1. Buckette Co. owned 60% of Shuvelle Corp. and 40% of Tayle Corp., and

Shuvelle owned 35% of Tayle.

When Buckette prepared

consolidated financial statements

, it should include

2. Buckette Co. owned 60% of Shuvelle Corp. and 40% of Tayle Corp., and

Shuvelle owned 35% of Tayle.

What is this pattern of ownership called?

3. Buckette Co. owned 60% of Shuvelle Corp. and 40% of Tayle Corp., and

Shuvelle owned 35% of Tayle.

What percentage of Tayle’s income is attributed to Buckette’s ownership

interest?

4. D Corp. had investments, direct and indirect, in several subsidiaries:

• E Co. is a domestic firm in which D Corp. owned a 90% interest

• F Co. is a domestic firm in which D Corp. owned 60% and E Co. owned 30%

• G Co. is a domestic firm wholly owned by E Co.

• H Co. is a foreign subsidiary in which D Corp. owned a 90% interest

• I Co. is a domestic firm in which D Corp. owned 50% and G Co. owned 25%

Which of these subsidiaries may be included in a

consolidated income tax

return

?

5. Evanston Co. owned 60% of Montgomery Corp. Montgomery owned 75% of

Noir Inc., and Noir owned 15% of Montgomery. This pattern of ownership would

be called

6. In a tax-free business combination,

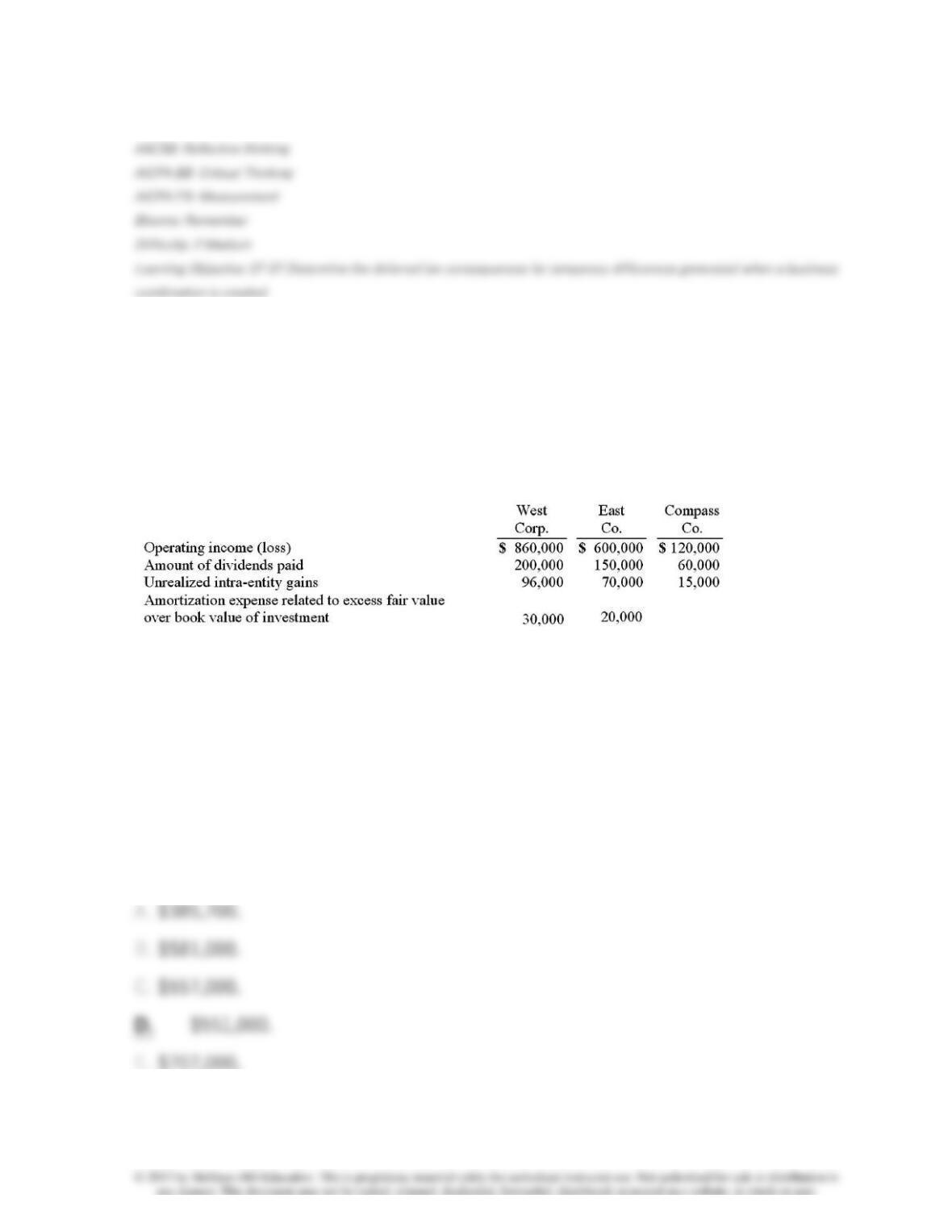

7. West Corp. owned 70% of the voting common stock of East Co. East owned

60% of Compass Co. West and East both used the

initial value method

to account

for their investments. The following information was available from the financial

statements and records of the three companies:

Operating income included unrealized intra-entity gains (which are related to

inventory transfers) but did not include dividend income from investment in

subsidiary.

