1. Future costs that do not differ among the alternatives are not relevant in a decision.

2. Fixed costs are irrelevant in a decision.

3. Sunk costs are considered to be avoidable costs.

4. Avoidable costs are also called relevant costs.

5. An avoidable cost is a cost that can be eliminated (in whole or in part) as a result of

choosing one alternative over another.

6. A sunk cost is a cost that has already been incurred and that cannot be avoided regardless

of what action is chosen.

7. The book value of a machine, as shown on the balance sheet, is relevant in a decision

concerning the replacement of that machine by another machine.

8. If by dropping a product a firm can avoid more in fixed costs than it loses in contribution

margin, then the firm is better off economically if the product is dropped.

9. Generally, a product line should be dropped when the fixed costs that can be avoided by

dropping the product line are less than the contribution margin that will be lost.

10. The cost of a resource that has no alternative use in a make or buy decision problem has

an opportunity cost of zero.

11. Vertical integration is the involvement by a company in more than one of the steps from

securing basic raw materials to the production and distribution of a finished product.

12. Depreciation expense on existing factory equipment is generally relevant to a decision of

whether to accept or reject a special offer for a company’s product.

13. When a company has a production constraint, the product with the highest contribution

margin per unit of the constrained resource should be given highest priority.

14. Managers should not authorize working overtime at a work station that contains a

bottleneck.

15. Joint costs are not relevant to the decision to sell a product at the split-off point or to

process the product further.

16. Joint production costs are relevant costs in decisions about what to do with a product from

the split-off point onward in the production process.

17. Costs which are always relevant in decision making are those costs which are:

18. A general rule in relevant cost analysis is:

19. The opportunity cost of making a component part in a factory with no excess capacity is

the:

20. Freestone Company is considering renting Machine Y to replace Machine X. It is

expected that Y will waste less direct materials than does X. If Y is rented, X will be sold on the

open market. For this decision, which of the following factors is(are) relevant?

I. Cost of direct materials used

II. Resale value of Machine X

21. Which of the following are valid reasons for eliminating a product line?

I. The product line’s contribution margin is negative.

II. The product line’s traceable fixed costs plus its allocated common corporate costs are less

than its contribution margin.

22. When there is a production constraint, a company should emphasize the products with:

23. In a sell or process further decision, which of the following costs are relevant?

I. A variable production cost incurred prior to the split-off point.

II. An avoidable fixed production cost incurred after the split-off point.

24. Scherer Corporation is preparing a bid for a special order that would require 720 liters of

material U48N. The company already has 560 liters of this raw material in stock that originally

cost $6.30 per liter. Material U48N is used in the company’s main product and is replenished on a

periodic basis. The resale value of the existing stock of the material is $5.80 per liter. New stocks

of the material can be readily purchased for $6.65 per liter. What is the relevant cost of the 720

liters of the raw material when deciding how much to bid on the special order?

25. Cung Inc. has some material that originally cost $68,400. The material has a scrap value

of $30,100 as is, but if reworked at a cost of $1,400, it could be sold for $30,800. What would be

the incremental effect on the company’s overall profit of reworking and selling the material rather

than selling it as is as scrap?

26. Liffick Corporation is a specialty component manufacturer with idle capacity.

Management would like to use its extra capacity to generate additional profits. A potential

customer has offered to buy 6,200 units of component VFG. Each unit of VFG requires 8 units of

material C79 and 6 units of material X70. Data concerning these two materials follow:

Material C79 is in use in many of the company’s products and is routinely replenished. Material

X70 is no longer used by the company in any of its normal products and existing stocks would not

be replenished once they are used up.

What would be the relevant cost of the materials, in total, for purposes of determining a minimum

acceptable price for the order for product VFG?

27. Schemm Inc. regularly uses material F04E and currently has in stock 460 liters of the

material for which it paid $2,622 several weeks ago. If this were to be sold as is on the open

market as surplus material, it would fetch $5.25 per liter. New stocks of the material can be

purchased on the open market for $5.85 per liter, but it must be purchased in lots of 1,000 liters.

You have been asked to determine the relevant cost of 800 liters of the material to be used in a

job for a customer. The relevant cost of the 800 liters of material F04E is:

