Chapter 5: Sarbanes-Oxley, Internal Control, and Cash

76. Receipts from cash sales of $5,700 were recorded incorrectly by the depositor as $7,500. The

$1,800 difference would be included on the bank reconciliation as a(n):

a. addition to the cash balance per books.

b. addition to the cash balance per bank.

c. deduction from the cash balance per bank.

d. deduction from the cash balance per books.

77. Receipts from cash sales of $7,500 were recorded incorrectly by the depositor as $5,700. What

adjustment is required in the bank’s accounts?

a. Decrease Sales; decrease Cash

b. Increase Cash; decrease Accounts Receivable

c. Increase Cash; increase Sales

d. No adjustment needed

78. Accompanying the bank statement was a credit memorandum for a short-term note collected

by the bank for the depositor. This item would be included on the bank reconciliation as a(n):

a. deduction from the cash balance per books.

b. addition to the cash balance per bank.

c. deduction from the cash balance per bank.

d. addition to the cash balance per books.

79. Accompanying the bank statement was a credit memorandum for a short-term note collected

by the bank for the customer. What adjustment is required in the depositor’s accounts?

a. Increase Notes Receivable; decrease Cash

b. Increase Cash; increase Miscellaneous Income

c. Increase Cash; decrease Notes Receivable

d. Increase Accounts Receivable; decrease Cash

80. The amount of the outstanding checks is included on the bank reconciliation as a(n):

a. deduction from the cash balance per books.

b. addition to the cash balance per bank.

c. deduction from the cash balance per bank.

d. addition to the cash balance per books.

Chapter 5: Sarbanes-Oxley, Internal Control, and Cash

81. What adjustment is required in the depositor’s accounts to record outstanding checks?

a. None

b. Increase Cash; decrease Accounts Receivable

c. Increase Cash; increase Accounts Payable

d. Increase Accounts Receivable; decrease Cash

82. Accompanying the bank statement was a debit memorandum for an NSF check received from

a customer. This item would be included on the bank reconciliation as a(n):

a. deduction from the cash balance per books.

b. addition to the cash balance per bank.

c. deduction from the cash balance per bank.

d. addition to the cash balance per books.

83. A check drawn by a depositor for $810 in payment of a liability was recorded by the depositor

as $180. The $630 difference would be included on the bank reconciliation as a(n):

a. addition to the cash balance per books.

b. addition to the cash balance per bank.

c. deduction from the cash balance per bank.

d. deduction from the cash balance per books.

84. The amount of deposits in transit is included on the bank statement as a(n):

a. deduction from the cash balance per books.

b. deduction from the cash balance per bank.

c. addition to the cash balance per bank.

d. addition to the cash balance per books.

85. Accompanying the bank statement was a debit memorandum for an NSF check received from

a customer. This item would require an adjusting entry including a:

a. debit to Accounts Receivable.

b. debit to Cash.

c. debit to Accounts Payable.

d. credit to Accounts Payable.

Chapter 5: Sarbanes-Oxley, Internal Control, and Cash

86. Which of the following would be deducted from the cash balance per books on a bank

reconciliation?

a. Service charges

b. Outstanding checks

c. Deposits in transit

d. Notes collected by the bank

87. Which of the following would be added to the cash balance per books on a bank

reconciliation?

a. Service charges

b. Outstanding checks

c. Deposits in transit

d. Notes collected by the bank

88. A special cash fund used to make small payments that occur frequently is called a(n):

a. operating expenses fund.

b. change fund.

c. market fund.

d. petty cash fund.

89. Which of the following should be considered as cash by an accountant?

a. Money orders

b. Corporate bonds

c. Postage stamps

d. Government bonds

90. Cash equivalents include:

a. checks.

b. coins and currency.

c. money market funds and commercial paper.

d. stocks and short-term bonds.

Chapter 5: Sarbanes-Oxley, Internal Control, and Cash

91. A minimum cash balance required by a bank is called:

a. cash in bank.

b. compensating balance.

c. average balance.

d. adjusted balance.

