115. If Dunford has a limit of 30,000 machine hours but no limit on units sold or direct labor

hours, then the ranking of the products from the most profitable to the least profitable use of the

constrained resource is:

116. How much profit (loss) does the company make by processing one batch of sugar beets

into the end products industrial fiber and refined sugar?

117. How much profit (loss) does the company make by processing the intermediate product

beet juice into refined sugar rather than selling it as is?

7-103

118. Which of the intermediate products should be processed further?

Resendes Refiners, Inc., processes sugar cane that it purchases from farmers. Sugar cane

is processed in batches. A batch of sugar cane costs $48 to buy from farmers and $16 to crush in

the company’s plant. Two intermediate products, cane fiber and cane juice, emerge from the

crushing process. The cane fiber can be sold as is for $24 or processed further for $17 to make

the end product industrial fiber that is sold for $38. The cane juice can be sold as is for $34 or

processed further for $23 to make the end product molasses that is sold for $76.

7-104

119. How much profit (loss) does the company make by processing one batch of sugar cane

into the end products industrial fiber and molasses?

120. How much profit (loss) does the company make by processing the intermediate product

cane juice into molasses rather than selling it as is?

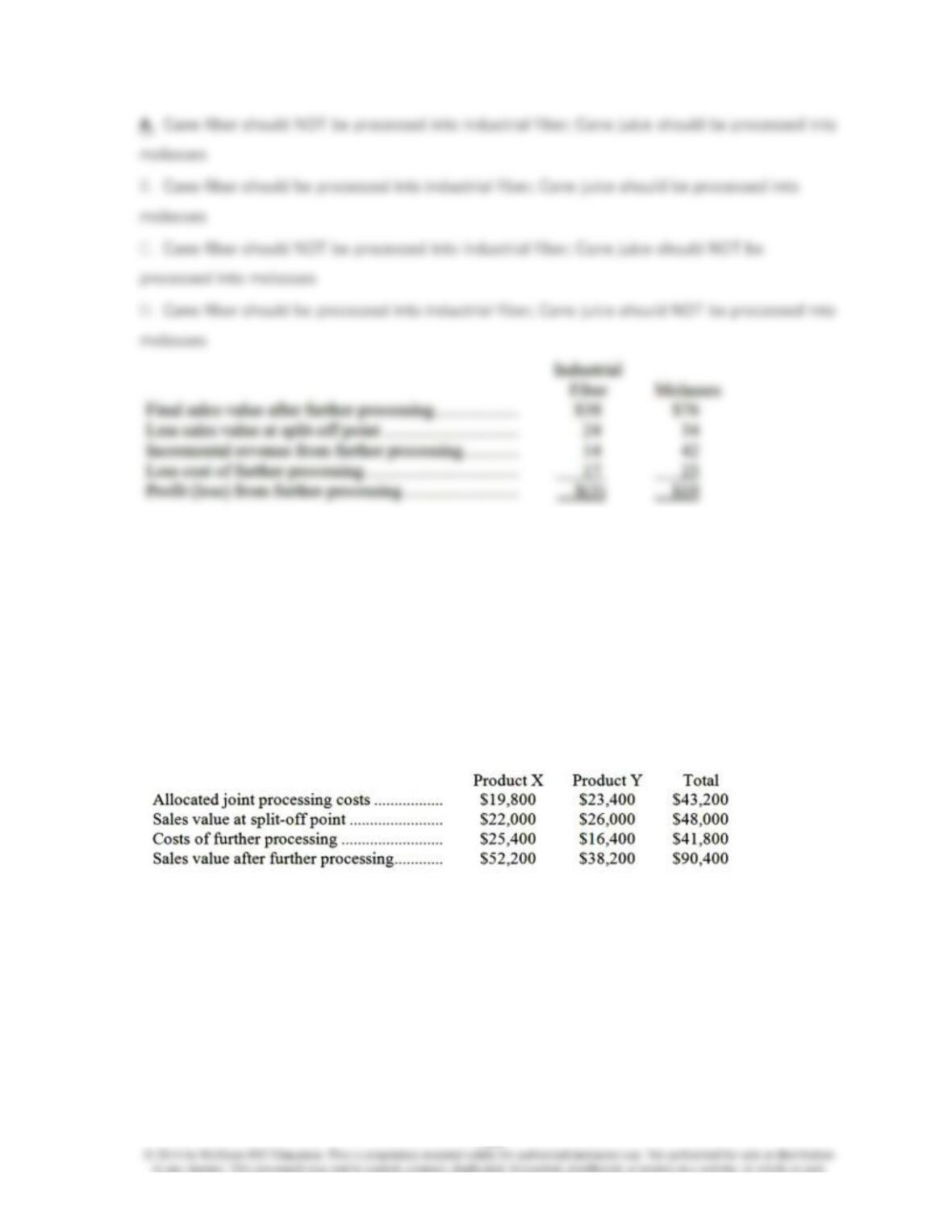

121. Which of the intermediate products should be processed further?

7-105

Cane fiber should NOT be processed into industrial fiber; Cane juice should be processed into

molasses.

Dodrill Company makes two products from a common input. Joint processing costs up to the

split-off point total $43,200 a year. The company allocates these costs to the joint products on

the basis of their total sales values at the split-off point. Each product may be sold at the split–off

point or processed further. Data concerning these products appear below:

122. What is the net monetary advantage (disadvantage) of processing Product X beyond the

split-off point?

123. What is the net monetary advantage (disadvantage) of processing Product Y beyond the

split-off point?

124. What is the minimum amount the company should accept for Product X if it is to be sold

at the split-off point?

7-108

125. If N is processed further and then sold, rather than being sold at the split-off point, the

change in monthly operating income would be a:

126. What would the selling price per unit of product N need to be after further processing in

order for Payne Company to be economically indifferent between selling N at the split-off point or

processing N further?

Profit from further processing

The company would be indifferent between selling Product N at the split-off point or processing

Product N further when the sales value at the split-off point equals the incremental profit that

the company could earn by processing further.

Sales value at split-off point = Final sales value after further processing – Cost of further

