Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

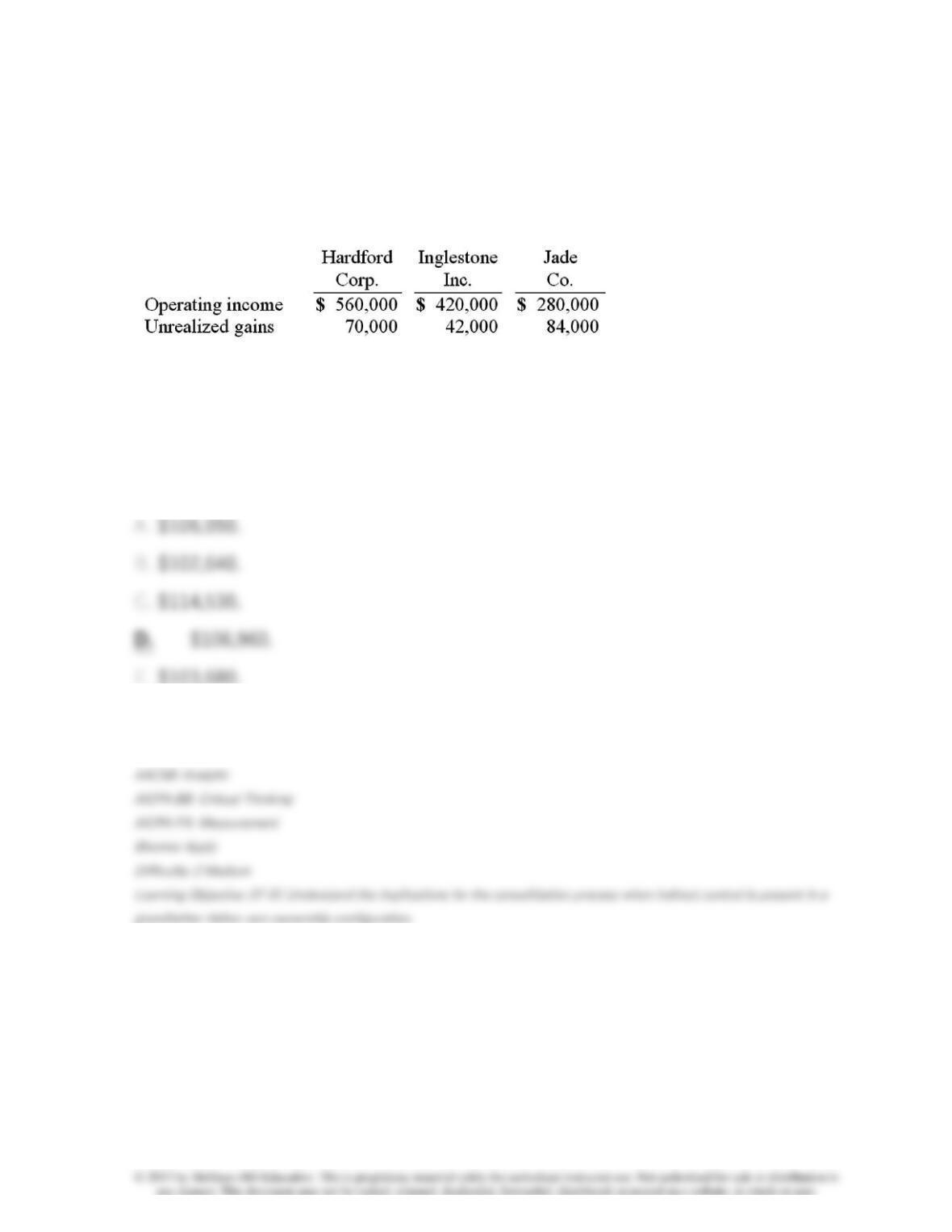

23. Hardford Corp. held 80% of Inglestone Inc. which, in turn, owned 80% of

Jade Co.

Operating income

figures (without investment income) as well as

unrealized upstream gains

included in the income for the current year follow:

The

accrual-based income of Jade Co.

is calculated to be

24. Hardford Corp. held 80% of Inglestone Inc. which, in turn, owned 80% of

Jade Co.