92. The ratio of cash to monthly cash expenses can be used to .

a. assess how long a company with positive cash flows from investing activities can continue

to operate

b. assess how long a company with negative cash flows from operations can continue to

operate

c. assess how long a company with negative cash flows from investing activities can continue

to operate

d. assess how long a company with positive cash flows from financing activities can continue

to operate

93. The ratio of cash to monthly cash expenses is computed as .

a. monthly cash expenses divided by cash

b. current assets divided by monthly cash expenses

c. cash divided by cash equivalents

d. cash and cash equivalents divided by monthly cash expenses

94. Denominator in the ratio of cash to monthly cash expense is calculated as .

a. total revenues divided by 12

b. net cash flows from investing activities divided by 12

c. earnings before taxes divided by 12

d. net cash flows from operations divided by 12

95. A primary cause of failure of new companies is that .

a. they don’t have sufficient cash from debt or equity financing to operate long enough to

generate positive cash flows from operations

b. they don’t have sufficient cash to operate long enough to generate positive cash flows from

financing activities

c. they pay double taxation

d. the occurrence of fraud is higher in such companies

Chapter 5: Sarbanes-Oxley, Internal Control, and Cash

96. When a company reports negative net cash flows from operations .

a. ratio of equity to annual cash expenses helps in assessing the survival of the company

b. ratio of equity to monthly cash expenses helps in assessing the survival of the company

c. ratio of cash to monthly cash expenses helps in assessing the survival of the company

d. ratio of accounts payable to annual financing expenses helps in assessing the survival of the

company

97. List the objectives of internal control and give an example of how each is implemented.

98. For each of the following procedures, indicate whether it is an internal control strength or a

weakness. Also, for each weakness, explain why it is a weakness and how it can be corrected.

(a) Only the best accounting graduates are hired to eliminate the need for training.

(b) The person responsible for ordering and receiving supplies is not permitted to record or

pay for the supplies.

(c) Company policy mandates that all employees take vacation time.

(d) Internal auditors constantly monitor the internal control system.

(e) The accountant deposits cash at least once each day to prevent holding large amounts of

cash on hand.

Chapter 5: Sarbanes-Oxley, Internal Control, and Cash

99. List and define each of the five elements of internal control set forth by the Integrated

Framework.

100. Describe the features of a voucher system and list typical supporting documents for a voucher.

101. List the advantages of Electronic Funds Transfers.

Chapter 5: Sarbanes-Oxley, Internal Control, and Cash

102. Using the following information, prepare a bank reconciliation for Hydrope Co. for May 31,

2015.

(a) The bank statement balance is $3,712.

(b) The cash account balance is $3,790.

(c) Outstanding checks amounted to $850.

(d) Deposits in transit are $845.

(e) The bank service charge is $45.

(f) Interest added to the checking account by the bank is $15.

(g) A check drawn for $45 was incorrectly charged by the bank as $98.

103. Using the following information, list the items that will require adjustments to the accounts of

Salem Co. Also, indicate which accounts will increase or decrease due to the adjustment.

(a) The bank statement balance is $2,597.

(b) The cash account balance is $2,680.

(c) Outstanding checks amounted to $703.

(d) Deposits in transit are $732.

(e) The bank service charge is $25.

(f) Interest added to the checking account by the bank is $7.

(g) A check drawn for $59 was incorrectly charged by the bank as $95.

Chapter 5: Sarbanes-Oxley, Internal Control, and Cash

104. The bank statement for Exible Co. indicates a balance of $10,252.50 on June 30, 2015. The

cash account for the company had a balance of $4,787.10. Prepare a bank reconciliation on the

basis of the following reconciling items:

(a) Cash sales of $351 had been erroneously recorded as $315.

(b) Deposits in transit not recorded by bank, $500.

(c) Bank debit memorandum for service charges, $45.

(d) Bank credit memorandum for note collected by bank, $2,782, including $63 interest.

(e) Bank debit memorandum for $223.40 NSF (not sufficient funds) check from Alice

Martin, a customer.

(f) Checks outstanding, $3,415.80.

Chapter 5: Sarbanes-Oxley, Internal Control, and Cash

105. The bank statement for Marley Co. indicates a cash balance of $10,000.50 on June 30, 2015.

The cash account in Marley’s records had a balance of $4,677.10. Illustrate the adjustments to

the accounts and their effect on Marley’s financial statements, based on the following

reconciling items:

(a) Cash sales of $342 had been erroneously recorded in the cash receipts journal as $324.

(b) Deposits in transit not recorded by bank, $700.

(c) Bank debit memorandum for service charges, $30.

(d) Bank credit memorandum for note collected by bank, $2,050, including $50 interest.

(e) Bank debit memorandum for $207.40 NSF (not sufficient funds) check from Alice

Martin, a customer.

(f) Checks outstanding, $4,192.80.

