Name:

Class:

Date:

chapter 6

Indicate whether the statement is true or false.

1. Companies with large amounts of fixed costs will generally have a high operating leverage.

a.

True

b.

False

2. Variable costs are costs that vary in total in direct proportion to changes in the activity level.

a.

True

b.

False

3. Variable costs are costs that remain constant in total dollar amount as the level of activity changes.

a.

True

b.

False

4. A rental cost of $20,000 plus $0.70 per machine hour of use is an example of a mixed cost.

a.

True

b.

False

5. If a business sells two products, it is not possible to estimate the break-even point.

a.

True

b.

False

6. Total fixed costs change as the level of activity changes.

a.

True

b.

False

7. Cost behavior refers to the manner in which a cost changes as the related activity changes.

a.

True

b.

False

8. Garmo Co. has an operating leverage of 5. Next year’s sales are expected to increase by 10%. The company’s operating

income will increase by 50%.

a.

True

b.

False

9. Only a single line, which represents the difference between total sales revenues and total costs, is plotted on the cost-

volume-profit chart.

a.

True

b.

False

10. Only a single line, which represents the difference between total sales revenues and total costs, is plotted on the profit-

volume chart.

a.

True

b.

False

11. If the volume of sales is $7,000,000 and sales at the break-even point amount to $4,800,000, the margin of safety is

Name:

Class:

Date:

chapter 6

45.8%.

a.

True

b.

False

12. If fixed costs are $850,000 and the unit contribution margin is $50, profit is zero when 15,000 units are sold.

a.

True

b.

False

13. If the unit selling price is $40, the volume of sales is $3,000,000, sales at the break-even point amount to $2,500,000,

and the maximum possible sales are $3,300,000, the margin of safety is 11,500 units.

a.

True

b.

False

14. If direct materials cost per unit increases, the break-even point will increase.

a.

True

b.

False

15. Direct materials and direct labor costs are examples of variable costs of production.

a.

True

b.

False

16. If fixed costs are $450,000 and the unit contribution margin is $50, the sales necessary to earn an operating income of

$50,000 are 10,000 units.

a.

True

b.

False

17. The relevant range is useful for analyzing cost behavior for management decision-making purposes.

a.

True

b.

False

18. Cost-volume-profit analysis can be presented in both equation form and graphic form.

a.

True

b.

False

19. If employees accept a wage contract that increases the unit contribution margin, the break-even point will decrease.

a.

True

b.

False

20. Cost-volume-profit relationships in a service company are measured with respect to customers and activities, rather

than units of product.

a.

True

b.

False

21. In order to choose the proper activity base for a cost, managerial accountants must be familiar with the operations of

the entity.

a.

True

Name:

Class:

Date:

chapter 6

b.

False

22. The reliability of cost-volume-profit analysis does not depend on the assumption that costs can be accurately divided

into fixed and variable components.

a.

True

b.

False

23. If the volume of sales is $6,000,000 and sales at the break-even point amount to $4,800,000, the margin of safety is

25%.

a.

True

b.

False

24. Rental charges of $40,000 per year plus $3 for each machine hour over 18,000 hours is an example of a fixed cost.

a.

True

b.

False

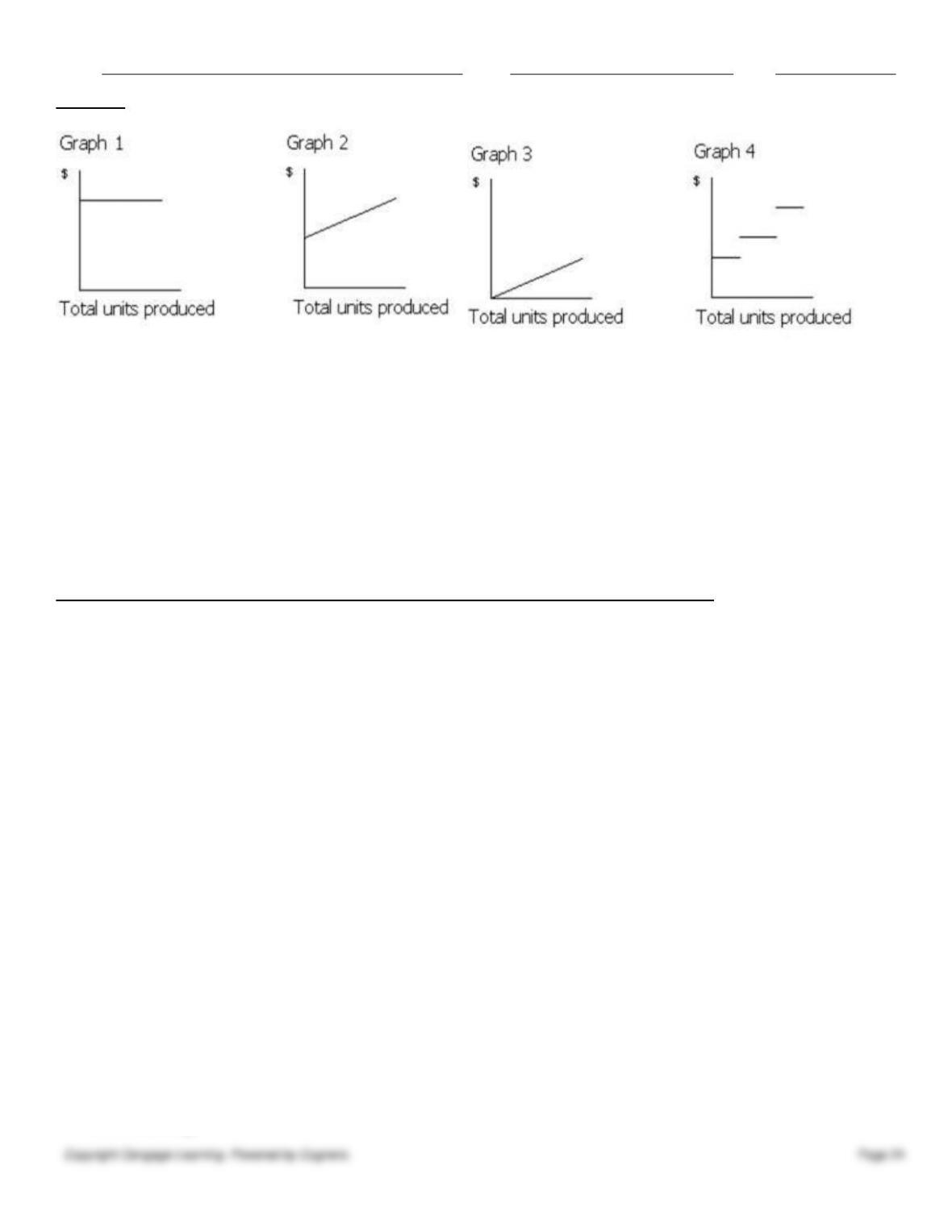

25. A low operating leverage is normal for highly automated industries.

a.

True

b.

False

26. If fixed costs are $500,000 and variable costs are 60% of break-even sales, profit is zero when sales revenue is

$930,000.

a.

True

b.

False

27. If fixed costs are $650,000 and the unit contribution margin is $30, the sales necessary to earn an operating income of

$30,000 are 14,000 units.

a.

True

b.

False

28. Variable costs are costs that vary on a per-unit basis with changes in the activity level.

a.

True

b.

False

29. If the unit selling price is $40, the volume of sales is $3,000,000, sales at the break-even point amount to $2,500,000,

and the maximum possible sales are $3,300,000, the margin of safety is 14,500 units.

a.

True

b.

False

30. If yearly insurance premiums are increased, this change in fixed costs will result in an increase in the break-even

point.

a.

True

b.

