86.

Refer to the information above. After closing the accounts, Retained Earnings at December

31 equals:

87.

Refer to the information above. The total debits in the After-Closing Trial Balance will

equal:

88.

Which account will appear on an After-Closing Trial Balance?

89.

Which account will

not

appear on an After-Closing Trial Balance?

90.

Which account appears on the After-Closing Trial Balance?

91.

Return on equity measures:

92.

Return on equity is calculated by:

93.

If current assets are $90,000 and current liabilities are $70,000, the current ratio will be:

94.

If current assets are $110,000 and current liabilities are $50,000, working capital will be:

95.

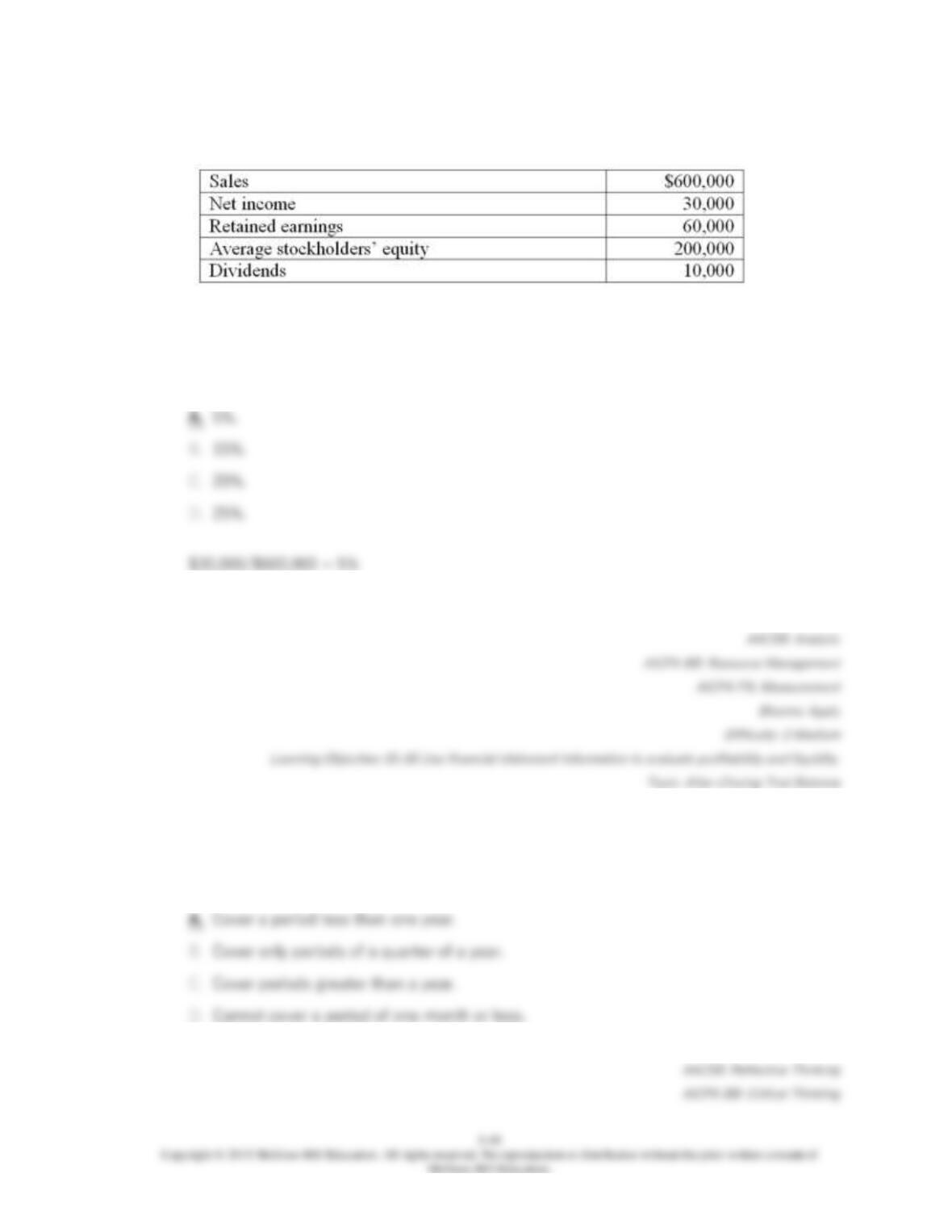

The following information is available:

What is the return on equity? (round to the nearest number)

96.

