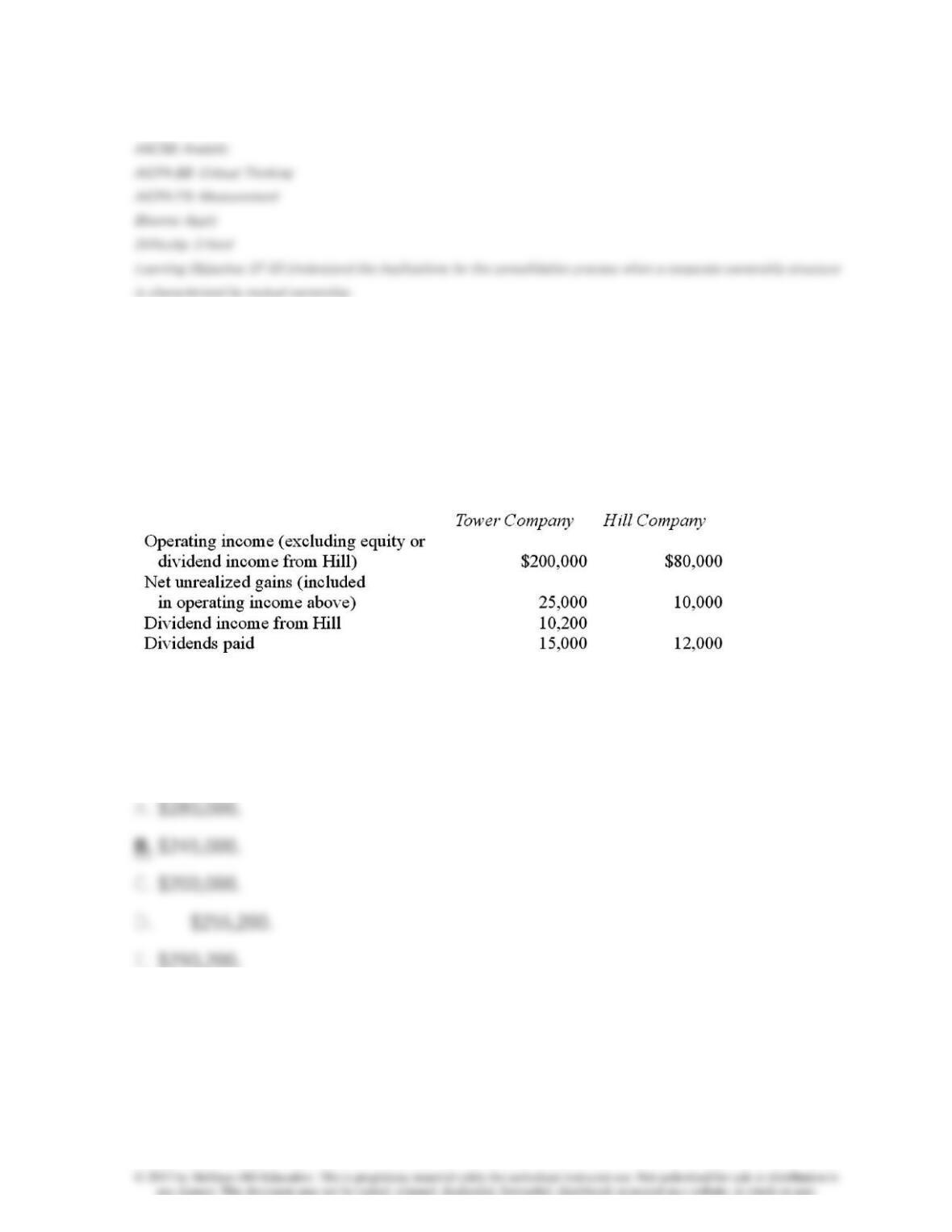

42. Tower Company owns 85% of Hill Company. The two companies engaged

in several intra-entity transactions. Each company’s operating and dividend

income for the current time period follow, as well as the effects of unrealized

gains. No income tax accruals have been recognized within these totals. The tax

rate for each company is 30%.

Compute accrual-based consolidated net income.

