7-21

35. Product R19N has been considered a drag on profits at Buzzeo Corporation for some time

and management is considering discontinuing the product altogether. Data from the company’s

accounting system appear below:

In the company’s accounting system all fixed expenses of the company are fully allocated to

products. Further investigation has revealed that $49,000 of the fixed manufacturing expenses

and $30,000 of the fixed selling and administrative expenses are avoidable if product R19N is

discontinued. What would be the effect on the company’s overall net operating income if product

R19N were dropped?

36. Lusk Company produces and sells 15,000 units of Product A each month. The selling

price of Product A is $20 per unit, and variable expenses are $14 per unit. A study has been made

concerning whether Product A should be discontinued. The study shows that $70,000 of the

$100,000 in fixed expenses charged to Product A would continue even if the product was

discontinued. These data indicate that if Product A is discontinued, the company’s overall net

operating income would:

37. Peluso Company, a manufacturer of snowmobiles, is operating at 70% of plant capacity.

Peluso’s plant manager is considering making the headlights now being purchased from an

outside supplier for $11 each. The Peluso plant has idle equipment that could be used to

manufacture the headlights. The design engineer estimates that each headlight requires $4 of

direct materials, $3 of direct labor, and $6.00 of manufacturing overhead. Forty percent of the

manufacturing overhead is a fixed cost that would be unaffected by this decision. A decision by

Peluso Company to manufacture the headlights should result in a net gain (loss) for each

headlight of:

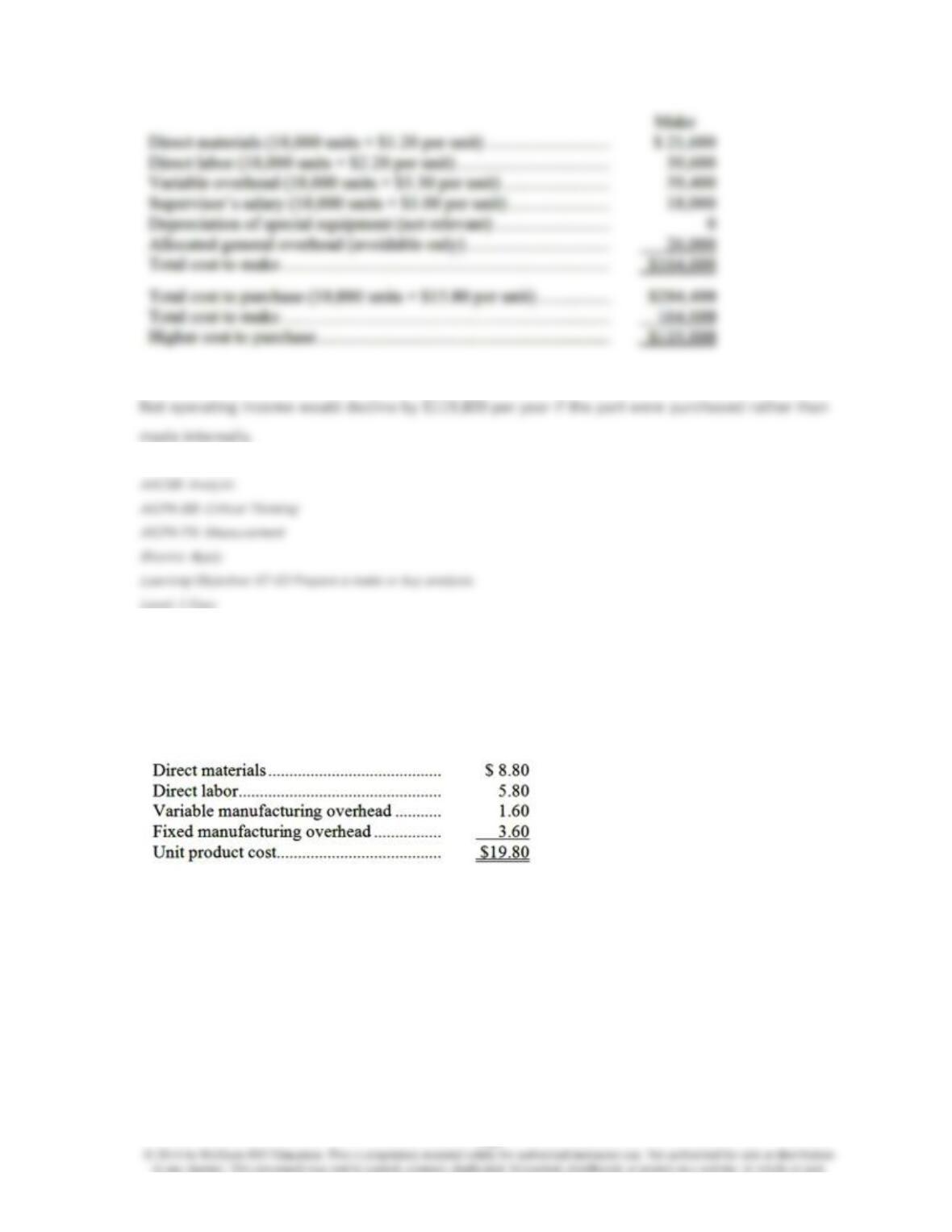

38. Part I51 is used in one of Pries Corporation’s products. The company makes 18,000 units

of this part each year. The company’s Accounting Department reports the following costs of

producing the part at this level of activity:

An outside supplier has offered to produce this part and sell it to the company for $15.80 each. If

this offer is accepted, the supervisor’s salary and all of the variable costs, including direct labor,

can be avoided. The special equipment used to make the part was purchased many years ago

and has no salvage value or other use. The allocated general overhead represents fixed costs of

the entire company. If the outside supplier’s offer were accepted, only $26,000 of these allocated

general overhead costs would be avoided.

If management decides to buy part I51 from the outside supplier rather than to continue making

the part, what would be the annual impact on the company’s overall net operating income?

7-25

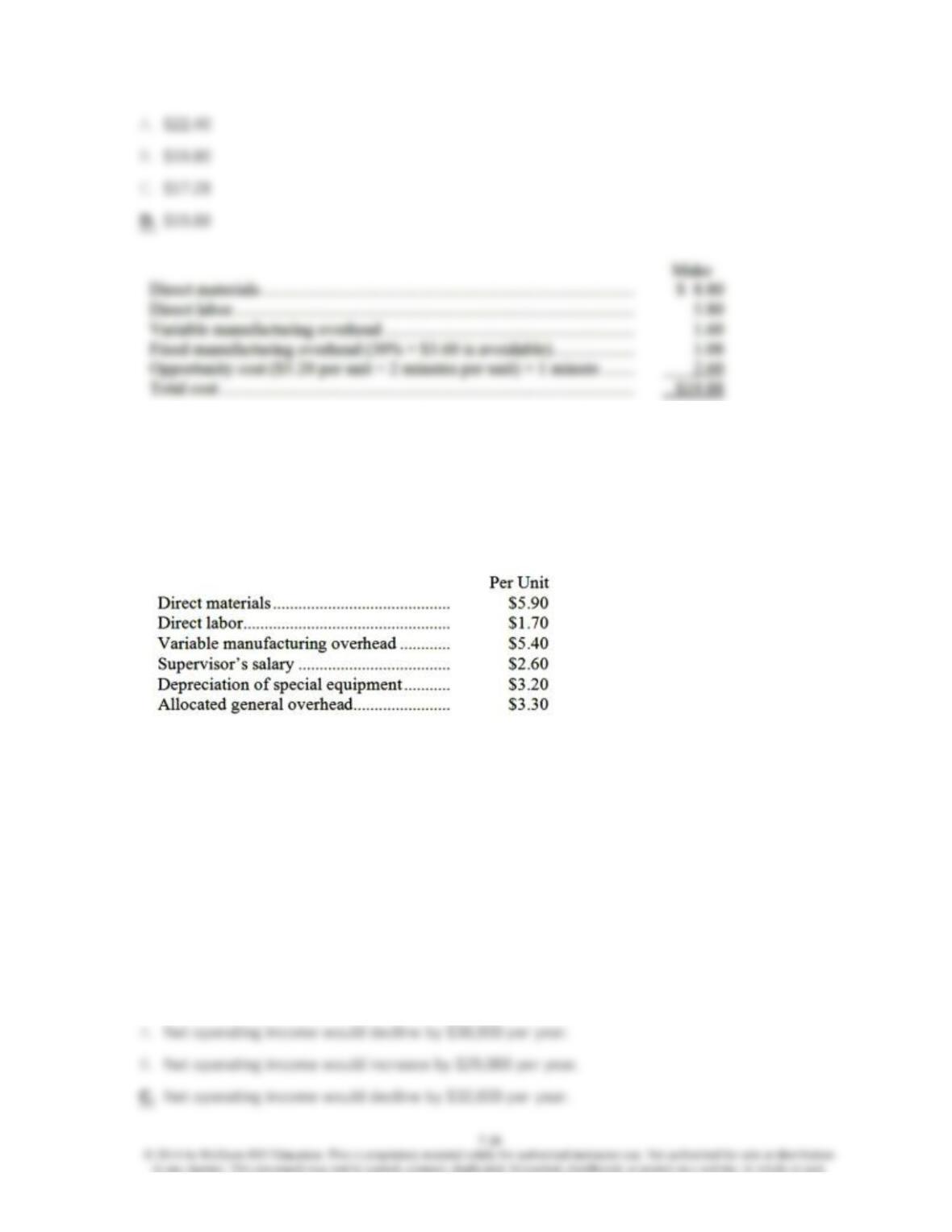

39. Iwasaki Inc. is considering whether to continue to make a component or to buy it from an

outside supplier. The company uses 13,000 of the components each year. The unit product cost

of the component according to the company’s cost accounting system is given as follows:

Assume that direct labor is a variable cost. Of the fixed manufacturing overhead, 30% is avoidable

if the component were bought from the outside supplier. In addition, making the component uses

1 minute on the machine that is the company’s current constraint. If the component were bought,

this machine time would be freed up for use on another product that requires 2 minutes on this

machine and that has a contribution margin of $5.20 per unit.