If current assets are $180,000 and current liabilities are $130,000, the current ratio will be:

97.

If current assets are $180,000 and current liabilities are $130,000, working capital will be:

98.

The following information is available:

What is the return on equity? (round to the nearest number)

99.

The following information is available:

What is the net income percentage? (round to the nearest number)

100.

Interim financial statements:

101.

Preparation of interim financial statements:

102.

If monthly financial statements are desired by management:

103.

The section of the annual report titled “Management Discussion and Analysis” is:

104.

A worksheet consists of all of the following

except

:

105.

When a worksheet is prepared, which account would

not

be entered into the income

statement columns?

106.

The worksheet:

107.

Which of the following amounts appears in both the Income Statement debit column and

the Balance Sheet credit column of a worksheet?

108.

A worksheet should be viewed as:

109.

The amount of net income (or loss) will appear on the debit side of the Income Statement

columns in a worksheet if:

110.

Which of the following is true regarding a worksheet prepared at year-end?

111.

When a worksheet is used:

112.

Only two adjustments appear in the adjustments column of a worksheet for Wycliff

Publications: one to record $800 depreciation of office equipment and the other to record

the use of $560 of office supplies. If the Trial Balance column totals are $15,380, what are

the totals of the Adjusted Trial Balance columns?

113.

The December 31, 2014 worksheet for Fran’s Fine Dining showed the following amounts

related to the Supplies Expense account:

(a). In the Trial Balance debit column: $745

(b). In the Adjustments debit column: $125

(c). In the Adjusted Trial Balance debit column: $870

What is the proper balance in the Supplies Expense account on January 1, 2015, after all

closing entries for 2014 have been posted, but before any 2015 transactions are

recorded?

114.

Only two adjustments appear in the adjustments column of a worksheet for Winona Mfg:

one to record $8,000 depreciation of factory equipment, and the other to record the use of

$1,500 of prepaid insurance. If the Trial Balance column totals are $145,380, what are the

totals of the Adjusted Trial Balance columns?

5-59

115.

The December 31, 2014 worksheet for Albertville Grill showed the following amounts

related to the Depreciation Expense account:

(a). In the Trial Balance debit column: $1,745

(b). In the Adjustments debit column: $1,125

(c). In the Adjusted Trial Balance debit column: $1,870

What is the proper balance in the Depreciation Expense account on January 1, 2015, after

all closing entries for 2014 have been posted, but before any 2015 transactions are

recorded?

Essay Questions

5-60

116.

