106. Kurton Inc. owned 90% of Luvyn Corp.’s voting common stock. The

consideration paid exceeded book value by $110,000. Of this amount, one half is

attributable to a patent and is to be amortized over 5 years. Luvyn held 20% of

Kurton’s voting common stock which cost $28,000 more than fair value.

During the current year, Kurton reported operating income of $224,000 and

dividend income from Luvyn of $37,800. At the same time, Luvyn reported

operating income of $70,000 and dividend income from Kurton of $19,600.

Required:

Prepare a schedule to show

consolidated net income

.

107. Kurton Inc. owned 90% of Luvyn Corp.’s voting common stock. The

consideration paid exceeded book value by $110,000. Of this amount, one half is

attributable to a patent and is to be amortized over 5 years. Luvyn held 20% of

Kurton’s voting common stock which cost $28,000 more than fair value.

During the current year, Kurton reported operating income of $224,000 and

dividend income from Luvyn of $37,800. At the same time, Luvyn reported

operating income of $70,000 and dividend income from Kurton of $19,600.

Required:

Prepare a schedule to show Kurton’s share of

controlling interest in Luvyn’s net

income

.

108. Wilkins Inc. owned 60% of Motumbo Co. During the current year, Motumbo

reported net income of $280,000 but paid a total cash dividend of only $56,000.

Required:

Assuming an income tax rate of 30%, what amount of

Deferred Income Tax

Liability

arising this year must be recognized in the

consolidated balance sheet

?

