23. If newly issued debt is issued from a parent to its subsidiary, which of the

following statements is

false

?

24. The accounting problems encountered in consolidated intra-entity debt

transactions when the debt is acquired by an affiliate from an outside party

include all of the following

except

:

25. Which of the following statements is true concerning the acquisition of

existing debt of a consolidated affiliate in the year of the debt acquisition?

26. Which of the following statements is

false

regarding the assignment of a

gain or loss on intercompany bond transfer?

27. What would differ between a statement of cash flows for a consolidated

company and an unconsolidated company using the indirect method?

28. Which of the following statements is true for a consolidated statement of

cash flows?

29. In reporting consolidated earnings per share when there is a wholly owned

subsidiary, which of the following statements is true?

30. A subsidiary issues new shares of common stock at an amount below

book value. Outsiders buy all of these shares. Which of the following statements

is true?

31. A subsidiary issues new shares of common stock. If the parent acquires all

of these shares at an amount greater than book value, which of the following

statements is true?

32. If a subsidiary reacquires its outstanding shares from outside ownership

for more than book value, which of the following statements is true?

33. If a subsidiary issues a stock dividend, which of the following statements

is true?

34. Stevens Company has had bonds payable of $10,000 outstanding for

several years. On January 1, 2011, when there was an unamortized discount of

$2,000 and a remaining life of 5 years, its 80% owned subsidiary, Matthews

Company, purchased the bonds in the open market for $11,000. The bonds pay

6% interest annually on December 31. The companies use the straight-line

method to amortize interest revenue and expense. Compute the consolidated

gain or loss on a consolidated income statement for 2011.

35. Keenan Company has had bonds payable of $20,000 outstanding for

several years. On January 1, 2011, there was an unamortized premium of $2,000

with a remaining life of 10 years, Keenan’s parent, Ross, Inc., purchased the

bonds in the open market for $19,000. Keenan is a 90% owned subsidiary of

Ross. The bonds pay 8% interest annually on December 31. The companies use

the straight-line method to amortize interest revenue and expense. Compute the

consolidated gain or loss on a consolidated income statement for 2011.

