of Arnaz Company showed a balance of $13,307 at March

31. The bank statement, however, showed a balance of $9,936 at the same date. The only

reconciling items consisted of a $4,902 deposit in transit, a bank service charge of $36,

outstanding checks totaling $2,600, and an NSF check from L. Ball, one of Arnaz’

customers.

(a) What is the amount of the adjusted cash balance on March 31?

(b) What is the amount of the NSF check?

(c) Record the journal entry necessary, if any, to adjust Arnaz Company’s accounting

records at March 31: (An explanation is not required; a single compound journal entry is

acceptable.)