The

accrual-based income of East Co.

is calculated to be

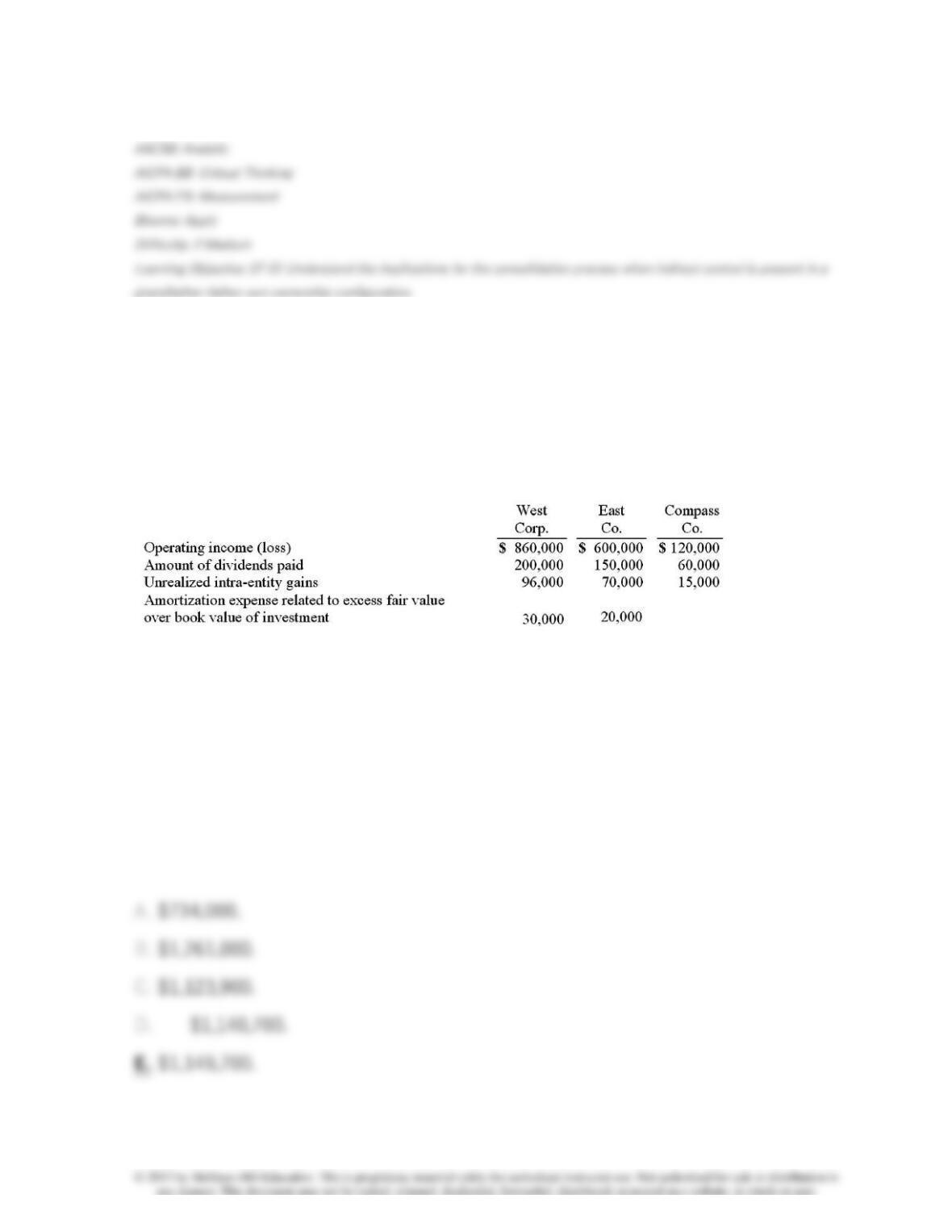

8. West Corp. owned 70% of the voting common stock of East Co. East owned

60% of Compass Co. West and East both used the

initial value method

to account

for their investments. The following information was available from the financial

statements and records of the three companies:

Operating income included unrealized intra-entity gains (which are related to

inventory transfers) but did not include dividend income from investment in

subsidiary.