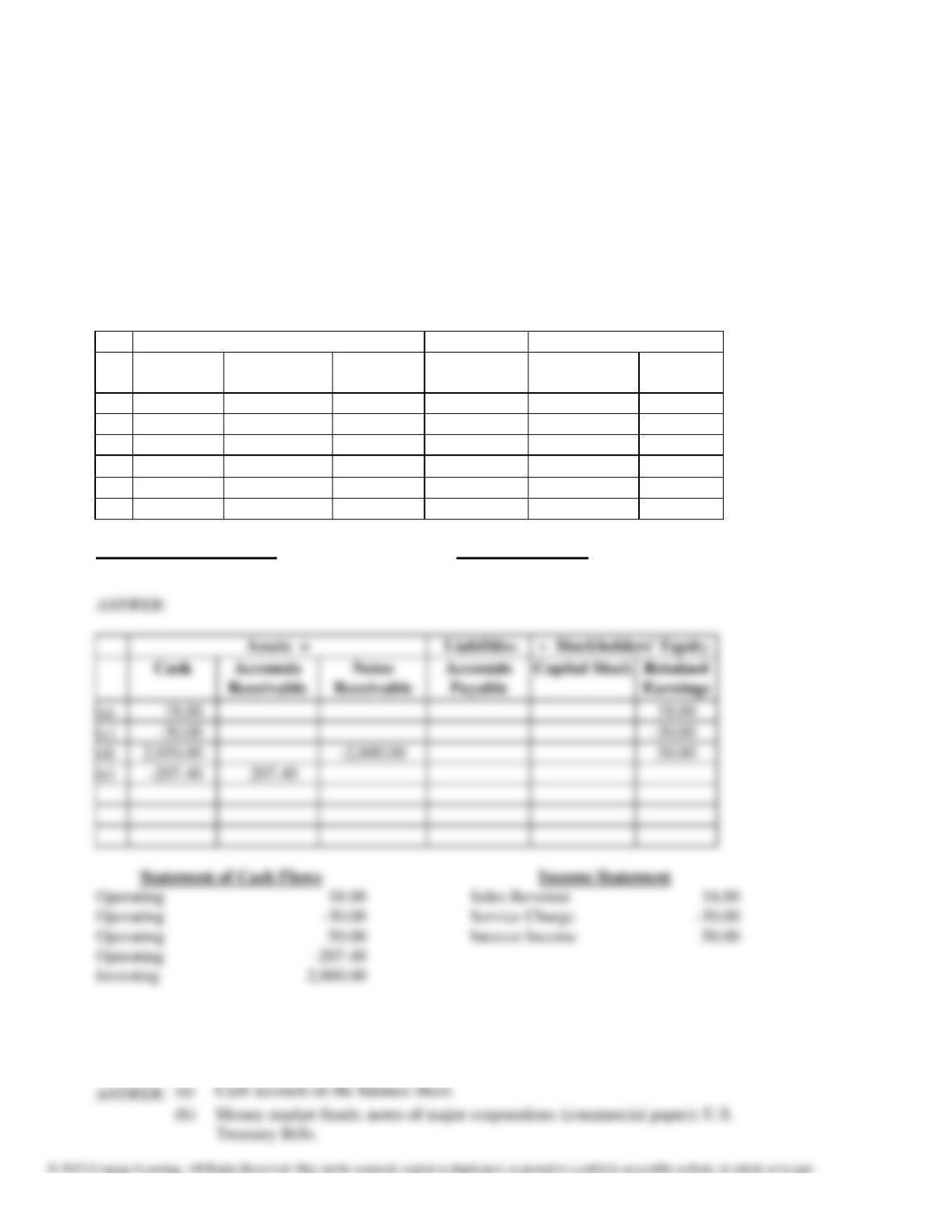

Assets =

Liabilities

+ Stockholders‘ Equity

Cash

Accounts

Receivable

Notes

Receivable

Accounts

Payable

Capital Stock

Retained

Earnings

Statement of Cash Flows Income Statement

(a)

(c)

(d)

(e)

106.

(a) Where are cash equivalents disclosed in the financial statements?

(b) List three examples of cash equivalents.

Chapter 5: Sarbanes-Oxley, Internal Control, and Cash

107. Why would a bank require a company to maintain a compensating balance?

108. What is the purpose of the Sarbanes-Oxley Act of 2002, and why was it enacted?

109. Discuss what would be included under personnel policies.

110. Explain why one person should not be permitted to purchase, receive, and pay for supplies.

111. What is a special-purpose cash fund? What is its purpose? Give two examples.

112. Identify each of the following as related to (a) the control environment, (b) risk assessment, or

(c) control procedures.

(1) Mandatory vacations

(2) Personnel policies

(3) Report of outside consultants on future market changes

Chapter 5: Sarbanes-Oxley, Internal Control, and Cash

113. Using the following information, prepare a bank reconciliation for Murack Co. for May 31,

2015:

(a) The bank statement balance is $4,063.

(b) The cash account balance is $3,735.

(c) Outstanding checks amounted to $640.

(d) Deposits in transit are $245.

(e) The bank service charge is $40.

(f) A check for $74 for supplies was recorded on the depositor’s books as $47.