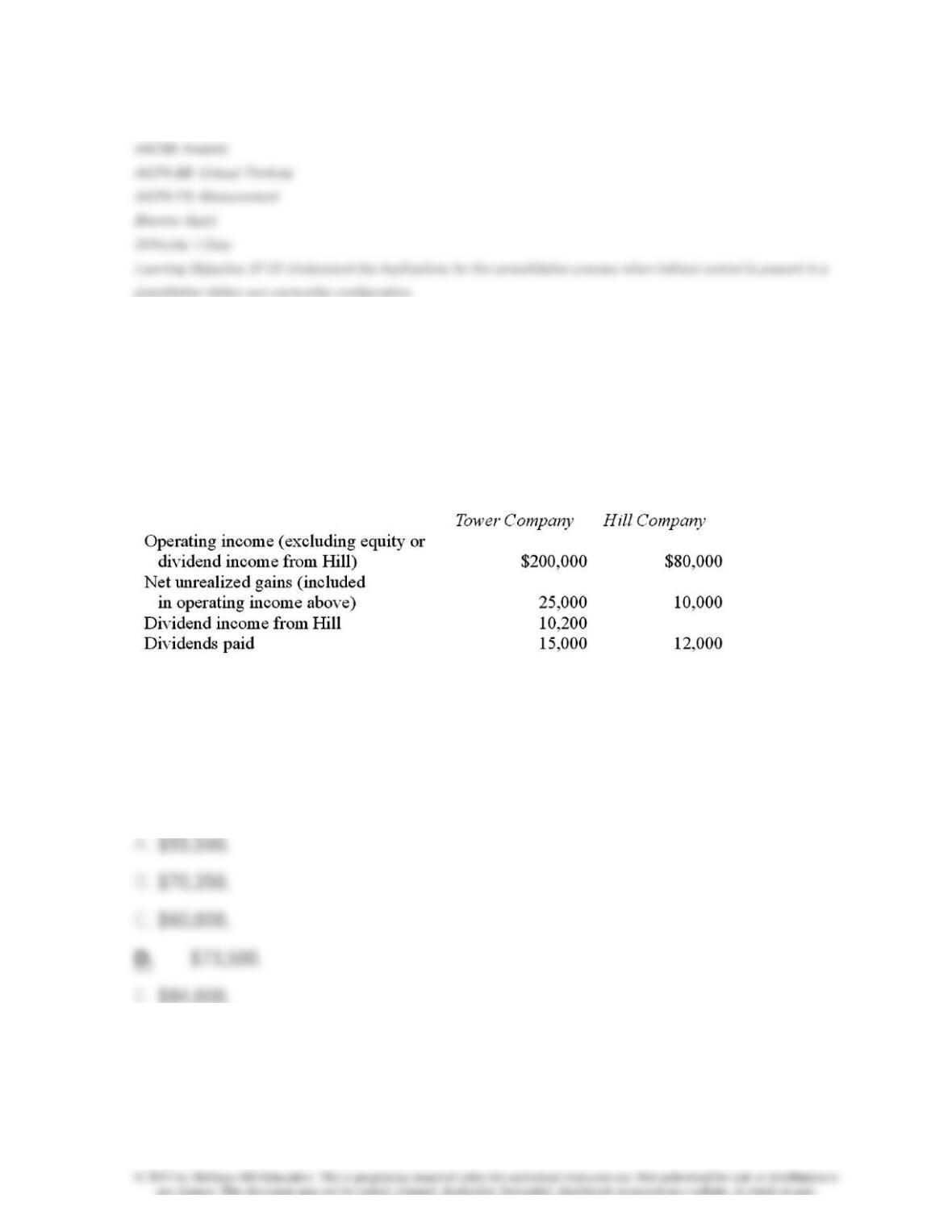

43. Tower Company owns 85% of Hill Company. The two companies engaged

in several intra-entity transactions. Each company’s operating and dividend

income for the current time period follow, as well as the effects of unrealized

gains. No income tax accruals have been recognized within these totals. The tax

rate for each company is 30%.

What is the tax liability for the current year if consolidated tax returns are

prepared?