False

31. The ratio that indicates the percentage of each sales dollar available to cover the fixed costs and to provide operating

income is termed the contribution margin ratio.

a.

True

Name:

Class:

Date:

chapter 6

b.

False

32. If the property tax rates are increased, this change in fixed costs will result in a decrease in the break-even point.

a.

True

b.

False

33. The relevant activity base for a cost depends upon which base is most closely associated with the cost and the

decision-making needs of management.

a.

True

b.

False

34. The point in operations at which revenues and expenses are exactly equal is called the break-even point.

a.

True

b.

False

35. For purposes of analysis, mixed costs can generally be separated into their variable and fixed components.

a.

True

b.

False

36. The fixed cost per unit varies with changes in the level of activity.

a.

True

b.

False

37. If a business sells four products, it is not possible to estimate the break-even point.

a.

True

b.

False

38. Variable costs are costs that remain constant on a per-unit basis as the level of activity changes.

a.

True

b.

False

39. Direct materials cost that varies with the number of units produced is an example of a fixed cost of production.

a.

True

b.

False

40. Total variable costs change as the level of activity changes.

a.

True

b.

False

41. Because variable costs are assumed to change in direct proportion to changes in the activity level, the graph of the

variable costs when plotted against the activity level appears as a circle.

a.

True

b.

False

42. The data required for determining the break-even point for a business are the total estimated fixed costs for a

period stated as a percentage of sales.

Name:

Class:

Date:

chapter 6

a.

True

b.

False

43. The amount of dollars available from each unit of sales to cover fixed cost and profit is the unit variable cost.

a.

True

b.

False

44. A mixed cost has characteristics of both a variable and a fixed cost.

a.

True

b.

False

45. If employees accept a wage contract that decreases the unit contribution margin, the break-even point will decrease.

a.

True

b.

False

46. If sales total $2,000,000, fixed costs total $800,000, and variable costs are 60% of sales, the contribution margin ratio

is 40%.

a.

True

b.

False

47. The range of activity over which changes in cost are of interest to management is called the relevant range.

a.

True

b.

False

48. Even if a business sells six products, it is possible to estimate the break-even point.

a.

True

b.

False

49. If direct materials cost per unit decreases, the amount of sales necessary to earn a desired amount of profit will

decrease.

a.

True

b.

False

50. The contribution margin ratio is the same as the profit-volume ratio.

a.

True

b.

False

51. Cost behavior refers to the methods used to estimate costs for use in managerial decision making.

a.

True

b.

False

52. Break-even analysis is one type of cost-volume-profit analysis.

a.

True

b.

False

53. With respect to cost-volume-profit analysis for service companies, a cost may be defined as fixed or variable,

Name:

Class:

Date:

chapter 6

depending on the unit of analysis.

a.

True

b.

False

54. If direct materials cost per unit increases, the break-even point will decrease.

a.

True

b.

False

55. A production supervisor’s salary that does not vary with the number of units produced is an example of a fixed cost.

a.

True

b.

False

56. If sales total $2,000,000, fixed costs total $800,000, and variable costs are 60% of sales, the contribution margin ratio

is 60%.

a.

True

b.

False

57. Unit variable cost does not change as the number of units of activity changes.

a.

True

b.

False

58. The break-even point is not as relevant in a service company as it is in a manufacturing company.

a.

True

b.

False

59. Variable costs as a percentage of sales are equal to 100% minus the contribution margin ratio.

a.

True

b.

False

Indicate the answer choice that best completes the statement or answers the question.

60. Which of the following describes the behavior of the fixed cost per unit?

a.

decreases with increasing production

b.

decreases with decreasing production

c.

remains constant with changes in production

d.

increases with increasing production

61. If fixed costs are $700,000 and the unit contribution margin is $17, the amount of units that must be sold in order to

realize an operating income of $100,000 is

a.

5,000 units

b.

41,176 units

c.

47,059 units

d.

58,882 units

62. Given the following cost and activity observations for Bounty Company’s utilities, use the high-low method to

determine Bounty’s variable utilities cost per machine hour. Round your answer to the nearest cent.

Name:

Class:

Date:

chapter 6

Cost

Machine Hours

March

$3,100

15,000

April

2,700

10,000

May

2,900

12,000

June

3,600

18,000

a.

$10.00

b.

$0.67

c.

$0.63

d.

$0.11

63. The point where the profit line intersects the horizontal axis on the profit-volume chart represents the

a.

maximum possible operating loss

b.

maximum possible operating income

c.

total fixed costs

d.

break-even point

64. Payton Industries has fixed costs of $490,000, the unit selling price is $35, and the unit variable costs are $20. The

break-even sales (units) if fixed costs are reduced by $40,000 is

a.

32,667 units

b.

14,000 units

c.

30,000 units

d.

24,500 units

65. If fixed costs are $500,000, the unit selling price is $55, and the unit variable costs are $30, the break-even sales

(units) if fixed costs are increased by $80,000 is

a.

10,545 units

b.

19,333 units

c.

23,200 units

d.

25,000 units

66. Given the following costs and activities for Dance Company’s electrical costs, use the high-low method to determine

Dance’s variable electrical costs per machine hour.

Costs

Machine Hours

August

$11,700

15,000

September

13,200

17,500

October

11,400

14,500

a.

$2.08

b.

$6.00

c.

$0.60

d.

$1.20

67. Which of the following types of cost is shown in the cost data below?

Total Cost

Number of Units

Name:

Class:

Date:

chapter 6

$20

1

40

2

60

3

80

4

a.

mixed cost

b.

variable cost

c.

fixed cost

d.

period cost

68. If sales are $400,000, variable costs are 80% of sales, and operating income is $40,000, the operating leverage is

a.

0.0

b.

7.5

c.

2.0

d.

1.3

69. If fixed costs are $46,800, the unit selling price is $42, and the unit variable costs are $24, the break-even sales (units)

if the variable costs are decreased by $2 is

a.

2,127 units

b.

1,114 units

c.

2,340 units

d.

1,950 units

70. Zeke Company sells 25,000 units at $21 per unit. Variable costs are $10 per unit, and fixed costs are $75,000. The

contribution margin ratio and the unit contribution margin, respectively, are

a.

47% and $11 per unit

b.

53% and $7 per unit

c.

47% and $8 per unit

d.

52% and $11 per unit

71. The difference between the current sales revenue and the sales at the break-even point is called the

a.

contribution margin

b.

margin of safety

c.

price factor

d.

operating leverage

Carter Co. sells two products: Arks and Bins. Last year, Carter sold 14,000 units of Arks and 56,000 units of Bins. Related

data are as follows:

Product

Unit Selling

Price

Unit Variable

Cost

Unit Contribution

Margin

Arks

$120

$80

$40

Bins

80

60

20

72. Carter Co.’s sales mix last year was

a.

20% Arks; 80% Bins

Name:

Class:

Date:

chapter 6

b.

12% Arks; 28% Bins

c.

70% Arks; 30% Bins

d.

40% Arks; 20% Bins

73. Lee Company’s sales are $525,000, variable costs are 53% of sales, and operating income is $19,000. The

contribution margin ratio is

a.

47.0%

b.

26.5%

c.

9.5%

d.

53.0%

74. Which of the following conditions would cause the break-even point to decrease?

a.

total fixed costs increase

b.

unit selling price decreases

c.

unit variable cost decreases

d.

unit variable cost increases

Carter Co. sells two products: Arks and Bins. Last year, Carter sold 14,000 units of Arks and 56,000 units of Bins. Related

data are as follows:

Product

Unit Selling

Price

Unit Variable

Cost

Unit Contribution

Margin

Arks

$120

$80

$40

Bins

80

60

20

75. Carter Co.’s unit contribution margin of E was

a.

$24

b.

$60

c.

$92

d.