processing

$3.20 = Final sales value after further processing – $2.50

Final sales value after further processing = $3.20 + $2.50 = $5.70

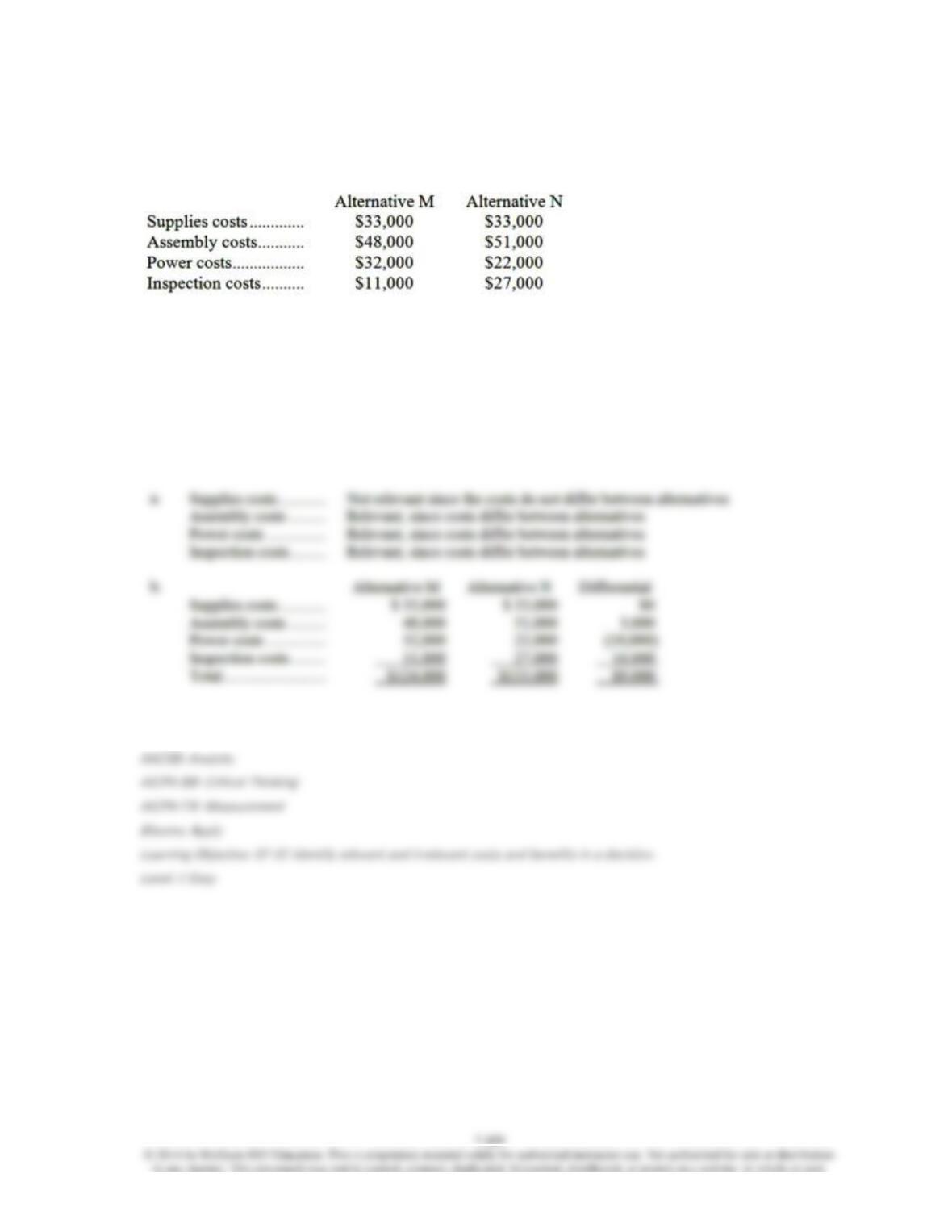

127. Marcell Corporation is considering two alternatives that are code-named M and N. Costs

associated with the alternatives are listed below:

Required:

a. Which costs are relevant and which are not relevant in the choice between these two

alternatives?

b. What is the differential cost between the two alternatives?

