1. On January 1, 2011, Riley Corp. acquired some of the outstanding bonds of

one of its subsidiaries. The bonds had a carrying value of $421,620, and Riley

paid $401,937 for them. How should you account for the difference between the

carrying value and the purchase price in the consolidated financial statements

for 2011?

2. Regency Corp. recently acquired $500,000 of the bonds of Safire Co., one of

its subsidiaries, paying more than the carrying value of the bonds. According to

the most practical view of this intra-entity transaction, to whom would the loss

be attributed?

3. Which one of the following characteristics of preferred stock would make

the stock a dilutive security for earnings per share?

4. Where do dividends paid to the non-controlling interest of a subsidiary

appear on a consolidated statement of cash flows?

5. Where do dividends paid by a subsidiary to the parent company appear in

a consolidated statement of cash flows?

6. Where do intra-entity sales of inventory appear in a consolidated

statement of cash flows?

7. How do intra-entity sales of inventory affect the preparation of a

consolidated statement of cash flows?

8. How would consolidated earnings per share be calculated if the subsidiary

has no convertible securities or warrants?

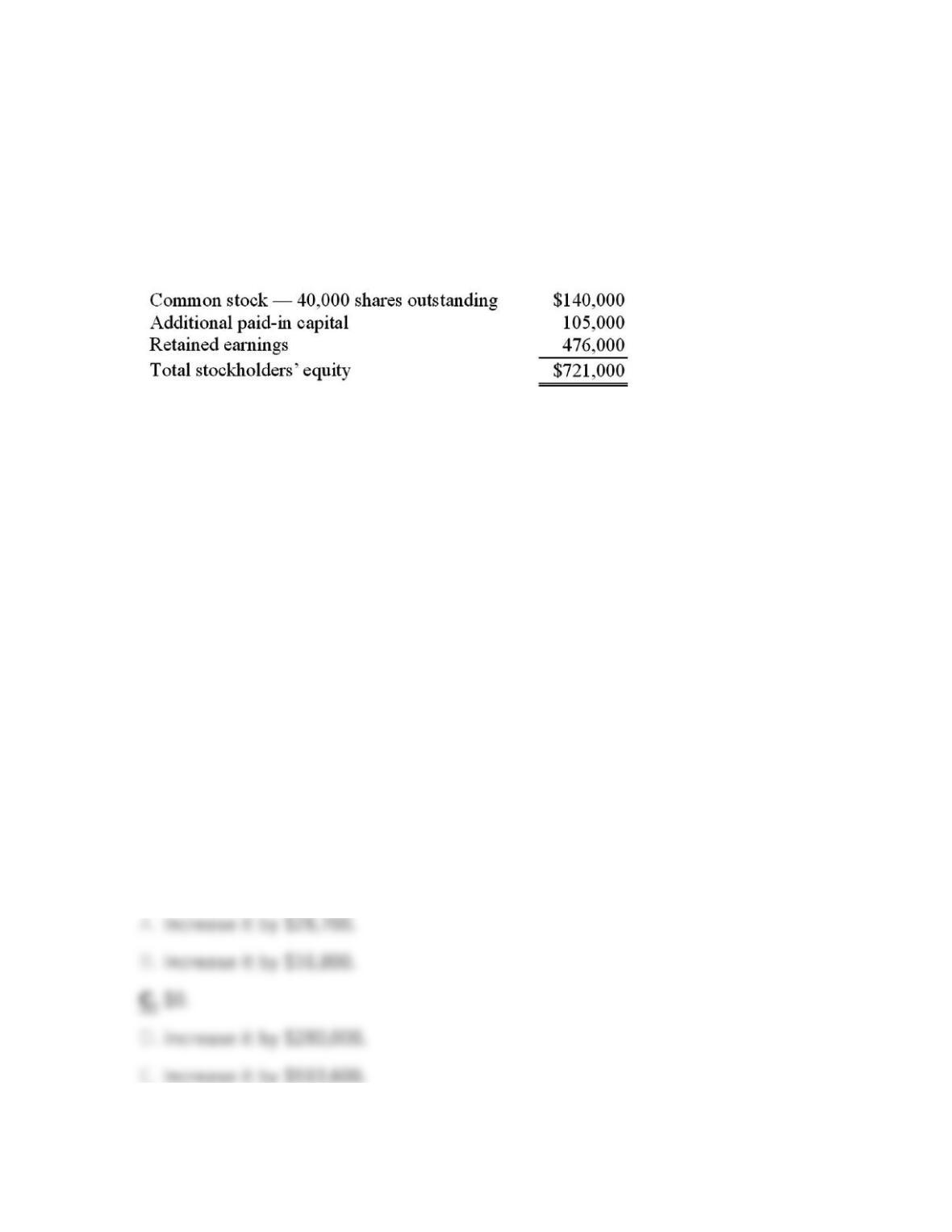

9. On January 1, 2011, Riney Co. owned 80% of the common stock of Garvin

Co. On that date, Garvin’s stockholders’ equity accounts had the following

balances:

The balance in Riney’s Investment in Garvin Co. account was $552,000, and the

non-controlling interest was $138,000. On January 1, 2011, Garvin Co. sold

10,000 shares of previously unissued common stock for $15 per share. Riney did

not acquire any of these shares.

What is the balance in Investment in Garvin Co. after the sale of the 10,000

shares of common stock?

10. On January 1, 2011, Riney Co. owned 80% of the common stock of Garvin

Co. On that date, Garvin’s stockholders’ equity accounts had the following

balances:

The balance in Riney’s Investment in Garvin Co. account was $552,000, and the

non-controlling interest was $138,000. On January 1, 2011, Garvin Co. sold

10,000 shares of previously unissued common stock for $15 per share. Riney did

not acquire any of these shares.

What is the balance in Non-controlling Interest in Garvin Co. after the sale of the

10,000 shares of common stock?

11. Rojas Co. owned 7,000 shares (70%) of the outstanding 10%, $100 par

preferred stock and 60% of the outstanding common stock of Brett Co. When

Brett reported net income of $780,000, what was the non-controlling interest in

the subsidiary’s income?

12. Knight Co. owned 80% of the common stock of Stoop Co. Stoop had