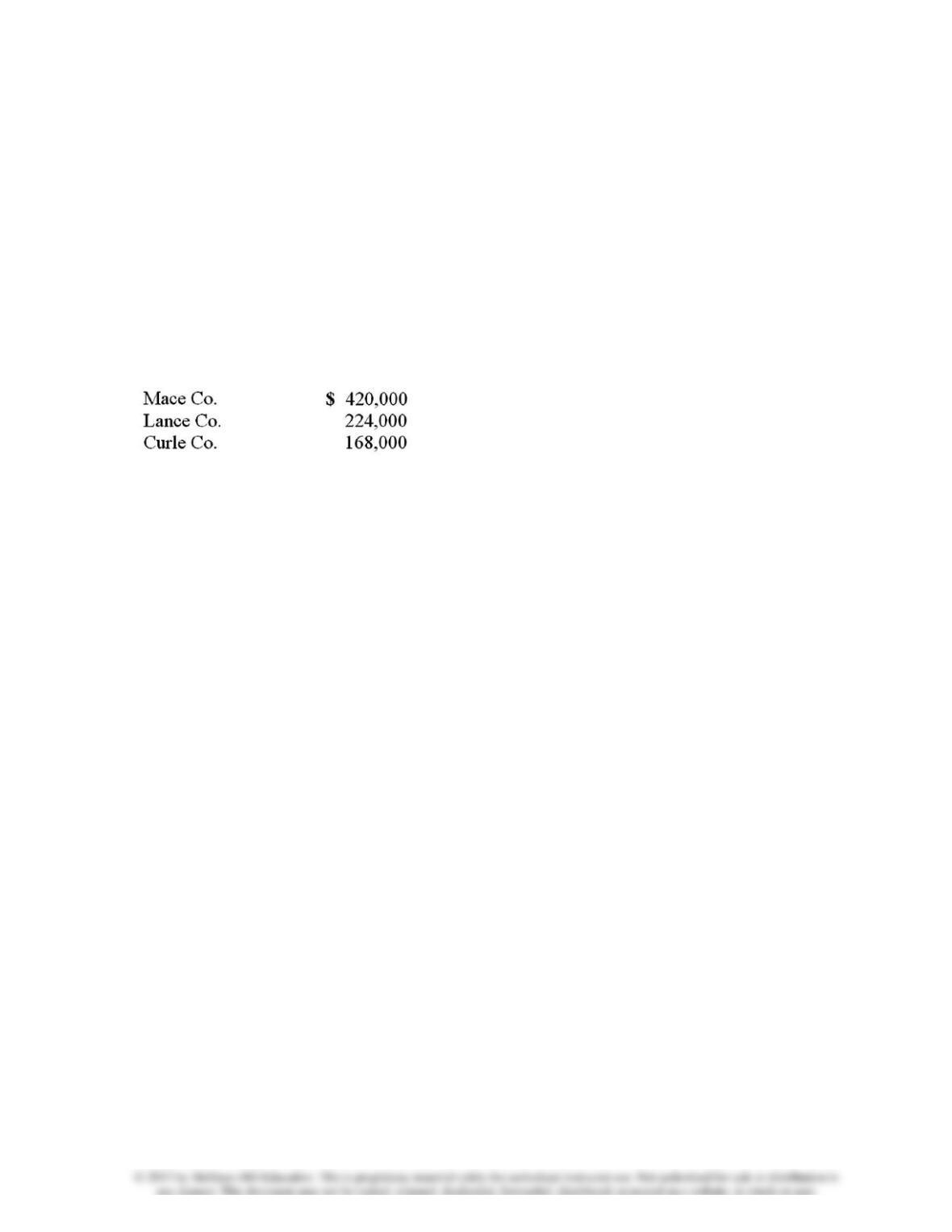

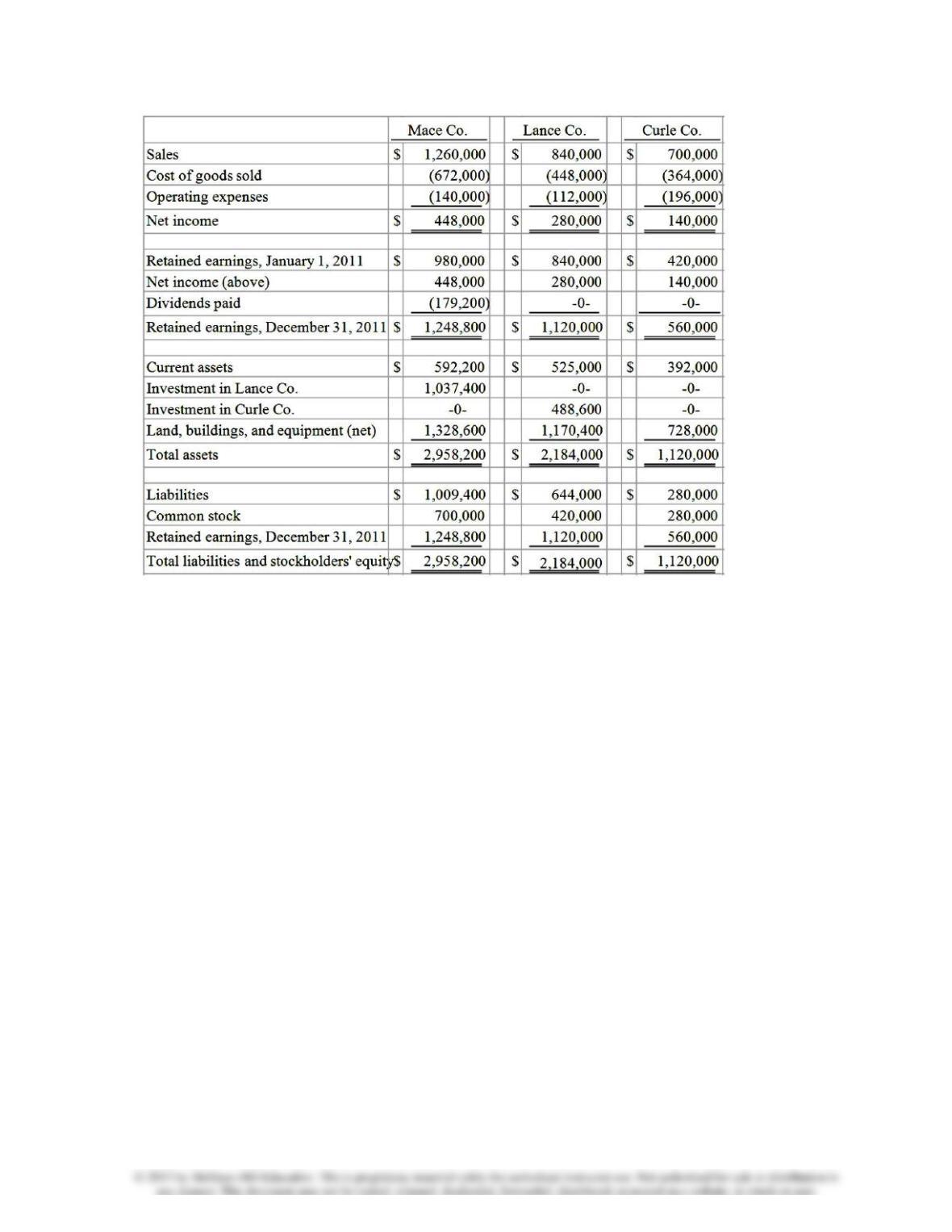