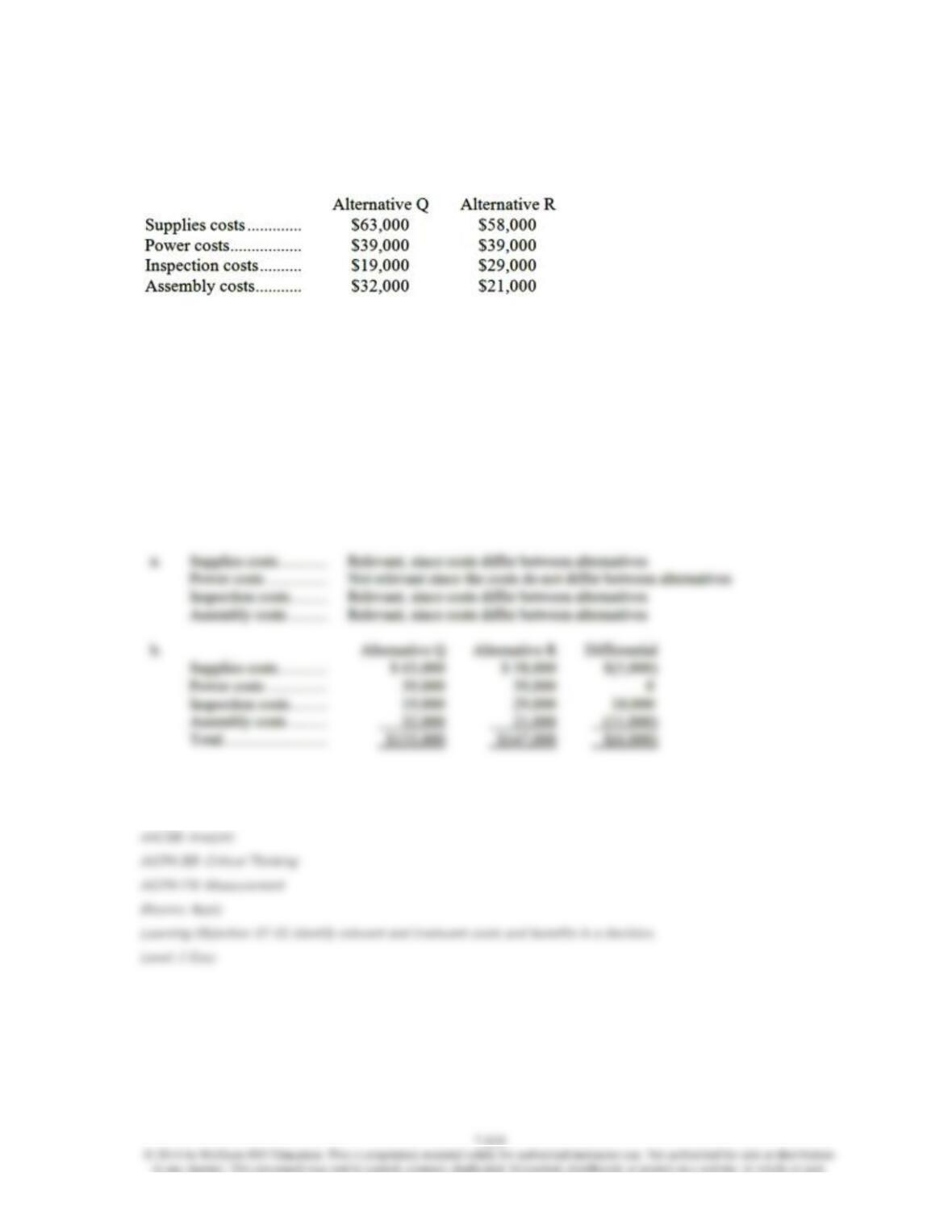

128. Costs associated with two alternatives, code-named Q and R, being considered by

Corniel Corporation are listed below:

Required:

a. Which costs are relevant and which are not relevant in the choice between these two

alternatives?

b. What is the differential cost between the two alternatives?

129. The management of Therriault Corporation is considering dropping product U51Y. Data

from the company’s accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company’s accounting

system. Further investigation has revealed that $280,000 of the fixed manufacturing expenses

and $140,000 of the fixed selling and administrative expenses are avoidable if product U51Y is

discontinued.

Required:

What would be the effect on the company’s overall net operating income if product U51Y were

dropped? Should the product be dropped? Show your work!

7-112

130. Nutall Corporation is considering dropping product N28X. Data from the company’s

accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company’s accounting

system. Further investigation has revealed that $199,000 of the fixed manufacturing expenses

and $114,000 of the fixed selling and administrative expenses are avoidable if product N28X is

discontinued.

Required:

a. According to the company’s accounting system, what is the net operating income earned by

product N28X? Show your work!

b. What would be the effect on the company’s overall net operating income of dropping product

N28X? Should the product be dropped? Show your work!

7-113

131. The management of Rodarmel Corporation is considering dropping product G91Q. Data

from the company’s accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company’s accounting

system. Further investigation has revealed that $57,000 of the fixed manufacturing expenses and

$40,000 of the fixed selling and administrative expenses are avoidable if product G91Q is

discontinued.

Required:

a. What is the net operating income earned by product G91Q according to the company’s

accounting system? Show your work!

b. What would be the effect on the company’s overall net operating income of dropping product

G91Q? Should the product be dropped? Show your work!