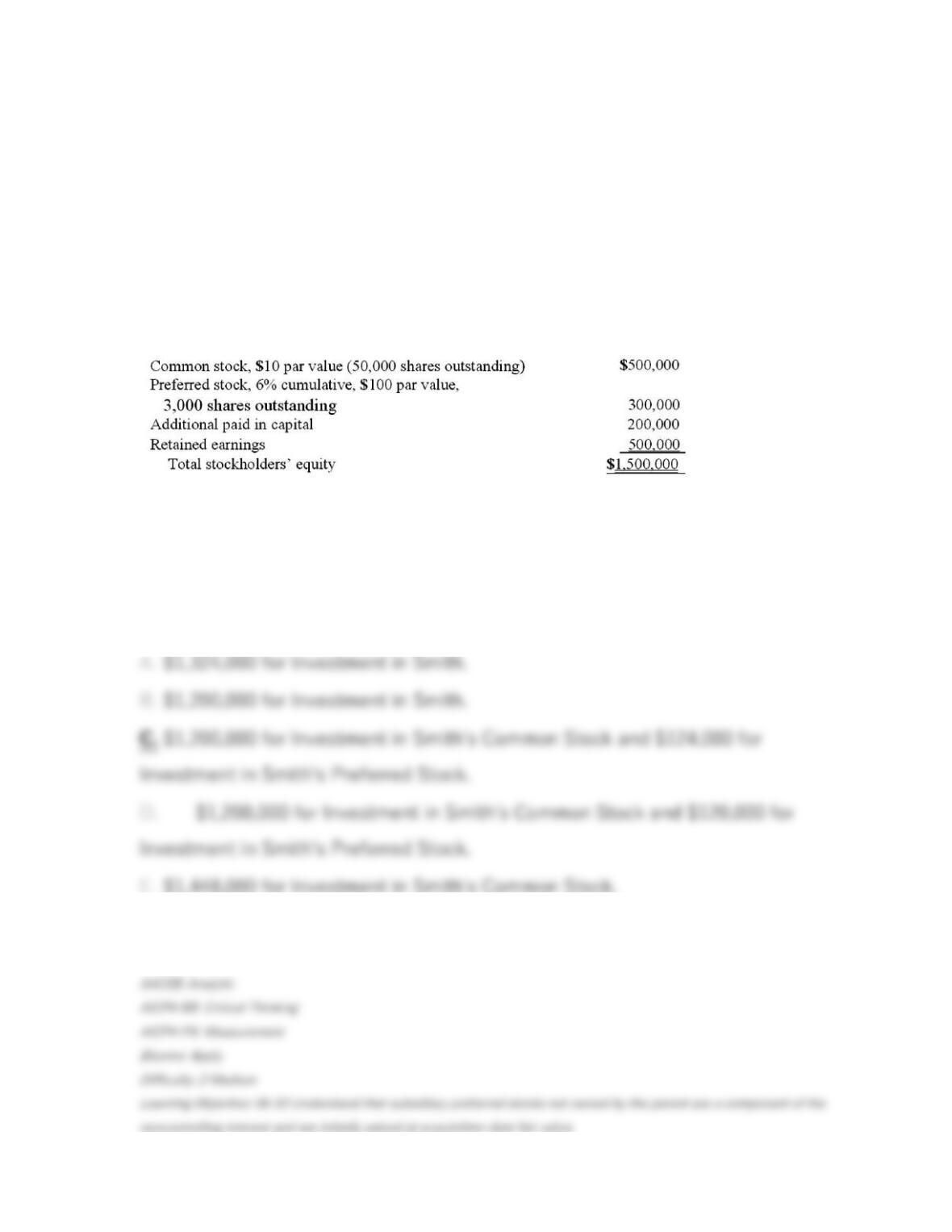

36. On January 1, 2009, Nichols Company acquired 80% of Smith Company’s

common stock and 40% of its non-voting, cumulative preferred stock. The

consideration transferred by Nichols was $1,200,000 for the common and

$124,000 for the preferred. Any excess acquisition-date fair value over book

value is considered goodwill. The capital structure of Smith immediately prior to

the acquisition is:

Determine the amount and account to be recorded for Nichols’ investment in

Smith.