The

accrual-based income of West Corp.

is calculated to be

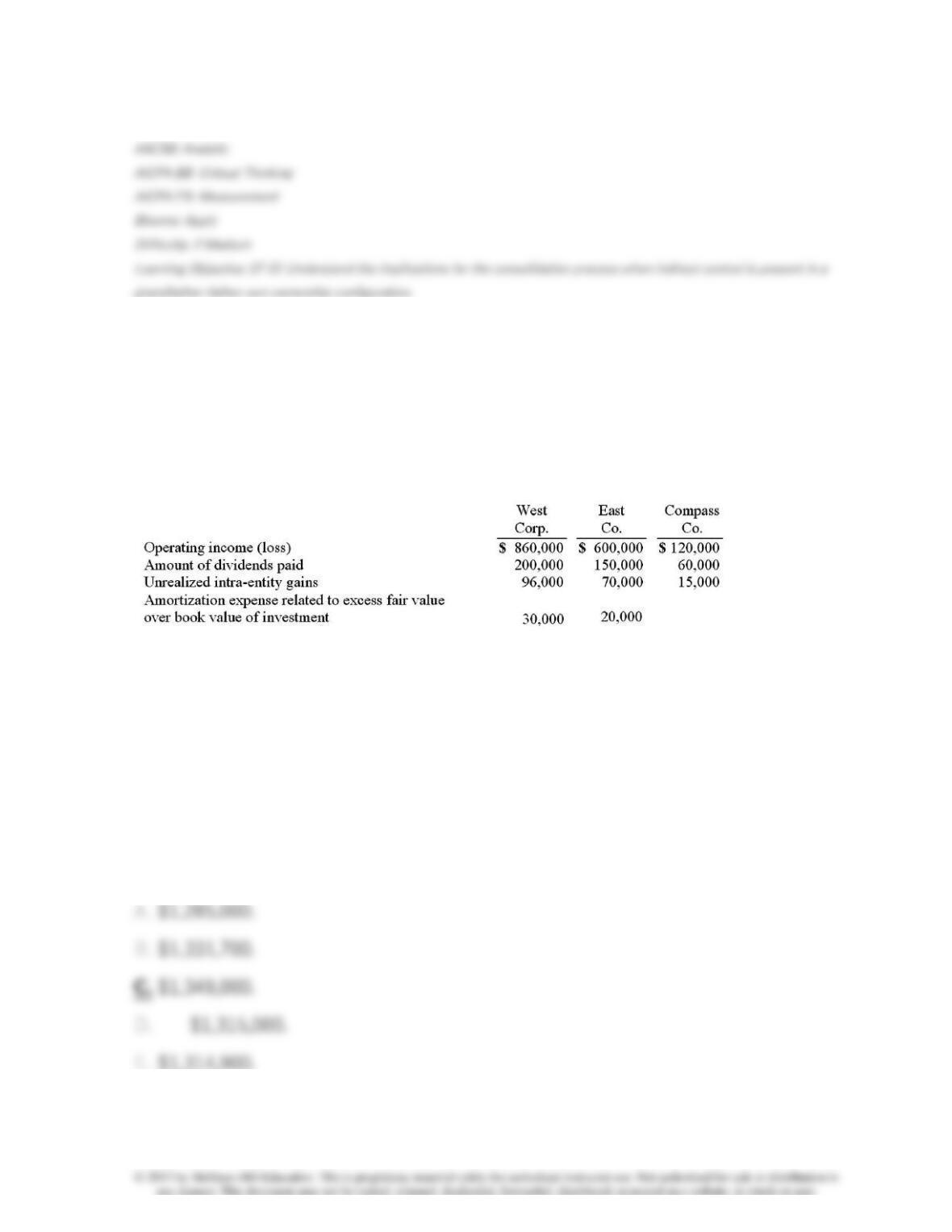

9. West Corp. owned 70% of the voting common stock of East Co. East owned

60% of Compass Co. West and East both used the

initial value method

to account

for their investments. The following information was available from the financial

statements and records of the three companies:

Operating income included unrealized intra-entity gains (which are related to

inventory transfers) but did not include dividend income from investment in

subsidiary.

What amount should have been reported for

consolidated net income

?