7-114

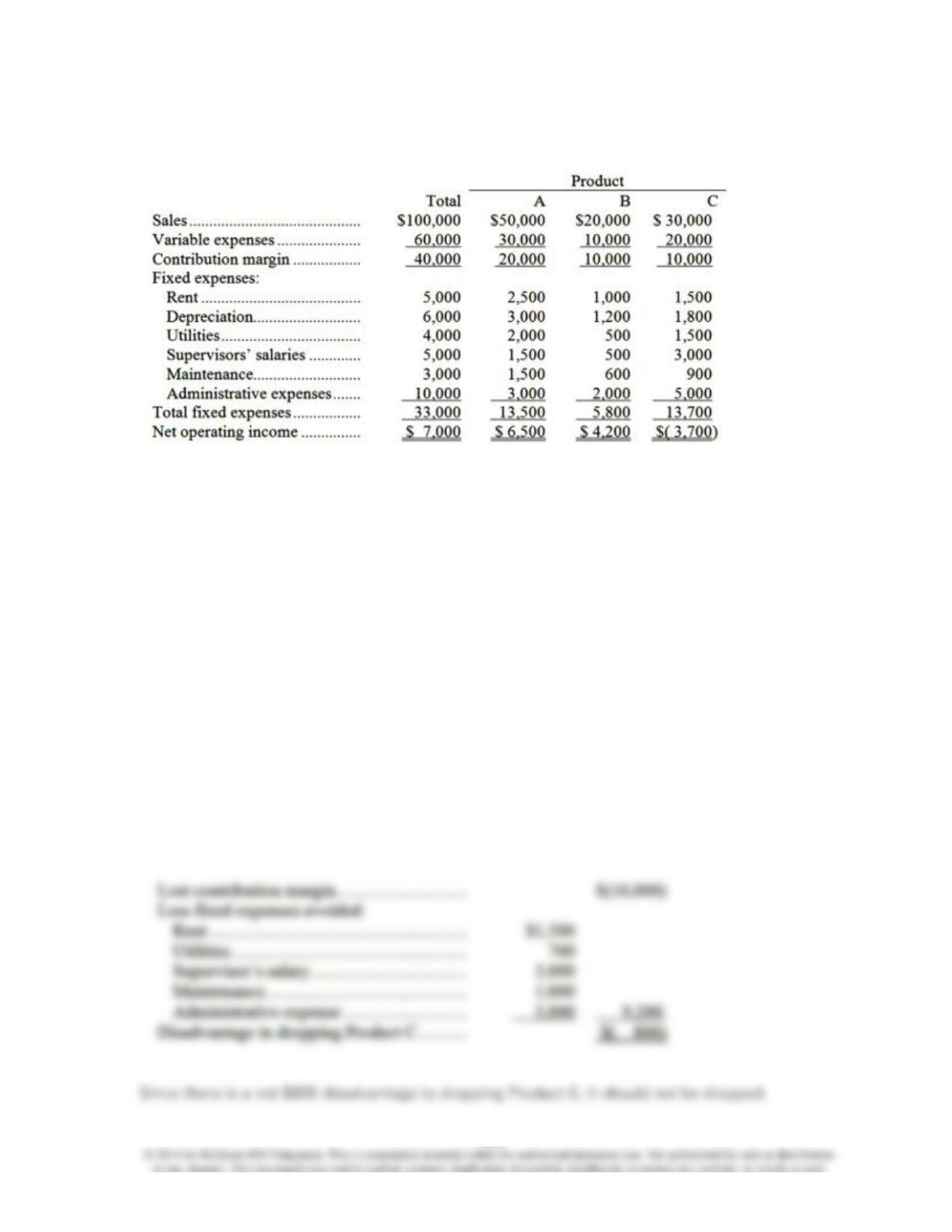

132. Mr. Earl Pearl, accountant for Margie Knall Co., Inc., has prepared the following product-

line income data:

The following additional information is available:

* The factory rent of $1,500 assigned to Product C is avoidable if the product were dropped.

* The company’s total depreciation would not be affected by dropping C.

* Eliminating Product C will reduce the monthly utility bill from $1,500 to $800.

* All supervisors’ salaries are avoidable.

* If Product C is discontinued, the maintenance department will be able to reduce monthly

expenses from $3,000 to $2,000.

* Elimination of Product C will make it possible to cut two persons from the administrative staff;

their combined salaries total $3,000.

Required:

Prepare an analysis showing whether Product C should be eliminated.