$20

76. If fixed costs are $500,000 and the unit contribution margin is $20, the break-even point in units if fixed costs are

reduced by $80,000 is

a.

25,000 units

b.

29,000 units

c.

4,000 units

d.

21,000 units

77. Thompson Company manufactures and sells cookware. Because of current trends, it expects to increase sales by 15%

next year. If this expected level of production and sales occurs and plant expansion is not needed, how should this

increase affect next year’s total amounts for the following costs?

Variable Costs Fixed Costs Mixed Costs

a.

increase increase increase

b.

increase no change increase

c.

no change no change increase

Name:

Class:

Date:

chapter 6

d.

decrease increase increase

Rusty Co. sells two products: X and Y. Last year, Rusty sold 5,000 units of X and 35,000 units of Y. Related data are as

follows:

Unit Selling

Unit Variable

Unit Contribution

Product

Price

Cost

Margin

X

$110

$70

$40

Y

70

50

20

78. For break-even analysis, the unit variable cost of E was

a.

$52.50

b.

$70.00

c.

$120.00

d.

$50.00

79. Variable costs as a percentage of sales for Lemon Inc. are 80%, current sales are $600,000, and fixed costs are

$130,000. How much will operating income change if sales increase by $40,000?

a.

$8,000 increase

b.

$8,000 decrease

c.

$30,000 decrease

d.

$30,000 increase

80. The graph of a variable cost when plotted against its related activity base appears as a

a.

circle

b.

rectangle

c.

straight line

d.

curved line

81. Beemer’s sales are $400,000, variable costs are 75% of sales, and operating income is $50,000. The operating leverage

is

a.

2.5

b.

7.5

c.

2.0

d.

0

82. If fixed costs are $400,000 and the unit contribution margin is $20, the amount of units that must be sold in order to

have a zero profit is

a.

25,000 units

b.

10,000 units

c.

400,000 units

d.

20,000 units

83. Rocky Company reports the following data:

Sales

$800,000

Name:

Class:

Date:

chapter 6

Variable costs

300,000

Fixed costs

120,000

Rocky Company’s operating leverage is

a.

6.7

b.

2.7

c.

1.0

d.

1.3

84. If fixed costs increased and variable costs per unit decreased, the break-even point

a.

would increase

b.

would decrease

c.

would remain the same

d.

cannot be determined from the data given

85. Which of the following statements is true regarding fixed and variable costs?

a.

Both costs are constant when considered on a per-unit basis.

b.

Both costs are constant when considered on a total basis.

c.

Fixed costs are constant in total, and variable costs are constant per unit.

d.

Variable costs are constant in total, and fixed costs vary in total.

86. If fixed costs are $250,000, the unit selling price is $125, and the unit variable costs are $73, the break-even sales

(units) is

a.

3,425 units

b.

2,381 units

c.

2,000 units

d.

4,808 units

Carter Co. sells two products: Arks and Bins. Last year, Carter sold 14,000 units of Arks and 56,000 units of Bins. Related

data are as follows:

Product

Unit Selling

Price

Unit Variable

Cost

Unit Contribution

Margin

Arks

$120

$80

$40

Bins

80

60

20

87. Carter Co.’s variable cost of E was

a.

$140

b.

$70

c.

$64

d.

$60

88. Costs that vary in total in direct proportion to changes in an activity level are called ______ costs.

a.

fixed

b.

sunk

c.

variable

Name:

Class:

Date:

chapter 6

d.

differential

Carter Co. sells two products: Arks and Bins. Last year, Carter sold 14,000 units of Arks and 56,000 units of Bins. Related

data are as follows:

Product

Unit Selling

Price

Unit Variable

Cost

Unit Contribution

Margin

Arks

$120

$80

$40

Bins

80

60

20

89. Assuming that last year’s fixed costs totaled $960,000, Carter Co.’s break-even point in units was

a.

40,000 units

b.

12,000 units

c.

35,000 units

d.

28,000 units

90. If fixed costs are $750,000 and variable costs are 60% of sales, the break-even point in sales dollars is

a.

$1,250,000

b.

$450,000

c.

$1,875,000

d.

$300,000

91. Costs that remain constant in total dollar amount as the level of activity changes are called ________ costs.

a.

fixed

b.

mixed

c.

product

d.

variable

92. Connor Company has fixed costs of $400,000, the unit selling price is $25, and the unit variable costs are $15. The

break-even sales (units) if the variable costs are increased by $2 is

a.

50,000 units

b.

30,770 units

c.

40,000 units

d.

26,667 units

93. Contribution margin is

a.

the excess of sales revenue over variable cost

b.

another term for volume in cost-volume-profit analysis

c.

profit

d.

the same as sales revenue

94. In a cost-volume-profit chart, the

a.

total cost line begins at zero

b.

slope of the total cost line is dependent on the fixed cost per unit

c.

total cost line begins at the total fixed cost value on the vertical axis

Name:

Class:

Date:

chapter 6

d.

total cost line normally ends at the highest sales value

95. Jacob Inc. has fixed costs of $240,000, the unit selling price is $32, and the unit variable costs are $20. The old and

new break-even sales (units), respectively, if the unit selling price increases by $4 is

a.

7,500 units and 6,667 units

b.

20,000 units and 30,000 units

c.

20,000 units and 15,000 units

d.

12,000 units and 15,000 units

96. Kaden Company’s fixed costs are $46,800, the unit selling price is $42, and the unit variable costs are $24. The break-

even sales (units) is

a.

2,400 units

b.

1,950 units

c.

1,114 units

d.

2,600 units

97. Which of the following types of cost is shown in the cost data below?

Total Cost

Number of Units

$8,000

1

8,500

2

9,000

3

9,500

4

a.

mixed cost

b.

variable cost

c.

fixed cost

d.

period cost

98. If sales are $820,000, variable costs are 55% of sales, and operating income is $260,000, the contribution margin ratio

is

a.

45%

b.

55%

c.

62%

d.

32%

99. Manley Co. manufactures office furniture. During the most productive month of the year, 4,500 desks were

manufactured at a total cost of $86,625. In its slowest month, the company made 1,800 desks at a cost of $49,500. Using

the high-low method of cost estimation, total fixed costs

a.

are $61,875

b.

are $33,875

c.

are $24,750

d.

cannot be determined from the data given

Rusty Co. sells two products: X and Y. Last year, Rusty sold 5,000 units of X and 35,000 units of Y. Related data are as

follows:

Name:

Class:

Date:

chapter 6

Unit Selling

Unit Variable

Unit Contribution

Product

Price

Cost

Margin

X

$110

$70

$40

Y

70

50

20

100. For break-even analysis, the unit contribution margin of E was

a.

$60.00

b.

$20.00

c.

$40.00

d.

