91. During 2011, Parent Corporation purchased at book value some of the

outstanding bonds of its subsidiary. How would this acquisition have been

reflected in the consolidated statement of cash flows?

92. On January 1, 2011, Parent Corporation acquired a controlling interest in

the voting common stock of Foxboro Co. At the same time, Parent purchased

sixty percent of Foxboro’s outstanding preferred stock. In preparing consolidated

financial statements, how should the acquisition of the preferred stock be

accounted for?

93. When a company has preferred stock in its capital structure, what amount

should be used to calculate non-controlling interest in the preferred stock of the

subsidiary when the company is acquired as a subsidiary of another company?

94. Parent Corporation acquired some of its subsidiary’s outstanding bonds.

Why might Parent purchase the bonds, rather than the subsidiary buying its own

bonds?

95. Parent Corporation had just purchased some of its subsidiary’s

outstanding bonds on the open market. What items related to these bonds will

have to be accounted for in the consolidation process?

96. Parent Corporation recently acquired some of its subsidiary’s outstanding

bonds, at an amount which required the recognition of a loss. In what ways could

the loss be allocated? Which allocation would you recommend? Why?

97. How does the existence of a non-controlling interest affect the preparation

of a consolidated statement of cash flows?

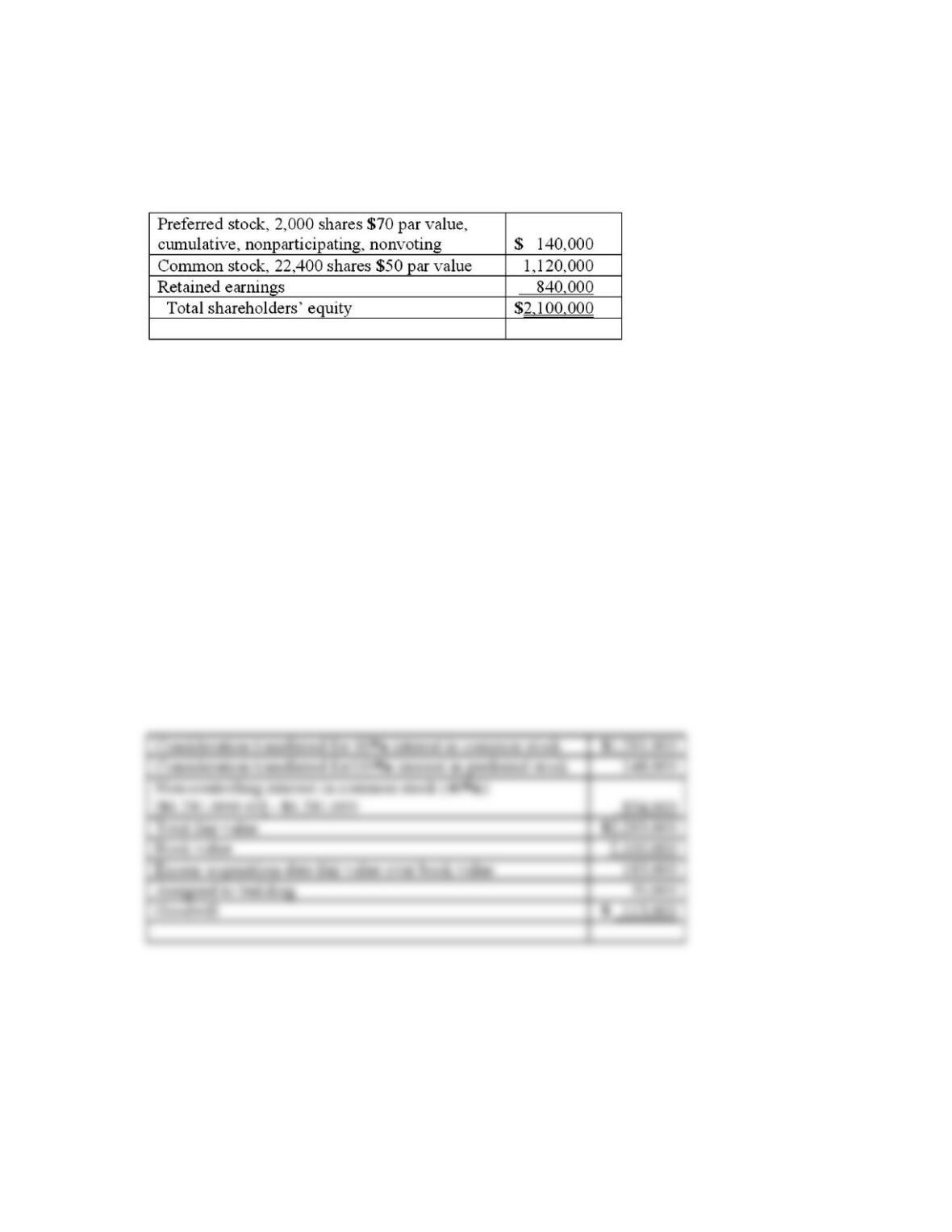

98. On January 1, 2011, Bast Co. had a net book value of $2,100,000 as

follows:

Fisher Co. acquired all of the outstanding preferred shares for $148,000 and 60%

of the common stock for $1,281,000. Fisher believed that one of Bast’s buildings,

with a twelve-year life, was undervalued on the company’s financial records by

$70,000.

Required:

What is the amount of goodwill to be recognized from this purchase?

99. Fargus Corporation owned 51% of the voting common stock of Sanatee,

Inc. The parent’s interest was acquired several years ago on the date that the

subsidiary was formed. Consequently, no goodwill or other allocation was

recorded in connection with the acquisition price.

On January 1, 2010, Sanatee sold $1,400,000 in ten-year bonds to the public at

108. The bonds pay a 10% interest rate every December 31. Fargus acquired 40%

of these bonds on January 1, 2012, for 95% of the face value. Both companies

utilized the straight-line method of amortization.

What balances would need to be considered in order to prepare the consolidation

entry in connection with these intra-entity bonds at December 31, 2012, the end

of the first year of the intra-entity investment? Prepare schedules to show

numerical answers for balances that would be needed for the entry.

100. Fargus Corporation owned 51% of the voting common stock of Sanatee,

Inc. The parent’s interest was acquired several years ago on the date that the

subsidiary was formed. Consequently, no goodwill or other allocation was

recorded in connection with the acquisition price.

On January 1, 2010, Sanatee sold $1,400,000 in ten-year bonds to the public at

108. The bonds pay a 10% interest rate every December 31. Fargus acquired 40%

of these bonds on January 1, 2012, for 95% of the face value. Both companies

utilized the straight-line method of amortization.

What consolidation entry would be recorded in connection with these intra-entity

bonds on December 31, 2012?

101. Fargus Corporation owned 51% of the voting common stock of Sanatee,

Inc. The parent’s interest was acquired several years ago on the date that the

subsidiary was formed. Consequently, no goodwill or other allocation was

recorded in connection with the acquisition price.

On January 1, 2010, Sanatee sold $1,400,000 in ten-year bonds to the public at

108. The bonds pay a 10% interest rate every December 31. Fargus acquired 40%

of these bonds on January 1, 2012, for 95% of the face value. Both companies

utilized the straight-line method of amortization.

What consolidation entry would be recorded in connection with these intra-entity

bonds on December 31, 2013?

102. Fargus Corporation owned 51% of the voting common stock of Sanatee,

Inc. The parent’s interest was acquired several years ago on the date that the

subsidiary was formed. Consequently, no goodwill or other allocation was

recorded in connection with the acquisition price.

On January 1, 2010, Sanatee sold $1,400,000 in ten-year bonds to the public at

108. The bonds pay a 10% interest rate every December 31. Fargus acquired 40%

of these bonds on January 1, 2012, for 95% of the face value. Both companies

utilized the straight-line method of amortization.

What consolidation entry would be recorded in connection with these intra-entity

bonds on December 31, 2014?

103. Skipen Corp. had the following stockholders’ equity accounts:

The preferred stock was participating and is therefore considered to be equity.

Vestin Corp. acquired 90% of this common stock for $2,250,000 and 70% of the

preferred stock for $1,120,000. All of the subsidiary’s assets and liabilities were

determined to have fair values equal to their book values except for land which is

undervalued by $130,000.

Required:

What amount was attributed to goodwill on the date of acquisition?

104. Thomas Inc. had the following stockholders’ equity accounts as of January

1, 2011:

Kuried Co. acquired all of the voting common stock of Thomas on January 1,

2011, for $20,656,000. The preferred stock remained in the hands of outside

parties and had a fair value of $3,060,000. A database valued at $656,000 was

recognized and amortized over five years.

During 2011, Thomas reported earning $630,000 in net income and paid $504,000

in total cash dividends. Kuried used the equity method to account for this

investment.

What is the amount of goodwill resulting from this acquisition?