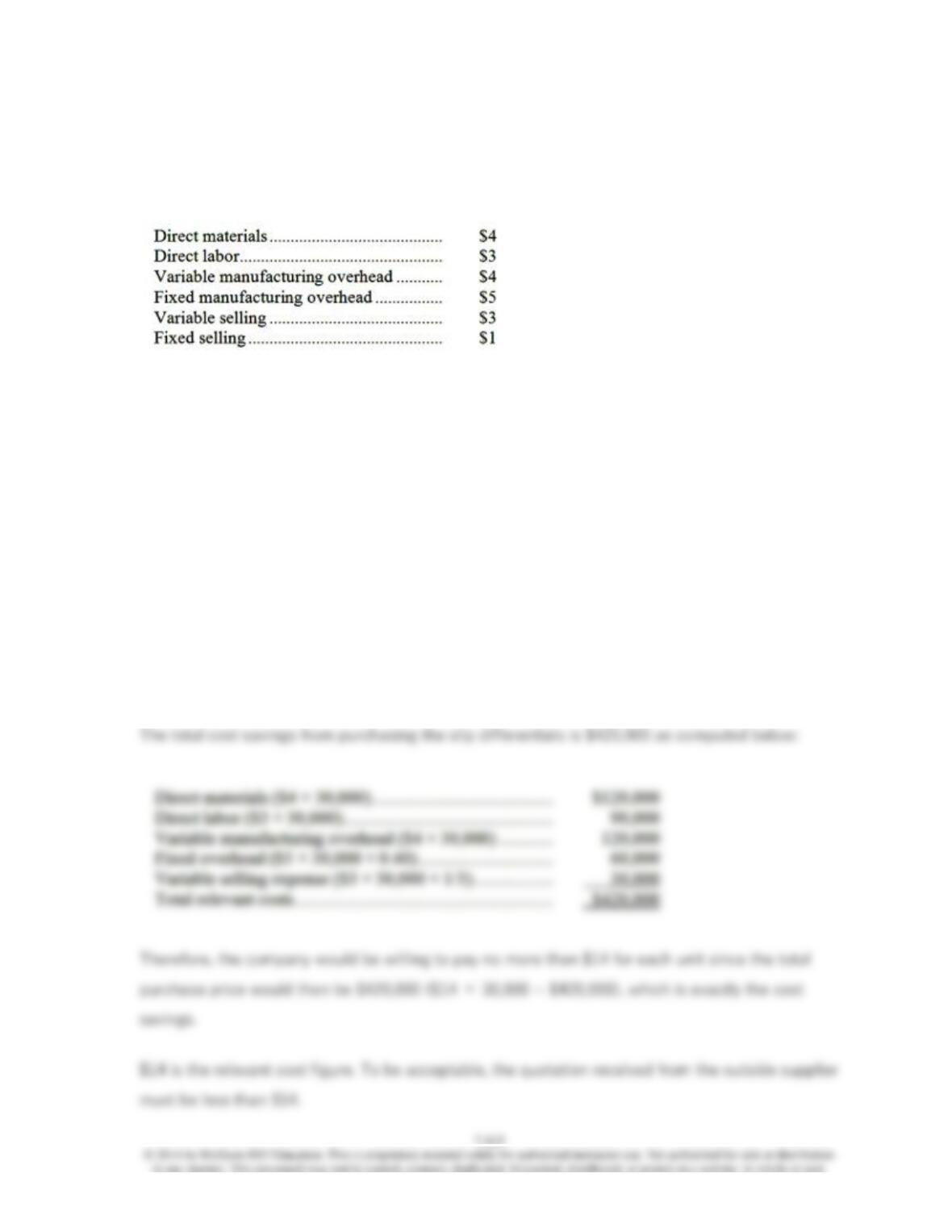

133. The Hayes Company manufactures and sells several products, one of which is called a

slip differential. The company normally sells 30,000 units of the slip differential each month. At

this activity level, unit costs are:

An outside supplier has offered to produce the slip differentials for the Hayes Company, and to

ship them directly to the Hayes Company’s customers. This arrangement would permit the Hayes

Company to reduce its variable selling expenses by one third (due to elimination of freight costs).

The facilities now being used to produce the slip differentials would be idle and fixed

manufacturing overhead would continue at 60 percent of its present level. The total fixed selling

expenses of the company would be unaffected by this decision.

Required:

What is the maximum acceptable price quotation for the slip differentials from the outside

supplier?

