Chapter 6: Receivables and Inventories

67. Inventory costing methods place primary emphasis on assumptions about:

a. flow of goods.

b. flow of costs.

c. flow of goods or costs depending on the method.

d. flow of values.

68. When merchandise sold is assumed to be in the order in which the expenditures were made,

the inventory costing method is called:

a. first-in, last-out.

b. last-in, first-out.

c. first-in, first-out.

d. average cost.

69. Under which method of inventory costing is the ending inventory assumed to be composed of

the most recent costs?

a. Average cost

b. Last-in, first-out

c. First-in, last-out

d. First-in, first-out

70. The two most widely used methods for determining the cost of inventory are:

a. FIFO and LIFO.

b. FIFO and average cost.

c. LIFO and average cost.

d. specific identification and average cost.

71. The inventory costing method that assigns the most recent costs to cost of good sold is:

a. FIFO.

b. LIFO.

c. average cost.

d. specific identification.

Chapter 6: Receivables and Inventories

72. Under which method of inventory costing is the cost flow assumed to be in the reverse order in

which the expenditures were made?

a. Average cost

b. Last-in, first-out

c. First-in, first-out

d. Specific identification method

The inventory data for an item for November are:

Nov. 1

Inventory

20 units at $25 each

10

Purchase

25 units at $20 each

30

Purchase

20 units at $22 each

Sale

35 units

73. Using the first-in, first-out method, what is the cost of the merchandise inventory of 30 units

on November 30?

a. $640

b. $660

c. $700

d. $600

74. Using the last-in, first-out method, what is the cost of the merchandise inventory of 30 units on

November 30?

a. $600

b. $660

c. $640

d. $700

75. Use the following data to calculate the cost of ending inventory under the FIFO method.

September 1

Beginning Inventory

15 units at $20 each

September 10

Purchase

20 units at $25 each

September 20

Purchase

25 units at $28 each

September 30

Ending Inventory

30 units

a. $825

b. $750

c. $675

d. $840

Chapter 6: Receivables and Inventories

76. Use the following data to calculate cost of merchandise sold under FIFO method.

September 1

Beginning Inventory

15 units at $20 each

September 10

Purchase

20 units at $25 each

September 20

Purchase

25 units at $28 each

September 30

Ending Inventory

30 units

a. $825

b. $750

c. $675

d. $600

77. Use the following data to calculate the cost of ending inventory using the LIFO method.

September 1

Beginning Inventory

15 units at $20 each

September 10

Purchase

20 units at $25 each

September 20

Purchase

25 units at $28 each

September 30

Ending Inventory

30 units

a. $825

b. $750

c. $675

d. $600

78. Use the following data to calculate the cost of ending inventory under average cost method.

September 1

Beginning Inventory

20 units at $10 each

September 10

Purchase

25 units at $20 each

September 20

Purchase

40 units at $25 each

September 30

Ending Inventory

35 units

a. $992

b. $400

c. $875

d. $700

Chapter 6: Receivables and Inventories

79. Calculate the cost of ending inventory using FIFO method.

1/1

Beginning inventory

10 units at $10 each

2/28

Purchase

40 units at $12 each

5/10

Purchase

50 units at $14 each

9/20

Purchase

30 units at $16 each

12/31

a. $800

Ending inventory

50 units

b. $760

c. $580

d. $500

b

80. During a period of consistently rising prices, the method of inventory costing that will result in

reporting the greatest cost of merchandise sold is:

a. FIFO.

b. average cost.

c. LIFO.

d. All methods will generate the same cost of merchandise sold.

81. If merchandise inventory is being valued at cost and the price level is steadily rising, the

method of costing that will yield the highest net income is:

a. average cost.

b. LIFO.

c. FIFO.

d. All methods will generate the same net income.

82. If merchandise inventory is being valued at cost and the price level is consistently rising,

which method of costing will yield the highest inventory?

a. Average cost

b. LIFO

c. FIFO

d. All methods will generate the same gross profit.

83. If merchandise inventory is being valued at cost and the price level is steadily falling, which

method of costing will yield the largest gross profit?

a. Average cost

b. LIFO

c. FIFO

d. All methods will generate the same gross profit.

Chapter 6: Receivables and Inventories

84. If the cost of an item of inventory is $60 and the current replacement cost is $65, the amount

included in inventory according to the lower-of-cost-or market method is:

a. $5.

b. $60.

c. $65.

d. $125.

85. If the cost of an item of inventory is $70, the current replacement cost is $65, and the sales

price is $85, the amount included in inventory according to the lower-of-cost-or-market

method is:

a. $65.

b. $70.

c. $85.

d. $160.

86. Merchandise inventory is reported on the balance sheet in the section entitled:

a. current assets.

b. fixed assets.

c. current liabilities.

d. stockholders’ equity.

87. The accounts receivable turnover is computed by dividing:

a. total assets by average accounts receivable.

b. net sales by average accounts receivable.

c. net income by average accounts receivable.

d. net purchases by average accounts receivable.