$22.50

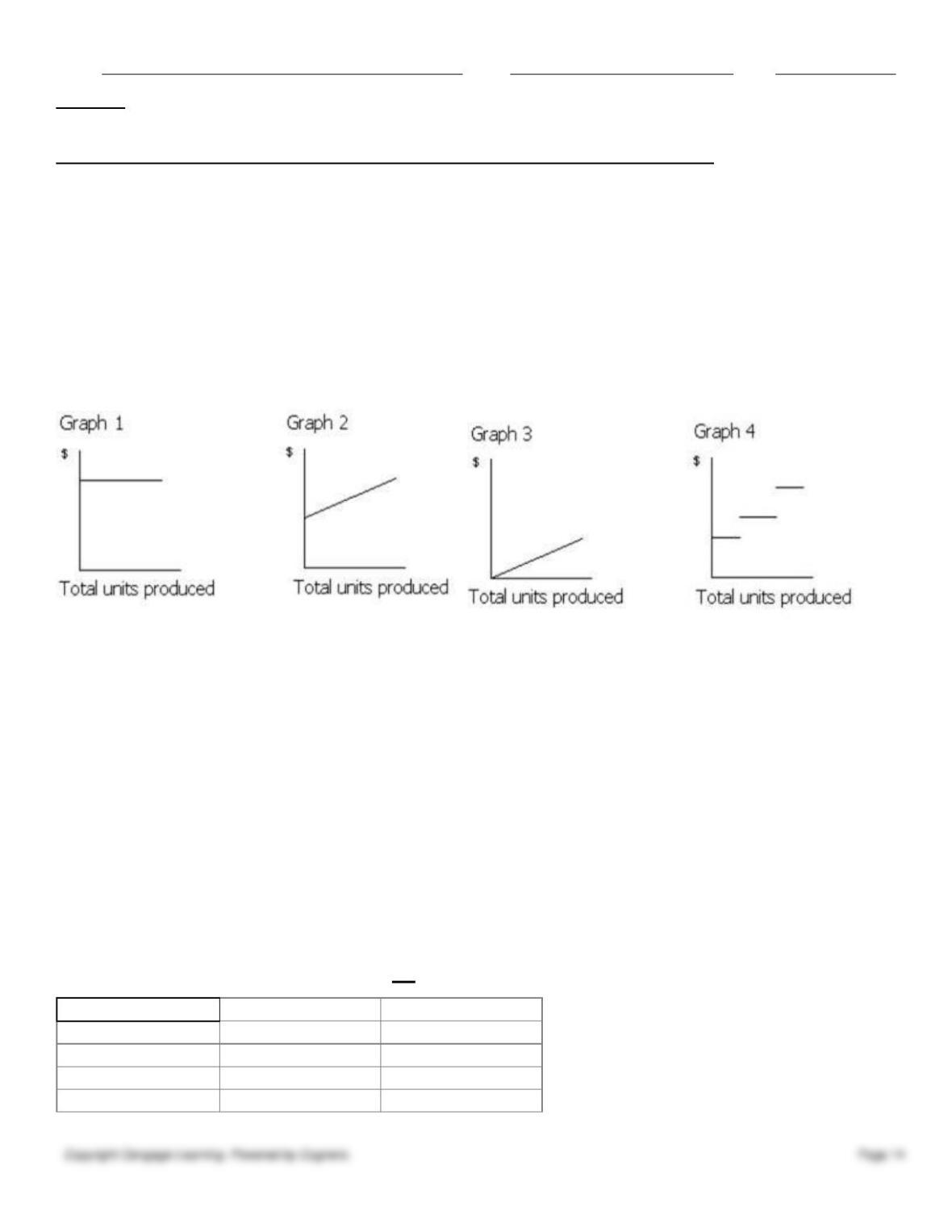

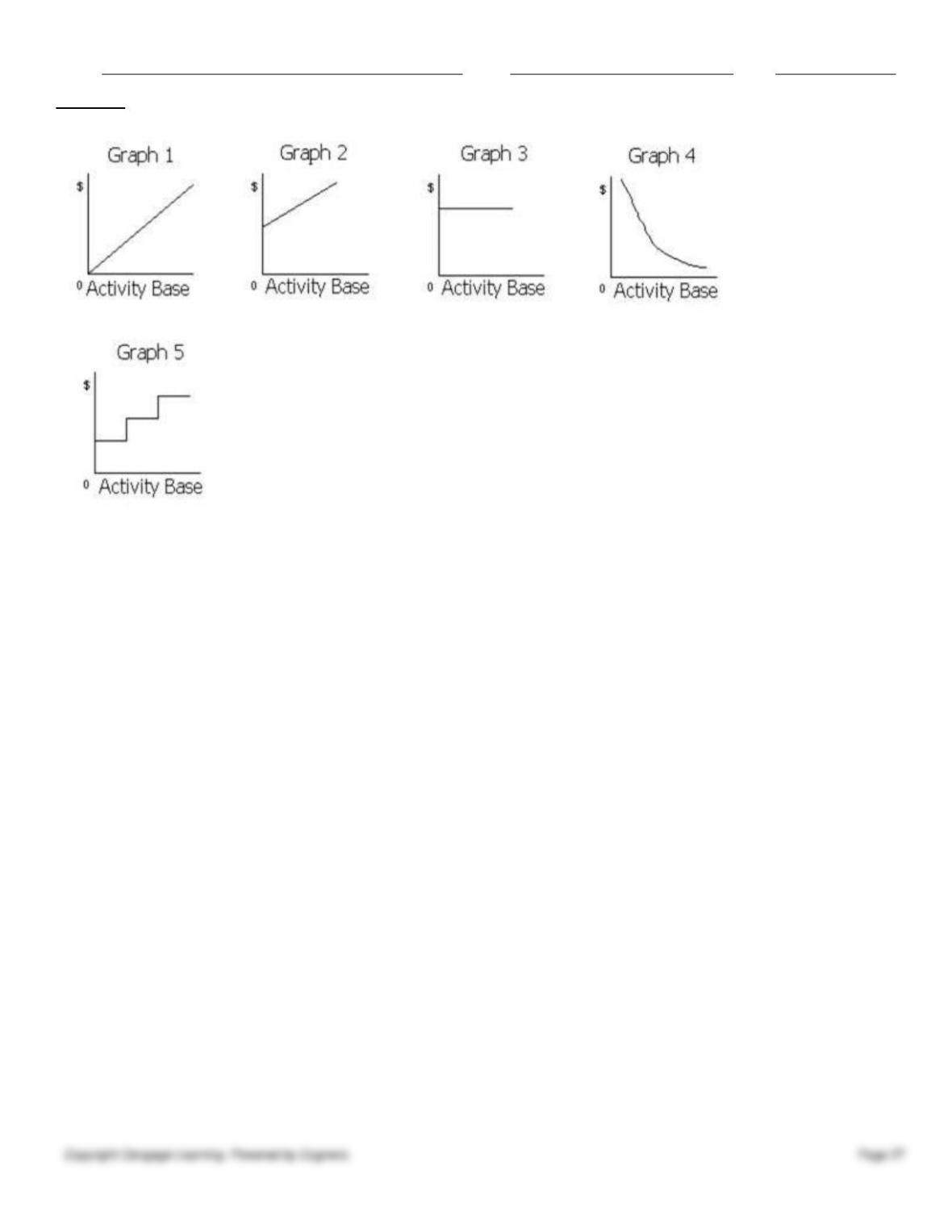

Figure 1

101. Which of the following graphs in Figure 1 illustrates the behavior of a total fixed cost?

a.

Graph 2

b.

Graph 3

c.

Graph 4

d.

Graph 1

102. When a business sells more than one product at varying selling prices, the business’s break-even point can be

determined as long as

a.

the number of products does not exceed two

b.

the number of products does not exceed three

c.

the number of products does not exceed fifteen

d.

there is no limit

103. Given the following cost and activity observations for Smithson Company’s utilities, use the high-low method to

determine Smithson’s fixed costs per month. Do not round your intermediate calculations.

Cost

Machine Hours

January

$52,200

20,000

February

75,000

29,000

March

57,000

22,000

April

64,000

24,500

a.

$1,533

Name:

Class:

Date:

chapter 6

a.

38.0%

b.

$2,530

c.

$22,800

d.

$50,600

104. If a business had sales of $4,000,000 and a margin of safety of 25%, the break-even point was

a.

$5,000,000

b.

$3,000,000

c.

$12,000,000

d.

$1,000,000

105. As production increases, the fixed cost per unit

a.

increases

b.

decreases

c.

remains the same

d.

either increases or decreases, depending on the variable costs

106. Spice Inc.’s unit selling price is $60, the unit variable costs are $35, fixed costs are $125,000, and current sales are

10,000 units. How much will operating income change if sales increase by 8,000 units?

a.