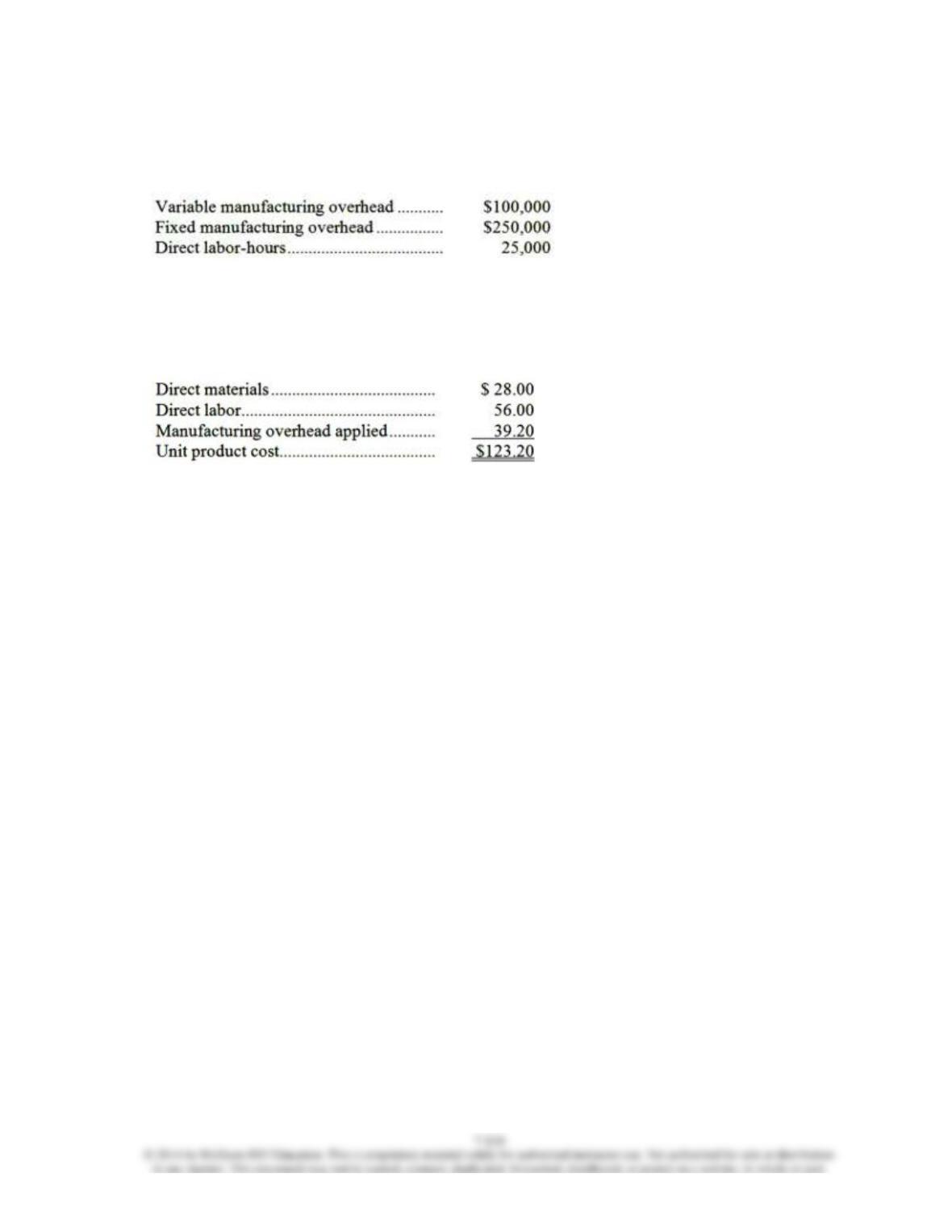

134. Bady Inc. makes a range of products. The company’s predetermined overhead rate is $14

per direct labor-hour, which was calculated using the following budgeted data:

Component M3 is used in one of the company’s products. The unit cost of the component

according to the company’s cost accounting system is determined as follows:

An outside supplier has offered to supply component M3 for $108 each. The outside supplier is

known for quality and reliability. Assume that direct labor is a variable cost, variable

manufacturing overhead is really driven by direct labor-hours, and total fixed manufacturing

overhead would not be affected by this decision. Bady chronically has idle capacity.

Required:

Is the offer from the outside supplier financially attractive? Why?

7-118

135. Kramer Company makes 4,000 units per year of a part called an axial tap for use in one of

its products. Data concerning the unit production costs of the axial tap follow:

An outside supplier has offered to sell Kramer Company all of the axial taps it requires. If Kramer

Company decided to discontinue making the axial taps, 40% of the above fixed manufacturing

overhead costs could be avoided. Assume that direct labor is a variable cost.

Required:

a. Assume Kramer Company has no alternative use for the facilities presently devoted to

production of the axial taps. If the outside supplier offers to sell the axial taps for $65 each,

should Kramer Company accept the offer? Fully support your answer with appropriate

calculations.

b. Assume that Kramer Company could use the facilities presently devoted to production of the

axial taps to expand production of another product that would yield an additional contribution

margin of $80,000 annually. What is the maximum price Kramer Company should be willing to pay

the outside supplier for axial taps?