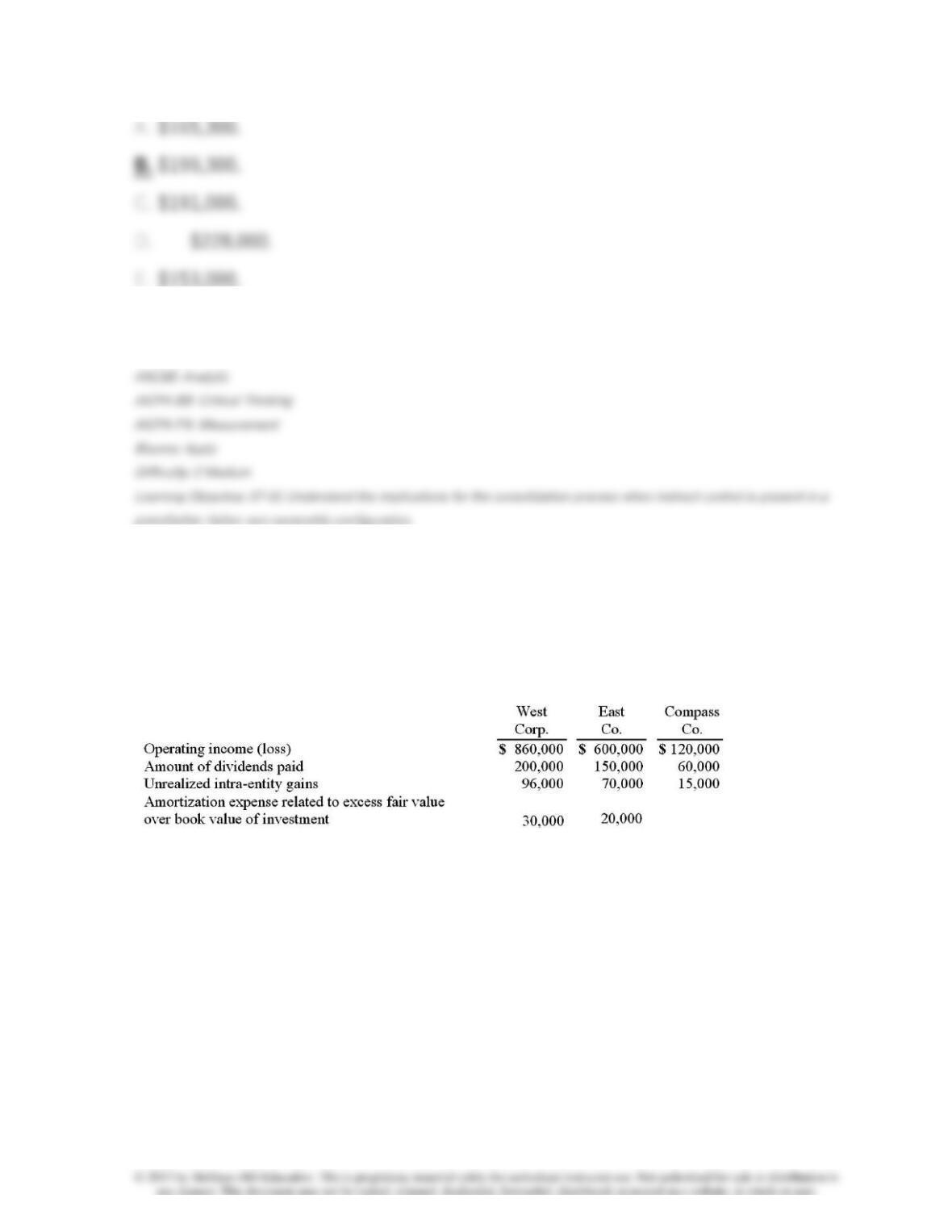

10. West Corp. owned 70% of the voting common stock of East Co. East owned

60% of Compass Co. West and East both used the

initial value method

to account

for their investments. The following information was available from the financial

statements and records of the three companies:

Operating income included unrealized intra-entity gains (which are related to

inventory transfers) but did not include dividend income from investment in

subsidiary.

For West Corp. and consolidated subsidiaries, what total amount would have

been reported for the

non-controlling interest’s share of subsidiaries’ net

income

?

11. West Corp. owned 70% of the voting common stock of East Co. East owned

60% of Compass Co. West and East both used the

initial value method

to account

for their investments. The following information was available from the financial

statements and records of the three companies:

Operating income included unrealized intra-entity gains (which are related to

inventory transfers) but did not include dividend income from investment in

subsidiary.

What amount of dividends did West Corp. receive from Compass Co.?