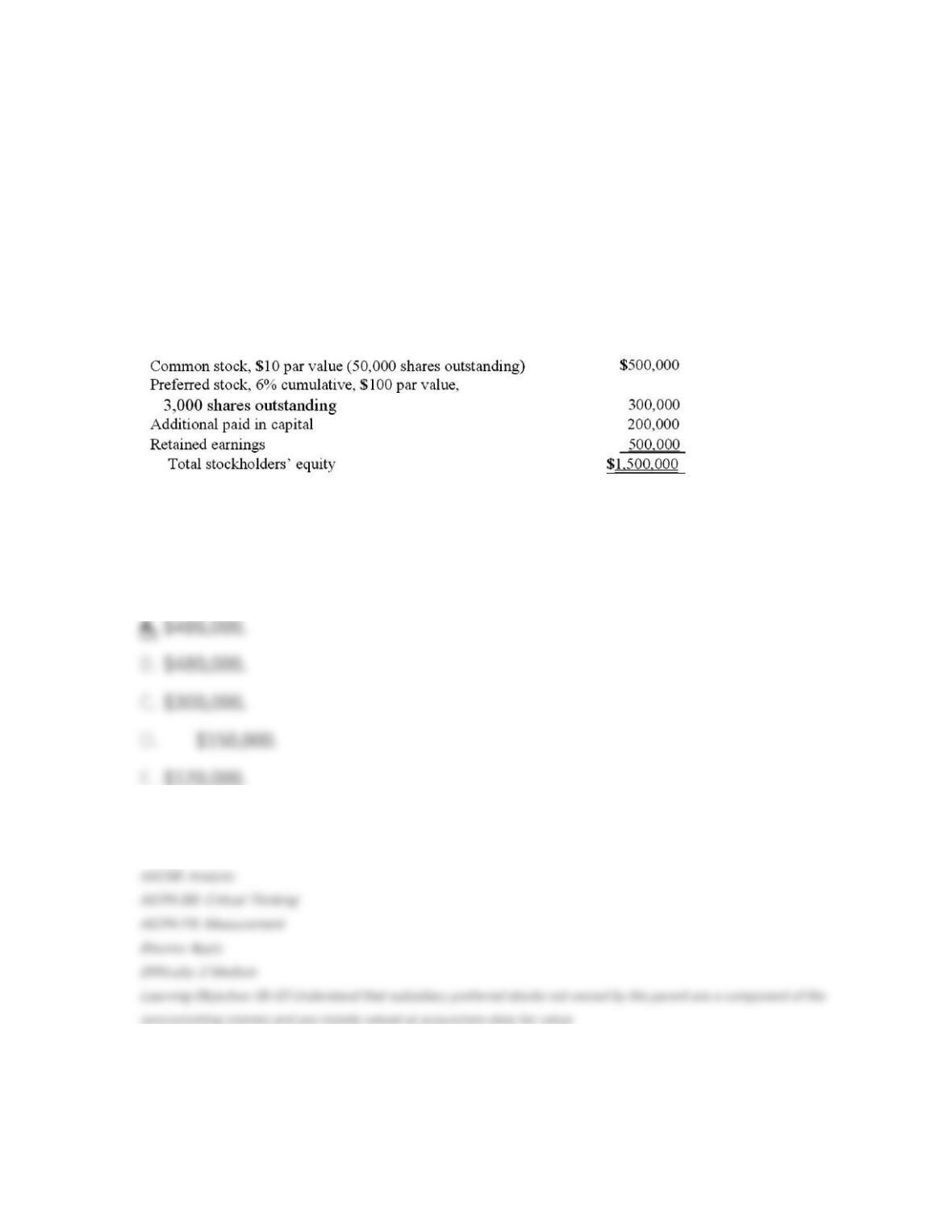

37. On January 1, 2009, Nichols Company acquired 80% of Smith Company’s

common stock and 40% of its non-voting, cumulative preferred stock. The

consideration transferred by Nichols was $1,200,000 for the common and

$124,000 for the preferred. Any excess acquisition-date fair value over book

value is considered goodwill. The capital structure of Smith immediately prior to

the acquisition is:

Compute the goodwill recognized in consolidation.

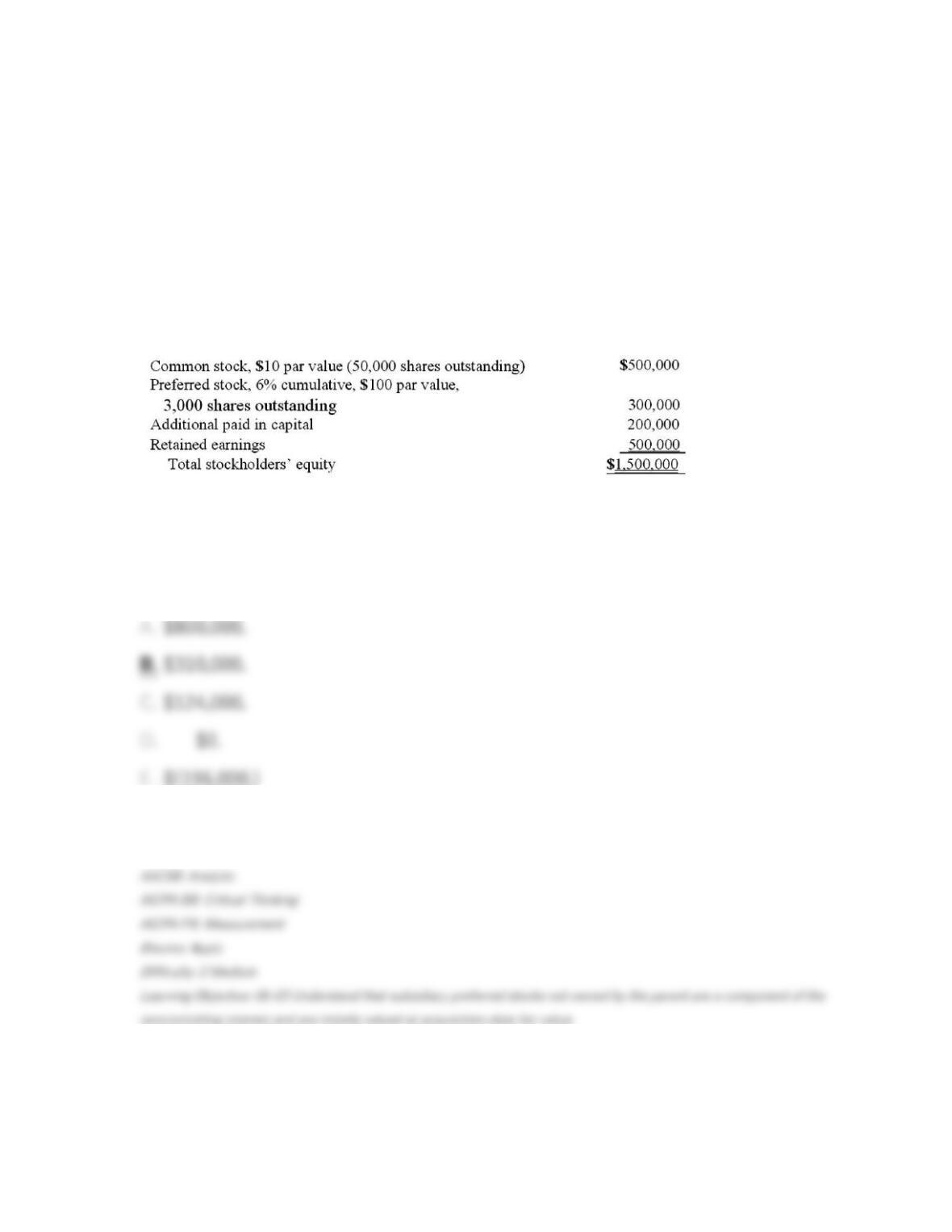

38. On January 1, 2009, Nichols Company acquired 80% of Smith Company’s

common stock and 40% of its non-voting, cumulative preferred stock. The

consideration transferred by Nichols was $1,200,000 for the common and

$124,000 for the preferred. Any excess acquisition-date fair value over book

value is considered goodwill. The capital structure of Smith immediately prior to

the acquisition is:

Compute the non-controlling interest in Smith at date of acquisition.