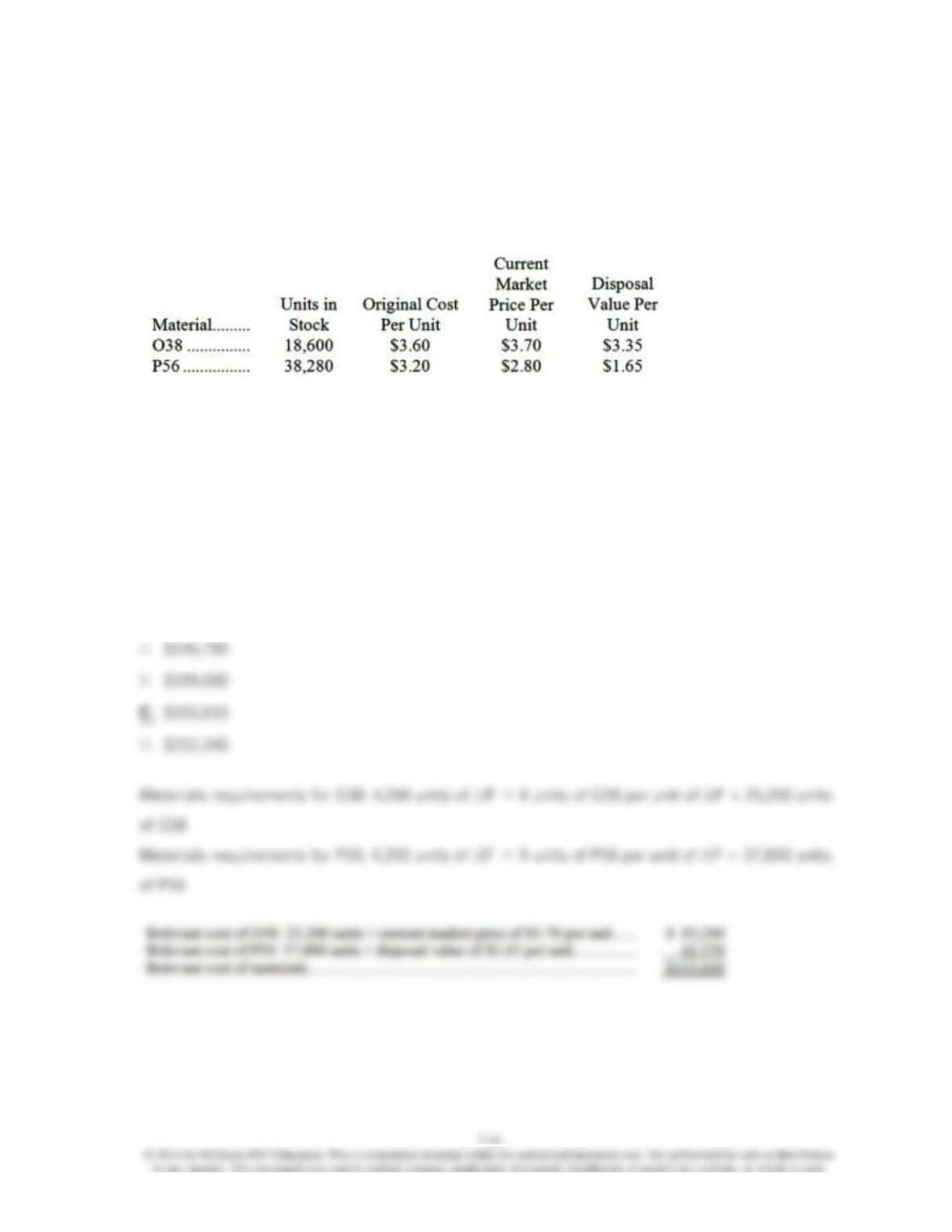

28. Stampka Corporation is a specialty component manufacturer with idle capacity.

Management would like to use its extra capacity to generate additional profits. A potential

customer has offered to buy 4,200 units of component JJF. Each unit of JJF requires 6 units of

material O38 and 9 units of material P56. Data concerning these two materials follow:

Material O38 is in use in many of the company’s products and is routinely replenished. Material

P56 is no longer used by the company in any of its normal products and existing stocks would not

be replenished once they are used up.

What would be the relevant cost of the materials, in total, for purposes of determining a minimum

acceptable price for the order for product JJF?

29. Janus Corporation has in stock 43,700 kilograms of material L that it bought five years

ago for $6.10 per kilogram. This raw material was purchased to use in a product line that has

been discontinued. Material L can be sold as is for scrap for $3.23 per kilogram. An alternative

would be to use material L in one of the company’s current products, E99D, which currently

requires 2 kilograms of a raw material that is available for $9.45 per kilogram. Material L can be

modified at a cost of $0.62 per kilogram so that it can be used as a substitute for this material in

the production of product E99D. However, after modification, 3 kilograms of material L is required

for every unit of product E99D that is produced. Janus Corporation has now received a request

from a company that could use material L in its production process. Assuming that Janus

Corporation could use all of its stock of material L to make product E99D or the company could

sell all of its stock of the material at the current scrap price of $3.23 per kilogram, what is the

minimum acceptable selling price of material L to the company that could use material L in its

own production process?

30. Lampshire Inc. is considering using stocks of an old raw material in a special project. The

special project would require all 160 kilograms of the raw material that are in stock and that

originally cost the company $1,136 in total. If the company were to buy new supplies of this raw

material on the open market, it would cost $7.25 per kilogram. However, the company has no

other use for this raw material and would sell it at the discounted price of $6.50 per kilogram if it

were not used in the special project. The sale of the raw material would involve delivery to the

purchaser at a total cost of $75 for all 160 kilograms. What is the relevant cost of the 160

kilograms of the raw material when deciding whether to proceed with the special project?