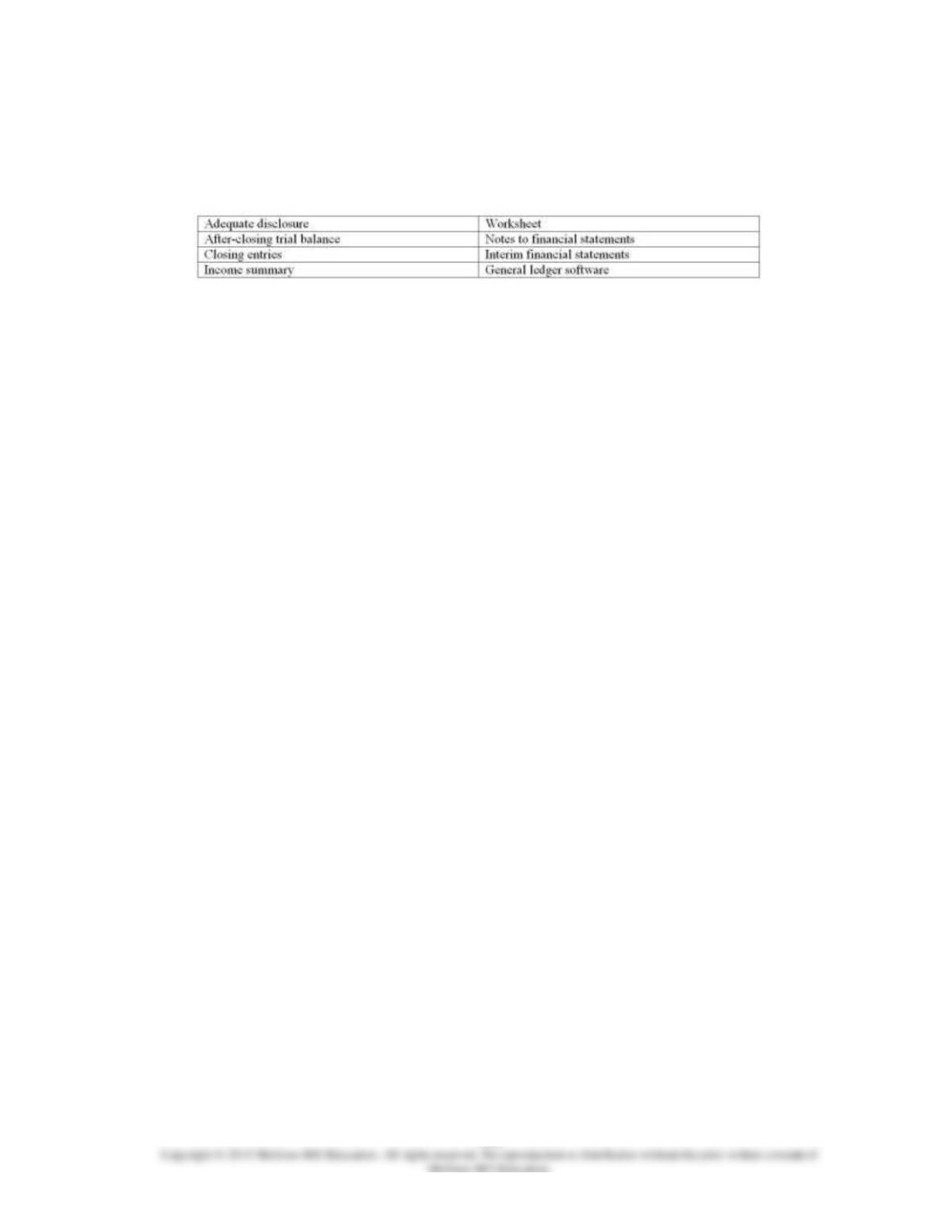

Accounting terminology

Listed below are eight technical accounting terms emphasized in this chapter:

In the space provided for each statement, indicate the accounting term described.

______ a. The generally accepted accounting principle of providing with financial

statements any information that users need to interpret those statements properly.

______ b. A trial balance prepared after all closing entries have been posted. This trial

balance consists only of accounts for assets, liabilities, and owners’ equity.

______ c. Journal entries made at the end of the period for the purpose of closing

temporary accounts (revenue, expense, and dividend accounts) and transferring balances

to the Retained Earnings account.

______ d. Computer software used for recording transactions, maintaining journals and

ledgers, and preparing financial statements. Also includes spreadsheet capabilities for

showing the effects of proposed adjusting entries or transactions on the financial

statements without actually recording these entries in the accounting records.

______ e. The summary account in the ledger to which revenue and expense accounts are

closed at the end of the period. The balance (credit balance for a net income, debit

balance for a net loss) is transferred to the Retained Earnings account.

______ f. Financial statements prepared for periods of less than one year (includes

monthly and quarterly statements).

______ g. Supplemental disclosures that accompany financial statements. They provide

users with various types of information considered necessary for the proper interpretation

of the statements.

______ h. A multicolumn schedule showing the relationships among the current account

balances (a trial balance), proposed or actual adjusting entries or transactions, and the

financial statements that would result if these adjusting entries or transactions were

recorded. Used both at the end of the accounting period as an aid to preparing financial

statements and for planning purposes.