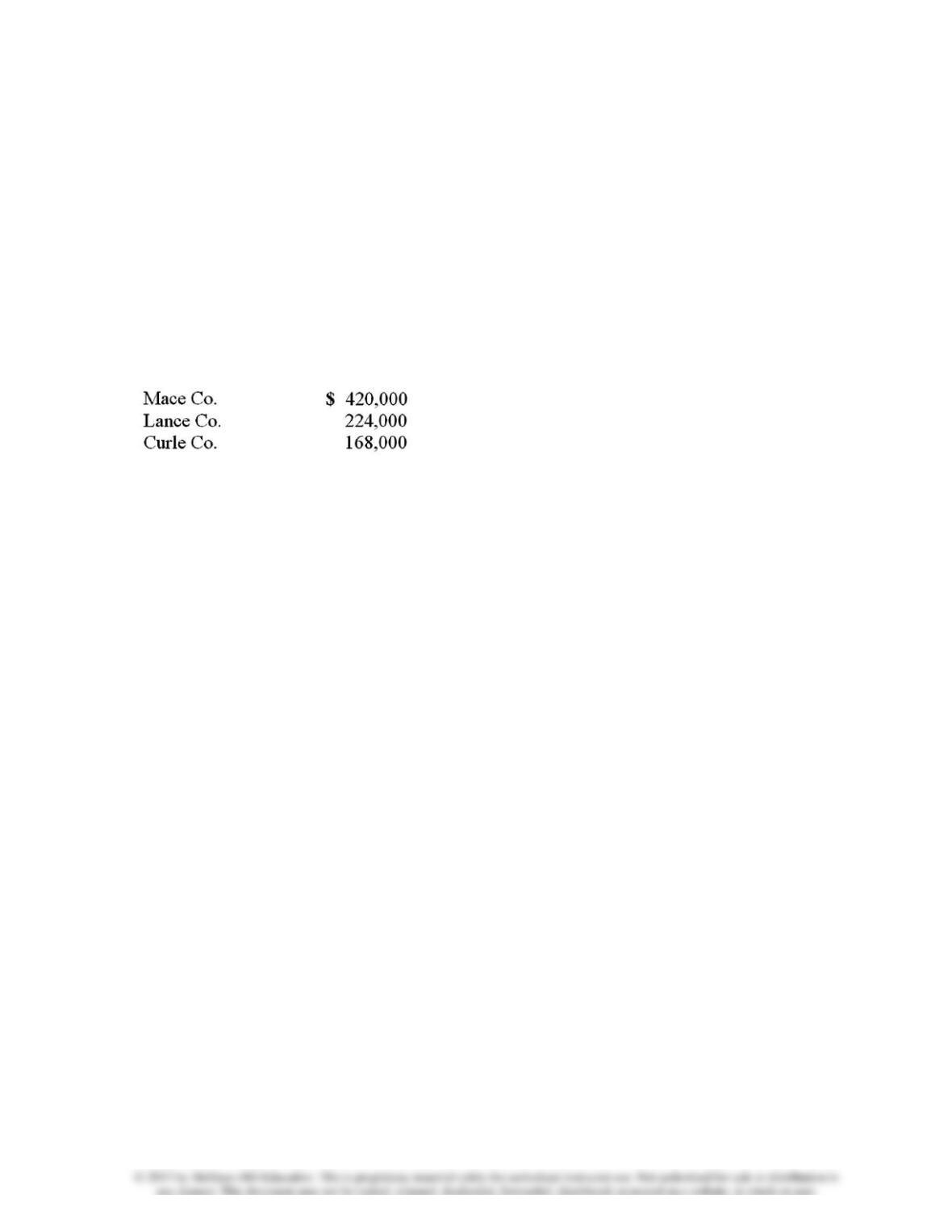

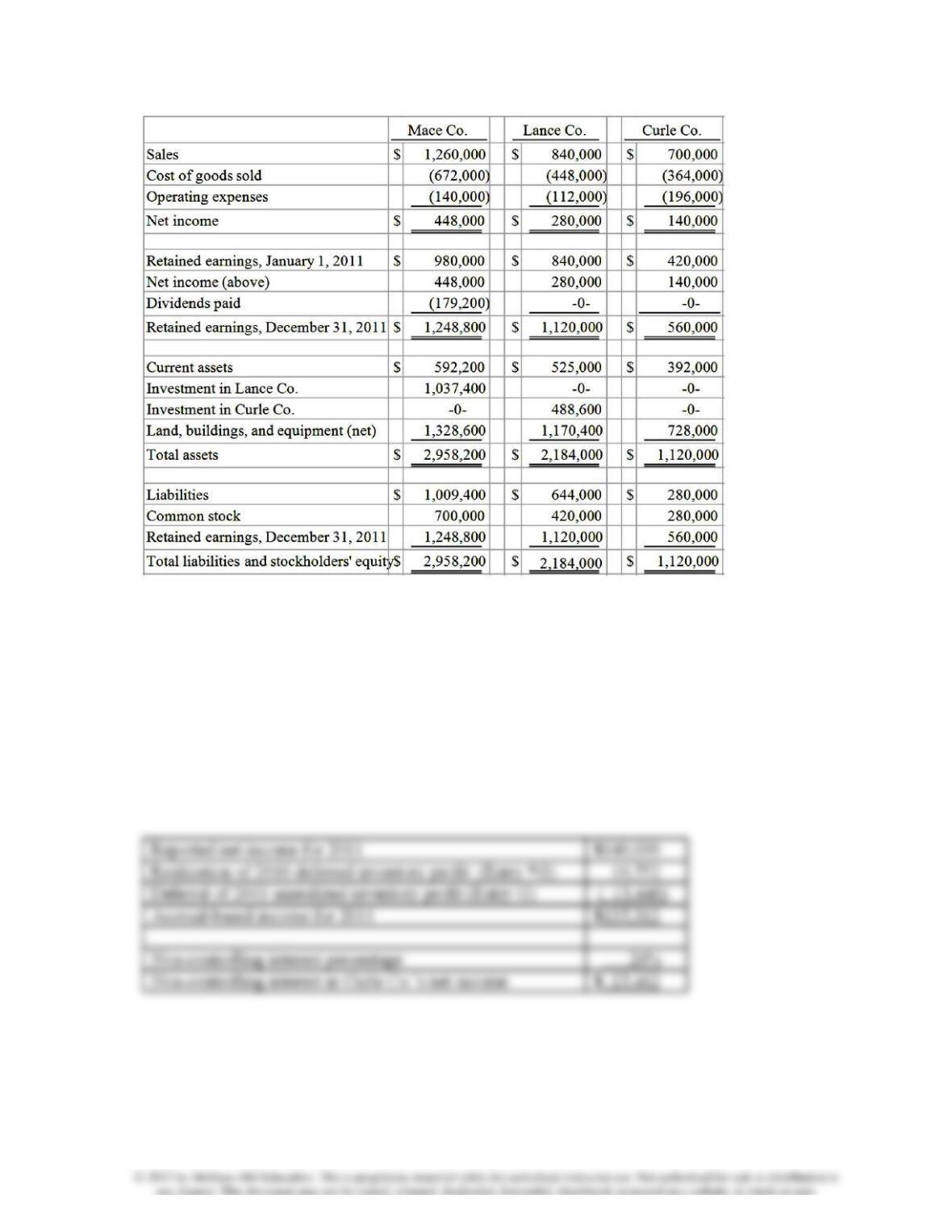