50,000 shares of $5 par value common stock and 2,000 shares of preferred stock

outstanding. Each preferred share received an annual per share dividend of $10

and is convertible into four shares of common stock. Knight did not own any of

Stoop’s preferred stock. Stoop also had 600 bonds outstanding, each of which is

convertible into ten shares of common stock. Stoop’s annual after-tax interest

expense for the bonds was $22,000. Knight did not own any of Stoop’s bonds.

Stoop reported income of $300,000 for 2011.

What was the amount of Stoop’s earnings that should be included in calculating

consolidated diluted earnings per share?

13. Knight Co. owned 80% of the common stock of Stoop Co. Stoop had

50,000 shares of $5 par value common stock and 2,000 shares of preferred stock

outstanding. Each preferred share received an annual per share dividend of $10

and is convertible into four shares of common stock. Knight did not own any of

Stoop’s preferred stock. Stoop also had 600 bonds outstanding, each of which is

convertible into ten shares of common stock. Stoop’s annual after-tax interest

expense for the bonds was $22,000. Knight did not own any of Stoop’s bonds.

Stoop reported income of $300,000 for 2011.

Stoop’s diluted earnings per share (rounded) is calculated to be

14. Campbell Inc. owned all of Gordon Corp. For 2011, Campbell reported net

income (without consideration of its investment in Gordon) of $280,000 while the

subsidiary reported $112,000. The subsidiary had bonds payable outstanding on

January 1, 2011, with a book value of $297,000. The parent acquired the bonds

on that date for $281,000. During 2011, Campbell reported interest income of

$31,000 while Gordon reported interest expense of $29,000. What is consolidated

net income for 2011?

15. Vontkins Inc. owned all of Quasimota Co. The subsidiary had bonds

payable outstanding on January 1, 2010, with a book value of $265,000. The

parent acquired the bonds on that date for $288,000. Subsequently, Vontkins

reported interest income of $25,000 in 2010 while Quasimota reported interest

expense of $29,000. Consolidated financial statements were prepared for 2011.

What adjustment would have been required for the retained earnings balance as

of January 1, 2011?

16. Tray Co. reported current earnings of $560,000 while paying $56,000 in

cash dividends. Sparrish Co. earned $140,000 in net income and distributed

$14,000 in dividends. Tray held a 70% interest in Sparrish for several years, an

investment that it originally acquired by transferring consideration equal to the

book value of the underlying net assets. Tray used the initial value method to

account for these shares.