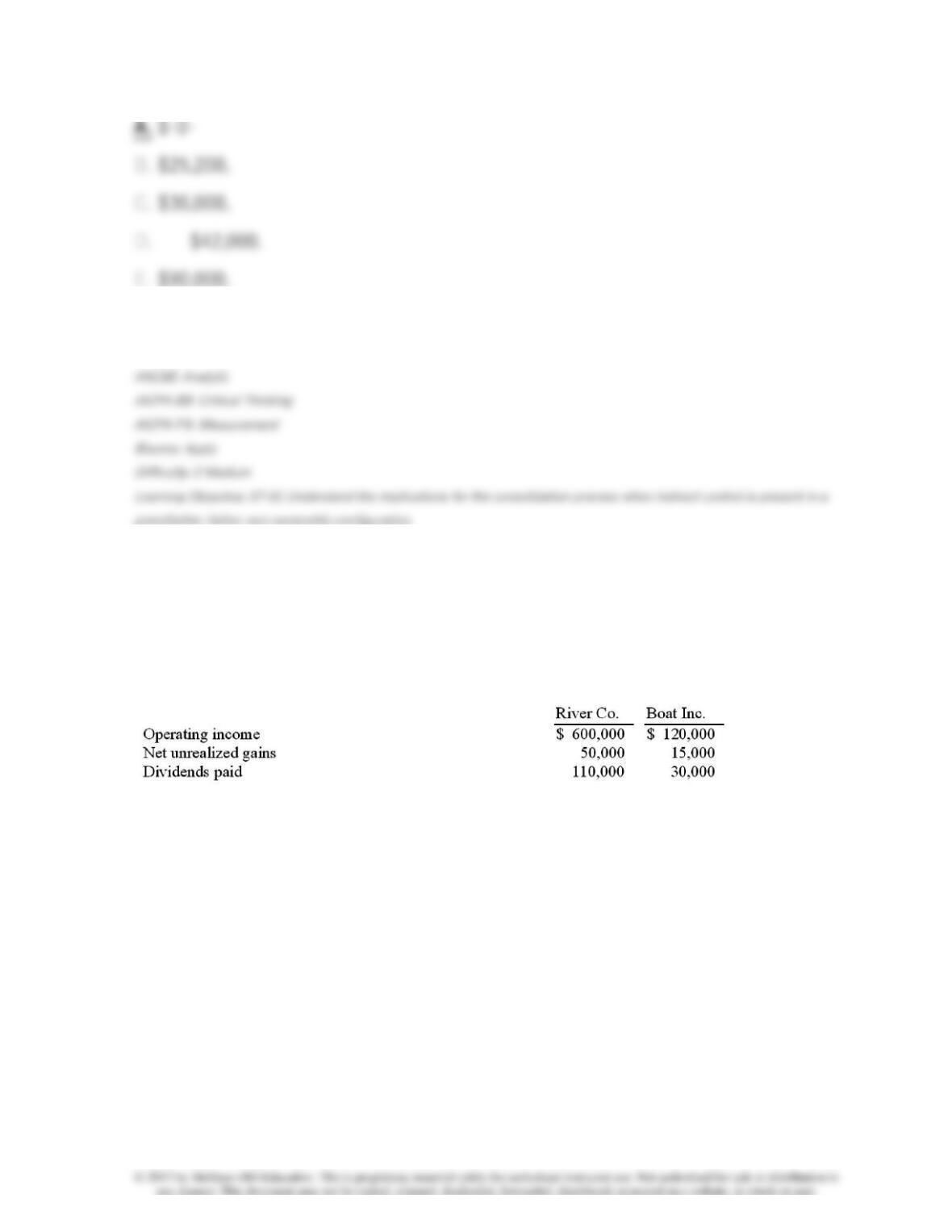

12. River Co. owned 80% of Boat Inc. The two companies filed a

consolidated

income tax return

and River used the

initial value method

to account for the

investment. The following information was available from the two companies’

financial statements:

Operating income included

net unrealized gains

, which are associated with

transfers of inventories between the two companies, but it did not include

dividends received from a subsidiary. The income tax rate was 30%.

What is the amount of

taxable income

reported on the

consolidated income tax

return

?