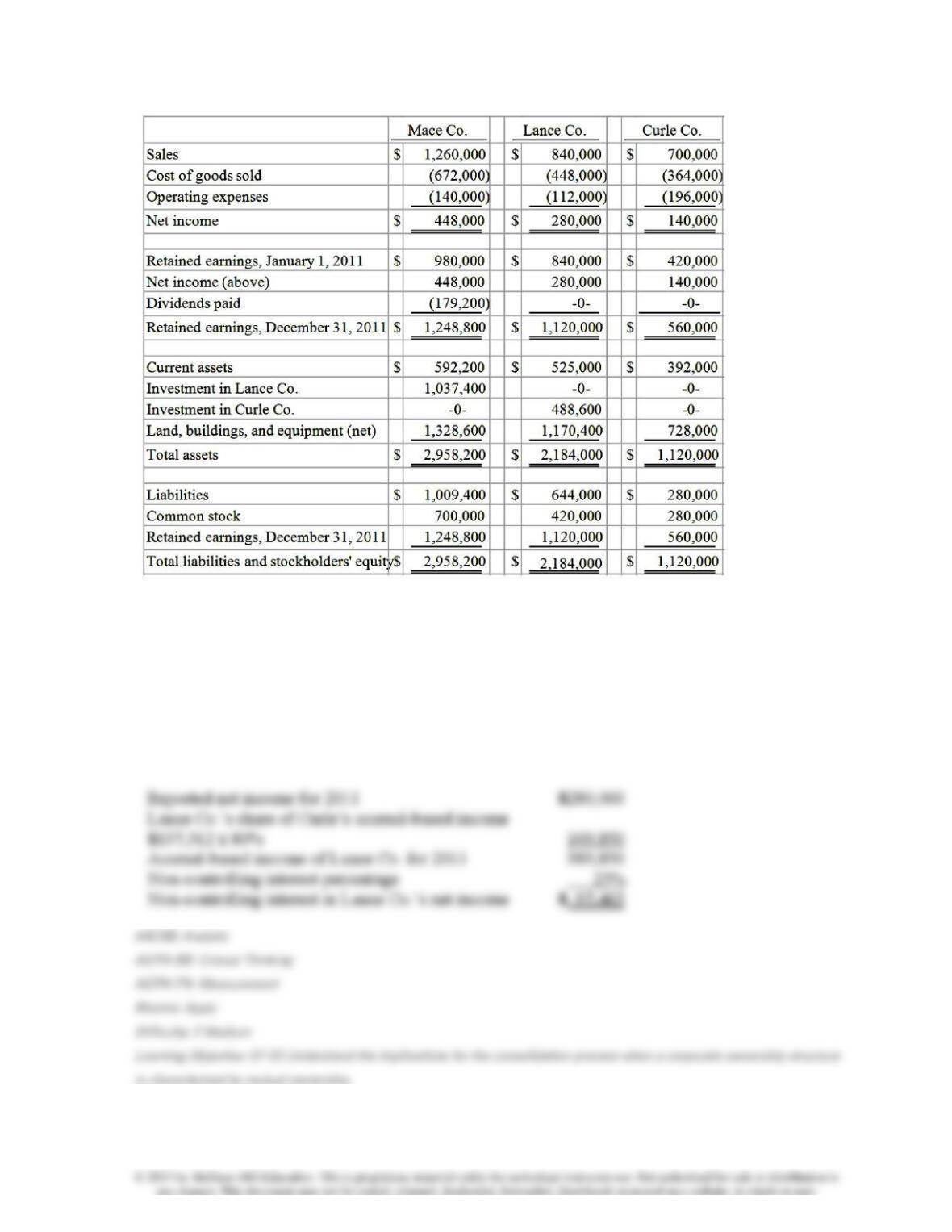

109. On January 1, 2010, Mace Co. acquired 75% of Lance Co.’s outstanding

common stock. On the same date, Lance acquired an 80% interest in Curle Co.