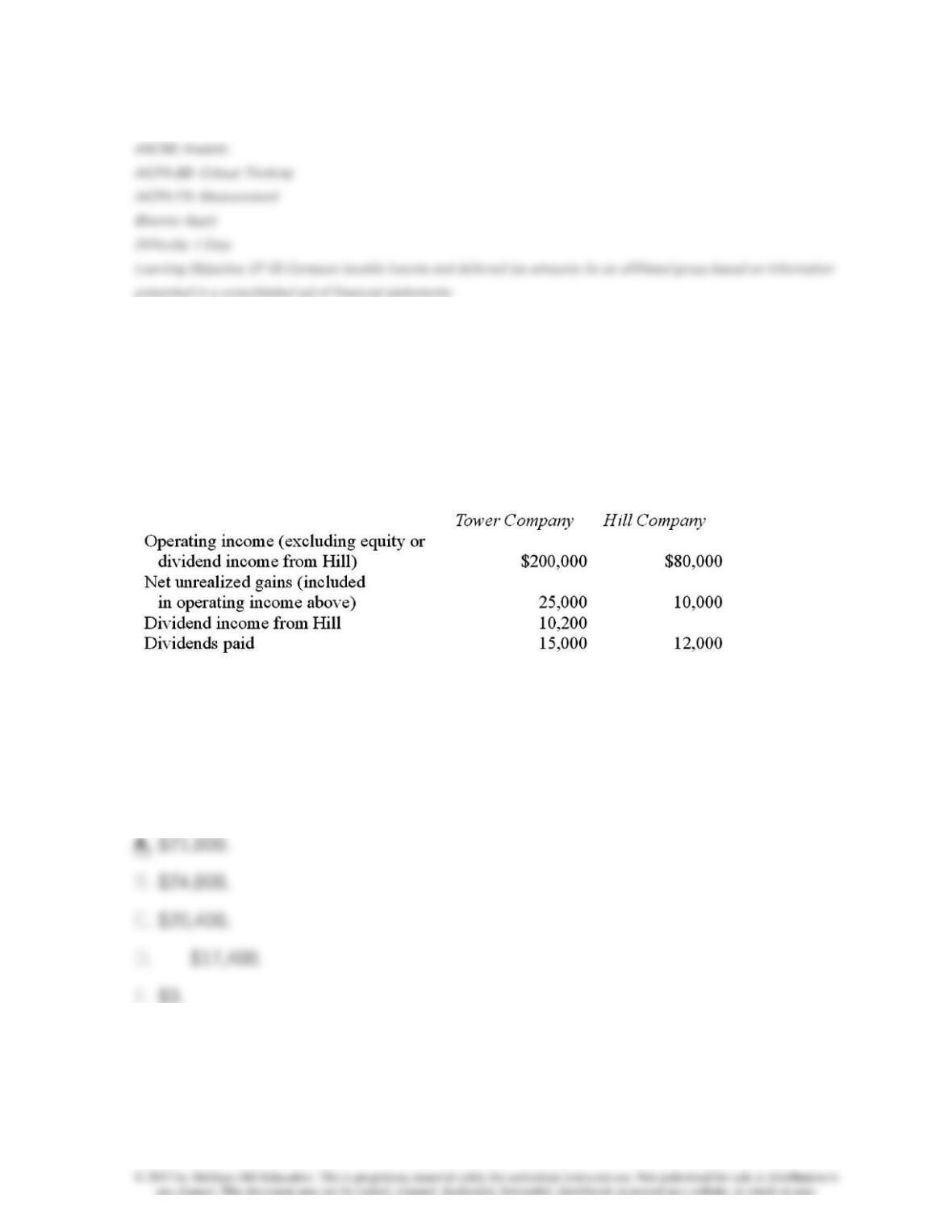

44. Tower Company owns 85% of Hill Company. The two companies engaged

in several intra-entity transactions. Each company’s operating and dividend

income for the current time period follow, as well as the effects of unrealized

gains. No income tax accruals have been recognized within these totals. The tax

rate for each company is 30%.

Using percentage allocation method, how much income tax expense is assigned

to Hill?