When deciding whether to make or buy the component, what cost of making the component

should be compared to the price of buying the component?

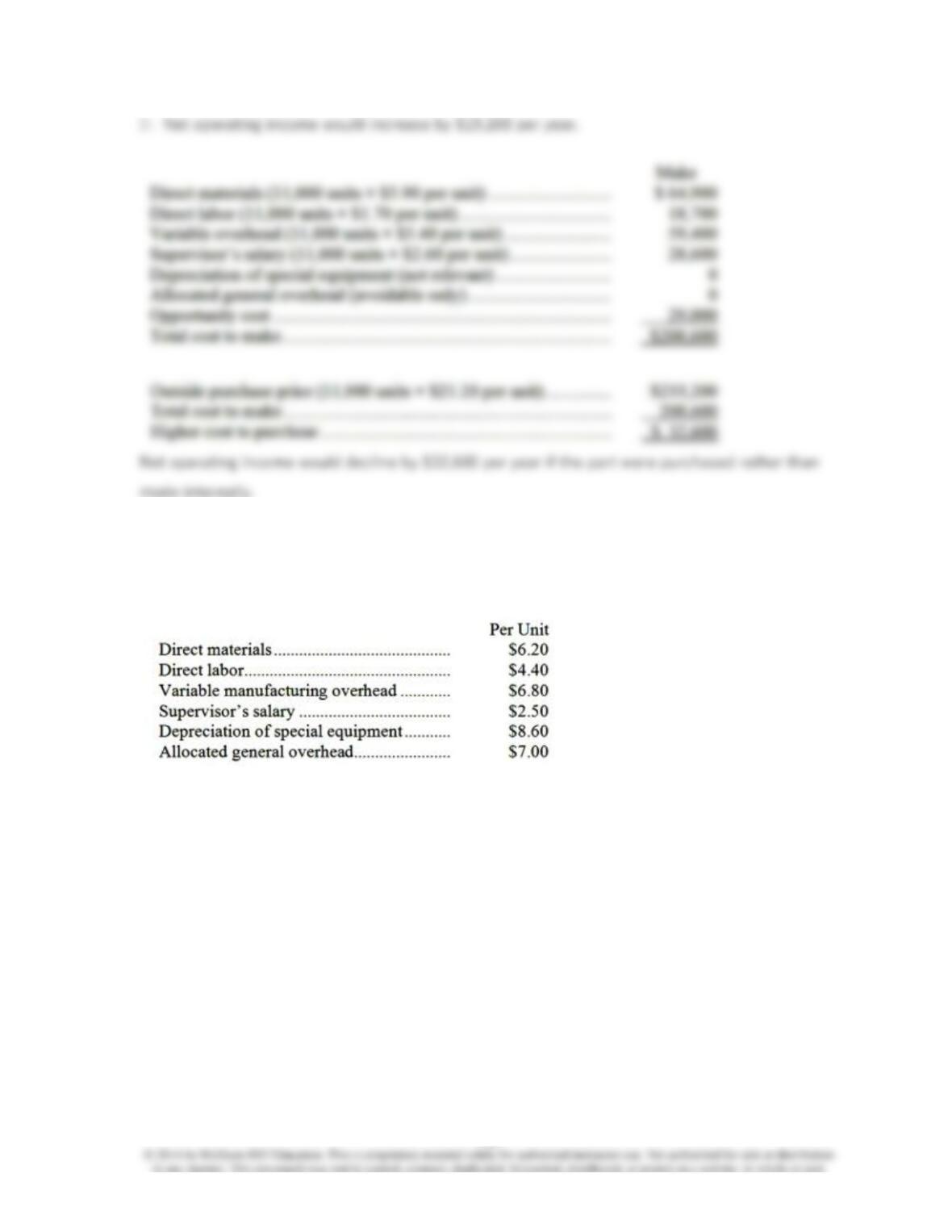

40. Part N29 is used by Farman Corporation to make one of its products. A total of 11,000

units of this part are produced and used every year. The company’s Accounting Department

reports the following costs of producing the part at this level of activity:

An outside supplier has offered to make the part and sell it to the company for $21.20 each. If

this offer is accepted, the supervisor’s salary and all of the variable costs, including the direct

labor, can be avoided. The special equipment used to make the part was purchased many years

ago and has no salvage value or other use. The allocated general overhead represents fixed costs

of the entire company, none of which would be avoided if the part were purchased instead of

produced internally. In addition, the space used to make part N29 could be used to make more of

one of the company’s other products, generating an additional segment margin of $29,000 per

year for that product. What would be the impact on the company’s overall net operating income

of buying part N29 from the outside supplier?