88. Inventory turnover is calculated by dividing:

a. cost of merchandise sold by average inventory.

b. amount of total asset by average inventory.

c. cost of inventory by average inventory.

d. amount of current assets by average inventory.

Chapter 6: Receivables and Inventories

89. If net sales is $550,000, beginning inventory is $110,000, and ending inventory is $125,000,

how much would be the accounts receivables turnover?

a. 4.4

b. 5.0

c. 4.7

d. 4.0

90. If sales is $1,000,000, cost of merchandise sold is $750,000, and average inventory is

$220,000, how much would be inventory turnover?

a. 1.1

b. 3.4

c. 1.3

d. 4.5

91. Classify the following as either Current Assets (CA), Investments (I), or both (CA and I).

(a) Trade Receivables

(b) Note Receivable due in 30 days

(c) Interest Receivable on note due in 30 days

(d) Note Receivable due in 2 years

(e) Five-year Note Receivable due in a series of equal annual payments

92. Other than accounts receivable and notes receivable, name other receivables that might be

included on the balance sheet.

93.

(a)

If the interest on a note is $1,500, the interest rate is 5%, and the time is 90 days, what

is the principal? (Assume 360 days in a year)

(b)

If the principal of a note is $50,000, the interest is $1,000, and the time is 60 days,

what is the interest rate? (Assume 360 days in a year)

Chapter 6: Receivables and Inventories

94. Determine the due date and amount of interest due at maturity on the following notes (Assume

360 days in a year):

Origination

Date

Face

Amount

Term

of Note

Interest

Rate

Maturity

Date

Interest

Amount

(a) March 1

$5,000

60 days

9%

_______

_______

(b) May 15

$9,000

120 days

8%

_______

_______

95. Determine the amount to be added to Allowance for Doubtful Accounts in each of the

following cases:

(a)

Balance of $3,000 in the allowance account just prior to adjustment. Analysis of

accounts receivable indicates doubtful accounts of $25,000.

(b)

Balance of $500 in the allowance account just prior to adjustment. Uncollectibles are

estimated at 2% of sales, which totaled $800,000 for the year.

96. Beginning inventory, purchases, and sales data for May are as follows:

May 1

Inventory

20 units at $40 each

12

Purchase

18 units at $42 each

Sales

25 units

The business uses the first-in, first-out inventory costing method. Determine the cost of the

inventory on hand at the end of May.

97. The following units are available for sale during the year:

January 1

Beginning Inventory

10 units at $18 each

April 3

Purchase

30 units at $20 each

August 31

Purchase

28 units at $25 each

September 29

Purchase

17 units at $30 each

December 31

Ending Inventory

21 units

Determine ending inventory cost by (a) FIFO method, (b) LIFO method, and (c) average cost

method.

Chapter 6: Receivables and Inventories

98. Beginning inventory, purchases and sales data for the month are as follows:

Beginning Inventory 10 units at $42 each

First Purchase 15 units at $44 each

Second Purchase 13 units at $45 each

Sales 26 units

Determine the total cost of ending inventory according to (a) FIFO method and (b) LIFO

method.

99.

September 5 Purchase 65 units at $6 each

September 13 Purchase 55 units at $8 each

September 29 Purchase 44 units at $10 each

September 30 Ending Inventory 70 units

Determine ending inventory cost by (a) FIFO method, (b) LIFO method, and (c) average cost method.

100. On the basis of the following data related to current assets for Mission Co. at December 2016,

prepare a partial balance sheet in good form.

Cash and cash equivalents

$100,000

Notes receivable

50,000

Accounts receivable

290,000

Allowance for doubtful accounts

20,000

Interest receivable

750

Merchandise inventory at lower-of-cost-(first-in, first-out method) or-market

120,000

Chapter 6: Receivables and Inventories

101. Prepare the Current Assets section of a balance sheet using some or all of the following

accounts:

Cash

Property, Plant, and Equipment

Accounts Receivable

Notes Receivable—90-day note

Merchandise Inventory

Allowance for Doubtful Accounts

Interest Receivable

Prepaid Advertising

Sales Returns and Allowances

102. Indicate the section of the balance sheet (current assets, fixed assets, investments, current

liabilities, long-term liabilities, stockholders’ equity) in which each of the following is

reported:

(a) Note receivable due in 3 years

(b) Note receivable due in 90 days

(c) Allowance for doubtful accounts

103. Beginning inventory, purchases, and sales for Product XCX are as follows:

Oct. 1

Beginning Inventory

24 units

at

$12 each

Oct. 17

Purchase

10 units

at

$15 each

Oct. 30

Sale

25 units

Assuming a periodic inventory system and the first-in, first-out method, determine (a) the cost

of the merchandise sold and (b) the inventory on October 31.

Chapter 6: Receivables and Inventories

104. Beginning inventory, purchases, and sales for Product XCX are as follows:

Oct. 1

Beginning Inventory

24 units

at

$12 each

Oct. 17

Purchase

10 units

at

$14 each

Oct. 30

Sale

52 units

Assuming a periodic inventory system and the last-in, first-out method, determine (a) the cost

of the merchandise sold for the October 30 sale and (b) the inventory on October 31.