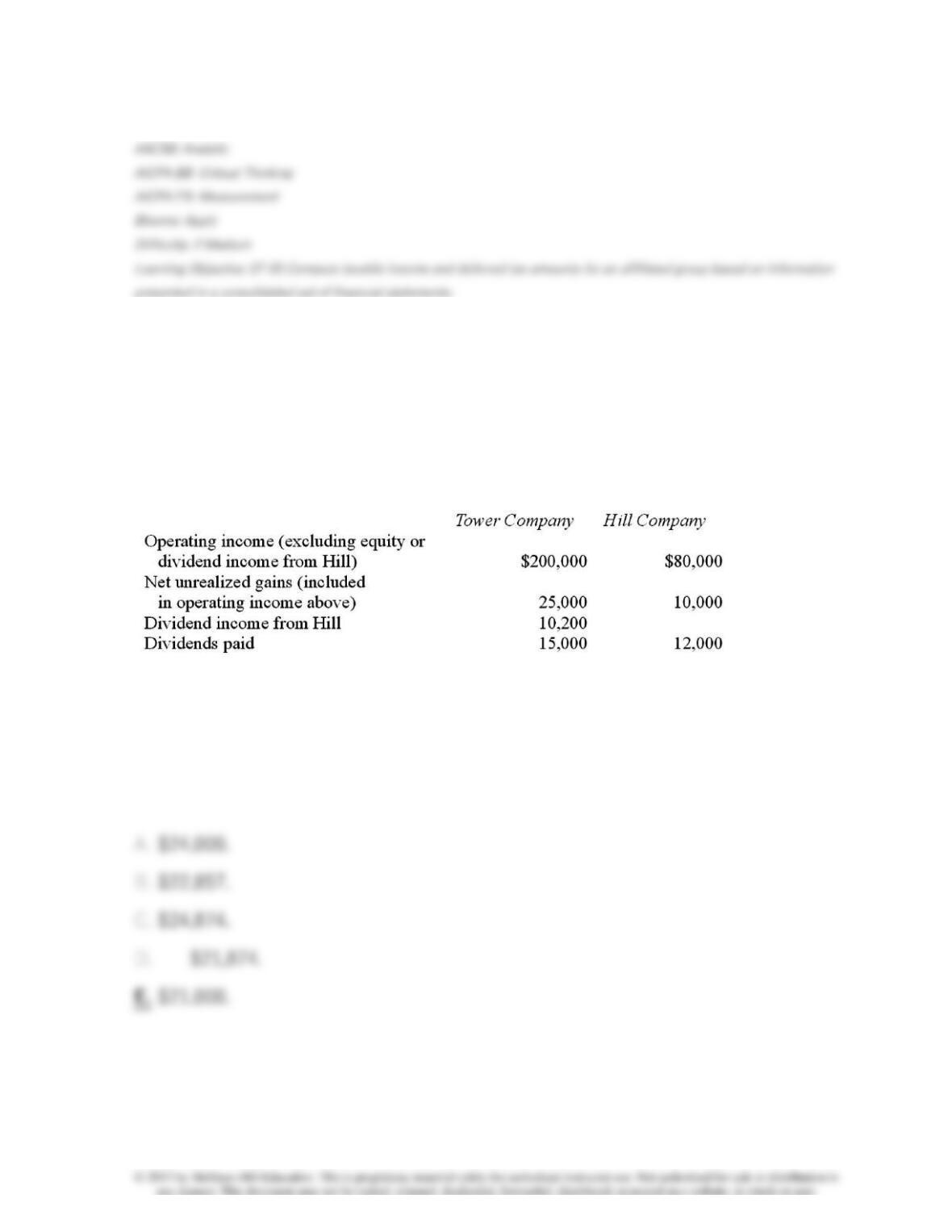

45. Tower Company owns 85% of Hill Company. The two companies engaged

in several intra-entity transactions. Each company’s operating and dividend

income for the current time period follow, as well as the effects of unrealized

gains. No income tax accruals have been recognized within these totals. The tax

rate for each company is 30%.

Under the separate return method, how much income tax expense will be

assigned to Hill?

46. White Company owns 60% of Cody Company. Separate tax returns are

required. For 2010, White’s operating income (excluding taxes and any income

from Cody) was $300,000 while Cody reported a pretax income of $125,000.