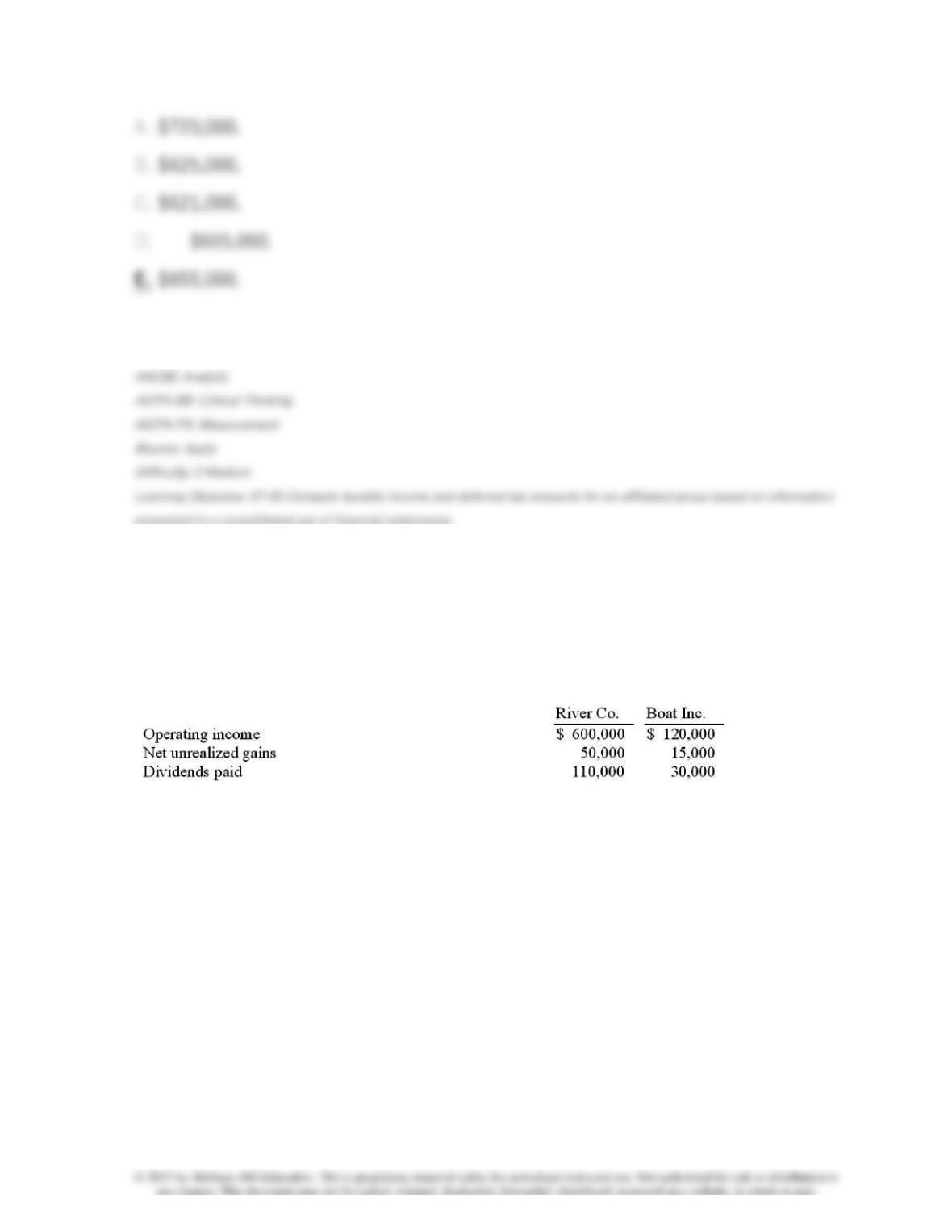

13. River Co. owned 80% of Boat Inc. The two companies filed a

consolidated

income tax return

and River used the

initial value method

to account for the

investment. The following information was available from the two companies’

financial statements:

Operating income included

net unrealized gains

, which are associated with

transfers of inventories between the two companies, but it did not include

dividends received from a subsidiary. The income tax rate was 30%.

What was the amount of

income tax expense

that should have been assigned to

Boat using the

percentage allocation method

?