Both of these investments were acquired when book value was equal to fair value

of identifiable net assets acquired. Both of these investments were accounted

using the

initial value method

. No dividends were distributed by either Lance or

Curle during 2010 or 2011. Mace paid cash dividends each year equal to 40% of

operating income. Reported operating income totals for 2010 were as follows:

Following are the 2011 financial statements for these three companies. Curle

made numerous transfers of inventory to Lance since the takeover: $112,000

(2010) and $140,000 (2011). These transactions included the same markup

applicable to Curle’s outside sales. In each of these years, Lance carried 20% of

this inventory into the succeeding year before disposing of it.

An effective income tax rate of 45% was applicable to all companies.

Required:

Determine the

total

amount of goodwill

for the January 1, 2010 acquisition of

Curle Co. and for the acquisition of Lance Co. on the same date.

110. On January 1, 2010, Mace Co. acquired 75% of Lance Co.’s outstanding

common stock. On the same date, Lance acquired an 80% interest in Curle Co.

Both of these investments were acquired when book value was equal to fair value

of identifiable net assets acquired. Both of these investments were accounted

using the

initial value method

. No dividends were distributed by either Lance or

Curle during 2010 or 2011. Mace paid cash dividends each year equal to 40% of

operating income. Reported operating income totals for 2010 were as follows:

Following are the 2011 financial statements for these three companies. Curle

made numerous transfers of inventory to Lance since the takeover: $112,000

(2010) and $140,000 (2011). These transactions included the same markup

applicable to Curle’s outside sales. In each of these years, Lance carried 20% of

this inventory into the succeeding year before disposing of it.

An effective income tax rate of 45% was applicable to all companies.

Required:

Determine the

non-controlling interest in Curle Co.’s net income

for the year

2011.

111. On January 1, 2010, Mace Co. acquired 75% of Lance Co.’s outstanding

common stock. On the same date, Lance acquired an 80% interest in Curle Co.

Both of these investments were acquired when book value was equal to fair value

of identifiable net assets acquired. Both of these investments were accounted

using the

initial value method

. No dividends were distributed by either Lance or

Curle during 2010 or 2011. Mace paid cash dividends each year equal to 40% of

operating income. Reported operating income totals for 2010 were as follows:

Following are the 2011 financial statements for these three companies. Curle

made numerous transfers of inventory to Lance since the takeover: $112,000

(2010) and $140,000 (2011). These transactions included the same markup

applicable to Curle’s outside sales. In each of these years, Lance carried 20% of

this inventory into the succeeding year before disposing of it.

An effective income tax rate of 45% was applicable to all companies.

Required:

Determine the

non-controlling interest in Lace Co.’s net income

for the year

2011.

112. On January 1, 2010, Mace Co. acquired 75% of Lance Co.’s outstanding

common stock. On the same date, Lance acquired an 80% interest in Curle Co.

Both of these investments were acquired when book value was equal to fair value

of identifiable net assets acquired. Both of these investments were accounted

using the

initial value method

. No dividends were distributed by either Lance or

Curle during 2010 or 2011. Mace paid cash dividends each year equal to 40% of

operating income. Reported operating income totals for 2010 were as follows:

Following are the 2011 financial statements for these three companies. Curle

made numerous transfers of inventory to Lance since the takeover: $112,000

(2010) and $140,000 (2011). These transactions included the same markup

applicable to Curle’s outside sales. In each of these years, Lance carried 20% of

this inventory into the succeeding year before disposing of it.

An effective income tax rate of 45% was applicable to all companies.