On January 1, 2011, Sparrish acquired in the open market $70,000 of Tray’s 8%

bonds. The bonds had originally been issued several years ago at 92, reflecting a

10% effective interest rate. On the date of the bond purchase, the book value of

the bonds payable was $67,600. Sparrish paid $65,200 based on a 12% effective

interest rate over the remaining life of the bonds.

What is the non-controlling interest’s share of the subsidiary’s net income?

17. A company had common stock with a total par value of $18,000,000 and

fair value of $62,000,000; and 7% preferred stock with a total par value of

$6,000,000 and a fair value of $8,000,000. The book value of the company was

$85,000,000. If 90% of this company’s total equity was acquired by another, what

portion of the value would be assigned to the non-controlling interest?

18. Cadion Co. owned a controlling interest in Knieval Inc. Cadion reported

sales of $420,000 during 2011 while Knieval reported $280,000. Inventory costing

$28,000 was transferred from Knieval to Cadion (upstream) during the year for

$56,000. Of this amount, twenty-five percent was still in ending inventory at

year’s end. Total receivables on the consolidated balance sheet were $112,000 at

the first of the year and $154,000 at year-end. No intra-entity debt existed at the

beginning or ending of the year. Using the direct approach, what is the

consolidated amount of cash collected by the business combination from its

customers?

19. Parker owned all of Odom Inc. Although the Investment in Odom Inc

.

account had a balance of $834,000, the subsidiary’s 12,000 shares had an

underlying book value of only $56 per share. On January 1, 2011, Odom issued

3,000 new shares to the public for $70 per share. How does this transaction

affect the Investment in Odom Inc

.

account?

20. These questions are based on the following information and should be

viewed as

independent situations

.

Popper Co. acquired 80% of the common stock of Cocker Co. on January 1, 2009,

when Cocker had the following stockholders’ equity accounts.

To acquire this interest in Cocker, Popper paid a total of $682,000 with any

excess acquisition date fair value over book value being allocated to goodwill,

which has been measured for impairment annually and has not been determined

to be impaired as of January 1, 2012.

On January 1, 2012, Cocker reported a net book value of $1,113,000 before the

following transactions were conducted. Popper uses the equity method to

account for its investment in Cocker, thereby reflecting the change in book value

of Cocker.

On January 1, 2012, Cocker issued 10,000 additional shares of common stock for

$35 per share. Popper acquired 8,000 of these shares. How would this

transaction affect the additional paid-in capital of the parent company?

21. These questions are based on the following information and should be

viewed as

independent situations

.

Popper Co. acquired 80% of the common stock of Cocker Co. on January 1, 2009,

when Cocker had the following stockholders’ equity accounts.

To acquire this interest in Cocker, Popper paid a total of $682,000 with any

excess acquisition date fair value over book value being allocated to goodwill,

which has been measured for impairment annually and has not been determined

to be impaired as of January 1, 2012.

On January 1, 2012, Cocker reported a net book value of $1,113,000 before the

following transactions were conducted. Popper uses the equity method to

account for its investment in Cocker, thereby reflecting the change in book value

of Cocker.

On January 1, 2012, Cocker issued 10,000 additional shares of common stock for

$21 per share. Popper did not acquire any of this newly issued stock. How would

this transaction affect the additional paid-in capital of the parent company?

22. These questions are based on the following information and should be

viewed as

independent situations

.

Popper Co. acquired 80% of the common stock of Cocker Co. on January 1, 2009,

when Cocker had the following stockholders’ equity accounts.

To acquire this interest in Cocker, Popper paid a total of $682,000 with any

excess acquisition date fair value over book value being allocated to goodwill,

which has been measured for impairment annually and has not been determined

to be impaired as of January 1, 2012.

On January 1, 2012, Cocker reported a net book value of $1,113,000 before the

following transactions were conducted. Popper uses the equity method to

account for its investment in Cocker, thereby reflecting the change in book value

of Cocker.

On January 1, 2012, Cocker reacquired 8,000 of the outstanding shares of its own

common stock for $34 per share. None of these shares belonged to Popper. How

would this transaction have affected the additional paid-in capital of the parent

company?