39. On January 1, 2009, Nichols Company acquired 80% of Smith Company’s

common stock and 40% of its non-voting, cumulative preferred stock. The

consideration transferred by Nichols was $1,200,000 for the common and

$124,000 for the preferred. Any excess acquisition-date fair value over book

value is considered goodwill. The capital structure of Smith immediately prior to

the acquisition is:

The consolidation entry at date of acquisition will include (referring to Smith):

40. On January 1, 2009, Nichols Company acquired 80% of Smith Company’s

common stock and 40% of its non-voting, cumulative preferred stock. The

consideration transferred by Nichols was $1,200,000 for the common and

$124,000 for the preferred. Any excess acquisition-date fair value over book

value is considered goodwill. The capital structure of Smith immediately prior to

the acquisition is:

If Smith’s net income is $100,000 in the year following the acquisition,

41. The following information has been taken from the consolidation

worksheet of Graham Company and its 80% owned subsidiary, Stage Company.

(1.) Graham reports a loss on sale of land of $5,000. The land cost Graham

$20,000.

(2.) Non-controlling interest in Stage’s net income was $30,000.

(3.) Graham paid dividends of $15,000.

(4.) Stage paid dividends of $10,000.

(5.) Excess acquisition-date fair value over book value was expensed by $6,000.

(6.) Consolidated accounts receivable decreased by $8,000.

(7.) Consolidated accounts payable decreased by $7,000.

How is the loss on sale of land reported on the consolidated statement of cash

flows?

42. The following information has been taken from the consolidation

worksheet of Graham Company and its 80% owned subsidiary, Stage Company.

(1.) Graham reports a loss on sale of land of $5,000. The land cost Graham

$20,000.

(2.) Non-controlling interest in Stage’s net income was $30,000.

(3.) Graham paid dividends of $15,000.

(4.) Stage paid dividends of $10,000.

(5.) Excess acquisition-date fair value over book value was expensed by $6,000.

(6.) Consolidated accounts receivable decreased by $8,000.

(7.) Consolidated accounts payable decreased by $7,000.

Where does the non-controlling interest in Stage’s net income appear on a

consolidated statement of cash flows?

43. The following information has been taken from the consolidation

worksheet of Graham Company and its 80% owned subsidiary, Stage Company.

(1.) Graham reports a loss on sale of land of $5,000. The land cost Graham

$20,000.

(2.) Non-controlling interest in Stage’s net income was $30,000.

(3.) Graham paid dividends of $15,000.

(4.) Stage paid dividends of $10,000.

(5.) Excess acquisition-date fair value over book value was expensed by $6,000.

(6.) Consolidated accounts receivable decreased by $8,000.

(7.) Consolidated accounts payable decreased by $7,000.

How will dividends be reported in consolidated statement of cash flows?

44. The following information has been taken from the consolidation

worksheet of Graham Company and its 80% owned subsidiary, Stage Company.

(1.) Graham reports a loss on sale of land of $5,000. The land cost Graham

$20,000.

(2.) Non-controlling interest in Stage’s net income was $30,000.

(3.) Graham paid dividends of $15,000.

(4.) Stage paid dividends of $10,000.

(5.) Excess acquisition-date fair value over book value was expensed by $6,000.

(6.) Consolidated accounts receivable decreased by $8,000.

(7.) Consolidated accounts payable decreased by $7,000.

How is the amount of excess acquisition-date fair value over book value

recognized in a consolidated statement of cash flows assuming the indirect

method is used?

45. The following information has been taken from the consolidation

worksheet of Graham Company and its 80% owned subsidiary, Stage Company.

(1.) Graham reports a loss on sale of land of $5,000. The land cost Graham

$20,000.

(2.) Non-controlling interest in Stage’s net income was $30,000.

(3.) Graham paid dividends of $15,000.

(4.) Stage paid dividends of $10,000.

(5.) Excess acquisition-date fair value over book value was expensed by $6,000.

(6.) Consolidated accounts receivable decreased by $8,000.

(7.) Consolidated accounts payable decreased by $7,000.

Using the indirect method, where does the decrease in accounts receivable

appear in a consolidated statement of cash flows?