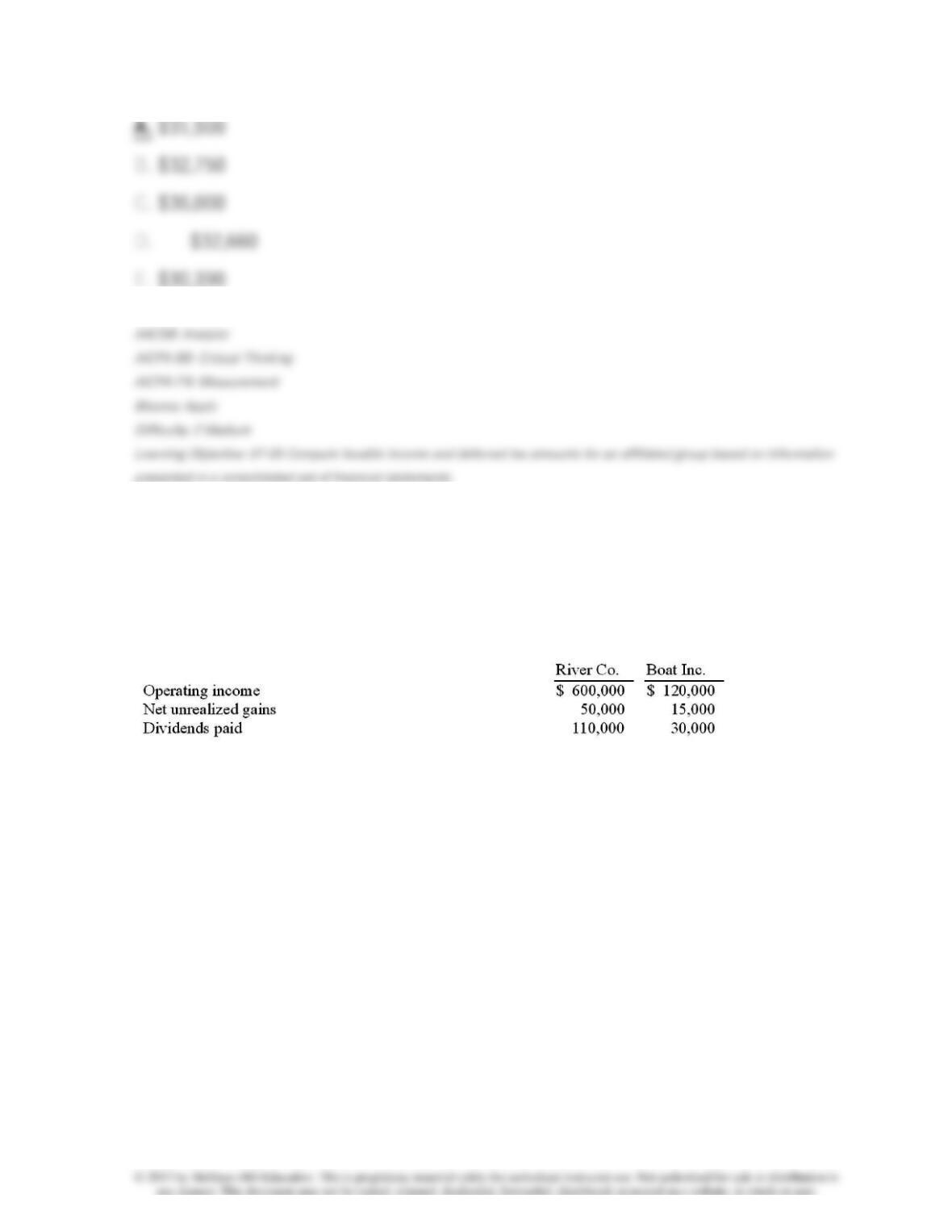

14. River Co. owned 80% of Boat Inc. The two companies filed a

consolidated

income tax return

and River used the

initial value method

to account for the

investment. The following information was available from the two companies’

financial statements:

Operating income included

net unrealized gains

, which are associated with

transfers of inventories between the two companies, but it did not include

dividends received from a subsidiary. The income tax rate was 30%.

What was the amount of

income tax expense

that should have been assigned to

Boat using the

separate return method

?