Operating income

figures (without investment income) as well as

unrealized upstream gains

included in the income for the current year follow:

The

non-controlling interest in the net income of Jade Co.

is calculated to be

25. Hardford Corp. held 80% of Inglestone Inc. which, in turn, owned 80% of

Jade Co.

Operating income

figures (without investment income) as well as

unrealized upstream gains

included in the income for the current year follow:

The

non-controlling interest in the net income of Inglestone Inc.

is calculated to

be

26. When indirect control is present, which of the following statements is

true?

27. Which of the following statements is

false

concerning a father-son-

grandson configuration?

28. Which of the following statements is true regarding mutual ownership

between a parent and its subsidiary?

29. Which of the following statements is true regarding a subsidiary's

investment in the parent company's stock?

30. Which of the following statements is true regarding the subsidiary's

investment in its parent's common stock?

31. Which of the following statements is true regarding the filing of income

taxes for an affiliated group?

32. The benefits of filing a consolidated tax return include all of the following

except

33. Which of the following statements is true regarding goodwill?

34. Chase Company owns 80% of Lawrence Company and 40% of Ross

Company. Lawrence Company also owns 30% of Ross Company. Separate

operating incomes for 2011 of Chase, Lawrence, and Ross are $450,000,

$300,000, and $250,000, respectively. Each company also retains a $20,000

unrealized gain in their current income figures. Annual amortization expense of

$15,000 is assigned to Chase's investment in Lawrence and another $15,000 is

assigned to Lawrence's investment in Ross.

Compute Chase's attributed ownership in Ross.

35. Chase Company owns 80% of Lawrence Company and 40% of Ross

Company. Lawrence Company also owns 30% of Ross Company. Separate

operating incomes for 2011 of Chase, Lawrence, and Ross are $450,000,

$300,000, and $250,000, respectively. Each company also retains a $20,000

unrealized gain in their current income figures. Annual amortization expense of

$15,000 is assigned to Chase's investment in Lawrence and another $15,000 is

assigned to Lawrence's investment in Ross.

Compute the non-controlling interest in Ross' net income for 2011.

36. Chase Company owns 80% of Lawrence Company and 40% of Ross

Company. Lawrence Company also owns 30% of Ross Company. Separate

operating incomes for 2011 of Chase, Lawrence, and Ross are $450,000,

$300,000, and $250,000, respectively. Each company also retains a $20,000

unrealized gain in their current income figures. Annual amortization expense of

$15,000 is assigned to Chase's investment in Lawrence and another $15,000 is

assigned to Lawrence's investment in Ross.

Compute Lawrence's accrual-based income for 2011.

37. Chase Company owns 80% of Lawrence Company and 40% of Ross

Company. Lawrence Company also owns 30% of Ross Company. Separate

operating incomes for 2011 of Chase, Lawrence, and Ross are $450,000,

$300,000, and $250,000, respectively. Each company also retains a $20,000

unrealized gain in their current income figures. Annual amortization expense of

$15,000 is assigned to Chase's investment in Lawrence and another $15,000 is

assigned to Lawrence's investment in Ross.

Compute Chase's accrual-based income for 2011.