$150,000 decrease

b.

$175,000 increase

c.

$200,000 increase

d.

$150,000 increase

107. Which of the following is an example of a cost that varies in total as the number of units produced changes?

a.

salary of a production supervisor

b.

direct materials cost

c.

property taxes on factory buildings

d.

straight-line depreciation on factory equipment

108. Which of the following conditions would cause the break-even point to increase?

a.

total fixed costs increase

b.

unit selling price increases

c.

unit variable cost decreases

d.

total fixed costs decrease

109. Harley Company has sales of $500,000, variable costs are 75% of sales, and operating income is $40,000. Harley’s

operating leverage is

a.

0.0

b.

1.2

c.

1.3

d.

3.1

110. If sales are $425,000, variable costs are 62% of sales, and operating income is $50,000, the contribution margin ratio

is

Name:

Class:

Date:

chapter 6

b.

26.8%

c.

11.8%

d.

62.0%

111. Piper Technology’s fixed costs are $1,500,000, the unit selling price is $250, and the unit variable costs are $130. The

amount of sales required to realize an operating income of $200,000 is

a.

14,167 units

b.

12,500 units

c.

16,000 units

d.

11,538 units

112. When Isaiah Company has fixed costs of $120,000 and the contribution margin is $30, the break-even point is

a.

16,000 units

b.

8,000 units

c.

6,000 units

d.

4,000 units

113. A firm operated at 80% of capacity for the past year, during which fixed costs were $330,000, variable costs were

70% of sales, and sales were $1,000,000. Operating income (loss) was

a.

$140,000

b.

$(30,000)

c.

$370,000

d.

$670,000

114. Xander Studios holds a sculpting class for which it charges students $250. The costs consist of the following:

Variable costs per student:

Sculpting supplies

$ 100

Enrollment costs

50

Fixed costs for the course:

Instructor’s salary

$1,000

Rental cost of the classroom

500

The break-even number of students is

a.

2

b.

11

c.

12

d.

20

115. O’Boyle Co.’s fixed costs are $256,000, the unit selling price is $36, and the unit variable costs are $20, the break-

even sales (units) is

a.

12,800 units

b.

4,571 units

c.

16,000 units

d.

7,111 units

Name:

Class:

Date:

chapter 6

116. Which of the following activity bases would be the most appropriate for food costs of a hospital?

a.

number of nurses scheduled to work

b.

how many MRIs are taken

c.

number of patients who stay in the hospital

d.

quantity of prescriptions filled

117. The point where the sales line and the total costs line intersect on the cost-volume-profit chart represents the

a.

maximum possible operating loss

b.

maximum possible operating income

c.

total fixed costs

d.

break-even point

118. The relative distribution of sales among the various products sold by a business is the

a.

business’s basket of goods

b.

contribution margin mix

c.

sales mix

d.

product portfolio

Rusty Co. sells two products: X and Y. Last year, Rusty sold 5,000 units of X and 35,000 units of Y. Related data are as

follows:

Unit Selling

Unit Variable

Unit Contribution

Product

Price

Cost

Margin

X

$110

$70

$40

Y

70

50

20

119. Assuming that last year’s fixed costs totaled $675,000, Rusty Co.’s break-even point in units was

a.

16,875 units

b.

30,100 units

c.

30,000 units

d.

11,250 units

120. A cost that has characteristics of both a variable cost and a fixed cost is called a

a.

variable/fixed cost

b.

mixed cost

c.

discretionary cost

d.

sunk cost

121. The three most common cost behavior classifications are

a.

variable costs, product costs, and sunk costs

b.

fixed costs, variable costs, and mixed costs

c.

variable costs, period costs, and differential costs

d.

variable costs, sunk costs, and opportunity costs

122. The systematic examination of the relationships among selling prices, volume of sales and production, costs, and

Name:

Class:

Date:

chapter 6

profits is termed _____ analysis.

a.

contribution margin

b.

cost-volume-profit

c.

budgetary

d.

gross profit

123. Cost behavior refers to the manner in which a cost

a.

changes as the related activity changes

b.

is allocated to products

c.

is used in setting selling prices

d.

is estimated

124. If the contribution margin ratio for France Company is 45%, sales are $425,000, and fixed costs are $100,000, the

operating income is

a.

$233,750

b.

$91,250

c.

$191,250

d.

$133,750

125. Assume that Corn Co. sold 8,000 units of Product A and 2,000 units of Product B during the past year. The unit

contribution margins for Products A and B are $30 and $60, respectively. Corn has fixed costs of $378,000. The break-

even point in units is

a.

8,000 units

b.

6,300 units

c.

12,600 units

d.

10,500 units

126. Which of the following conditions would cause the break-even point to increase?

a.

total fixed costs decrease

b.

unit selling price increases

c.

unit variable cost decreases

d.

unit variable cost increases

127. Cost-volume-profit analysis cannot be used if which of the following occurs?

a.

Costs cannot be properly classified into fixed and variable costs.

b.

The total fixed costs change.

c.

The per-unit variable costs change.

d.

Per-unit sales prices change.

128. A firm operated at 90% of capacity for the past year, during which fixed costs were $420,000, variable costs were

40% of sales, and sales were $1,000,000. Operating income was

a.

$180,000

b.

$420,000

c.

$1,080,000

d.

$980,000

Name:

Class:

Date:

chapter 6

129. Charlotte Co. has budgeted salary increases to factory supervisors totaling 9%. If selling prices and all other cost

relationships are held constant, next year’s break-even point

a.

will decrease by 9%

b.

will increase by 9%

c.

cannot be determined from the data given

d.

will increase at a rate greater than 9%

130. The contribution margin ratio is the

a.

same as the variable cost ratio

b.

same as profit

c.

portion of equity contributed by the stockholders

d.

same as the profit-volume ratio

131. As production increases, variable costs per unit

a.

stay the same

b.

increase

c.

decrease

d.

either increase or decrease, depending on the fixed costs

132. The manufacturing costs of Calico Industries for three months of the year are provided below.

Total Cost

Production

(units)

April

$120,000

280,000

May

74,000

165,000

June

90,900

230,000

Using the high-low method, the variable cost per unit and the total fixed costs are

a.

$0.78 per unit and $4,000

b.

$0.40 per unit and $8,000

c.

$4.00 per unit and $800

d.

$7.80 per unit and $4,000

133. If fixed costs are $450,000, the unit selling price is $75, and the unit variable costs are $50, the old and new break-

even sales (units), respectively, if the unit selling price increases by $10 are

a.

6,000 units and 5,294 units

b.

18,000 units and 6,000 units

c.

18,000 units and 12,857 units

d.

9,000 units and 15,000 units

134. Kaiser Air is considering a new flight between Atlanta and Tampa. The average fare per seat is $400. The fixed costs

for the flight, which include crew salaries, operating costs, and aircraft depreciation, total $32,000. Variable costs per

passenger total $75. The break-even number of passengers per flight is

a.

5

b.

80

Name:

Class:

Date:

chapter 6

c.

98

d.

427

135. With the aid of computer software, managers can vary assumptions regarding selling prices, costs, and volume, and

can immediately see the effects of each change on the break-even point and profit. This is called

a.

“what if” or sensitivity analysis

b.

vary the data analysis

c.

computer-aided analysis

d.

data gathering

136. Which of the following is not an example of a cost that varies in total as the number of units produced changes?

a.

electricity per KWH to operate factory equipment

b.

direct materials cost

c.

insurance premiums on factory building

d.

wages of assembly worker

137. Which of the following describes the behavior of a variable cost per unit?

a.

It varies in increasing proportion with changes in the activity level.

b.