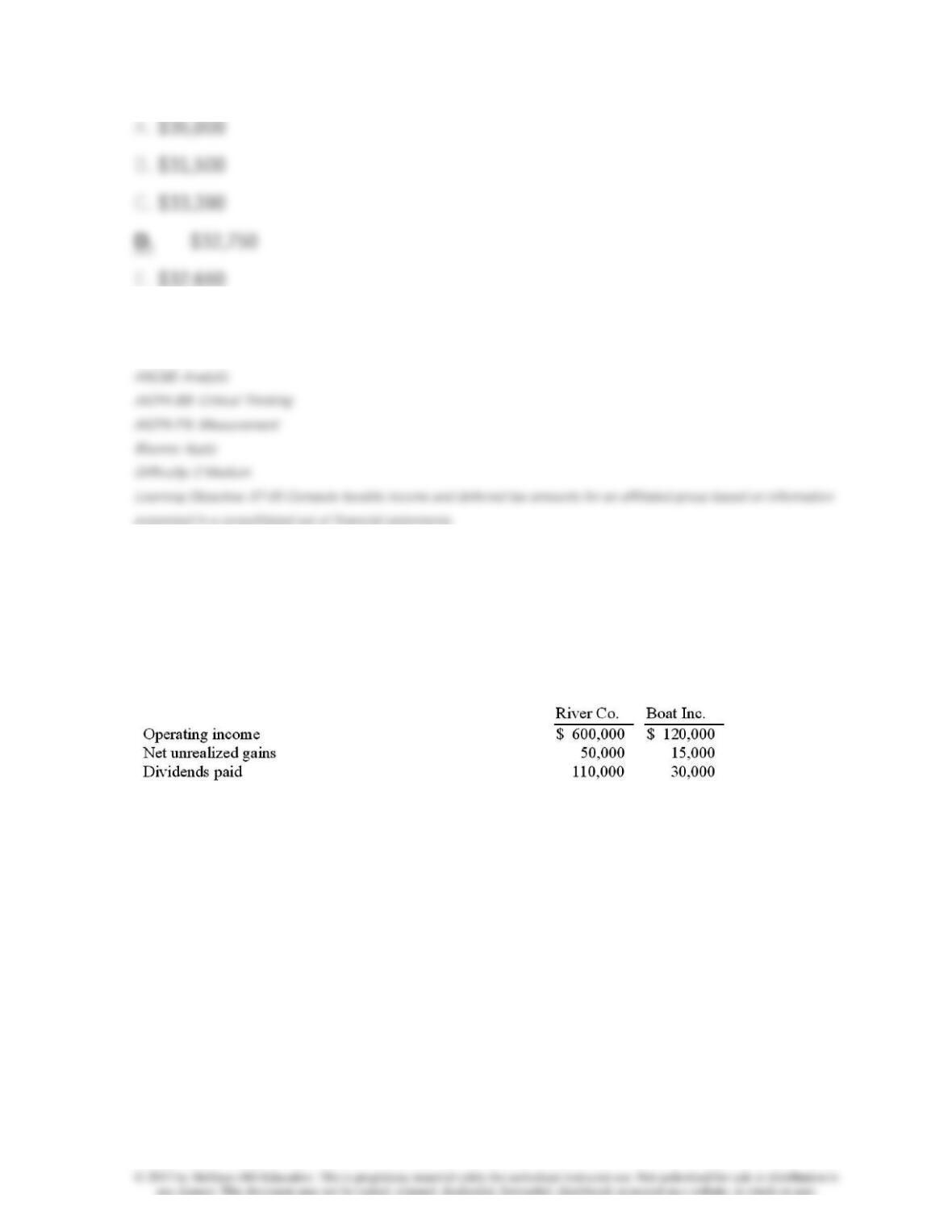

15. River Co. owned 80% of Boat Inc. The two companies filed a

consolidated

income tax return

and River used the

initial value method

to account for the

investment. The following information was available from the two companies’

financial statements:

Operating income included

net unrealized gains

, which are associated with

transfers of inventories between the two companies, but it did not include

dividends received from a subsidiary. The income tax rate was 30%.

What was the

non-controlling interest in Boat Inc.’s net income

, assuming that

the

separate return method

was used?

16. Prescott Corp. owned 90% of Bell Inc., while Bell owned 10% of the

outstanding common shares of Prescott. No goodwill or other allocations were

recognized in connection with either of these acquisitions. Prescott reported

operating income of $266,000 for 2011 whereas Bell earned $98,000 during the

same period. No investment income was included within either of these income

totals. On a

consolidated income statement

, what is the

non-controlling interest

in Bell’s net income

?

17. Prescott Corp. owned 90% of Bell Inc., while Bell owned 10% of the

outstanding common shares of Prescott. No goodwill or other allocations were

recognized in connection with either of these acquisitions. Prescott reported

operating income of $266,000 for 2011 whereas Bell earned $98,000 during the

same period. No investment income was included within either of these income

totals. How would the 10% investment in Prescott owned by Bell be presented in

the consolidated balance sheet?

18. On January 1, 2011, a subsidiary bought 10% of the outstanding shares of

its parent company. Although the total book value and fair value of the parent’s

net assets were $5.5 million, the consideration transferred for these shares was

$590,000. During 2011, the parent reported operating income (no investment

income was included) of $714,000 while paying dividends of $196,000. How were

these shares reported at December 31, 2011?

19. Jastoon Co. acquired all of Wedner Co. for $588,000 cash in a tax-free

transaction. On that date, the subsidiary had net assets with a $560,000 fair value

but a $420,000 book value and income tax basis. The income tax rate was 30%.

What amount of

goodwill

should have been recognized on the date of the

acquisition?

20. Beagle Co. owned 80% of Maroon Corp. Maroon owned 90% of Eckston Inc.

Operating income totals for 2011 are shown below; these figures contained no

investment income. Amortization expense was not required by any of these

acquisitions. Included in Eckston’s operating income was a $56,000 unrealized

gain on intra-entity transfers to Maroon.

The

accrual-based income of Eckston Inc.

is calculated to be

21. Beagle Co. owned 80% of Maroon Corp. Maroon owned 90% of Eckston Inc.

Operating income totals for 2011 are shown below; these figures contained no

investment income. Amortization expense was not required by any of these

acquisitions. Included in Eckston’s operating income was a $56,000 unrealized

gain on intra-entity transfers to Maroon.

The

accrual-based income of Maroon Corp.

is calculated to be

22. Beagle Co. owned 80% of Maroon Corp. Maroon owned 90% of Eckston Inc.

Operating income totals for 2011 are shown below; these figures contained no

investment income. Amortization expense was not required by any of these

acquisitions. Included in Eckston’s operating income was a $56,000 unrealized

gain on intra-entity transfers to Maroon.

The

accrual-based income of Beagle Co.

is calculated to be