43. A building was purchased for $50,000. The asset has an expected useful life of 6 years

and depreciation expense each year is $8,000 using the straight-line method. What is the

residual value of the building?

44. Bricker Enterprises purchased a machine for $100,000 on October 1, 2012. The estimated

service life is ten years with a $10,000 residual value. Bricker records partial-year

depreciation based on the number of months in service. Depreciation expense for 2012, using

straight-line, is:

45. Schager Company purchased a computer system on January 1, 2012, at a cost of $40,000.

The estimated useful life is 10 years, and the estimated residual value is $5,000. Assuming the

company will use the double-declining-balance method, what is the depreciation expense for

the second year?

46. Shasta Exploring purchases a piece of equipment on January 1, 2012, for $50,000 and the

equipment has an expected useful life of five years. Its residual value is estimated to be

$4,000. Assuming Shasta uses the double-declining balance depreciation method, what is the

depreciation expense for the equipment for 2013?

47. During 2012 and 2013, Supplies, Inc. drove the truck 15,000 and 22,000 miles,

respectively, to deliver merchandise to its customers. The company originally purchased the

truck at the beginning of 2012 for $175,000. If the truck has an estimated life of 10 years and

300,000 miles, with an estimated residual value of $25,000, what amount of deprecation

expense should Supplies, Inc. record in 2013 using the activity method?

48. Crestview Estates purchased a tractor on January 1, 2012, for $65,000. The tractor’s useful

life is estimated to be 30,000 miles and has a residual value of $5,000. If Crestview used the

tractor 5,000 miles in 2012 and 3,000 miles in 2013, what is the balance for accumulated

depreciation at the end of 2013 using the activity method?

49. Nanki Corporation purchased equipment at the beginning of 2012 for $650,000. In 2012

and 2013, Nanki depreciated the asset on a straight-line basis with an estimated useful life of

8 years and a $10,000 residual value. In 2014, due to changes in technology, Nanki revised

the useful life to a total of six years (four more years) with zero residual value. What

depreciation expense would Nanki record for the year 2014 on this equipment?

50. Which of the following intangible assets is not amortized?

51. Which of the following statements is true regarding the amortization of intangible assets?

52. Bricktown Exchange purchases a copyright on January 1, 2012, for $50,000. The

copyright has a remaining legal life of 25 years, but only an expected useful life of five years

with no residual value. Assuming the company uses the straight-line method, what is the

amortization expense for the year ended December 31, 2012?

53. Berry Co. purchases a patent on January 1, 2012, for $40,000 and the patent has an

expected useful life of five years with no residual value. Assuming Berry Co. uses the

straight-line method, what is the amortization expense for the year ended December 31,

2013?

54. Berry Co. purchases a patent on January 1, 2012, for $40,000 and the patent has an

expected useful life of five years with no residual value. Assuming Berry Co. uses the

straight-line method, what is the carrying value of the patent on December 31, 2013?

55. Gains on the sale of fixed assets for cash:

56. Abbott Company purchased a computer that cost $10,000. It had an estimated useful life

of 5 years and no residual value. The computer was depreciated by the straight-line method

and was sold at the end of the fourth year of use for $3,000 cash. Abbott should record:

57. On January 1, 2010, Jacob Inc. purchased a commercial truck for $48,000 and uses the

straight-line depreciation method. The truck has a useful life of eight years and an estimated

residual value of $8,000. On December 31, 2012, Jacob Inc. sold the truck for $30,000. What

amount of gain or loss should Jacob Inc. record on December 31, 2012?

58. Alliance Products purchased equipment that cost $120,000. It had an estimated useful life

of four years and no residual value. The equipment was depreciated by the straight-line

method and was sold at the end of the third year of use for $25,000 cash. Alliance should

record:

59. Career Services, Incorporated sold some office equipment for $52,000 on December 31,

2012. The journal entry to record the sale would include which of the following if the original

cost of the equipment was $80,000 with a residual value of $5,000 and a useful life of 10

years? Assume the machine was purchased on January 1, 2009 and depreciated using the

straight-line method.

60. ABO purchased a truck at the beginning of 2012 for $140,000. They sold the truck at the

end of 2013 for $95,000. If the expected life of the truck was six years with a residual value of

$20,000 and ABO uses straight-line depreciation, which of the following is true regarding the

entry to record the sale of the truck?

61. Oregon Adventures purchased equipment at the beginning of 2012 for $80,000. They sold

the equipment at the end of 2014 for $45,000. If the expected life of the equipment was seven

years with a residual value of $10,000, and they use straight-line depreciation, which of the

following is true regarding the entry to record the sale of the equipment?

62. The return on assets is calculated as:

63. The return on assets is equal to the:

64. The balance sheet of Hidden Valley Farms reports total assets of $450,000 and $550,000

at the beginning and end of the year, respectively. Net income and sales for the year are

$100,000 and $800,000, respectively. What is Hidden Valley’s return on assets?

65. The balance sheet of Hidden Valley Farms reports total assets of $450,000 and $550,000

at the beginning and end of the year, respectively. Net income and sales for the year are

$100,000 and $800,000, respectively. What is Hidden Valley’s profit margin?

66. The balance sheet of Hidden Valley Farms reports total assets of $450,000 and $550,000

at the beginning and end of the year, respectively. Net income and sales for the year are

$100,000 and $800,000, respectively. What is Hidden Valley’s asset turnover?

67. The balance sheet of Hidden Valley Farms reports total assets of $450,000 and $550,000

at the beginning and end of the year, respectively. The return on assets for the year is 10%.

What is Hidden Valley’s net income for the year?