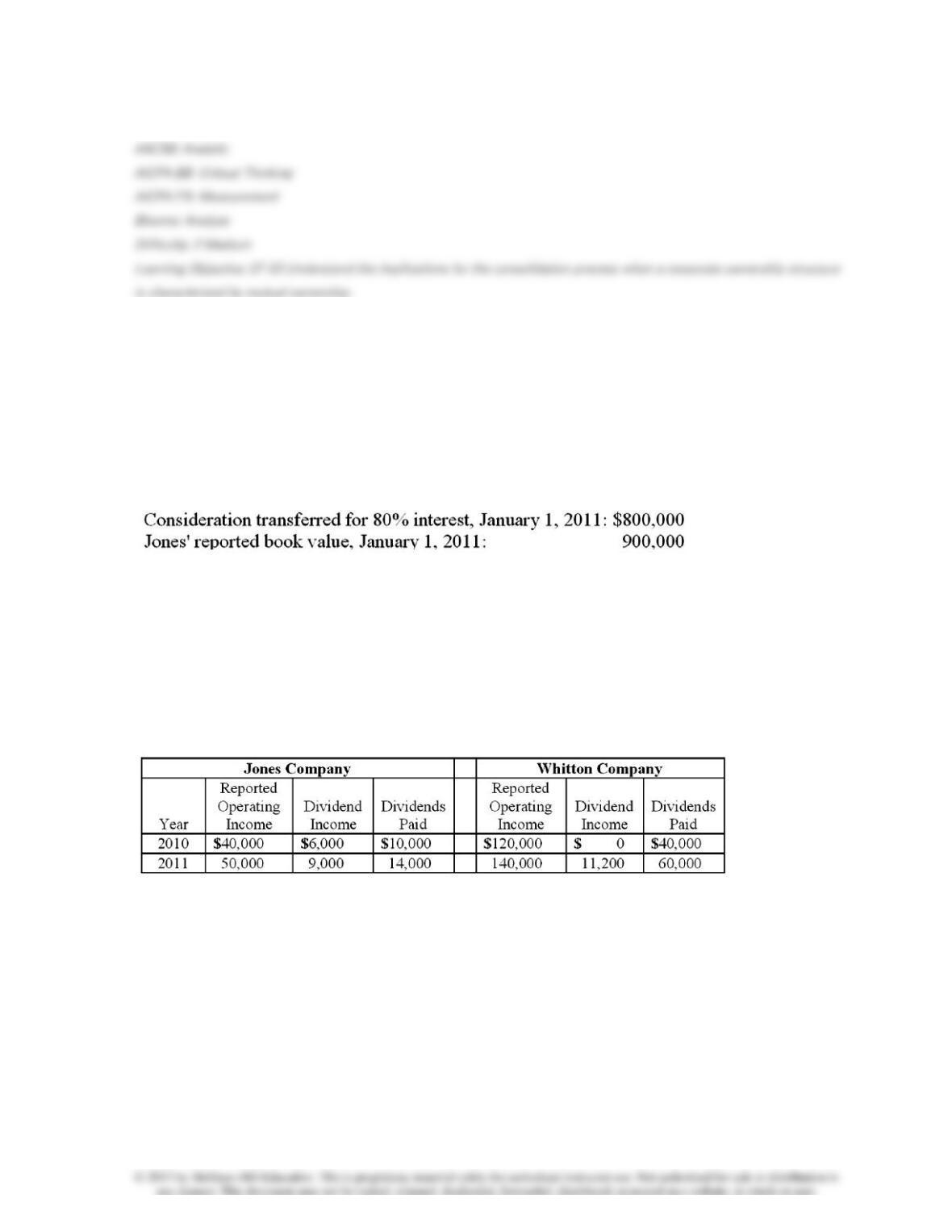

38. On January 1, 2010, Jones Company bought 15% of Whitton Company.

Jones paid $150,000 for these shares, an amount that exactly equaled the

proportionate book value of Whitton. On January 1, 2011, Whitton acquired 80%

ownership of Jones. The following data are available concerning Whitton's

acquisition of Jones:

Excess fair value over book value (assigned to trademarks) is amortized over 20

years.

The initial value method is used by both companies.

The following information is available regarding Jones and Whitton:

What would be included in a consolidation worksheet entry for 2011?