31. A study has been conducted to determine if Product A should be dropped. Sales of the

product total $200,000 per year; variable expenses total $140,000 per year. Fixed expenses

charged to the product total $90,000 per year. The company estimates that $40,000 of these fixed

expenses will continue even if the product is dropped. These data indicate that if Product A is

dropped, the company’s overall net operating income would:

32. The Kelsh Company has two divisions—North and South. The divisions have the following

revenues and expenses:

Management at Kelsh is pondering the elimination of North Division. If North Division were

eliminated, its traceable fixed expenses could be avoided. The total common corporate expenses

would be unaffected. Given these data, the elimination of North Division would result in an

overall company net operating income of:

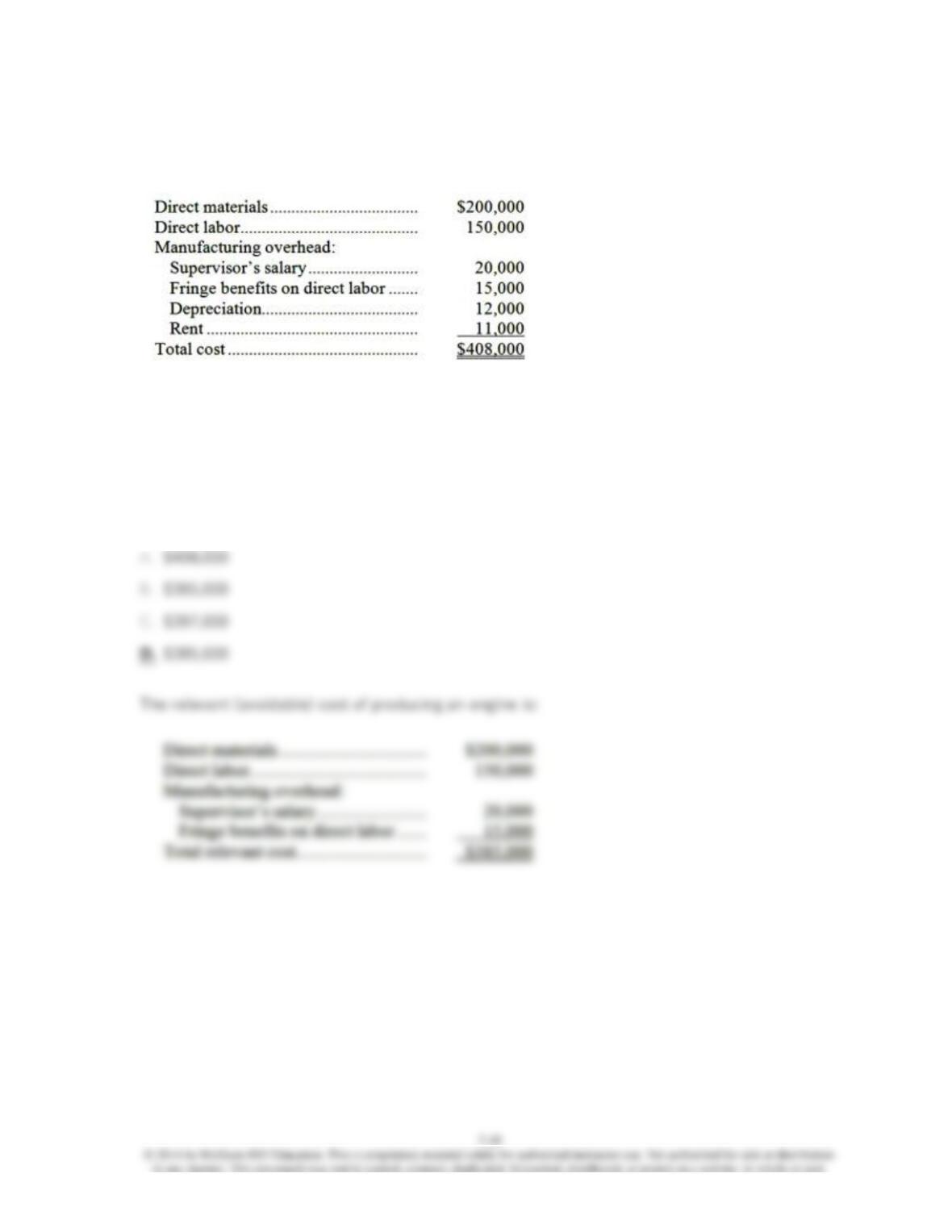

33. Power Systems Inc. manufactures jet engines for the United States armed forces on a

cost-plus basis. The production cost of a particular jet engine is shown below:

If production of this engine was discontinued, the production capacity would be idle, and the

supervisor would be laid off. The depreciation referred to above is for special equipment that

would have no resale value and that does not wear out through use. When asked to bid on the

next contract for this engine, the minimum unit price that Power Systems should bid is:

34. The management of Heider Corporation is considering dropping product J14V. Data from

the company’s accounting system appear below:

In the company’s accounting system all fixed expenses of the company are fully allocated to

products. Further investigation has revealed that $211,000 of the fixed manufacturing expenses

and $172,000 of the fixed selling and administrative expenses are avoidable if product J14V is

discontinued. What would be the effect on the company’s overall net operating income if product

J14V were dropped?