7-27

41. Fillip Corporation makes 4,000 units of part U13 each year. This part is used in one of the

company’s products. The company’s Accounting Department reports the following costs of

producing the part at this level of activity:

An outside supplier has offered to make and sell the part to the company for $21.60 each. If this

offer is accepted, the supervisor’s salary and all of the variable costs, including direct labor, can

be avoided. The special equipment used to make the part was purchased many years ago and

has no salvage value or other use. The allocated general overhead represents fixed costs of the

entire company. If the outside supplier’s offer were accepted, only $3,000 of these allocated

general overhead costs would be avoided. In addition, the space used to produce part U13 would

be used to make more of one of the company’s other products, generating an additional segment

margin of $13,000 per year for that product.

What would be the impact on the company’s overall net operating income of buying part U13

from the outside supplier?

42. Ethridge Corporation is presently making part H25 that is used in one of its products. A

total of 9,000 units of this part are produced and used every year. The company’s Accounting

Department reports the following costs of producing the part at this level of activity:

An outside supplier has offered to make and sell the part to the company for $15.40 each. If this

offer is accepted, the supervisor’s salary and all of the variable costs can be avoided. The special

equipment used to make the part was purchased many years ago and has no salvage value or

other use. The allocated general overhead represents fixed costs of the entire company, none of

which would be avoided if the part were purchased instead of produced internally. If

management decides to buy part H25 from the outside supplier rather than to continue making

the part, what would be the annual impact on the company’s overall net operating income?

43. Pitkin Company produces a part used in the manufacture of one of its products. The unit

product cost of the part is $33, computed as follows:

An outside supplier has offered to provide the annual requirement of 10,000 of the parts for only

$27 each. The company estimates that 30% of the fixed manufacturing overhead costs above will

continue if the parts are purchased from the outside supplier. Assume that direct labor is an

avoidable cost in this decision. Based on these data, the per unit dollar advantage or

disadvantage of purchasing the parts from the outside supplier would be:

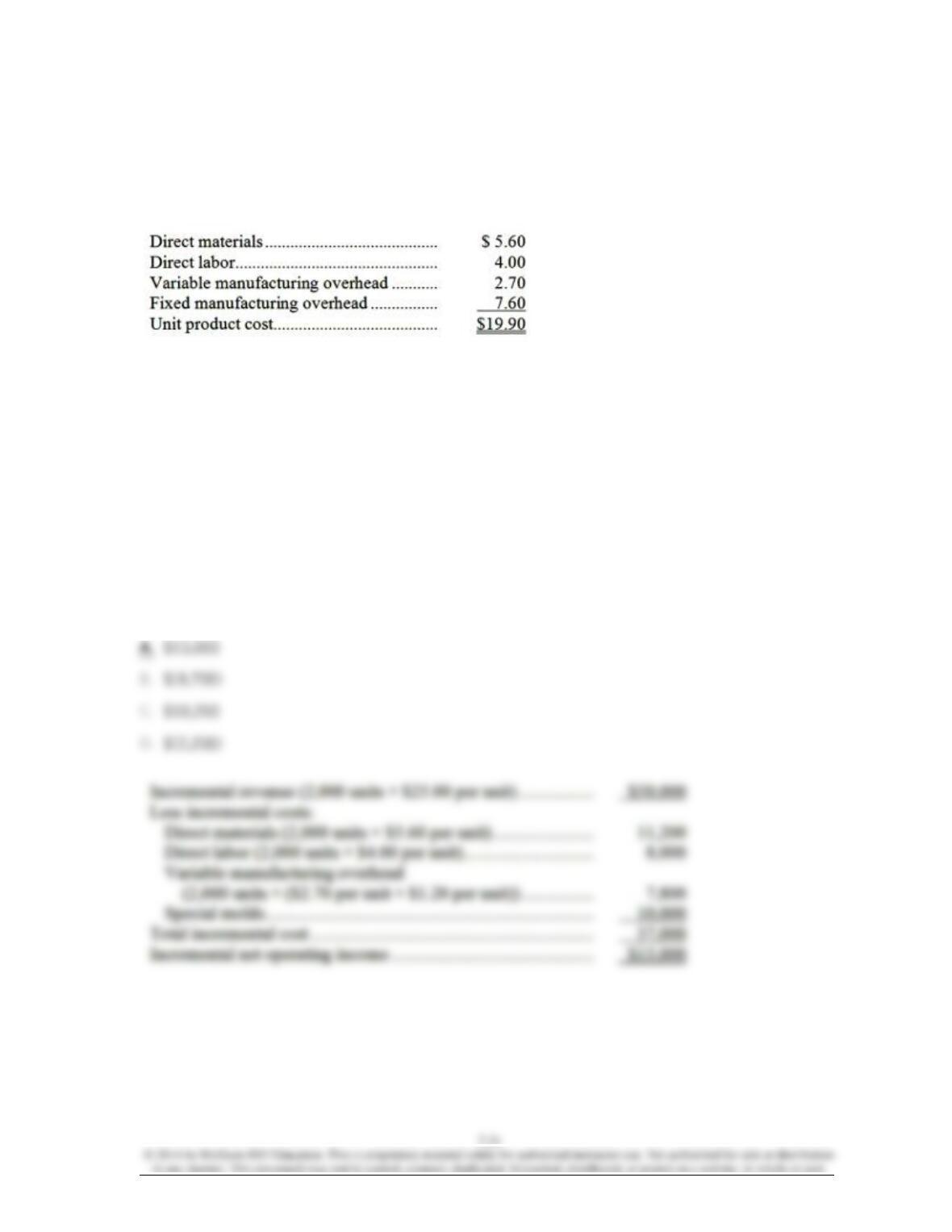

44. A customer has requested that Inga Corporation fill a special order for 2,000 units of

product K81 for $25.00 a unit. While the product would be modified slightly for the special order,

product K81’s normal unit product cost is $19.90:

Direct labor is a variable cost. The special order would have no effect on the company’s total

fixed manufacturing overhead costs. The customer would like modifications made to product K81

that would increase the variable costs by $1.20 per unit and that would require an investment of

$10,000 in special molds that would have no salvage value.

This special order would have no effect on the company’s other sales. The company has ample

spare capacity for producing the special order. If the special order is accepted, the company’s

overall net operating income would increase (decrease) by:

45. Rojo Corporation has received a request for a special order of 8,000 units of product W68

for $27.20 each. Product W68’s unit product cost is $18.50, determined as follows:

Direct labor is a variable cost. The special order would have no effect on the company’s total

fixed manufacturing overhead costs. The customer would like modifications made to product W68

that would increase the variable costs by $7.90 per unit and that would require an investment of

$31,000 in special molds that would have no salvage value.

This special order would have no effect on the company’s other sales. The company has ample

spare capacity for producing the special order. If the special order is accepted, the company’s

overall net operating income would increase (decrease) by:

46. Ellis Television makes and sells portable televisions. Each television regularly sells for

$210. The following cost data per television is based on a full capacity of 10,000 televisions

produced each period.

A special order has been received by Ellis for a sale of 2,000 televisions to an overseas customer.

The only selling costs that would be incurred on this order would be $6 per television for

shipping. Ellis is now selling 6,000 televisions through regular channels each period. What should

be the minimum selling price per television in negotiating a price for this special order?