105. The units of Product YY2 available for sale during the year were as follows:

Apr. 1

Inventory

16 units

at

$30 each

Jun. 16

Purchase

30 units

at

$33 each

Sep. 28

Purchase

45 units

at

$37 each

There are 17 units of the product in the physical ending inventory at March 31. The periodic

inventory system is used. Determine the ending inventory cost by (a) FIFO, (b) LIFO, and (c)

average cost methods.

106. The units of Product YY2 available for sale during the year were as follows:

Apr 1

Inventory

16 units

at

$30 each

Jun 16

Purchase

30 units

at

$33 each

Sep 28

Purchase

45 units

at

$37 each

There are 15 units of the product in the physical inventory at March 31. The periodic inventory

system is used. Determine the difference in gross profit between the LIFO and FIFO inventory

cost systems.

Chapter 6: Receivables and Inventories

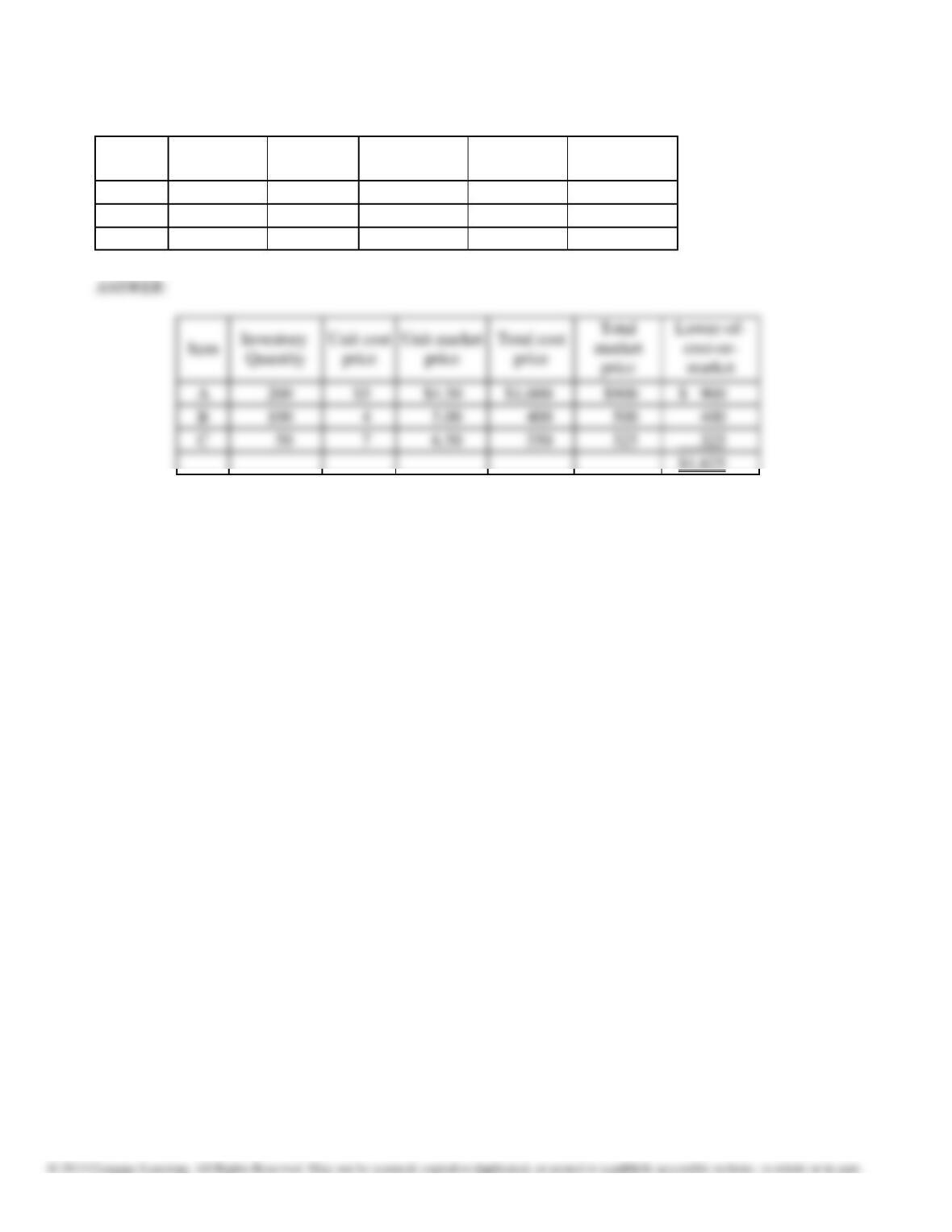

107. Using the lower-of-cost-or-market method of inventory valuation, what should the total

inventory value be for the following items:

Item

Inventory

Quantity

Unit cost

price

Unit market

price

Total cost

price

Total market

price

A

200

$5

$4.50

$1,000

$900

B

100

4

5.00

400

500

C

50

7

6.50

350

325

$5

$4.50

5.00

6.50