7-120

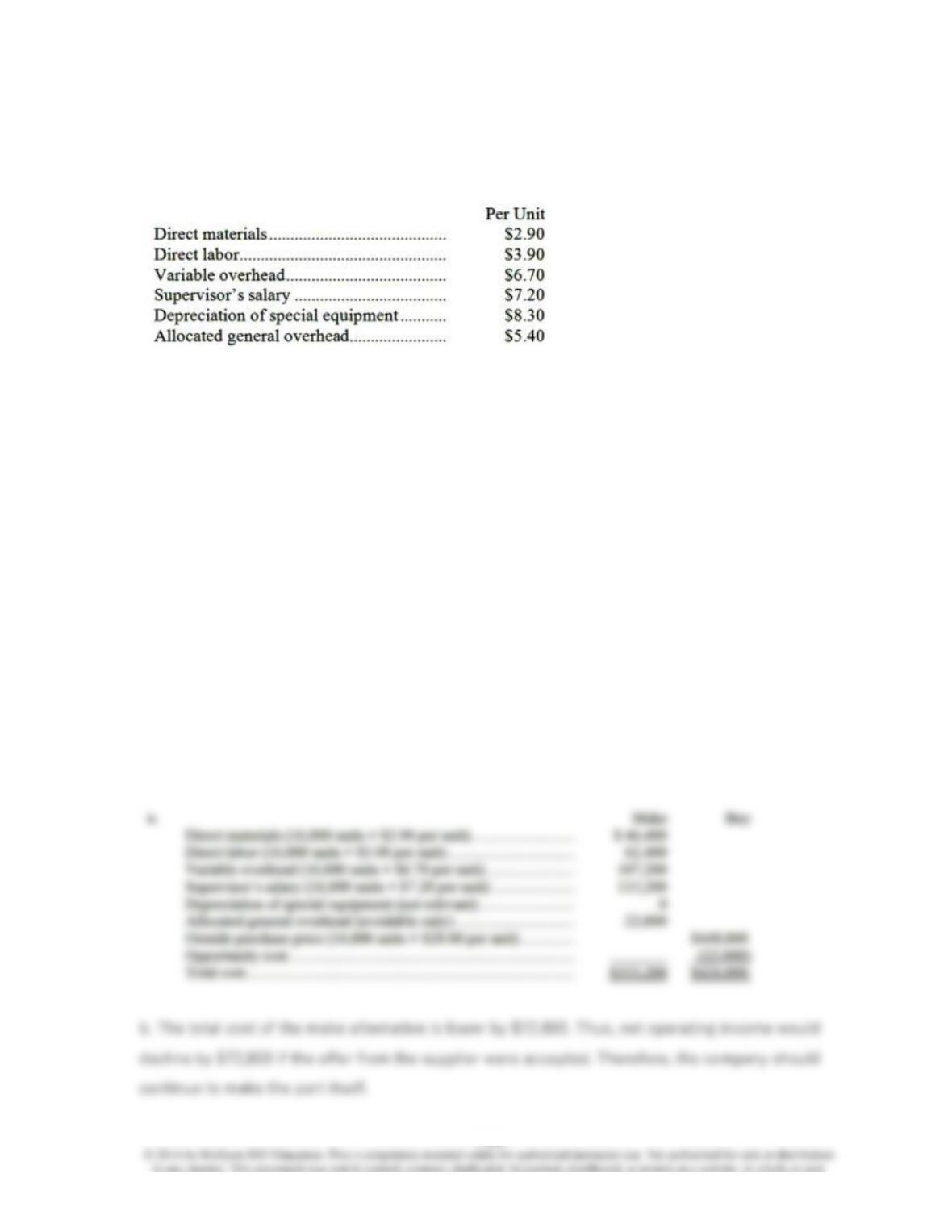

136. Masse Corporation uses part G18 in one of its products. The company’s Accounting

Department reports the following costs of producing the 16,000 units of the part that are needed

every year.

An outside supplier has offered to make the part and sell it to the company for $28.00 each. If

this offer is accepted, the supervisor’s salary and all of the variable costs, including direct labor,

can be avoided. The special equipment used to make the part was purchased many years ago

and has no salvage value or other use. The allocated general overhead represents fixed costs of

the entire company. If the outside supplier’s offer were accepted, only $22,000 of these allocated

general overhead costs would be avoided. In addition, the space used to produce part G18 could

be used to make more of one of the company’s other products, generating an additional segment

margin of $22,000 per year for that product.

Required:

a. Prepare a report that shows the effect on the company’s total net operating income of buying

part G18 from the supplier rather than continuing to make it inside the company.

b. Which alternative should the company choose?