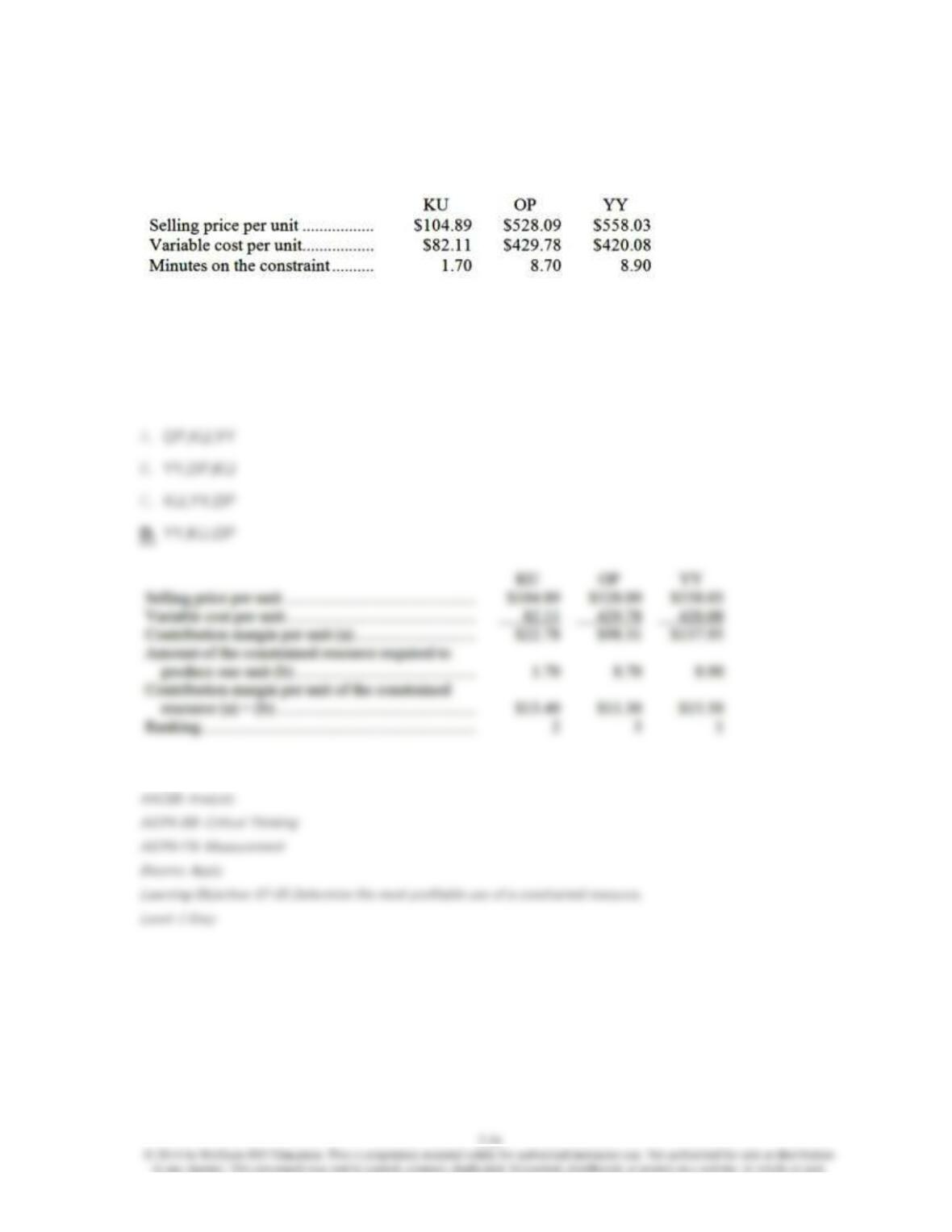

47. An automated turning machine is the current constraint at Naik Corporation. Three

products use this constrained resource. Data concerning those products appear below:

Rank the products in order of their current profitability from most profitable to least profitable. In

other words, rank the products in the order in which they should be emphasized.

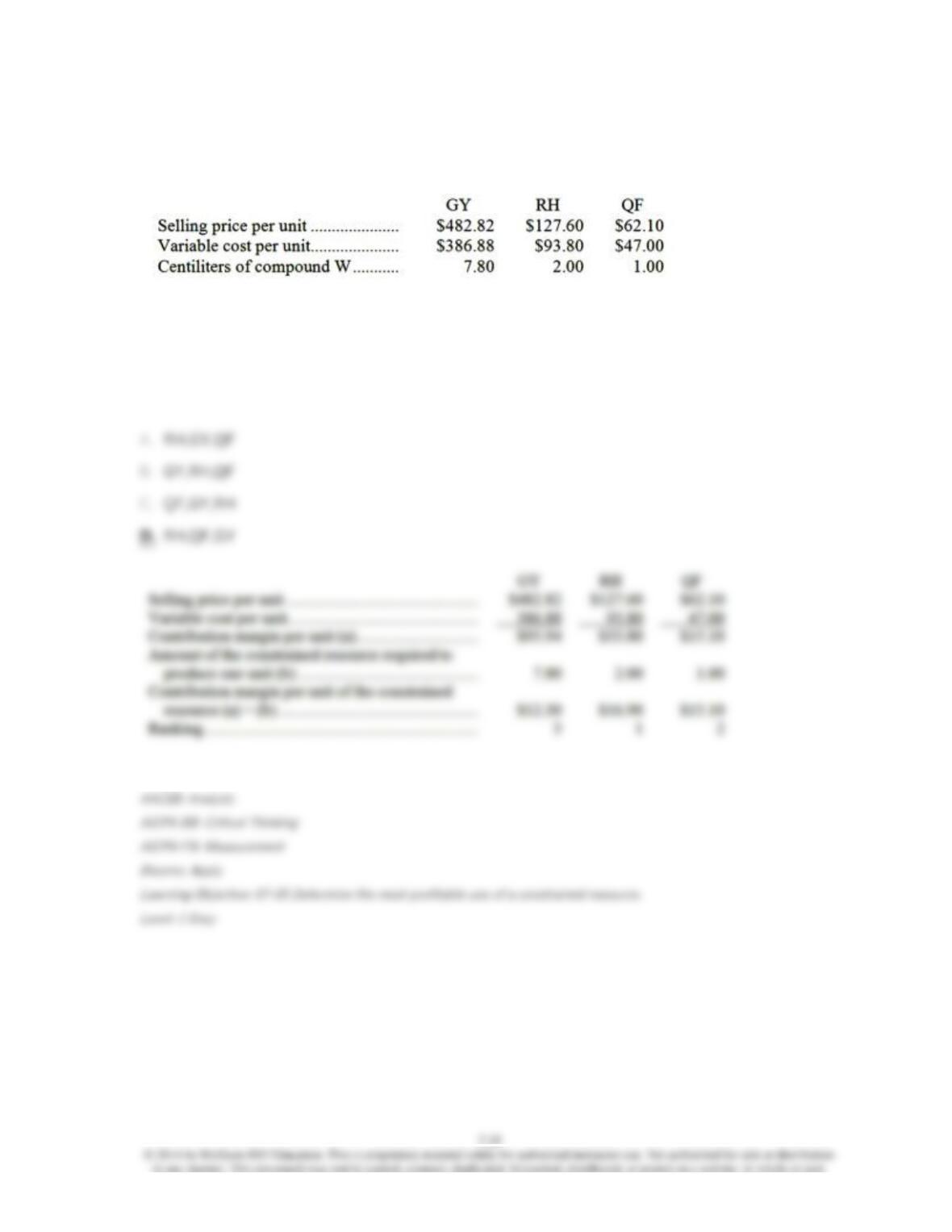

48. Pappan Corporation makes three products that use compound W, the current constrained

resource. Data concerning those products appear below:

Rank the products in order of their current profitability from most profitable to least profitable. In

other words, rank the products in the order in which they should be emphasized.