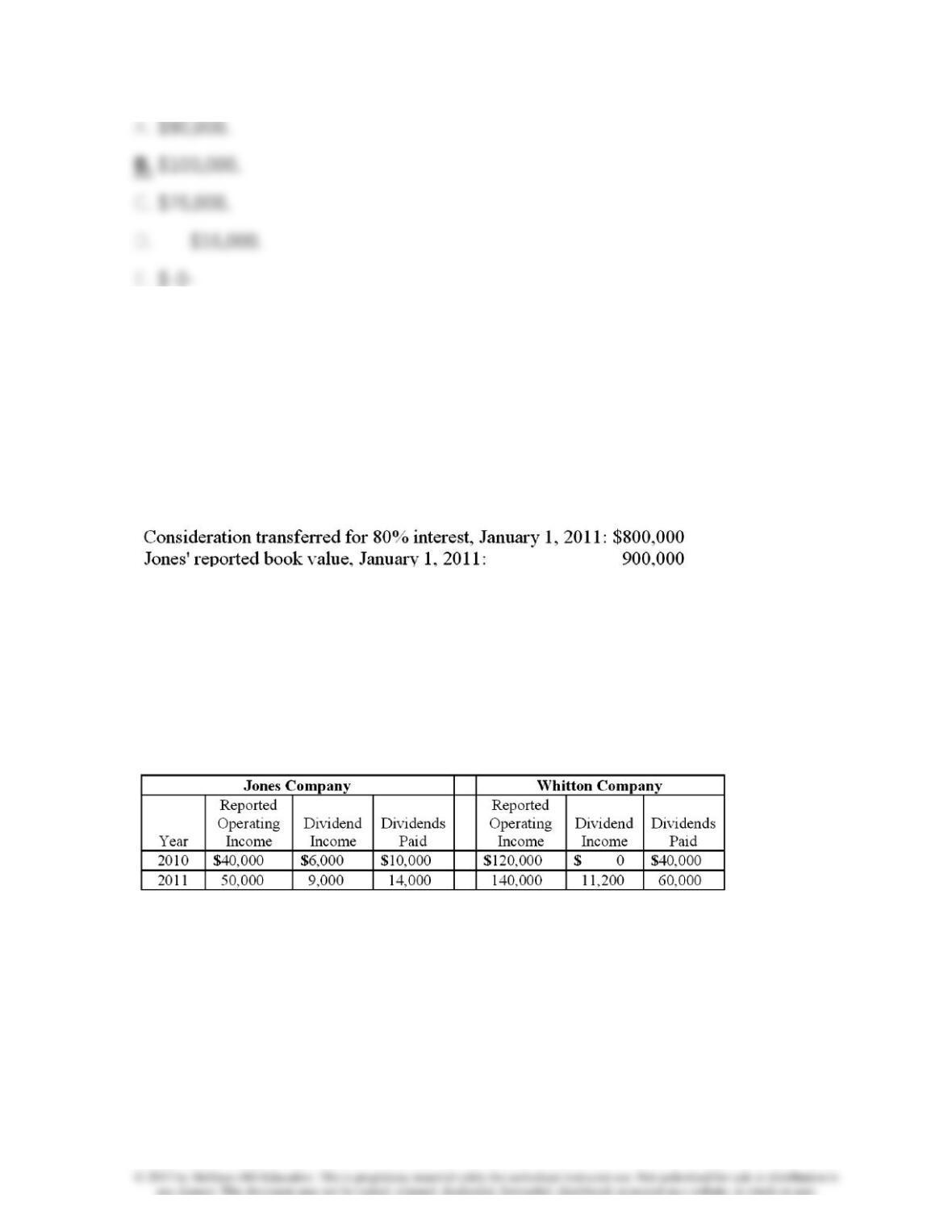

39. On January 1, 2010, Jones Company bought 15% of Whitton Company.

Jones paid $150,000 for these shares, an amount that exactly equaled the

proportionate book value of Whitton. On January 1, 2011, Whitton acquired 80%

ownership of Jones. The following data are available concerning Whitton's

acquisition of Jones:

Excess fair value over book value (assigned to trademarks) is amortized over 20

years.

The initial value method is used by both companies.

The following information is available regarding Jones and Whitton:

Compute the amount allocated to trademarks recognized in the January 1, 2011

consolidated balance sheet.

40. On January 1, 2010, Jones Company bought 15% of Whitton Company.

Jones paid $150,000 for these shares, an amount that exactly equaled the

proportionate book value of Whitton. On January 1, 2011, Whitton acquired 80%

ownership of Jones. The following data are available concerning Whitton's

acquisition of Jones:

Excess fair value over book value (assigned to trademarks) is amortized over 20

years.

The initial value method is used by both companies.

The following information is available regarding Jones and Whitton:

Compute Whitton's accrual-based consolidated net income for 2011.