68. Recognition of impairment for long-term assets is required if book value exceeds:

69. The amount of impairment loss is the excess of book value over:

70. Accounting for impairment losses:

71. In testing for recoverability of an operational asset, an impairment loss is required if the:

72. Wilson Inc. owns equipment for which it paid $70 million. At the end of 2012, it had

accumulated depreciation on the equipment of $12 million. Due to adverse economic

conditions, Wilson’s management determined that it should assess whether an impairment

should be recognized for the equipment. The estimated future cash flows to be provided by

the equipment total $60 million, and its fair value at that point totals $50 million. Under these

circumstances, Wilson:

73. Leonard’s Jewelry owns a patent with a carrying value of $50 million at the end of 2012.

Due to adverse economic conditions, Leonard’s management determined that it should assess

whether an impairment should be recognized for the patent. The estimated future cash flows

to be provided by the patent total $43 million, and its fair value at that point totals $35

million. Under these circumstances, Leonard:

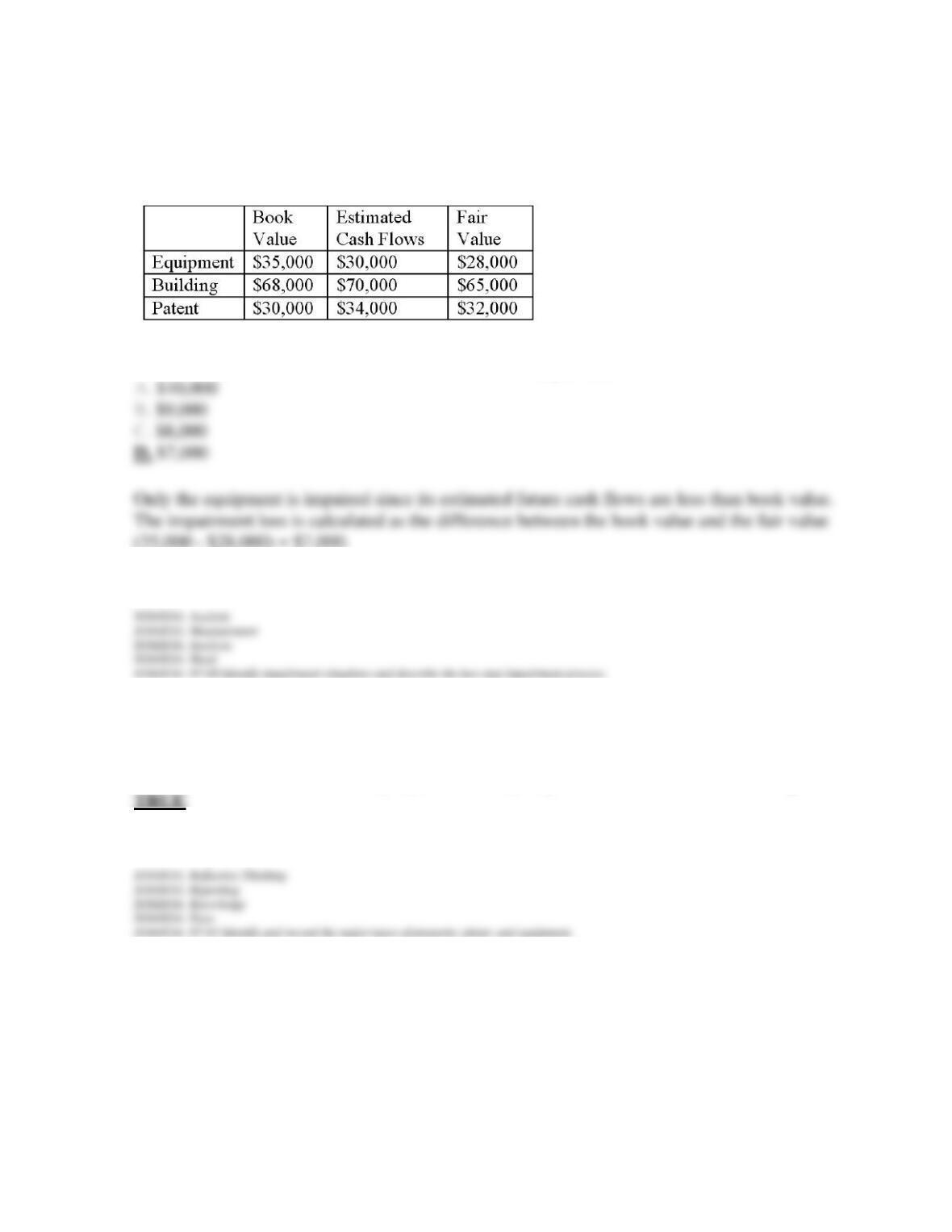

74. C-Stop reports the following information at year-end:

Based on the above information, what is the total amount of impairment loss that C-Stop

should record at year end?

75. Maple Inc. has the following information regarding its assets:

What amount of loss should be recorded due to asset impairments?

76. The CEO, as head of the company, is ultimately responsible for the firm’s accounting.

77. We record a long-term asset at its cost less all expenditures necessary to get the asset

ready for use.

78. We use the term capitalize to describe recording an expenditure as an expense.

79. Cash received from the sale of salvaged materials increases the total cost of land.

80. Land improvements are recorded separately from the land itself because, unlike land,

these assets are subject to depreciation.

81. Capitalized interest refers to interest costs we add to the asset account rather than

recording as interest expense.

82. Many intangible assets are not recorded on the balance sheet at their estimated market

values.

83. We record purchased intangible assets at their original cost plus all other costs necessary

to get the asset ready for use.

84. Most of the costs associated with internally developed intangible assets are recorded as

intangible assets on the balance sheet.

85. Research and development costs incurred in developing a patent internally are not

recorded as an intangible asset in the balance sheet, but rather are expensed directly in the

income statement.

86. International accounting standards allow firms to record development costs that benefit

future periods as an intangible asset.