49. Consider the following production and cost data for two products, X and Y:

The company has 15,000 machine hours available each period, and there is unlimited demand for

each product. What is the largest possible total contribution margin that can be realized each

period?

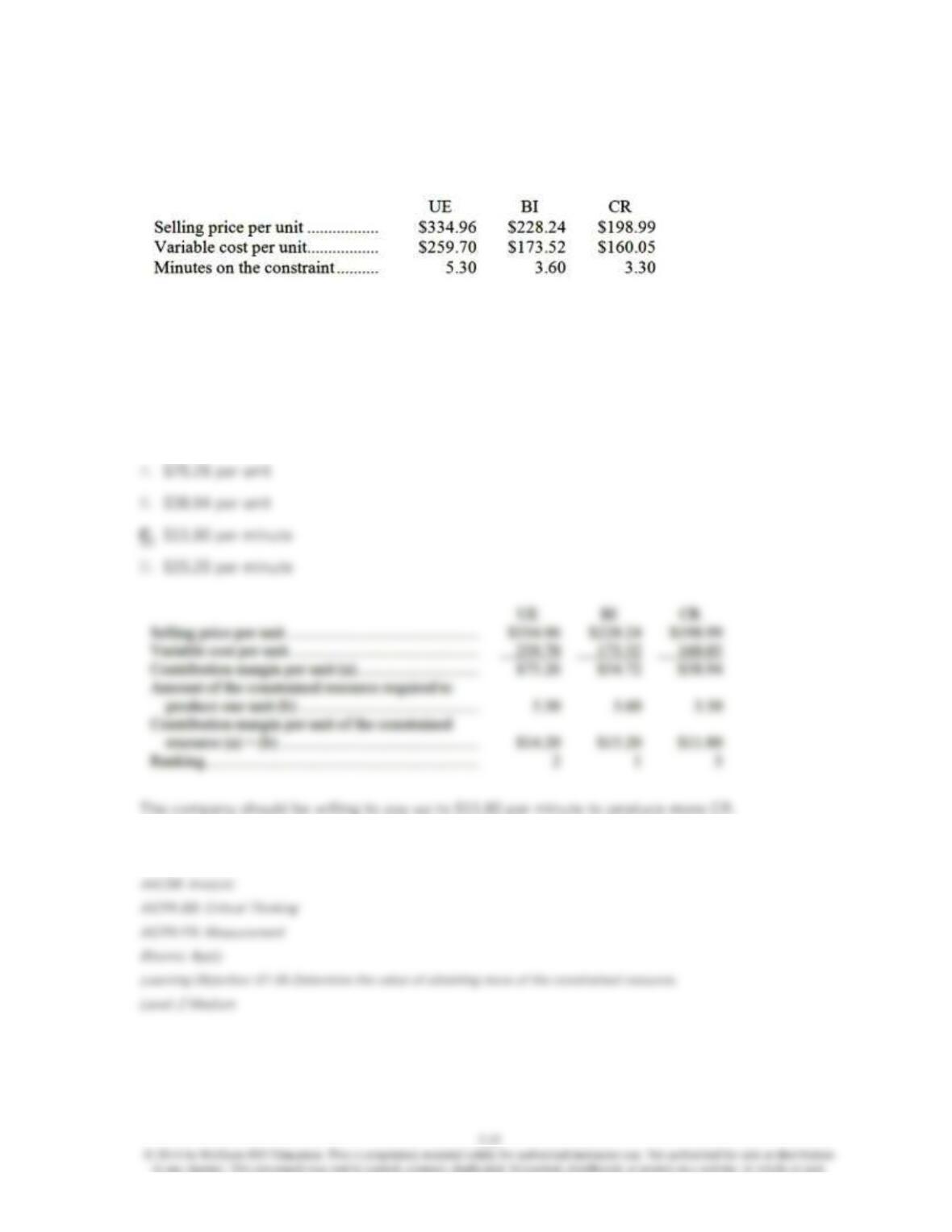

50. The constraint at Mcglathery Corporation is time on a particular machine. The company

makes three products that use this machine. Data concerning those products appear below:

Assume that sufficient time is available on the constrained machine to satisfy demand for all but

the least profitable product. Up to how much should the company be willing to pay to acquire

more of the constrained resource?