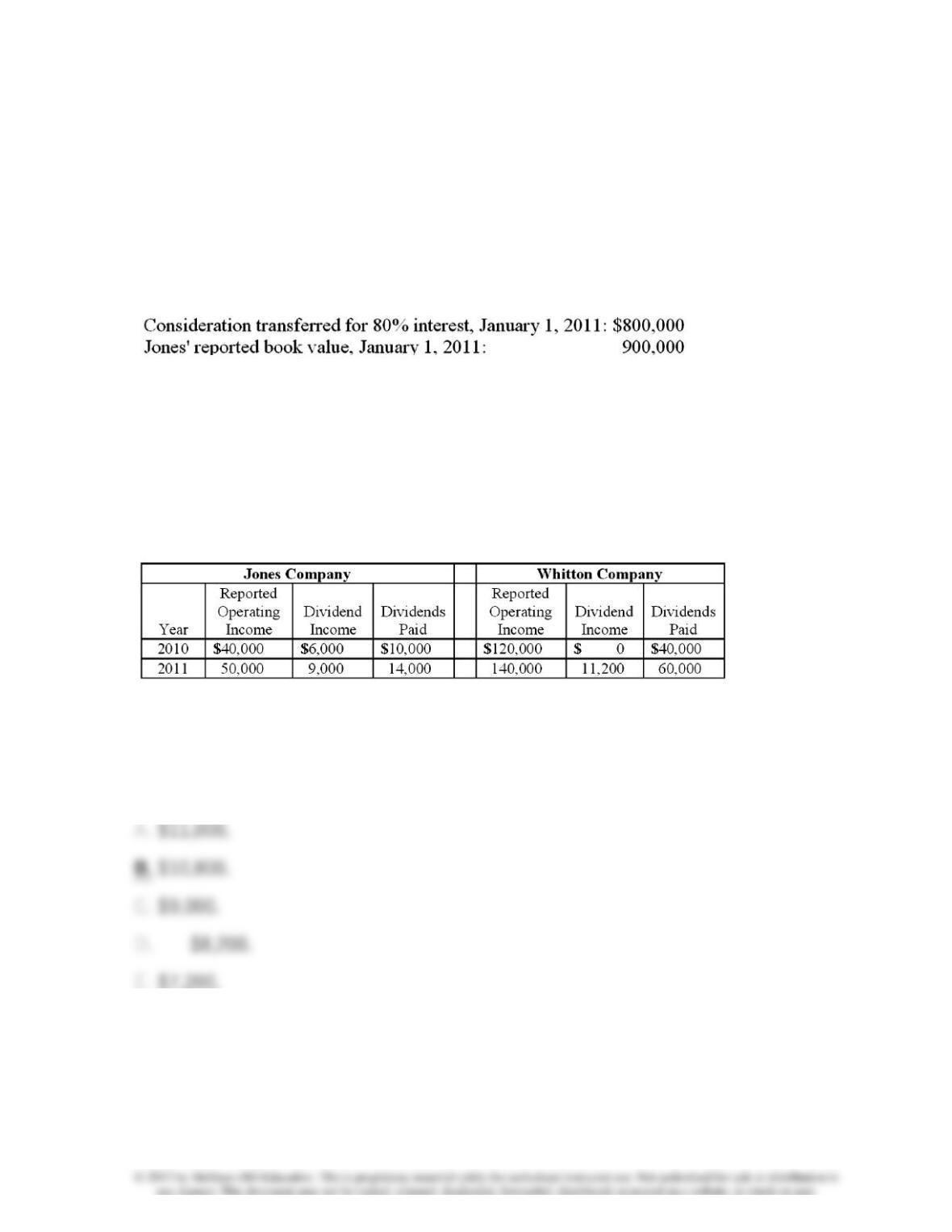

41. On January 1, 2010, Jones Company bought 15% of Whitton Company.

Jones paid $150,000 for these shares, an amount that exactly equaled the

proportionate book value of Whitton. On January 1, 2011, Whitton acquired 80%

ownership of Jones. The following data are available concerning Whitton's

acquisition of Jones:

Excess fair value over book value (assigned to trademarks) is amortized over 20

years.

The initial value method is used by both companies.

The following information is available regarding Jones and Whitton:

Compute the non-controlling interest in net income for 2011.