It varies in decreasing proportion with changes in the activity level.

c.

It remains constant with changes in the activity level.

d.

It varies in direct proportion with the activity level.

138. If fixed costs are $300,000, the unit selling price is $31, and the unit variable costs are $22, the break-even sales

(units) if fixed costs are reduced by $30,000 is

a.

30,000 units

b.

8,710 units

c.

12,273 units

d.

20,000 units

139. If fixed costs are $561,000 and the unit contribution margin is $8.00, the break-even point in units if variable costs

are decreased by $0.50 per unit is

a.

66,000 units

b.

70,125 units

c.

74,800 units

d.

60,000 units

140. Which of the following is an example of a mixed cost?

a.

salary of a factory supervisor

b.

electricity costs of $3 per kilowatt-hour

c.

rental costs of $10,000 per month plus $0.30 per machine hour of use

d.

straight-line depreciation on factory equipment

141. Which of the following costs is an example of a cost that remains the same in total as the number of units produced

changes?

a.

direct labor

Name:

Class:

Date:

chapter 6

b.

salary of a factory supervisor

c.

units-of-production depreciation on factory equipment

d.

direct materials

142. If fixed costs are $600,000 and the unit contribution margin is $40, the break-even point if fixed costs are increased

by $90,000 is

a.

17,250 units

b.

15,000 units

c.

8,333 units

d.

9,667 units

Figure 1

143. Which of the following graphs in Figure 1 illustrates the behavior of a total variable cost?

a.

Graph 2

b.

Graph 3

c.

Graph 4

d.

Graph 1

144. Reynold’s Company has a product with fixed costs of $350,000, a unit selling price of $29, and unit variable costs of

$20. The break-even sales (units) if the variable costs are decreased by $4 is

a.

26,923 units

b.

12,069 units

c.

21,875 units

d.

38,889 units

145. If fixed costs are $850,000 and variable costs are 60% of sales, the break-even point (dollars) is

a.

$2,125,000

b.

$340,000

c.

$3,400,000

d.

$1,416,666

146. For purposes of analysis, mixed costs are

a.

classified as fixed costs

Name:

Class:

Date:

chapter 6

b.

classified as variable costs

c.

classified as period costs

d.

separated into their variable and fixed cost components

147. Which of the following activity bases would be the most appropriate for gasoline costs of a delivery service?

a.

number of truck drivers

b.

total miles driven

c.

number of trucks in service

d.

number of packages picked up

148. In cost-volume-profit analysis, all costs are classified into which of the following two categories?

a.

mixed costs and variable costs

b.

sunk costs and fixed costs

c.

discretionary costs and sunk costs

d.

variable costs and fixed costs

Carter Co. sells two products: Arks and Bins. Last year, Carter sold 14,000 units of Arks and 56,000 units of Bins. Related

data are as follows:

Product

Unit Selling

Price

Unit Variable

Cost

Unit Contribution

Margin

Arks

$120

$80

$40

Bins

80

60

20

149. Carter Co.’s unit selling price of E, with E representing one overall “enterprise” product, was

a.

$200

b.

$100

c.

$80

d.

$88

150. Strait Co. manufactures office furniture. During the most productive month of the year, 3,000 desks were

manufactured at a total cost of $59,000. In the month of lowest production, the company made 1,125 desks at a cost of

$38,000. Using the high-low method of cost estimation, total fixed costs are

a.

$21,000

b.

$25,400

c.

$42,000

d.

$13,000

151. If variable costs per unit increased because of an increase in hourly wage rates, the break-even point would

a.

decrease

b.

increase

c.

remain the same

d.

increase or decrease, depending on the percentage increase in wage rates

152. Zipee Inc.’s unit selling price is $90, the unit variable costs are $40.50, fixed costs are $170,000, and current sales are

12,000 units. How much will operating income change if sales increase by 5,000 units?

Name:

Class:

Date:

chapter 6

a.

$125,000 decrease

b.

$175,000 increase

c.

$75,000 increase

d.

$247,500 increase

153. If variable costs per unit decreased because of a decrease in utility rates, the break-even point would

a.

decrease

b.

increase

c.

remain the same

d.

increase or decrease, depending on the percentage increase in utility rates

154. Which of the following types of cost is shown in the cost data below?

Cost per Unit

Number of Units

$6,000

1

3,000

2

2,000

3

1,500

4

a.

mixed cost

b.

variable cost

c.

fixed cost

d.

period cost

155. Which of the following ratios indicates the percentage of each sales dollar that is available to cover fixed costs and to

provide a profit?

a.

margin of safety ratio

b.

contribution margin ratio

c.

costs and expenses ratio

d.

profit ratio

156. Understanding how costs behave is useful to management for all of the following reasons except

a.

predicting customer demand

b.

predicting profits as sales and production volumes change

c.

estimating costs

d.

changing an existing product production

Figure 1

Name:

Class:

Date:

chapter 6

157. Which of the following graphs in Figure 1 illustrates the nature of a mixed cost?

a.

Graph 2

b.

Graph 3

c.

Graph 4

d.

Graph 1

Rusty Co. sells two products: X and Y. Last year, Rusty sold 5,000 units of X and 35,000 units of Y. Related data are as

follows:

Unit Selling

Unit Variable

Unit Contribution

Product

Price

Cost

Margin

X

$110

$70

$40

Y

70

50

20

158. For break-even analysis, the unit selling price of E was

a.

$180

b.

$75

c.

$100

d.

$110

159. Flying Cloud Co. has the following operating data for its manufacturing operations:

Unit selling price

$ 250

Unit variable cost

100

Total fixed costs

840,000

The company has decided to increase the wages of hourly workers which will increase the unit variable cost by 10%.

Increases in the salaries of factory supervisors and property taxes for the factory will increase fixed costs by 4%. If sales

prices are held constant, the next break-even point for Flying Cloud Co. will be

a.

increased by 640 units

b.

increased by 400 units

c.

decreased by 640 units

d.

increased by 800 units

160. Most operating decisions of management focus on a narrow range of activity called the ______ of production.

a.

relevant range

Name:

Class:

Date:

chapter 6

b.

strategic level

c.

optimal level

d.

tactical operating level

161. Which of the following is not an assumption underlying cost-volume-profit analysis?

a.

The break-even point will be passed during the period.

b.

Total sales and total costs can be represented by straight lines.

c.

Costs can be accurately divided into fixed and variable components.

d.

The sales mix is constant.

162. Bryce Co. sales are $914,000, variable costs are $498,130, and operating income is $196,000. The contribution

margin ratio is

a.

52.2%

b.

28.4%

c.

54.5%

d.

45.5%

163. If fixed costs are $1,200,000, the unit selling price is $240, and the unit variable costs are $110, the amount of sales

(units) required to realize an operating income of $200,000 is

a.

9,231 units

b.

12,000 units

c.

10,769 units

d.

5,833 units

Rusty Co. sells two products: X and Y. Last year, Rusty sold 5,000 units of X and 35,000 units of Y. Related data are as

follows:

Unit Selling

Unit Variable

Unit Contribution

Product

Price

Cost

Margin

X

$110

$70

$40

Y

70

50

20

164. Rusty Co.’s sales mix last year was

a.

58% X; 42% Y

b.

60% X; 40% Y

c.

30% X; 70% Y

d.

12.5% X; 87.5% Y

165. Given the following cost and activity observations for George Company’s utilities, use the high-low method to

determine George’s variable utilities cost per machine hour.

Cost

Machine Hours

May

$16,500

105,000

June

18,000

120,000

July

16,000

100,000

Name:

Class:

Date:

chapter 6

August

17,500

117,000

a.

$100.00

b.

$1.00

c.

$10.00

d.