During the period, Cody paid a total of $25,000 in cash dividends; $15,000 (60%)

to White and $10,000 to the non-controlling interest. White paid dividends of

$180,000. The income tax rate for both companies is 30%.

Compute Cody’s income tax expense for 2011.

47. White Company owns 60% of Cody Company. Separate tax returns are

required. For 2010, White’s operating income (excluding taxes and any income

from Cody) was $300,000 while Cody reported a pretax income of $125,000.

During the period, Cody paid a total of $25,000 in cash dividends; $15,000 (60%)

to White and $10,000 to the non-controlling interest. White paid dividends of

$180,000. The income tax rate for both companies is 30%.

Compute Cody’s undistributed earnings for 2011.

48. White Company owns 60% of Cody Company. Separate tax returns are

required. For 2010, White’s operating income (excluding taxes and any income

from Cody) was $300,000 while Cody reported a pretax income of $125,000.

During the period, Cody paid a total of $25,000 in cash dividends; $15,000 (60%)

to White and $10,000 to the non-controlling interest. White paid dividends of

$180,000. The income tax rate for both companies is 30%.

Compute the income tax payable by White for 2011.

49. White Company owns 60% of Cody Company. Separate tax returns are

required. For 2010, White’s operating income (excluding taxes and any income

from Cody) was $300,000 while Cody reported a pretax income of $125,000.

During the period, Cody paid a total of $25,000 in cash dividends; $15,000 (60%)

to White and $10,000 to the non-controlling interest. White paid dividends of

$180,000. The income tax rate for both companies is 30%.

Compute White’s deferred income taxes for 2011.

50. Woods Company has one depreciable asset valued at $800,000. Because of

recent losses, the company has a net operating loss carry-forward of $150,000.

The tax rate is 30%. The company was acquired for $1,000,000. It is likely the

benefit will be realized. Compute the goodwill realized in consolidation.

51. Under current U.S. tax law for consolidated tax returns:

52. Strong Company has had poor operating results in recent years and has a

$160,000 net operating loss carry-forward. Leader Corp. pays $700,000 to acquire

Strong and is optimistic about its future profitability potential. The book value and

fair value of Strong’s identifiable net assets is $500,000 at date of acquisition.

Strong’s tax rate is 30% and Leader’s tax rate is 40%. What is goodwill resulting

from this business combination?

53. According to International Financial Reporting Standards: In the

consolidation process for subsidiaries that are indirectly controlled:

54. In a father-son-grandson combination, which of the following statements is

true?

55. Which of the following statements is true concerning connecting affiliations

and mutual ownerships?

56. Which of the following is true concerning the treasury stock approach in

accounting for a subsidiary’s investment in parent company stock?

57. Which of the following is

not

an advantage of filing a consolidated income

tax return?

58. On January 1, 2011, a subsidiary buys 8 percent of the outstanding voting

stock of its parent corporation. The payment of $350,000 exceeded book value of

the acquired shares by $50,000, attributable to a copyright with a 10-year useful

life. During the year, the parent reported operating income of $675,000 (excluding

investment income from the subsidiary), and paid $100,000 in dividends. If the

treasury stock approach is used, how is the Investment in Parent Stock reported

in the consolidated balance sheet at December 31, 2011?

59. On January 1, 2011, a subsidiary buys 12 percent of the outstanding voting

stock of its parent corporation. The payment of $400,000 exceeded book value of

the acquired shares by $80,000, attributable to a copyright with a 10-year useful

life. During the year, the parent reported operating income of $1,000,000

(excluding investment income from the subsidiary), and paid $120,000 in

dividends. If the treasury stock approach is used, how is the Investment in Parent

Stock reported in the consolidated balance sheet at December 31, 2011?

60. Which of the following conditions will allow two companies to file a

consolidated income tax return?

61. How is goodwill amortized?

62. Why might a consolidated group file separate income tax returns?

63. Alpha Corporation owns 100 percent of Beta Company, and Beta owns 80

percent of Gamma, Inc., all of which are domestic corporations. Information for

the three companies for the year ending December 31, 2011 follows:

Which of the following statements is true?