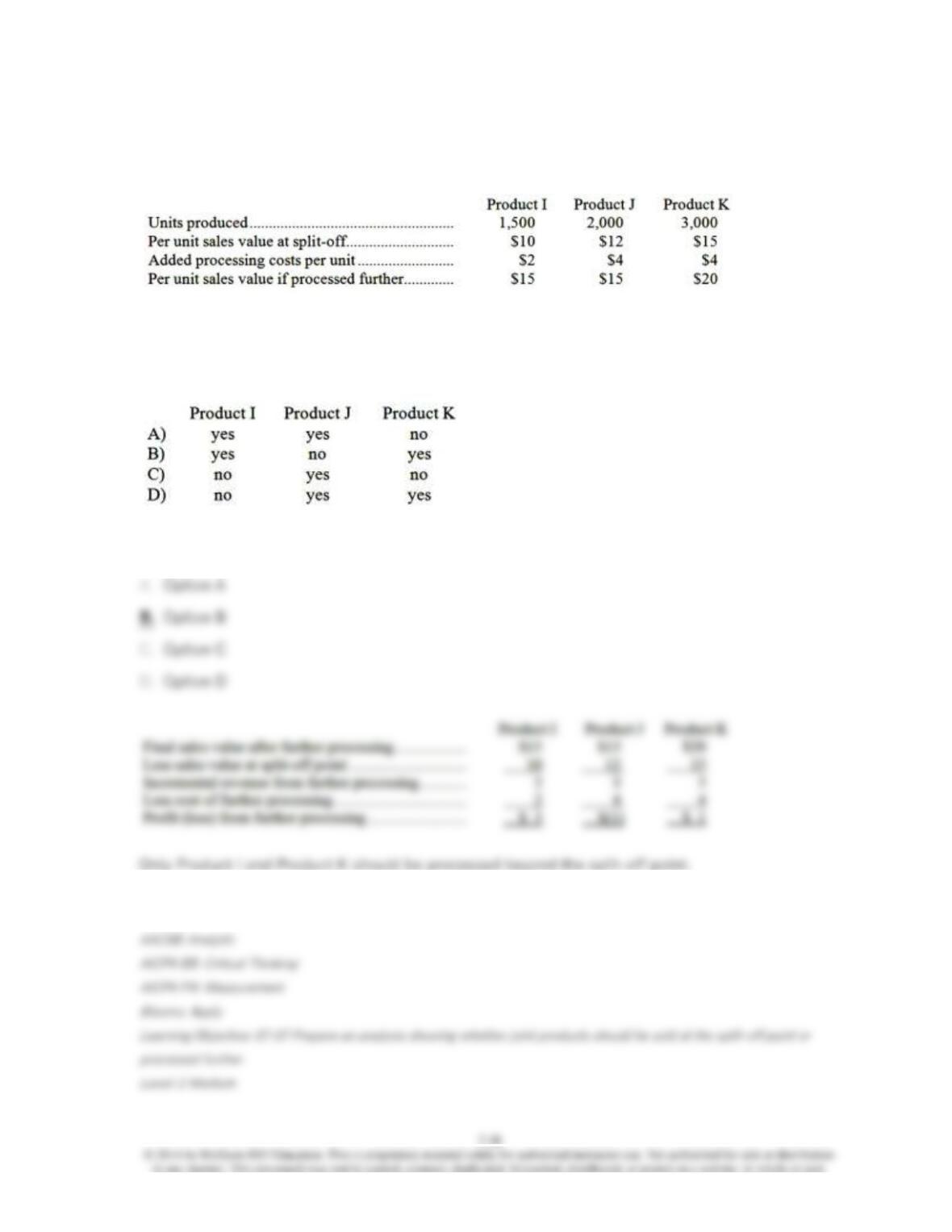

51. Wright Company produces products I, J, and K from a single raw material input. Budgeted

data for the next month follows:

If the cost of the raw material input is $78,000, which of the products should be processed

beyond the split-off point?

52. Two products, IF and RI, emerge from a joint process. Product IF has been allocated

$25,300 of the total joint costs of $46,000. A total of 2,000 units of product IF are produced from

the joint process. Product IF can be sold at the split-off point for $11 per unit, or it can be

processed further for an additional total cost of $10,000 and then sold for $13 per unit. If product

IF is processed further and sold, what would be the effect on the overall profit of the company

compared with sale in its unprocessed form directly after the split-off point?

53. Coakley Beet Processors, Inc., processes sugar beets in batches. A batch of sugar beets

costs $48 to buy from farmers and $10 to crush in the company’s plant. Two intermediate

products, beet fiber and beet juice, emerge from the crushing process. The beet fiber can be sold

as is for $24 or processed further for $16 to make the end product industrial fiber that is sold for

$36. The beet juice can be sold as is for $44 or processed further for $28 to make the end

product refined sugar that is sold for $70. How much profit (loss) does the company make by

processing the intermediate product beet juice into refined sugar rather than selling it as is?