$0.10

166. Forde Co. has an operating leverage of 4. Sales are expected to increase by 12% next year. Operating income is

a.

unaffected

b.

expected to increase by 3%

c.

expected to increase by 48%

d.

expected to increase by 4%

167. Which of the following is not an example of a cost that varies in total as the number of units produced changes?

a.

electricity per KWH to operate factory equipment

b.

direct materials cost

c.

straight-line depreciation on factory equipment

d.

wages of assembly worker

Match each of the following descriptions with the appropriate term (a–e).

a.

Profit-volume chart

b.

Cost-volume-profit chart

c.

Sales mix

d.

Operating leverage

e.

Margin of safety

168. Indicates the possible decrease in sales that may occur before operating loss results

169. Contribution margin divided by operating income

170. Graphically shows costs, sales, and operating profit or loss at various levels of units sold

171. Plots only the difference between total sales and total costs

172. The relative distribution of sales among products sold by a company

Match each of the following costs with the graph (a–e) that best portrays its cost behavior as the number of units

produced and sold increases.

Name:

Class:

Date:

chapter 6

a.

Graph 1

b.

Graph 2

c.

Graph 3

d.

Graph 4

e.

Graph 5

173. Sales commissions of $6,000 plus $0.05 for each item sold

174. Rent on warehouse of $12,000 per month

175. Insurance costs of $2,500 per month

176. Per-unit cost of direct labor

177. Total salaries of quality control supervisors (One supervisor must be added for each additional work shift.)

178. Total employer pension costs of $0.35 per direct labor hour

179. Per-unit straight-line depreciation costs

180. Per-unit cost of direct materials

181. Total direct materials cost

182. Electricity costs of $5,000 per month plus $0.0004 per kilowatt-hour

183. Per-unit cost of plant superintendent’s salary

184. Salary of the night-time security guard of $3,800 per month

Name:

Class:

Date:

chapter 6

185. Repairs and maintenance costs of $3,000 for each 2,000 hours of factory machine usage

186. Total direct labor cost

187. Straight-line depreciation on factory equipment

Match each of the following descriptions with the appropriate term (a–e).

a.

Relevant range

b.

Break-even point

c.

Contribution margin

d.

Fixed costs

e.

Variable costs

188. Vary(ies) in proportion to changes in activity levels

189. Remain(s) the same in total dollar amount as the level of activity changes

190. The point at which a business’s revenues exactly equal costs

191. A specific activity range over which the cost changes are of interest

192. The excess of sales revenues over variable costs

Match each of the following costs of producing T-shirts with the appropriate classification (a–c).

a.

Variable cost

b.

Fixed cost

c.

Mixed cost

193. Ink used for screen printing

194. Warehouse rent of $8,000 per month plus $0.50 per square foot of storage used

195. Thread

196. Electricity costs of $0.038 per kilowatt-hour

197. Janitorial costs of $4,000 per month

198. Advertising costs of $12,000 per month

199. Accounting salaries

200. Color dyes for producing different colors of T-shirts

201. Salary of the production supervisor

202. Straight-line depreciation on sewing machines

203. Salaries of internal pattern designers

Name:

Class:

Date:

chapter 6

204. Hourly wages of sewing machine operators

205. Property taxes on factory, building, and equipment

206. Cotton and polyester cloth

207. Maintenance costs with sewing machine company (The cost is $2,000 per year plus $0.001 for each machine hour of

use.)

208. Waterfall Company sells a product for $150 per unit. The variable cost is $80 per unit, and fixed costs are $270,000.

Determine the (a) break-even point in sales units and (b) break-even point in sales units if the company desires a target

profit of $36,000. Round your answer to the nearest whole number.

209. Steven Company has fixed costs of $160,000. The unit selling price, variable cost per unit, and contribution margin

per unit for the company’s two products are provided below.

Product

Selling Price per Unit

Variable Cost per Unit

Contribution Margin

per Unit

X

$180

$80

$100

Y

100

50

50

The sales mix for Products X and Y is 60% and 40%, respectively. Determine the break-even point in units of X and Y.

210. Dean Company has sales of $500,000, and the break-even point in sales dollars is $300,000. Determine the

company’s margin of safety percentage.

211. Penny Company sells 25,000 units at $59 per unit. Variable costs are $29 per unit, and operating loss is $(50,000).

Determine the (a) unit contribution margin, (b) contribution margin ratio, and (c) fixed costs per unit at production of

25,000 units.

212. Bluegill Company sells 45,000 units at $18 per unit. Fixed costs are $62,000, and operating income is $298,000.

Determine the (a) variable cost per unit, (b) unit contribution margin, and (c) contribution margin ratio.

213. Racer Industries has fixed costs of $900,000. The selling price per unit is $250, and the variable cost per unit is $130.

a. How many units must Racer sell in order to break even?

b. How many units must Racer sell in order to earn a profit of $480,000?

c. A new employee suggests that Racer Industries sponsor a 10K marathon as a form of advertising. The cost to

sponsor the event is $7,200. How many more units must be sold to cover this cost?

214. Safari Co. sells two products: Orks and Zins. Last year, Safari sold 21,000 units of Orks and 14,000 units of Zins.

Related data are as follows:

Product

Unit Selling

Price

Unit Variable

Cost

Unit Contribution

Margin

Orks

$120

$80

$40

Zins

80

60

20

Determine the following:

a. Safari Co.’s sales mix

Name:

Class:

Date:

chapter 6

b. Safari Co.’s unit selling price of E

c. Safari Co.’s unit contribution margin of E

d. Safari Co.’s break-even sales in units of E assuming that last year’s fixed costs were $160,000

215. If a business had a capacity of $10,000,000 of sales, actual sales of $6,000,000, break-even sales of $4,200,000, fixed

costs of $1,800,000, and variable costs of 60% of sales, what is the margin of safety expressed as a percentage of sales?

216. Gladstorm Enterprises sells a product for $60 per unit. The variable cost is $20 per unit, while fixed costs are

$85,000. Determine the (a) break-even point in sales units and (b) break-even point in sales units if the selling price

increased to $80 per unit. Round your answer to the nearest whole number.

217. Bobby Company has fixed costs of $160,000. The unit selling price, variable cost per unit, and contribution margin

per unit for the company’s two products are provided below.

Product

Selling Price per Unit

Variable Cost per Unit

Contribution Margin

per Unit

X

$180

$100

$80

Y

100

60

40

The sales mix for Products X and Y is 60% and 40%, respectively. Determine the break-even point in units of X and Y.

218. Trail Bikes, Inc. sells three Deluxe bikes for every seven Standard bikes. The Deluxe bike sells for $1,800 and has

variable costs of $1,200. The Standard bike sells for $600 and has variable costs of $200.

a. If Trail Bikes has fixed costs that total $1,702,000, how many bikes must be sold in order for the company to break

even?

b. How many of the bikes determined in (a) will be Deluxe bikes, and how many will be the Standard bikes?

219. Grant Company has sales of $300,000, and the break-even point in sales dollars is $225,000. Determine the

company’s margin of safety percentage.

220. Mia Enterprises sells a product for $90 per unit. The variable cost is $40 per unit, while fixed costs are $75,000.

Determine the (a) break-even point in sales units and (b) break-even point in sales units if the selling price increased to

$100 per unit.

221. For the current year ending April 30, Hal Company expects fixed costs of $60,000, a unit variable cost of $70, and an

anticipated break-even point of 1,715 sales units.

a.

Compute the unit sales price.

b.

Compute the sales (units) required to realize an operating profit of $8,000.

Round your answer to the nearest whole number.

222. Global Publishers has collected the following data for recent months:

Month Issues Published Total Cost

March 20,500 $20,960

April 21,800 22,464

May 17,750 18,495

June 21,200 21,395

a. Using the high-low method, find variable cost per unit, total fixed costs, and the total cost equation.

b. What is the estimated cost for a month in which 19,000 issues are published?

Name:

Class:

Date:

chapter 6

223. Given the following information:

Variable cost per unit = $5

July fixed cost per unit = $7

Units sold and produced in July = 28,000

What is the total estimated cost for August if 30,000 units are projected to be produced and sold?

224. Silver River Company sells Products S and T and has made the following estimates for the coming year:

Product

Unit Selling Price

Unit Variable Cost

Sales Mix

S

$30

$24

60%

T

70

56

40

Fixed costs are estimated at $202,400. For the purposes of break-even analysis, determine the following:

a. Break-even sales (units) for E

b. Break-even sales (units) of S and T

c. Sales units of E necessary to realize an operating income of $119,600 for the coming year

225. Tom Company reports the following data:

Sales

$600,000

Variable costs

400,000

Fixed costs

100,000

Determine Tom Company’s operating leverage.

226. A business had a margin of safety ratio of 20%, variable costs of 75% of sales, fixed costs of $240,000, a break-even

point of $960,000, and operating income of $60,000 for the current year. Compute the current year’s sales.

227. Louis Company sells a single product at a price of $65 per unit. Variable costs per unit are $45, and total fixed costs

are $625,500. Louis is considering the purchase of a new piece of equipment that would increase the fixed costs to

$800,000 but decrease the variable costs per unit to $42.

If Louis Company expects to sell 44,000 units next year, should it purchase this new equipment?

228. Douglas Company has a contribution margin ratio of 30%. If Douglas has $336,420 in fixed costs, what amount of

sales will need to be generated in order for the company to break even?

229. A company with a break-even point at $900,000 in sales revenue had fixed costs of $225,000. When actual sales

were $1,000,000, variable costs were $750,000. Determine (a) the margin of safety expressed in dollars, (b) the margin of

safety expressed as a percentage of sales, (c) the contribution margin ratio, and (d) the operating income.

230. For the current year ending January 31, Harp Company expects fixed costs of $188,500 and a unit variable cost of

$51.50. For the coming year, a new wage contract will increase the unit variable cost to $55.50. The selling price of

$70.00 per unit is expected to remain the same.

a.

Compute the break-even sales (units) for the current year. Round your answer to the nearest

whole number.

b.

Compute the anticipated break-even sales (units) for the coming year, assuming the new

wage contract is signed.

231. The manufacturing costs of Mocha Industries for three months of the year are as follows:

Total Cost

Production

Name:

Class:

Date:

chapter 6

April

$ 63,100

1,100 units

May

80,920

1,800

June

100,900

2,600

Using the high-low method, determine the (a) variable cost per unit, and (b) the total fixed costs.

232. Carrolton, Inc., currently sells widgets for $80 per unit. The variable cost is $30 per unit, and total fixed costs equal

$240,000 per year. Sales are currently 20,000 units annually.

The company is considering a 20% drop in selling price that it believes will raise units sold by 20%. Assuming all costs

stay the same, what is the impact on income if this change is made?

233. Klein Company reports the following data:

Sales

$980,000

Variable costs

500,000

Fixed costs

350,000

Determine Klein Company’s operating leverage. Round your answer to two decimal places.

234. Blane Company has the following data:

Total sales

$800,000

Total variable costs

$300,000

Fixed costs

$200,000

Units sold

50,000 units

What will operating income be if units sold double to 100,000 units?

235. Define operating leverage. Explain the relationship between a company’s operating leverage and how a change in

sales is expected to impact profits.

236. Currently, the unit selling price is $50, the variable cost is $34, and the total fixed costs are $108,000. A proposal is

being evaluated to increase the selling price to $54.

a. Compute the current break-even sales (units).

b. Compute the anticipated break-even sales (units), assuming that the unit selling price is

increased and all costs remain constant.

237. The manufacturing costs of Carrie Industries for the first three months of the year are provided below.

Total Cost

Production

January

$ 93,300

2,300 units

February

115,500

3,100

March

79,500

1,900

Using the high-low method, determine the (a) variable cost per unit, and (b) the total fixed cost.

238. a. If Swannanoa Company’s budgeted sales are $1,000,000, fixed costs are $350,000, and variable costs are

$600,000, what is the budgeted contribution margin ratio?

b. If the contribution margin ratio is 30%, sales are $900,000, and fixed costs are $200,000, what is the operating income?

239. A company has a margin of safety of 25%, a contribution margin ratio of 30%, and sales of $1,000,000.

Name:

Class:

Date:

chapter 6

Fixed costs = $200,000

a.

What is the break-even point in sales dollars?

b.

What is the operating income?

c.

If neither the relationship between variable costs and sales nor the amount of fixed costs is

expected to change in the next year, how much additional operating income can be earned

by increasing sales by $110,000?

240. For the coming year, River Company estimates fixed costs at $109,000, the unit variable cost at $21, and the unit

selling price at $85. Determine (a) the break-even point in units of sales, (b) the unit sales required to realize operating

income of $150,000, and (c) the probable operating income if sales total $500,000.

Round units to the nearest whole number and percentage to one decimal place.

241. For the past year, Pedi Company had fixed costs of $70,000, unit variable costs of $32, and a unit selling price of

$40. For the coming year, no changes are expected in revenues and costs, except that property taxes are expected to

increase by $10,000. Determine the break-even sales (units) for (a) the past year and (b) the coming year.

242. Atlantic Company sells a product with a break-even point of 3,000 sales units. The variable cost is $60 per unit, and

fixed costs are $270,000.

Determine the (a) unit sales price and (b) break-even point in sales units if the company desires a target profit of $36,000.

243. For the past year, Iris Company had fixed costs of $6,708,000, a unit variable cost of $444, and a unit selling price of

$600. For the coming year, no changes are expected in revenues and costs, except that a new wage contract will increase

variable costs by $6 per unit. Determine the break-even sales (units) for (a) the past year and (b) the coming year.

244. Cordell, Inc., has an operating leverage of 3. Sales are expected to increase by 9% next year. What is the expected

change in operating income next year?

245. Perfect Stampers makes and sells aftermarket hub caps. The variable cost for each hub cap is $4.75, and the hub cap

sells for $9.95. Perfect Stampers has fixed costs per month of $3,120. Compute the contribution margin per unit and the

break-even sales in units and in dollars for the month.

246. Copper Hill Inc. manufactures laser printers within a relevant range of production of 70,000 to 100,000 printers per

year. The following partially completed manufacturing cost schedule has been prepared:

Number of Printers Produced

70,000

90,000

100,000

Total costs:

Total variable costs

$350,000

(d)

(j)

Total fixed costs

630,000

(e)

(k)

Total costs

$980,000

(f)

(l)

Cost per unit:

Variable cost per unit

(a)

(g)

(m)

Fixed cost per unit

(b)

(h)

(n)

Total cost per unit

(c)

(i)

(o)

Complete the preceding cost schedule, identifying each cost by the appropriate letter (a) through (o).

247. Given the following:

Variable cost as a percentage of sales = 60%

Unit variable cost = $30

Name:

Class:

Date:

chapter 6

What is the break-even point in units?

Name:

Class:

Date:

chapter 6

Answer Key

Name:

Class:

Date:

chapter 6

Name:

Class:

Date:

chapter 6

Name:

Class:

Date:

chapter 6

Name:

Class:

Date:

chapter 6

Name:

Class:

Date:

chapter 6

Name:

Class:

Date:

chapter 6

Name:

Class:

Date:

chapter 6

Name:

Class:

Date:

chapter 6

Name:

Class:

Date:

chapter 6

Name:

Class:

Date:

chapter 6

Name:

Class:

Date:

chapter 6

Name:

Class:

Date:

chapter 6